Wachiwit

“Vision is the art of seeing things invisible…”

Jonathan Swift (1667-1745) Anglo-Irish satirist, author of Gulliver’s Travels, Tales of the Tub).

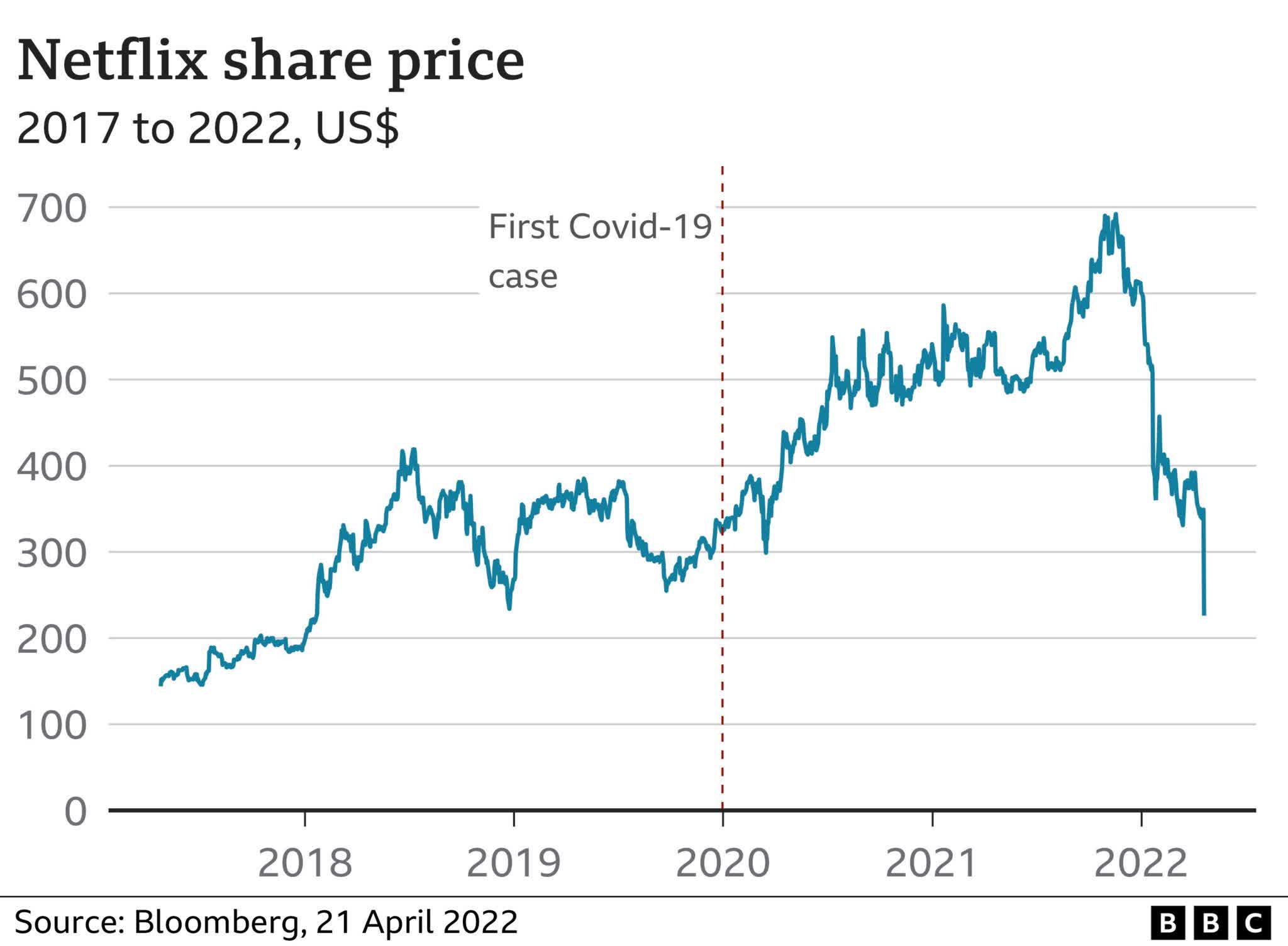

Author’s note: Few places online or off have poured out as much analysis, exhaustive data sets, and diversity of opinion on the shares of Netflix, Inc. (NASDAQ:NFLX) as has Seeking Alpha. Much of what has been published is really good, providing readers with a balanced perspective on the stock.

In connection with this article I went through much SA material on the stock so as to avoid adding to the hash and re-hash of many well-made points. That’s perfectly understood. Netflix as a company and a stock is a complex, challenged entity facing a watershed moment.

However, the article that follows makes no pretense of piling even more data upon data by slicing and dicing into infinity the mountain of info already available to readers. My objective here is to veer the ongoing discussion into an entirely different direction. A few relevant numbers are included for context only.

I looked at the company entirely from the viewpoint of a strategy with a central proposition that the best solution to the dilemma that faces the company is not necessarily an ad-free and ad-friendly price split. It’s not a matter of quarreling with management’s conclusion on two-tier pricing. It is an idea that urges Netflix to consider another pathway, totally out of the box: an acquisition aimed at diversification of its business to include a related, existing business.

That suggested acquisition target as you will read is DraftKings Inc. (DKNG).

Why propose this seemingly bizarre thought? How could the pieces of both companies mesh into a really exciting whole that would have a better chance of solving the company’s continuing loss of its subscriber base? For one thing, the average revenue per NFLX member now sits at $15.95. This vs. the average revenue per DKNG customer is $103 per month.

Both companies are engaged in ecommerce, selling entertainment services of one kind or another. Both operate in fields growing more chaotic and crowded by the day. Both face daunting challenges to build their businesses from now forward as even more competition looms. In the case of DKNG, we have Disney’s ESPN and privately held sports gear giant Fanatics peering seriously into the betting sector.

Disney (DIS) remains mired in the hamada hammada, navel contemplation expressed by CEO Chapek. That will change. Fanatics 90m sports-wearable addicts may or may not prove potent as gamblers. Time will tell. Either way, the sports betting sector faces even more competition ahead from potential resource-rich entrants than even does the streaming space.

DKNG’s homilies to shareholders about how it intends to become profitable by next year or the year after are pure speculation. Stagflation is already biting into consumer discretionary budgets. It could rear a very ugly head both for NFLX and DKNG in the years ahead. But together, their strengths outweigh their weaknesses.

I believe the price of DKNG shares including a viable premium would be welcomed by holders. The promise that such a deal could solve key problems for both at once is the premise of this article.

google

A Modest Proposal

The world-famous 1729 satiric essay by Dr. Jonathan Swift, A Modest Proposal, weighed in on the widespread poverty in Ireland and the sniffing of British aristocrats decrying the wanton excessive population growth. In a macabre response to failed policy nostrums advocated by authorities, Swift’s satiric essay proposed that the Irish should eat their excess children, a strategy that would produce many benefits at once.

He posited that it would help with population control, cure hunger, make money, prevent crime, and make fashionable clothing out of various parts of kids. He assayed that kids might be tasty boiled, fried, or turned on a spit. In the end, Swift assured that his elegant solution would solve the core problem of Ireland: poverty and its many ills.

The famous essay has been cited (ex its ghoulish theme, of course), alluded to as an example, of a perfectly elegant solution to a massive problem. It is quoted here because it suggests that sometimes an utterly out of the box solution to a problem requires a draconian, or at least, normally unheard-of action. My own recollection of its being cited as an example of innovative thinking, somewhat on the wild side, was in grad school.

