theasis/E+ via Getty Images

“Man’s mind may be likened to a garden, which may be intelligently cultivated or allowed to run wild.” – James Allen.

It has been just over two years since our first article on Neuronetics, Inc. (NASDAQ:STIM). At that time, the borderline recommendation was that this small medical device concern was worthy of a few hundred shares within a “watch item” position. A lot has happened around the company since then, and it is time for a follow-up. An analysis follows below.

Seeking Alpha

Company Overview

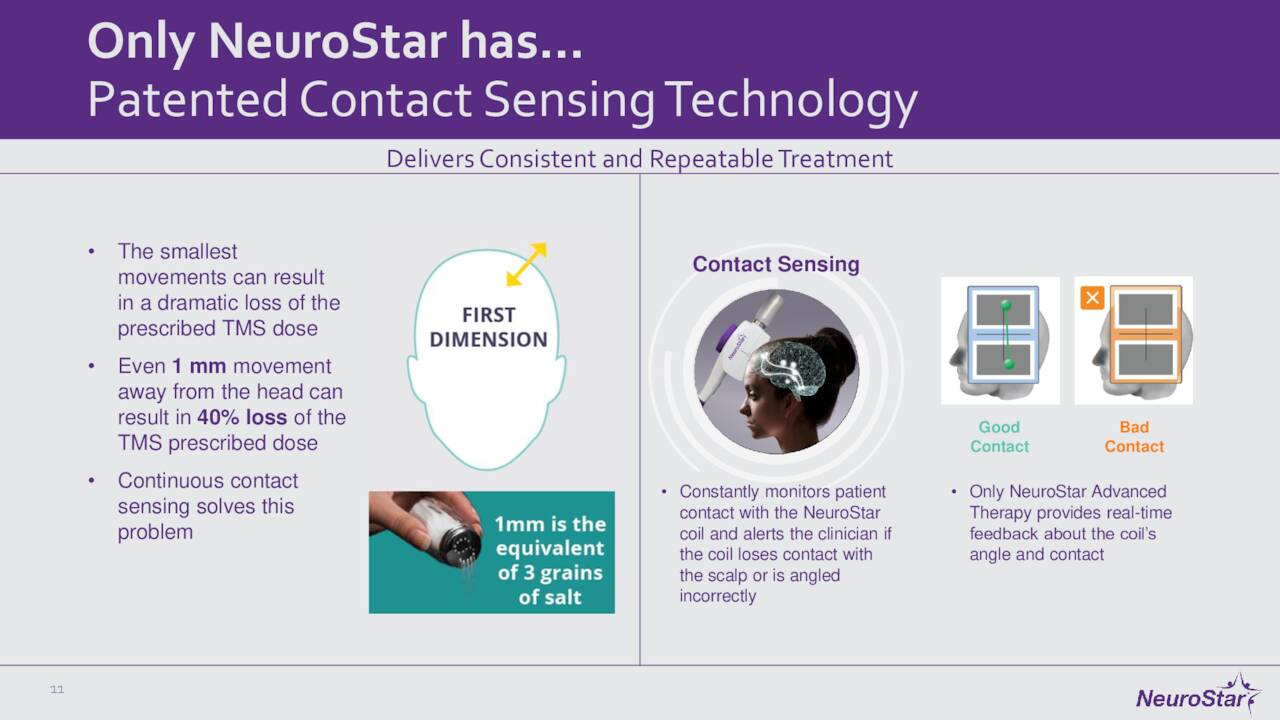

Neuronetics, Inc. is a medical device company based in Pennsylvania. The one product it has on the market is called the NeuroStar Advanced Therapy System and is marketed to psychiatrists in the U.S. and through a partner in Japan. As we described this device in our previous article:

November Company Presentation

NeuroStar is a transcranial magnetic stimulation {TMS} machine that comes with a dentist-like chair. A patient sits in the chair and a clinician places the TMS device in specific locations near the patients head, creating a pulsed, MRI-strength magnetic field that induces electrical currents designed to stimulate areas of the brain associated with mood. It was first approved by the FDA in 2008 and is now indicated for patients with major depressive disorder {MDD}, who have not achieved satisfactory improvement from one or more prior lines of antidepressants. It has also received marketing authorizations from Japan and the EU.“

