da-kuk

Investment Thesis: While Nestle has seen strong sales growth in the first half of this year, inflation and a potential rise in price sensitivity on the part of consumers could be risk factors.

In a previous article back in February 2021, I made the argument that Nestle (OTCPK:NSRGY) should see solid long-term growth prospects, on the basis of strong growth across the pet care business as well as an expansion across the healthy prepared meals segment in the United States.

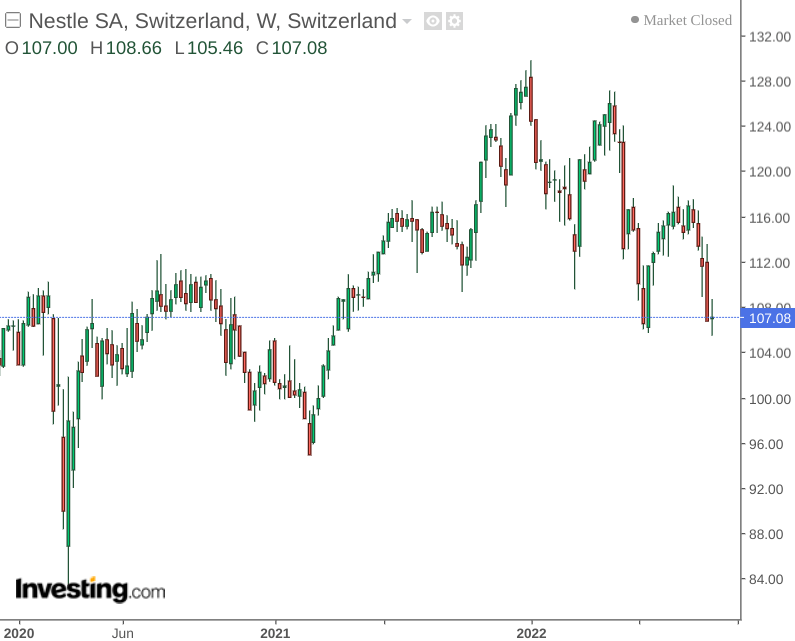

While the stock saw gains throughout the rest of 2021, Nestle has come under pressure this year – in significant part due to bearish market conditions and concerns with respect to inflation.

investing.com

The purpose of this article is to assess whether there is a significant disconnect between the recent price drop and Nestle’s performance, and whether we could see scope for a significant rebound going forward.

Performance

When looking at the company’s balance sheet, we can see that the quick ratio (calculated as cash and cash equivalents plus trade and other receivables all over total current liabilities) has decreased from 0.45 to 0.38.

| Dec 2021 | Jun 2022 | |

| Cash and cash equivalents | 6988 | 5364 |

| Trade and other receivables | 11155 | 11553 |

| Total current liabilities | 40020 | 44475 |

| Quick ratio | 0.45 | 0.38 |

Source: Figures sourced from Nestle Half-Year Report January-June 2022. Figures in millions of CHF. Quick ratio calculated by author.

This indicates that Nestle is in a slightly less favourable position to pay off its short-term debts, as a result of a decrease in cash and a concurrent increase in total current liabilities.

In addition, it is also notable that Nestle reported an increase in net debt from CHF 32.9 billion in December 2021 to CHF 48.5 billion in June 2022.

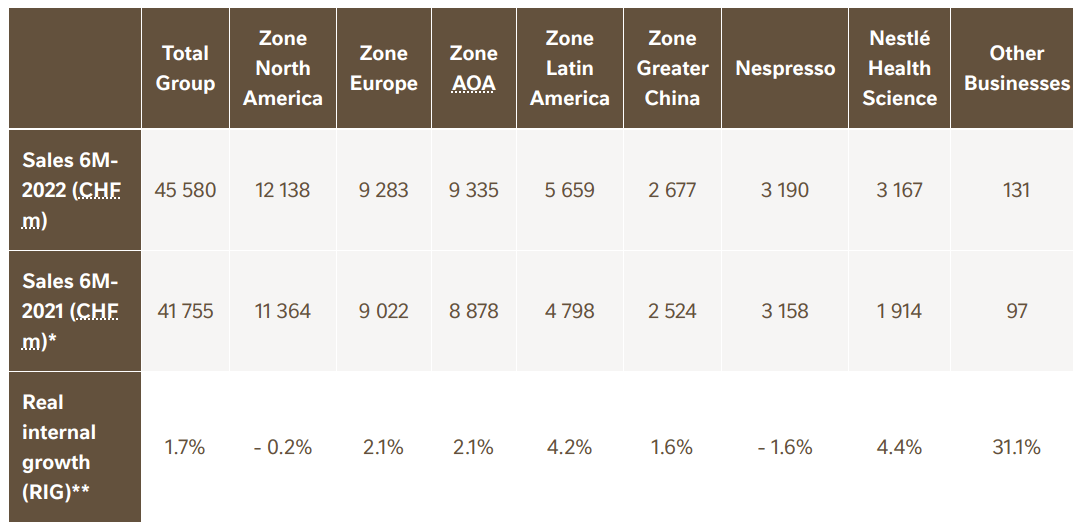

In terms of sales, we can see that the Water and PetCare segments showed the most organic growth for the half-year 2022 results as compared with the half-year 2021.

| Category | Sales 6M-2022 | Sales 6M-2021 | Organic growth** |

| Water | 2291 | 1792 | 17.20% |

| PetCare | 7403 | 8589 | 13.90% |

| Confectionery | 3229 | 3595 | 10.80% |

| Nutrition & Health Science | 6060 | 7689 | 7.80% |

| Powdered & liquid beverages | 11648 | 12335 | 7.60% |

| Milk products & ice cream | 5205 | 5443 | 3.50% |

| Prepared dishes & cooking aids | 5919 | 6137 | 2.90% |

| Total Group | 41755 | 45580 | 8.10% |

Source: Figures sourced from Nestle reports half-year results for 2022 Press Release.

Additionally, when looking at growth by geography – we can see that real internal growth saw a slight decrease across North America, with Europe and Asia up by 2.1% and Latin America showing the most growth on a percentage basis:

Press Release: Nestle reports half-year results for 2022

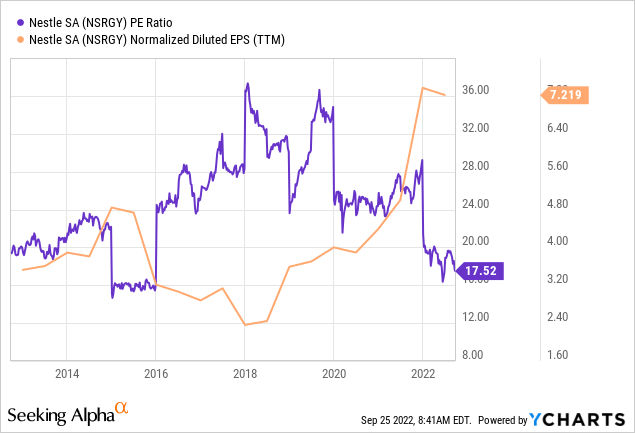

When looking at the company’s P/E ratio, we can see that the ratio is trading near a 10-year low, while earnings (on a normalised diluted basis) is trading near a 10-year high.

investing.com

As a result, there could be a case for arguing that Nestle is undervalued on an earnings basis after the recent price drop and could see significant upside in the event of a rebound.

Looking Forward

Going forward, inflation is likely to be a key consideration for investors in terms of how it stands to affect Nestle’s business.

Earlier this year, cost-push inflation meant that the company raised prices on key offerings such as KitKat chocolate and Perrier bottled water – with first half prices rising by 6.5%.

Product segments such as Water, PetCare and Confectionary have continued to see growth on account of food and drinks being considered necessities, as well as a continued propensity for pet-owners to spend on pet care even in inflationary periods.

However, the main risk for Nestle at this time is that consumers become more price-sensitive and decide to switch to cheaper brands.

With the World Bank citing an increased risk of a global recession in 2023, the second-half of this year may prove to be a significant telling point as to whether consumer spending could remain resilient under such a scenario.

Conclusion

To conclude, Nestle has continued to see strong sales growth and the company could see a significant rebound if earnings continue to grow.

However, the risk of recession resulting in a slowdown in sales growth as well as an increase in debt levels could mean that the stock sees more modest growth in the short to medium term.

Be the first to comment