Anton Petrus/Moment via Getty Images

The New Germany Fund (NYSE:GF) had a dismal FY22 across all metrics, with the negative impact of an energy crisis and the Russia-Ukraine conflict weighing on the overall German equity performance. It came as no surprise then that distributions were down across the board – per the December release, GF holders will not receive any further capital gains distribution beyond the May distribution, though the implied ~8% yield for FY22 is still decent, all things considered. FY23 is shaping up to be a much better year – economic indicators in recent weeks, including the ZEW index and the FY22 GDP print, point to a more benign outcome as a resilient German economy looks to bounce back from the impact of the energy shock last year. With lower spot energy prices and elevated gas reserves also supporting the improved data points, an upside surprise could come sooner than previously expected. At the current NAV discount, GF’s high-quality mid-cap portfolio presents a good proxy for investors looking to ride a growth rebound in the coming months.

Morningstar

A Relatively Diversified Middle-Market German Equity Fund

DWS Group’s closed-end New Germany Fund held $161m in net assets as of December 31, 2022. Its 1.11% expense ratio screens favorably for a closed-end fund offering access to middle-market German equities typically out of reach of US investors.

New Germany Fund

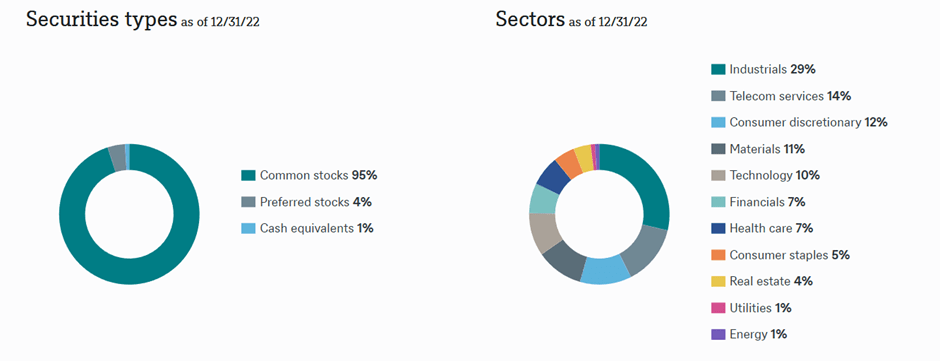

As reflected in the graphic below, the fund’s sector allocation skews toward the industrials, telecom services, and consumer discretionary sectors, which accounted for a combined 55% of the total portfolio as of December 31, 2022. The sector weightage is largely in line with GF’s September disclosure.

New Germany Fund

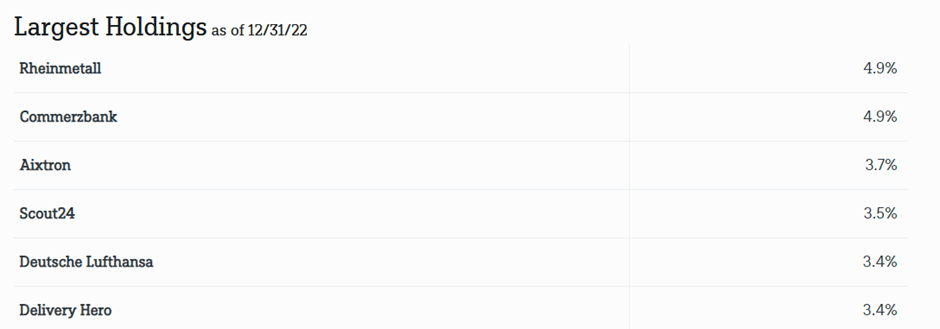

The fund’s largest holdings are German defense contractor Rheinmetall (4.9%), leading German universal bank Commerzbank (4.9%), and semiconductor equipment manufacturer Aixtron (3.7%). The latest disclosure marks an increased weightage toward Rheinmetall and Commerzbank, likely helped by their equity outperformance, as well as a rebalancing away from residential and commercial real estate platform Scout24 (down 80bps to 3.5%) toward Aixtron. All in all, the top ten holdings account for a cumulative 35.5% of an 85-stock portfolio, so the fund is fairly well-diversified.