In a course using SWOT analysis of companies (STRENGTHS, WEAKNESSES, OPPORTUNITIES, THREATS), our professor read out the fifteen three-sentence solutions each of us had submitted to solve a theoretical problem of a broken business model in a consumer corporation. He held up the pages and tore them apart and said,

Paraphrasing from my memory:

“Nothing with nothing here. Now let’s begin again with Jonathan Swift and his Modest Proposal to rethink your options Get out of the box and stay there.” He proceeded to read A Modest Proposal to us, triggering peals of laughter in the classroom.. But he then laid down his principles of problem solving in business:

You always look (and do not always find, but the looking is key anyway) for the elegant solution. It’s one that attacks the causes, the symptoms of the problem in one fell swoop. It is a solution that is utterly apparent when the epiphany hits you in the gut.

The Netflix dilemma: A shot at an elegant solution

The veritable mountain of data and opinion by analysts, industry gurus and investors regarding the next phase of Netflix’s corporate life is staggering. We have sifted through much of it, looking for pathways explored which we believe offer the most elegant solutions to the core dilemma of the company:

How do you stem the tide of subscriber losses and reinvent a rationale in a marketplace that has exhibited every symptom of excess capacity triggering a discount or price cut solution for openers.

Great new content is a way forward, but it has become a hiding place for streaming managements under stress.

Fair enough. We’ve seen more intellectual power applied to the dilemma facing all the streamers in one way or another than the solving of Quantum Theory that even puzzled the likes of Einstein. Much of the deep-dive analysis has been very good. There is a clear misalignment between a saturated North American market, and price elasticity that can reliably reduce churn. Price cutting once begun, never stops.

At the same time, we have to acknowledge that the demographic data management and development skills of NFLX must rank at the top of corporate America. During the process that brought it from its red envelope-stuffed mailbox days to where it stands now with the apogee of top streamers, we can conclude that there is little of that Netflix does not know about their customers and what rings their bells.

Yet it is hard to deny that from some perspectives, a switch to dual pricing seems like a Hail Mary business strategy. The decision to address their negative churn to go to a two-tier price system with or without ads surely has sound foundational research. Members clearly have gotten fed up with burgeoning monthly bills.

It’s fair to conclude that if after what clearly was a deep-dive numbers crunch and research effort, the decision to go to tier pricing was the best NFLX could come up with. Remember, this is the company formed out of a dazzling insight: Blockbuster was broken, red envelopes are better. So we have to respect the price strategy decision. Linked to that is clearly the de rigueur promise we hear of every streamer in crisis: We’re gonna spend billions on great new content our customers will love.

That presses two questions: one, will customers love new content to the extent of enduring even the proposed limit per hour of ads? Does the little Skip Ads button on YouTube movies have a message about public toleration of intrusive messaging?

And two, does anyone in their right mind really believe that the limited ad-to-content ratio initiated and sworn to be upheld will remain in place. Ads have a long history of metastasizing into content in ever longer chunks. Viewers tend to be passive only so far. The entire streaming business was built on the premise that people sought escape from ads. So what this presages, perhaps, is that streaming ultimately reverts to a form of the broadcast TV medium consumers ran from as soon as technology came to the rescue.

Stepped-up content spend may be good news to the so-called creative community, but it does not totally auger well for Netflix investors. The deluge of new programming has a terrible financial paradigm in general. There will be solid hits ahead no doubt, and some will coin money—yes. But the odds are that most of them will be what’s known in the crap game as prop bets: longer shots with longer odds for bigger payoffs that never seem to be regular visitors to a gambler’s house. Which leads us to the ever inventive, eerie mind of Mr. Jonathan Swift.

Mr. Hastings: Take a long hard look at DraftKings

Netflix archives

Above: Hastings is a past master of the elegant solution from way back in the red envelope mail days.

The question before the house: what on earth does a sports-betting ecommerce platform have to do with a TV streaming business? Talk about out of the box. Such a suggestion on the surface, we realize, may seem out of this solar system for openers. So, let’s try to construct an elegant solution here that could in turn:

- Bring Netflix an existing $2b business by next year now that could be comfortably nested on its site housed within an app to be clicked between or in lieu of shows.

- Offer DKNG a monster audience of 73m for them to slice, dice and target potential new betting customers many of whom are already NFLX customers.

- The potential would be confined to the 30 currently legal states with tracking apps easily within the tech stack of Netflix engineers.

- In a second phase, Netflix could extend the DKNG betting platform to countries where sports betting is already legal. This gives the company instant international branding and cash flow it does not now have in any meaningful way. Including global customers, Netflix has 220m paying customers.

- Add sports entertainment content to the betting site.

- Avoid the same old same old promises of breakthrough content. In such an acquisition, Netflix would be acquiring DKNG content as a gift that does not stop giving with the subscriber’s monthly bill.

Looking forward to the full maturation of the U.S. sports betting sector by 2025, we are forecasting it becoming a $25b business. We expect DKNG to hold onto at least an 18% share of market at that point. That would bring ~$4.5b to $5b in annual revenue to NFLX. By then, promotional cost savings could have brought the DKNG business into accretive EBITDA meaningful for NTFLX bottom line.

Compare that to what a divided ad-no ad price strategy could bring and in our view, it is no contest. Such a deal solves the future of both companies in what we believe to be a somewhat elegant way that a simple two-tier pricing model cannot of itself.

If DKNG achieves a $5b revenue share in 2025, no matter what the forward revenue growth of NFLX would be from its current $31.7b, it would appear to contribute at least more than 10% of total revenue. Shorn of its excessive promotional costs, which now keep it mired in losses, DKNG could operate on a very respectable gross margin for NFLX, highly accretive to earnings going forward from 2024.

Valuing the transaction

The acquisition by one company ten times the size of its target presages a thorny challenge for investment bankers. In NFLX you have a profitable company facing revenue decline but otherwise in good financial health. On the other, you have a money-loser with a rapid sales growth arc. But in both cases you have two companies with their stocks dramatically down from their historic highs and ripe for a deal. And they share a singular objective: how to build greater revenue per customer with more customers over time by providing them with an established high demand service.

The cash position comparably is interesting:

NFLX has $5.8b

DKNG: $1.33b

NFLX debt: $16b

DKNG debt: 1.33b

At $16.75 a share, it seems to us that a 20% premium of DKNG would be attractive, but subject to endless numbers-crunching leading nowhere. DKNG is still losing far too much money. It seems to us a better approach would be a swapping of shares.

For the sake of discussion only, we’d think a 20 to I ratio make sense. DKNG holders get 1 share of NFLX for every twenty they own. I let the bankers way above my pay grade to suss this out. Over the long term, we think the upside of NFLX shares could creep much higher than where DKNG might settle.

Frankly, a two-tier price strategy is okay, but to us it is something akin to eating your young. But offering the immense convenience for sports bettors and NFLX viewers to streamline and eliminate steps speaks to us of the key reason the Netflix original business model made so much sense. It was elegance personified. You watched what you want, when you wanted it, how you wanted it at a price you were comfortable with.

When the steaming business model was created there was Netflix and its handful of marginal wannabees. That’s gone with the wind, as they say. It’s time to build anew and think way out of the box as to what may really work big time beyond a price move.

It’s a modest proposal. Its elegance to us would naturally be in the hands of inventive bankers. Whether this is a deal for a chunk of the equity or all of it is a matter of stock prices at deal time. Either way, the outcome longer term could be:

- NFLX customer avoids ads.

- NFLX data base generates betting customers by the ton with cross marketing deals with DKNG.

- DKNG gets to save a ton on promotions to generate new bettors or steal from competitors.

- As DKNG becomes profitable, it will be a meaningful contributor to accretive EBITDA to NFLX.

- DKNG is better positioned to defend itself if and when ESPN and Fanatics crash the sports betting party.

And not one kid becomes a tempting slice of pizza.

Be the first to comment