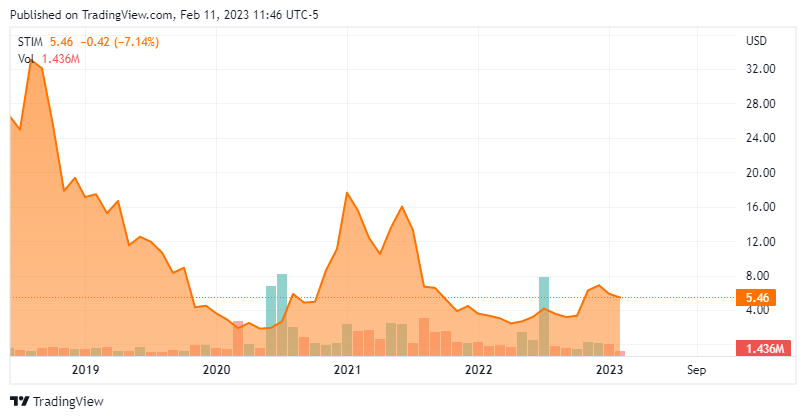

Neuronetics, Inc. stock has risen from four bucks a share at the time of our first piece on the company to around $5.50 a share now, even as the shares have traded much higher over the past two years. The stock now sports an approximate market capitalization of $150 million.