New Germany Fund

Fund Performance and Distributions Still Respectable Despite a Poor FY22

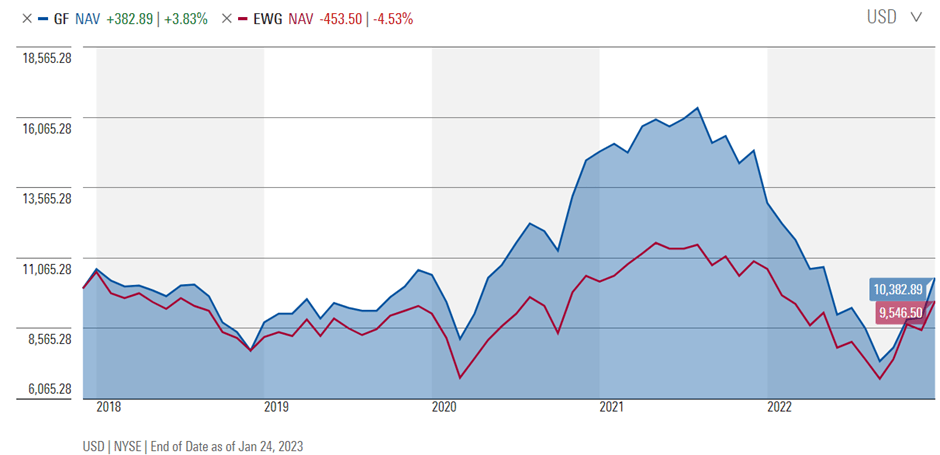

On a YTD basis, GF’s returns haven’t been great at -42.3%, its worst year of performance in a decade. That said, the returns need to be viewed in context – the fund’s focus on mid-market companies meant it took on an outsized hit from last year’s macro challenges. Zooming out, the fund has still compounded its NAV at a respectable high-single-digits % return since inception and outperformed the next best available option, the iShares MSCI Germany ETF (EWG), across short and long-term time horizons.

Morningstar

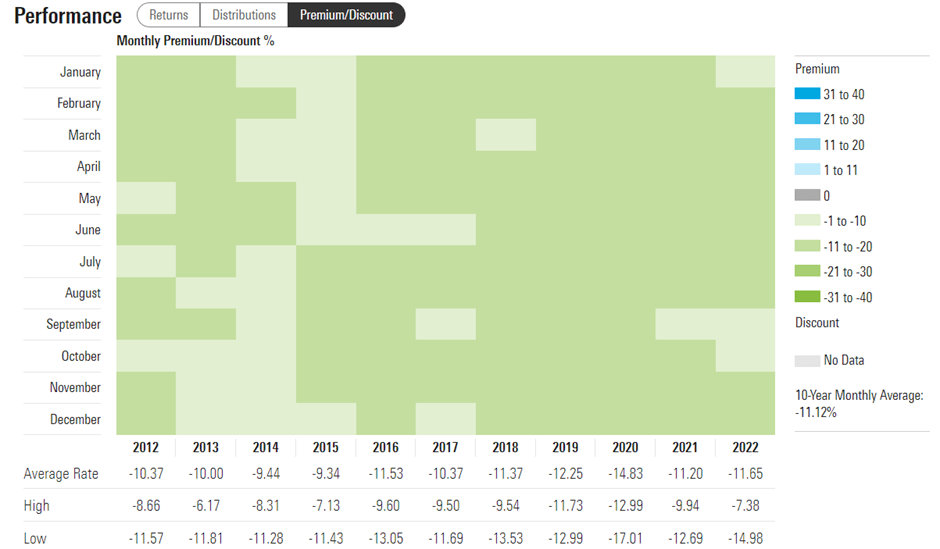

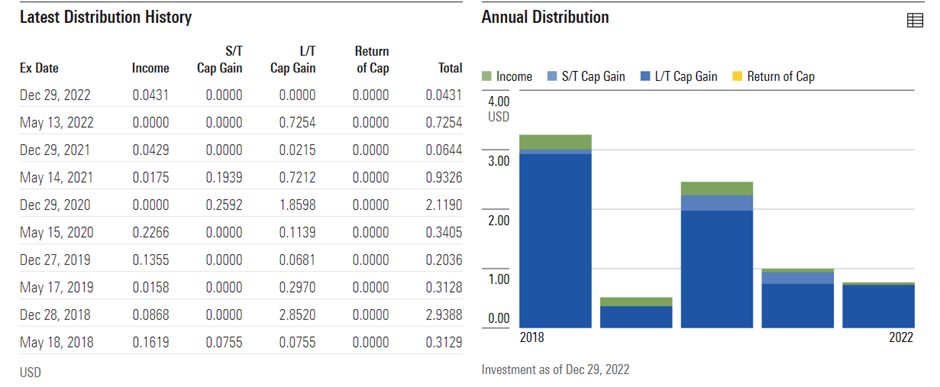

Of note, the fund has also paid out an attractive yield over the years – distributions comprise a through-cycle income component and a larger (albeit cyclical) portion from realized short and long-term gains. In FY22, the fund paid out $0.7685 in total distributions (~8% of the fund’s market value), with the vast majority paid out of long-term capital gains in June, followed by a smaller distribution out of investment income in December. Given last year’s performance, the relatively low distribution has likely been priced into expectations at this point (note the historically wide discount to NAV). Instead, with FY23 already shaping up to be a rebound year (GF is up +14.3% YTD at the time of writing), near-term distributions look poised to surprise to the upside.

Morningstar

Economic Indicators Signal an Improving Business/Economic Outlook

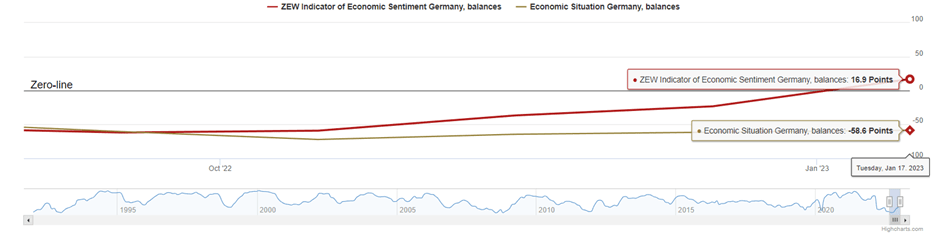

The case for a GF rebound is supported by recent data points out of Germany indicating a more resilient economy than many had expected. The ZEW economic situation index, a measure of economic conditions in Germany, rose +2.8pts to -58.6 in January, while the ZEW sentiment indicator, a leading measure of financial market experts’ sentiment, reversed to +16.9pts (from -23.3pts prior), the first positive print since the Russia-Ukraine conflict last year.

ZEW

Per the accompanying release, the improved indicators were down to “the more favorable situation on the energy markets and the German government’s energy price caps.” Also helping is the recent China zero-COVID policy U-turn, which has driven a step change in the outlook for Germany’s export-driven economy. The sector-specific read-through also bodes well for GF – the biggest swing in profit expectations over the next six months is projected to be in consumer discretionary and services (recall, GF has a 15% and 10% exposure to communication services and consumer discretionary, respectively). Its biggest sector exposure, industrials, is also poised to benefit from an export-driven earnings rebound.

The ZEW data follows an upbeat GDP release showing +1.9% growth in 2022 (implying flat sequential growth in Q4). Underlying the headline print was surprisingly resilient activity, despite the bearish economic forecasts following the Russia-Ukraine conflict and the resulting energy-driven inflation. In particular, private consumption was the standout contributor at +4.6% for the full year, supported by strong wage growth and excess post-COVID savings. Elsewhere, machinery and equipment investment also surprised at +2.5% amid a large order backlog and easing supply chain pressures.

Bears will point to the weakness in construction and the significant decline in November factory orders as reasons for caution. And given we’ve only had one or two months of positive data, it would be prudent not to underwrite a full recovery just yet. That said, I think a partial rebound, at the very least, is on the cards. In addition to the economic data, energy prices have been in decline since the summer peak, and elevated gas storage levels seem to have negated a worst-case scenario for industrials this winter. Plus, consensus expectations are low – German growth in FY23 is still expected to be negative, in stark contrast with the rebound in spot momentum activity over the last month. Thus, it seems likely that expectations will need to be revised up for FY23 in the coming months; GF’s quality mid-market portfolio leaves it well-positioned to capitalize on future upward revisions.

Levered to a More Resilient German Economy

With FY22 in the rearview mirror, the New Germany Fund looks set to turn a new chapter this year, helped by a more resilient economy. Consensus forecasts still call for a German recession – the European Commission, for instance, pegs GDP growth at -0.6% in FY23 before recovering to a modest +1.4% in FY24. In contrast to this view, the leading ZEW indicator this month points to a more benign economic outcome, as lower energy prices and elevated reserves support improving business sentiment in Germany. A positive FY22 GDP print, particularly on private consumption, further reinforces the case for more upside revisions on the horizon. GF’s quality mid-market-focused portfolio offers an ideal way to ride the German bounce back – at a mid-teens % NAV discount and with the yield set to increase from the ~8% in FY22 (assuming contribution from short-term capital gains), this CEF offers investors many ways to win.

Be the first to comment