Adrian Wojcik/iStock via Getty Images

While most gold and silver producers have seen outperformance from the recent surge in precious metals prices, one breed of companies has also been a significant beneficiary. This group is gold and copper producers like New Gold (NYSE:NGD), Evolution Mining (OTCPK:CAHPF), and K92 Mining (OTCQX:KNTNF). In New Gold’s case, it may not have industry-leading growth like K92 Mining (300% production growth from 2023 to 2027) but it has all of its production coming from Canada and operates a copper-gold block cave operation at New Afton which is on track for significant growth once the C-Zone ramps to full capacity. Simultaneously, costs are set to improve materially at its Rainy River Mine in Ontario, setting up exponential growth in free cash flow post-2024.

Rainy River Operations – Company Website

In this update, we’ll dig into New Gold’s FY2023 results, recent developments, and where the stock’s updated buy zone lies:

Q4 & FY2023 Results

New Gold was one of the first companies to release its Q4 and FY2023 results and saw a significant improvement in sales, margins, and cash flow on a year-over-year basis. This was driven by higher gold prices and a much stronger quarter from its New Afton Mine (British Columbia) which produced ~40,800 gold-equivalent ounces [GEOs], a ~54% increase from the year-ago period. The sharp increase in production was related to increased throughput (~761,000 tonnes processed) at much higher copper and gold grades, plus a 400 basis point increase in recovery rates for both metals. Meanwhile, although production was down at Rainy River, this was largely because of lapping difficult year-over-year comparisons.