Third Quarter Results

November Company Presentation

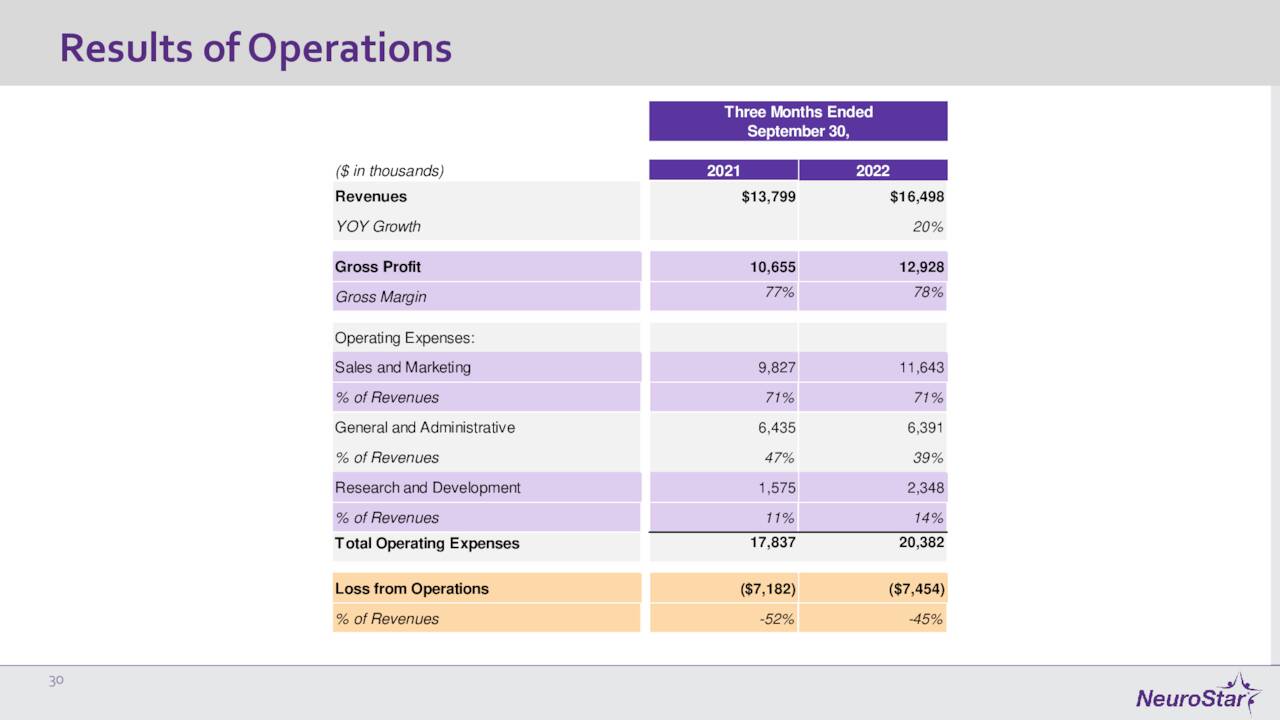

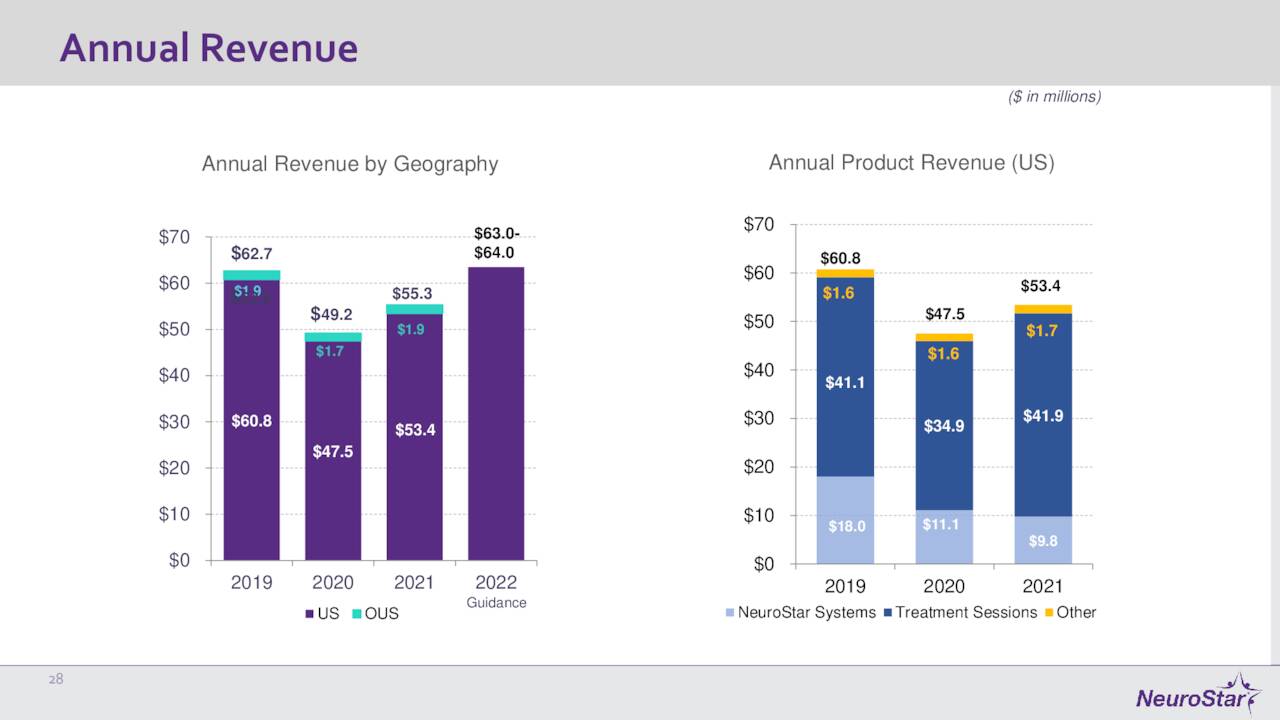

On November 8th, the company posted its third quarter numbers. Neuronetics had a GAAP loss of 28 cents a share, 14 cents better than expectations. Revenues rose some 20% on a year-over-year basis to $16.5 million. U.S. NeuroStar Advanced Therapy System revenue for the quarter came in at $3.9 million, an increase of 51% from the same period a year while U.S. Treatment Session revenue was $11.9 million, up 16% from 3Q2021. Operating expenses did rise to $20.4 million, which was up from the $17.8 million level in the same period a year ago. However, this was a sequential $1.7 million improvement from the second quarter of this year thanks to some recently implemented cost-cutting measures. The increase from 3Q2021 was primarily due to an expanded sales force, the opening of NeuroStar University, and, of course, increased costs from inflationary pressures.

