Dzmitry Dzemidovich/iStock via Getty Images

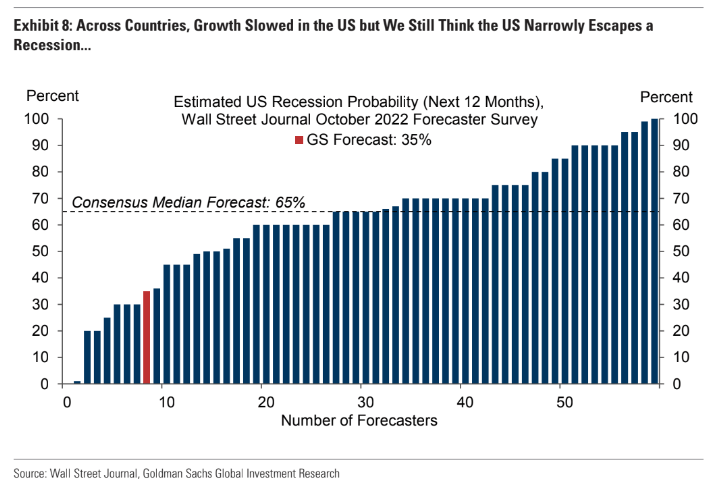

2023 recession risks are front and center. According to Goldman Sachs, the current consensus median recession forecast chance is high at 65%. While Goldman sees the domestic economy sidestepping significant contraction next year, many cyclical, consumer, and housing-related stocks might be particularly at risk.

One REIT had a bearish earnings preannouncement in October and features a dicey chart. But is there value in shares of New York Mortgage Trust (NASDAQ:NYMT) given its juicy yield? Let’s investigate.

Recession Risk Ahead

Goldman Sachs Investment Research

According to Bank of America Global Research, New York Mortgage Trust (NYMT) is an internally managed mREIT that invests in residential mortgage loans, Agency RMBS, and multi-family commercial mortgage-backed securities, as well as mezzanine loans and preferred equity investments. NYMT’s objective is to deliver long-term, stable distributions to stockholders over a range of economic conditions through a combination of net interest margin and capital gains. The portfolio is actively managed to maintain dividend and book value stability.

The New York-based $1.0 billion market cap Mortgage Real Estate Investment Trusts (REITs) industry company within the Financial sector does not have positive trailing 12-month GAAP earnings and pays a high 15.6% dividend yield, according to The Wall Street Journal.

The firm declared another $0.10 dividend back on December 12 and recently promoted Nicholas Mah to the role of president. This comes as troubling trends in the real estate and capital markets rattle so many REITs. Redfin recently forecasted home sales to drop in 2023. Not surprisingly, NYMT issued an earnings miss along with a weak total net interest income figure back in early November. The firm preannounced preliminary earnings for Q3 in mid-October, reporting a book value per share drop of 8.5%.

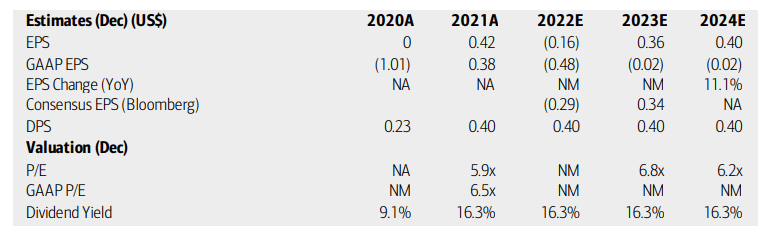

On valuation, analysts at BofA see operating earnings turning into the black in 2023 after a negative 2022 print. GAAP per-share profits will likely remain negative, though. The Bloomberg consensus forecast is about on par with what BofA sees. Dividends are expected to remain at an annual run rate of $0.40 while the operating P/E turns decent in the years ahead, but macro risks make that outlook uncertain. With a bleak housing market and a high chance of a recession next year, I continue to be somewhat cautious on the name.

New York Mortgage Trust: Earnings, Valuation, Dividend Forecasts

BofA Global Research

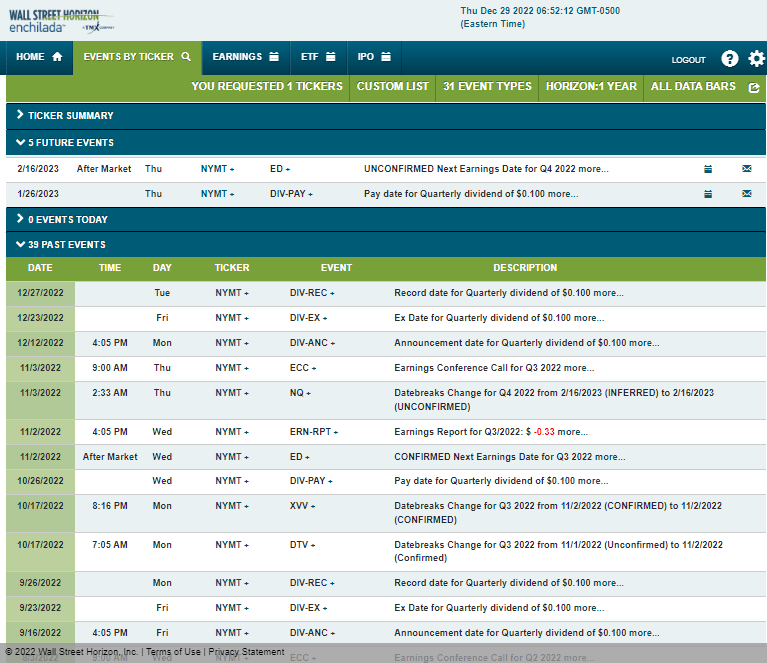

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Thursday, February 16. Before that, NYMT has a dividend pay date of January 26. The calendar is light on volatility catalysts in the near term.

Corporate Event Calendar

Wall Street Horizon

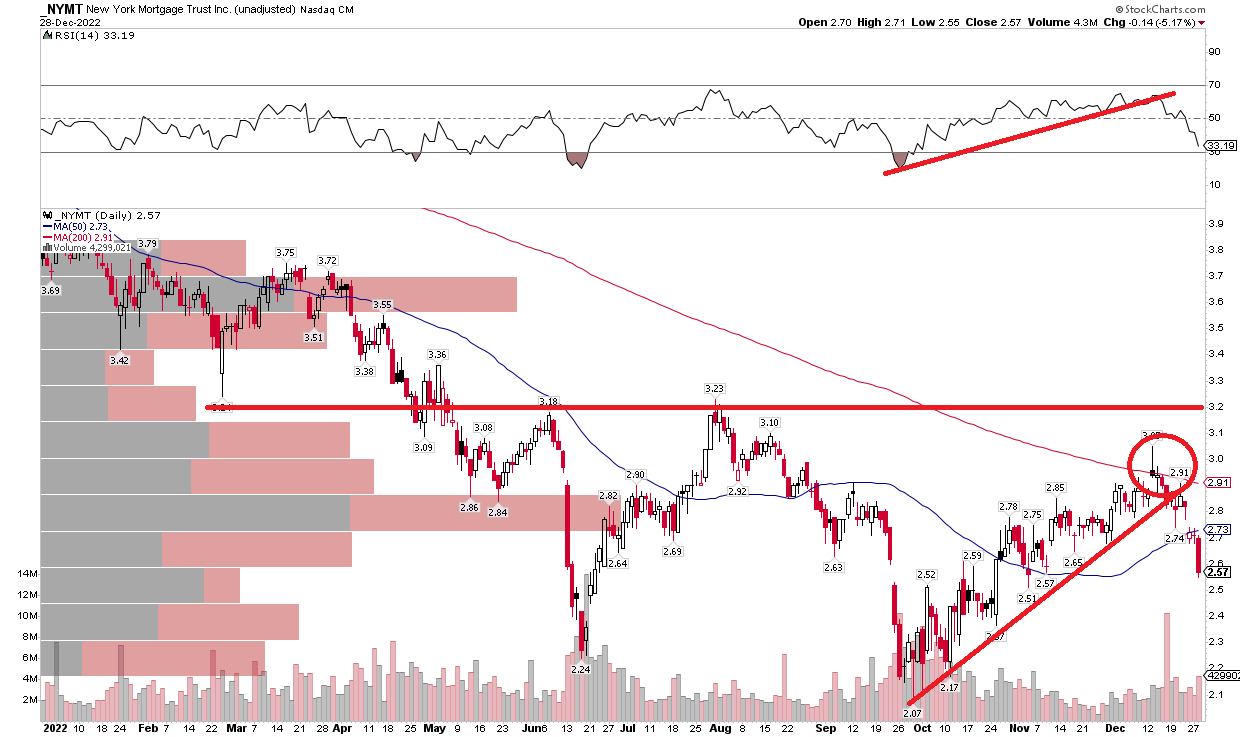

The Technical Take

I was a hold on NYMT back in the summer as the stock had appeared to put in a decent-looking bottom in June. The $2.24 nadir was violated on high volume during a September plunge, and after a strong rally back to its falling 200-day moving average, the shares have taken a significant leg lower lately. Notice in the chart below that the stock has broken its uptrend line and RSI has also fallen from a nice rise – so momentum is confirming price action. I see longer-term resistance near $3.20. Ultimately, more downside may be ahead for the stock. I would turn more optimistic on a move above the 200-day and the $3.20 to $3.30 area.

NYMT: Shares Break the Uptrend, Could Challenge the September Low

StockCharts.com

The Bottom Line

With an uncertain macro outlook and valuation, NYMT should be avoided right now. A bearish chart is another risk to weigh for shorter-term traders.

Be the first to comment