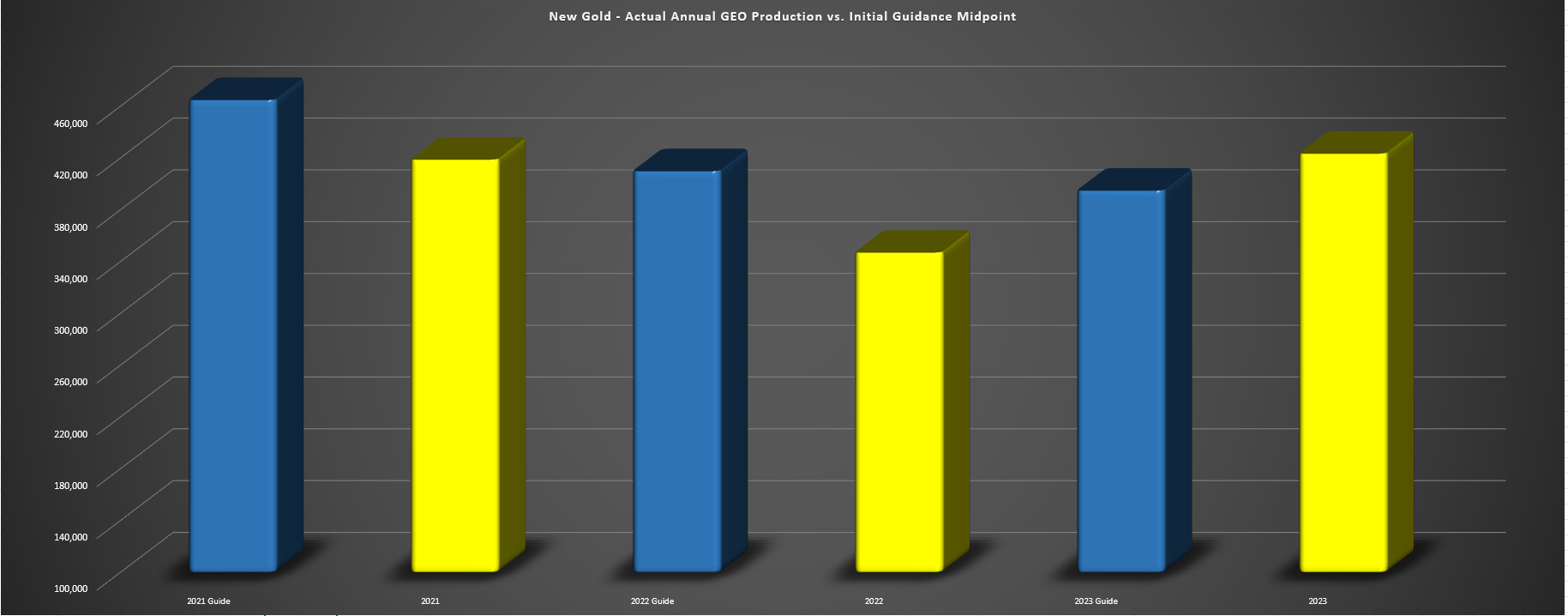

New Gold Actual Annual GEO Production vs. Initial Guidance Midpoint – Company Filings, Author’s Chart New Gold Quarterly GEO Production & Revenue – Company Filings, Author’s Chart

Looking at the full-year results, New Gold was one of the few producers to trounce its FY2023 production estimates, reporting full-year production of ~423,500 GEOs at all-in sustaining costs of $1,545/oz. This translated to a 7% plus beat vs. its initial guidance mid-point of 395,000 GEOs, a ~15% decline in operating costs and helped New Gold to report significant year-over-year revenue growth of 30% (~$787 million vs. ~$604 million). And while this was partially because of being up against easy comparisons from FY2022, revenue was also up materially on a two-year basis (+5%) given the higher average realized gold price. However, while the average realized gold and copper price of $1,944/oz and $3.84/lb helped the FY2023 results, things are looking dramatically better just four months into 2024. Let’s take a look below.

2024 Outlook

As for New Gold’s 2024 outlook, its Rainy River Mine is expected to have a better year, benefiting from higher throughput and slightly higher gold grades, with the mine expected to produce 265,000 ounces at the mid-point. The bulk of this production will be back-end weighted with significantly lower costs in H2 vs. H1, benefiting from lower sustaining capital and a significant increase in gold sales. However, the real growth in production and free cash flow from this asset will begin in 2025, with its gold production set to increase to ~320,000 ounces next year at more competitive operating costs (sub $1,250/oz AISC), with further growth in 2026. At the same time, Rainy River is expected to see a material decline in capital expenditures with reduced capitalized stripping, setting this asset up to be a free cash flow machine after what was a much less impressive first decade of operations than initially forecasted by New Gold during project construction.

Rainy River Presentation & Production/Cost Projections – 2015 Presentation

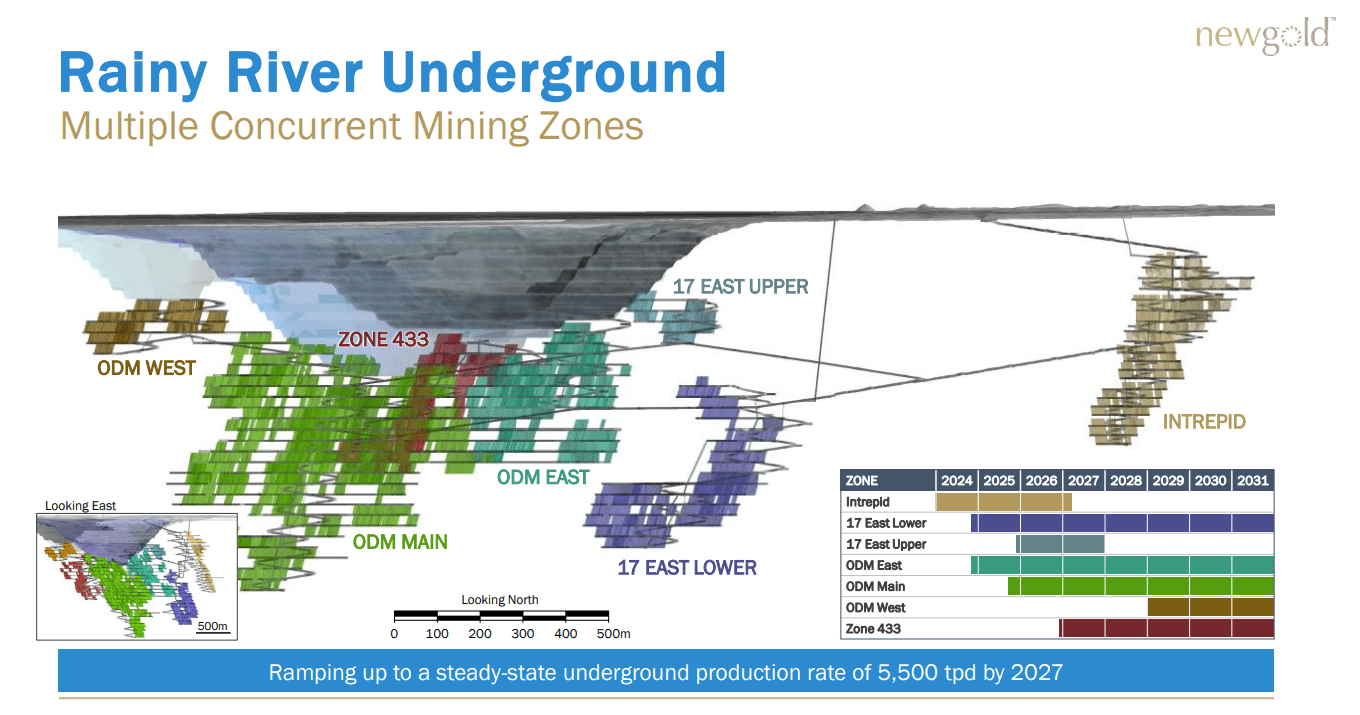

While Rainy River has undoubtedly been a disappointment relative to projections, New Gold has a far stronger team in place currently and has done an impressive job of over-delivering on promises under new CEO Patrick Godin. In addition, Rainy River is now moving into its most profitable five-year period of its mine life and thanks to a higher gold price, it actually generated free cash flow last year during a period of higher growth capital as the company works on completing underground development. And as for development progress, underground development of the Main Zone remains on schedule, with the first ore from the underground Main Zone on track for Q4 of this year. The result is another a further reduction in all-in sustaining costs this year, with a further improvement in 2025.

Rainy River Underground Schedule – Company Website

While the outlook at Rainy River is looking much better, New Afton’s future is even more impressive. This is because the asset is set to see further growth in output in 2024 ahead of what will be a massive increase in gold production in 2026 at industry-leading costs, with gold production set to increase to ~100,000 ounces while copper production increases to ~76 million pounds. If successful, these figures would represent a near doubling of copper output and ~60% increase in gold production from last year’s levels, with a surge in free cash flow given that block caves are very capital intensive upfront but extremely low cost to operate relative to other underground mining methods and with modest sustaining capital once in production (crusher and conveyor set to be complete in H2-2024). And with higher grades on deck in 2026 from the much-awaited C-Zone combined with a very favorable supply/demand outlook for copper, it’s finally a great time to be a New Gold shareholder, never mind the exploration upside at this growing copper-gold asset.

New Afton C-Zone & Exploration Upside – Company Presentation

Putting it all together, New Gold expects to see ~3% growth in gold production year-over-year at the mid-point (330,000 ounces vs. 321,000 ounces) and ~16% growth in copper production as we see a ramp up in mining from the C-Zone this year. As for costs, we should see all-in sustaining costs per gold ounce net of by-product credits decline to $1,300/oz or lower, a nearly 10% decline year-over-year. So, what does this mean for free cash flow generation?

An Improved Free Cash Flow Outlook

While New Gold has struggled to consistently generate free cash flow over the past few years despite a rising gold price, like many of its smaller peers (FY2023 free cash flow: [-] $17 million), the company is finally set to see the fruits of its labor after years of investment. And while some of this timing was certainly luck, the company couldn’t have picked a better time to ramp up production at both of its mines given that gold and copper prices are both sitting at multi-year and/or all-time highs. This is certainly an exciting development for patient investors and while the company will see relatively modest free cash flow generation this year, it could see cumulative free cash flow of $700+ million in 2025 and 2026, translating to half of the company’s current enterprise value. In fact, free cash flow could easily exceed this figure if gold/copper remains at/above their current levels.

New Gold Annual Operating Cash Flow & Free Cash Flow – Company Filings, Author’s Chart

In an industry where free cash flow is king, the outlook for New Gold has never been better and its improved balance sheet strength could allow it to buy back its Ontario Teachers’ Pension Plan free cash flow interest which has now reached its four-year anniversary with the $300 million partnership at New Afton announced in Q1 2020. In addition, New Gold could look at strategic acquisitions to potentially diversify its production profile further and/or ramp up exploration aggressively and aim to further extend the mine lives of its assets. Finally, assuming NGD continues to trade at a significant discount to fair value, buying back shares could be an option as well to improve its per share metrics after significant share dilution in 2019 under prior management.

And while the designated home for this growing cash pile assuming it executes successfully is not yet clear, the improved commodity price outlook has made it possible to pursue multiple options over the next few years, including a larger exploration budget, debt paydown, repurchasing the free cash flow interest and also a dividend or share buybacks.

Valuation

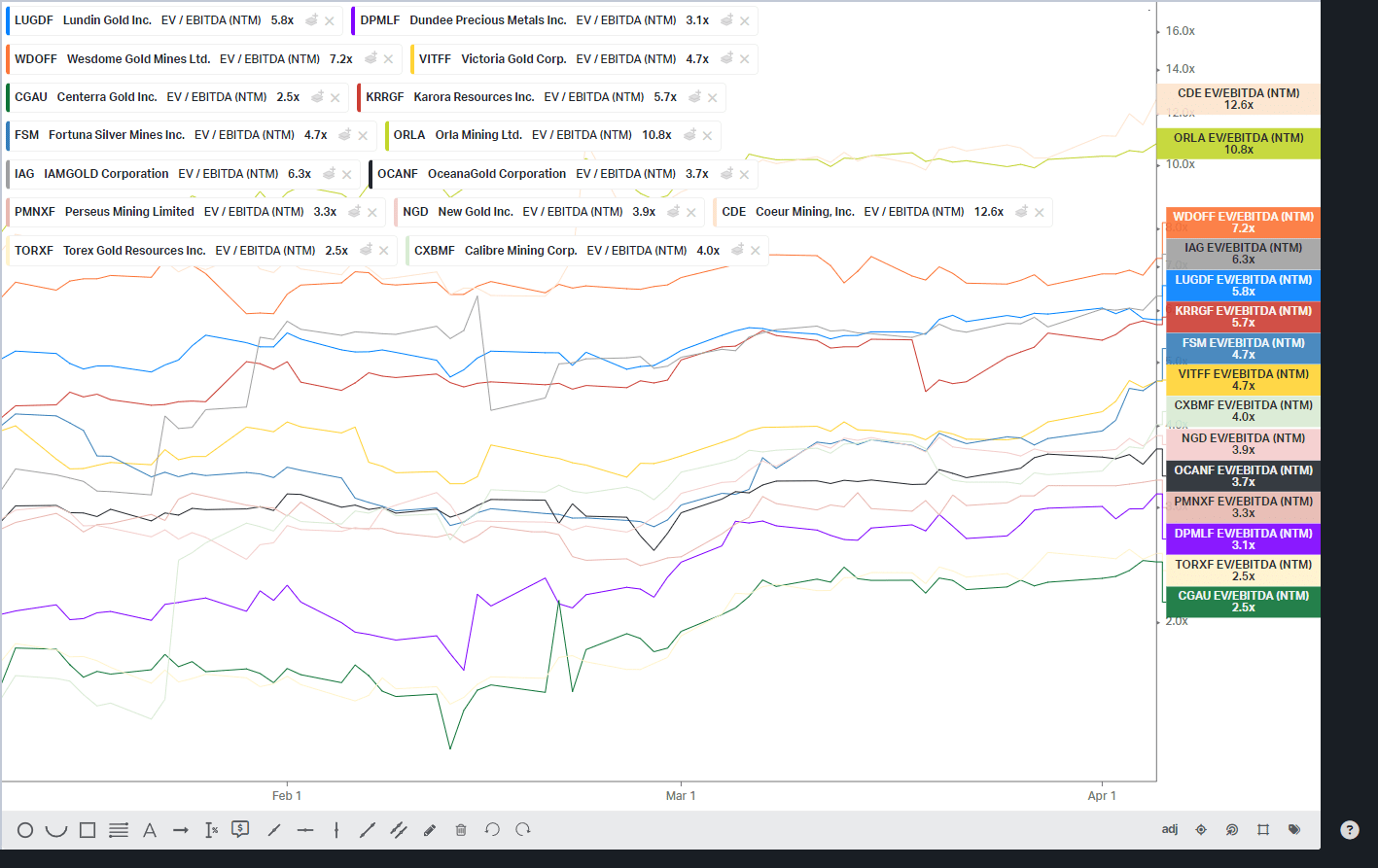

Based on ~692 million fully diluted shares and a share price of US$1.76, New Gold trades at a market cap of ~$1.2 billion and an enterprise value of ~$1.4 billion. This may seem like a steep valuation for a relatively high-cost producer with trailing two-year average all-in sustaining costs of ~$1,680/oz, but it’s important to note that New Gold is on the eve of a transformation that will morph it into a lower-cost producer with significantly higher free cash flow margins. The setup is like that of K92 Mining that expects to see a 40% plus reduction in all-in sustaining costs from 2024 to 2027, coupled with significant production growth. Hence, while New Gold may not jump out as overly cheap from the below chart of its junior/mid-tier peers and for those taking a rearview mirror approach, this is a company whose future will look nothing like its past. In fact, New Gold is still quite cheap here for those with a long-term horizon, trading at just ~5x conservative FY2025 free cash flow estimates of ~$280 million.

New Gold vs. Peers Forward EV/EBITDA Multiples – Koyfin

So, what’s a fair value for the stock?

Using what I believe to be conservative multiples of 5.0x FY2024 P/CF estimates and 1.0x P/NAV (5%) and a 65/35 weighting to P/NAV vs. P/CF, I see a fair value for New Gold of US$2.20. This points to a 22% upside from current levels, suggesting that NGD could make a run at its 2021 highs if it were to reach its updated fair value estimate. That said, I am looking for a minimum 40% discount to fair value to justify starting new positions in small-cap producers to ensure a margin of safety. So, while I see further upside in NGD from current levels, the stock’s updated ideal buy zone comes in at US$1.33 or lower. Obviously, there’s no guarantee that the stock gets to this level, but I prefer to pay the right price or pass entirely for highly cyclical stocks with depleting assets.

Summary

New Gold had an impressive year in 2023 and 2024 is expected to be even better given that it expects to see slightly higher production at lower consolidated costs. However, a decent 2024 outlook has improved into a phenomenal 2024 outlook with the help of record gold prices, setting New Gold up to generate upwards of $80 million in free cash flow this year, with free cash flow set to triple in 2025 (~$260 million) and potentially double again in 2026 (~$520 million). Hence, for patient investors looking for a cash-flow rich story, NGD certainly makes an attractive buy-the-dip candidate if we see a sharp correction. That said, with NGD now ~65% off its low-risk buy zone (US$1.10) discussed in my February update, I remain focused on other opportunities elsewhere in the sector currently.

Be the first to comment