Leadership bumped up its FY2022 revenue guidance up $2 million to a range of $62 million to $64 million and expects total operating expenses for the fiscal year to be between $86 million to $88 million.

Notable Milestones

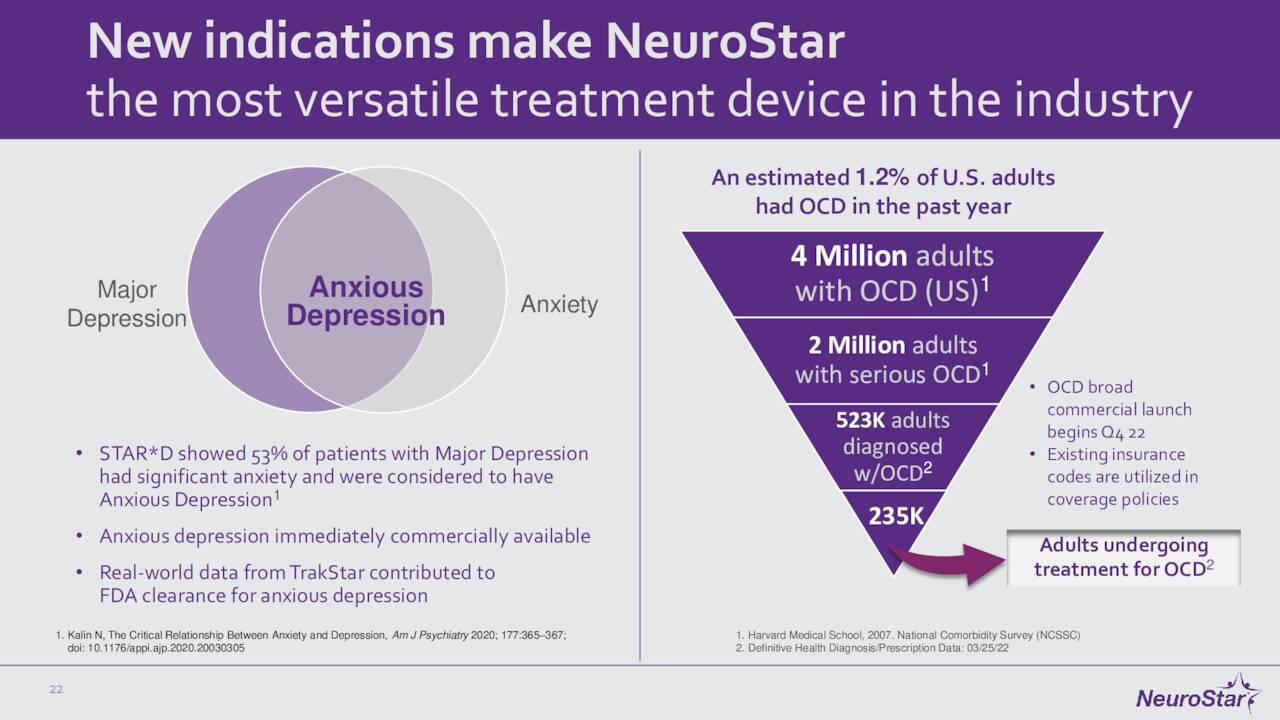

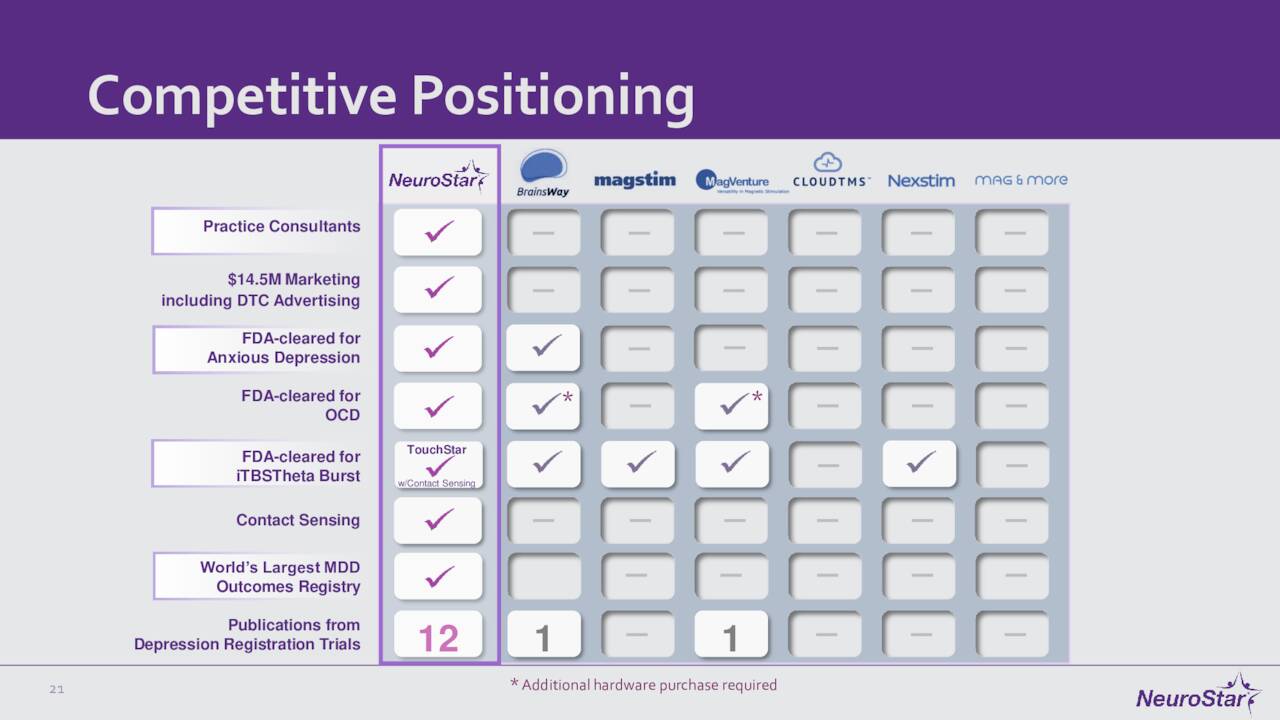

Since we last visited Neuronetics, the company has had some notable milestones. Neuronetics continues to expand its footprint by inking new partnerships with clinics and other medical facilities. It also continues to expand the indications for its flagship product. In May of this year, the FDA approved the NeuroStar Advanced Therapy as an adjunct treatment for patients with obsessive-compulsive disorder. Then in July, the government agency cleared this device to treat anxiety symptoms for adult patients with MDD. The FDA also greenlighted an accessory product for NeuroStar Advanced Therapy in late August, and the company also recently settled some minor litigation. This progress should open up access to some big potential markets for Neuronetics over time.

November Company Presentation

Analyst Commentary & Balance Sheet:

Since third quarter results were posted, Canaccord Genuity ($10 price target, up from $9 previously), JMP Securities ($12 price target), and Piper Sandler ($8 price target) have reiterated Buy/Overweight ratings on Neuronetics, Inc.

Here is what Sandler’s analyst had to say after Neuronetics signed Canada-based mental care provider Greenbrook TMS (GBNH) to a six-year deal on Thursday to use the company’s transcranial magnetic stimulation system at Greenbrook locations.

Neuronetics NeuroStar system will be the only TMS equipment supplied at all Greenbrook locations. Furthermore, Greenbrooks acquisition of Success TMS will add 47 more TMS centers to the company’s network, which should yield even more system placements and treatment sessions provided by Neuronetics.”

Only approximately one percent of the outstanding float is currently sold short. Insiders have been frequent sellers of the shares over the past year. They sold nearly $1.3 million worth of equity collectively in the fourth quarter. So far in 2023, they have disposed of just over $2 million worth of shares.

November Company Presentation

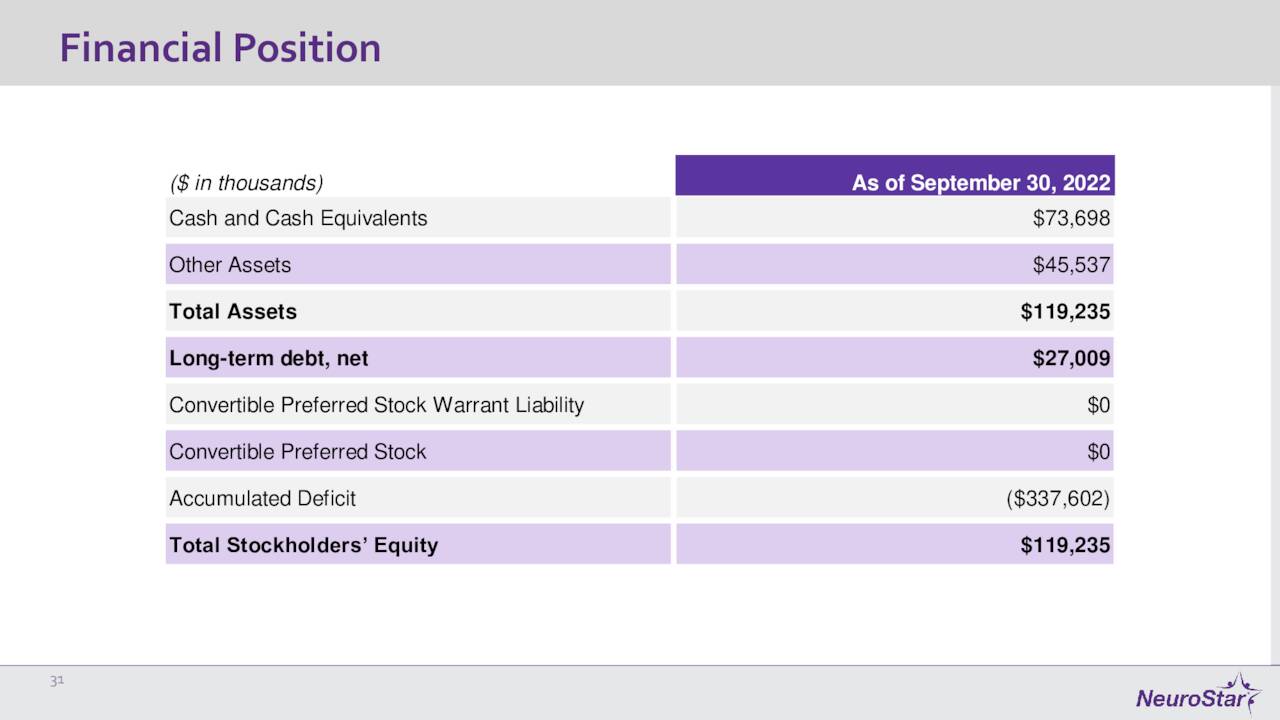

The company ended the quarter with just under $75 million worth of cash and marketable securities on its balance sheet against approximately $27 million of long-term debt. The company had a net loss of $7.6 million in the third quarter, slightly better than the $8.2 million loss from the same period a year ago.

Verdict:

November Company Presentation

The current analyst firm consensus has Neuronetics, Inc. losing $1.45 a share in FY2022 as sales rise 15% to some $64 million, in line with company guidance. Similar sales growth is expected in FY2023, and losses are projected to drop by some 20 cents a share.

The company is making some slow progress and delivering mid-teens sales growth. In addition, the company had over $330 million worth of net loss carryforwards, which will be valuable if/when Neuronetics becomes profitable.

November Company Presentation

Neuronetics, Inc. has made progress on the FDA approval front since we last looked in on it as well. That said, I want to see these positive events boost sales growth and narrow quarterly losses further before upgrading STIM from anything more than a small “watch item” holding. Fresh data points from fourth quarter results should be forthcoming shortly from Neuronetics to assess.

“Assumptions are quick exits for lazy minds that like to graze out in the fields without bother.” – Suzy Kassem.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment