Petmal

Dear readers/Followers,

In this article, I’ll be taking a look at Norwegian company Nel ASA (OTCPK:NLLSY), the world’s largest producer and enabler of Hydrogen. If you wonder why you (probably) have never heard of the business, that’s because Hydrogen in terms of what Nel does hasn’t exactly become mainstream yet. Nonetheless, the company has been around for many years

So, let’s take a deep dive into Nel and see what we have here.

What is Nel ASA?

Nel is a company in the renewables sector that has been around since the late 1920s. It’s global, and it works in hydrogen to deliver hydrogen solutions through renewable energy. It’s very much “in the now” given the current ESG trends, and the current decarbonization trends across the world.

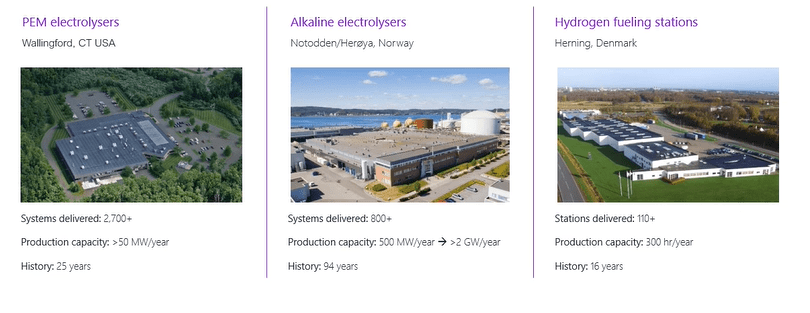

It’s the world’s largest manufacturer of electrolyzers, with over 3,500 units delivered to over 80 countries globally in its soon-100-year tradition. It’s also a leading manufacturer of hydrogen fueling stations, with over 120 delivered to 14 countries, and it manufactures purely in “The west”, not China, with factories found in Norway, Denmark, and the USA.

The company doesn’t really have a credit rating, and it employs less than 1,000 people – only 575, as it happens.

Still, it has 3.5BNOK in cash reserves, making it a massively cash/liquidity-heavy company for its size. Hydrogen renewables have unfortunately taken a bit of a backseat since EVs have come into play – at least in terms of automotive.

However, Nel isn’t just automotive – not even mostly automotive. While the company’s solutions and its plans are to serve fuel cell vehicles, it has a different place in the value chain than just automotive.

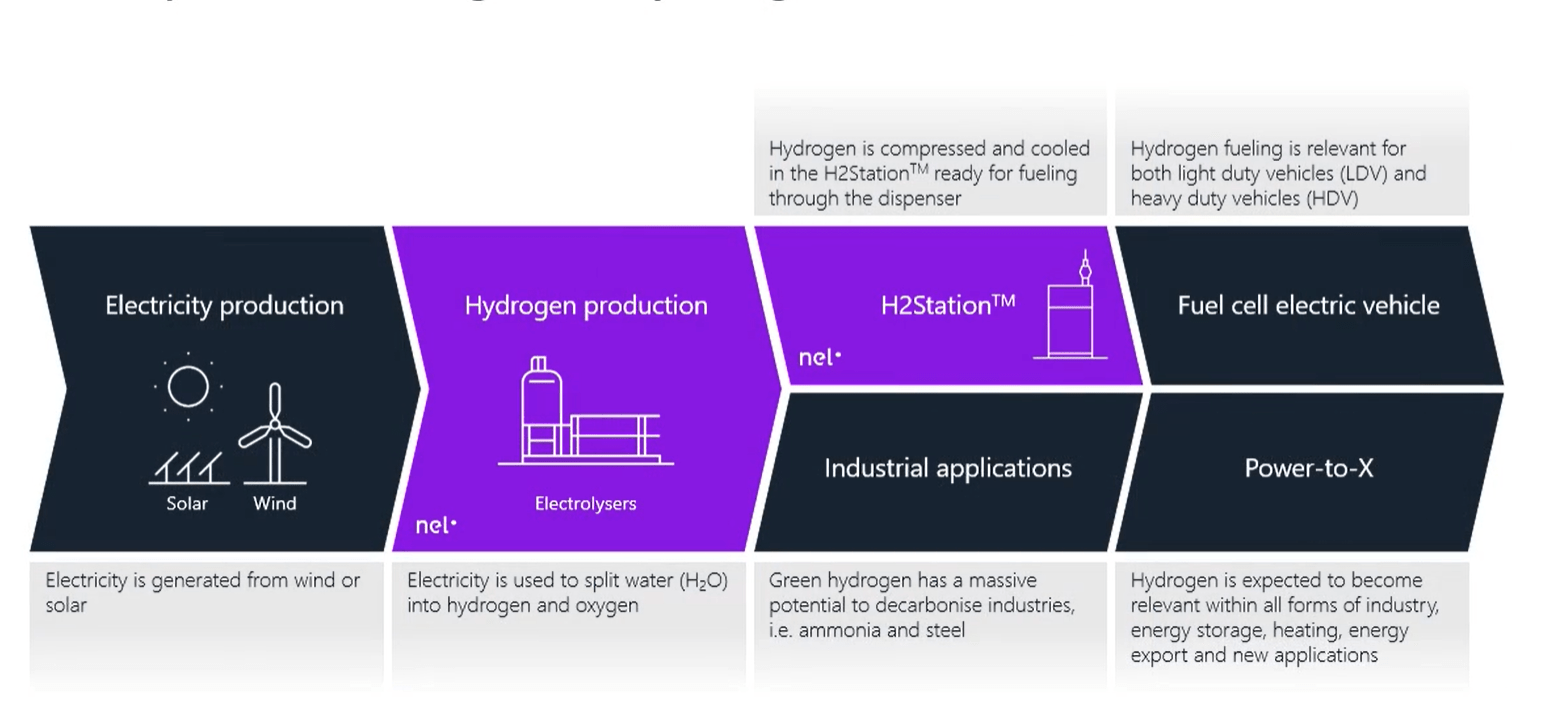

Nel IR (Nel IR)

Nel takes the place right after electricity production, manufacturing not just fuelling but the equipment needed to produce Hydrogen on-site. This production can in turn be used not only in fuel cells for cars but across industries in the interest of decarbonization.

The company has incredible expertise in this field because this is what they’ve been doing for the past 80-90 years.

Nel IR (Nel IR)

And the industrial application potential for this is broad – from food production to Glass, polysilicon, labs, chemicals, thermal processing, steel, Power, and life support – it can be used here. By using renewable hydrogen, companies can decrease the costs of renewables, which gives the company exciting opportunities within both existing and new sectors across the board.

While hydrogen likely won’t be used in automotive in the near term on a consumer level, the commercial sector is looking different. The heavy-duty sector is developing hydrogen faster than anticipated, and the company considers it a relevant fuel here.

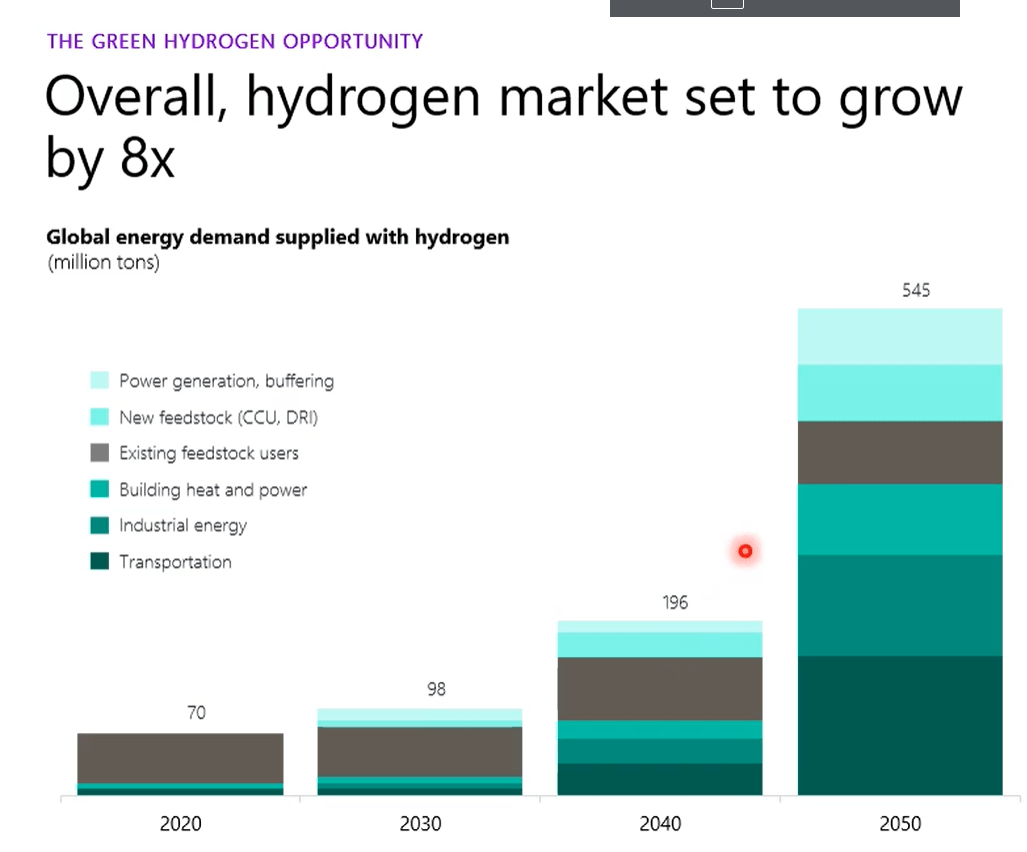

The company’s base case is an increase of 8x over the next 20-30+ years.

Nel IR (Nel IR)

These numbers come from a biased source, so they need to be taken with more than a spoonful of salt – but the underlying demand drivers are realistic. The regulations will likely lower surplus demand for fuel, and the ongoing decreased quality of crude across the world should, and likely will increase the demand for Hydrogen for processing. The company believes there is a move from coal to hydrogen – again, the move is there, but the scope is somewhat in question.

The company believes that as the market for electrolyzers grows because it’s starting from so small a market, you’re looking at the potential growth of 800x over this period.

The company also makes the case that current electrification of wind and solar is by themselves making the case for green hydrogen, and Nel targets to have the cost for hydrogen down to $1.5/kilogram by 2025, based on $20/Mwh, 8% cost of capital with a lifetime of 20 years. While the electricity numbers need to be looked over, the other assumptions are not wrong as such and could work.

The company believes in its current model and is expanding its capacity significantly in Norway in order to increase production and reduce the costs of its electrodes and other components as well, driving efficiencies.

All of this sounds interesting – but does the math work? Are we even talking about a profitable business?

So-So.

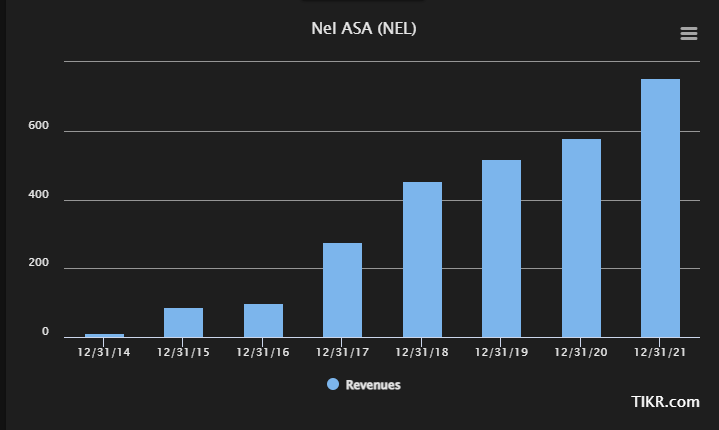

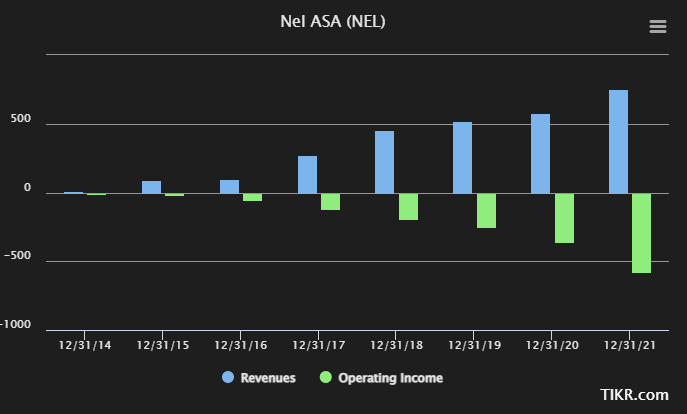

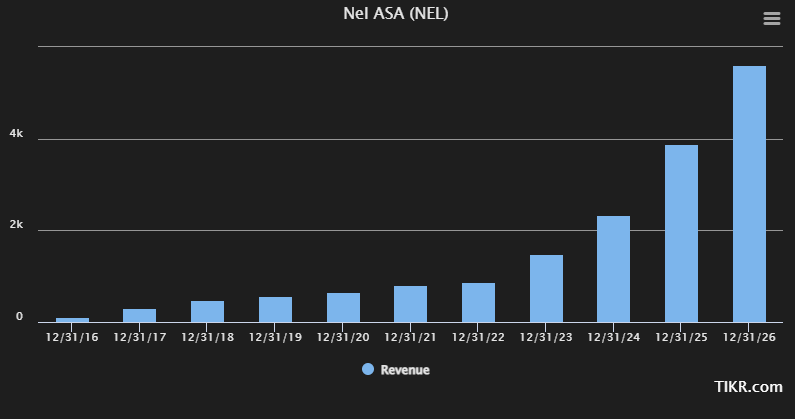

Nel certainly has sales – they even have impressively growing sales…

NEL Revenues (TIKR.com)

…with latest annuals up over 600M NOK. However, looking closer at the bottom line, we find some issues. Flowing to GAAP Gross, the company’s gross margins have declined from over 70% in 2014 to around 26.14% in 2021, which would imply that the company’s efficiencies in scaling up are not working out as the company expects or that the company needs to scale more. As it stands now, the more revenues the company generates, the less it makes in terms of gross profit.

Moving through SG&A, D&A, and other Operating expenses, the company has been able to generate positive net income only once in the last 7 years – and this was due to income from investments.

Nel Operating Income (TIKR.com)

A few ways to view this sort of development. I will say that this company is still in its starting phases, meaning once they start scaling more, it’s possible that things will reverse. The company has a very outsized SG&A. For LTM 2022, out of 781M NOK in revenues, 574M NOK is going to SG&A, with another 332M towards other OpEx, and that doesn’t even include 607M of COGS.

Highlights for the latest quarter are as follows. The company managed 183M NOK worth of revenues with 148M from electrolyzers, resulting in a negative FCF/EBITDA of 214MNOK. The company does have 2.1B NOK worth of order backlog – but at current margins, that just means that the company has the potential for negative 3-4BNOK worth of operating income unless something changes.

Nel IR (Nel IR)

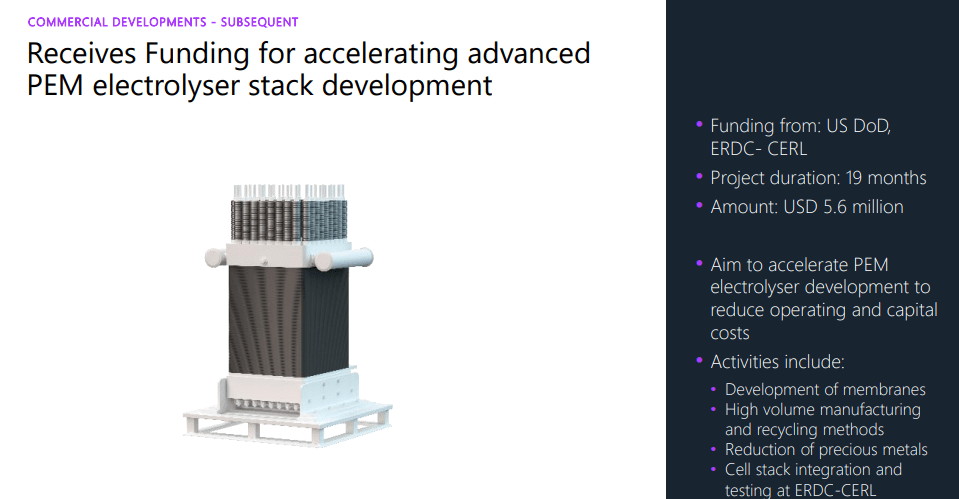

Order intake is strong – up 456%, and the company’s purchase orders include 200MW worth of alkaline stack at a value of almost 450M NOK. The US DoD is also in play, with $6M worth of funding for accelerating the development of the PEM electrolyzer stack.

So there’s plenty of interest in the company’s various technologies, from all manner of directions. But as of now, and given that the company has a very long history, I can’t see that it’s ever managed to turn a profit for its shareholders. Like with tech companies, the focus seems to lie more on top-line growth, which makes sense given the company’s argument of being in a starting phase.

However, it doesn’t take away from the worry and the question regarding when we will be able to see profitability from this business. The company seems to rely largely on political initiatives…

Nel IR (Nel IR)

…and the corresponding inflation reduction act in the US. The fact that production capacity is increased also speaks some promise to the company eventually getting margins up – and not just gross margins either.

However, to be fair – the company hasn’t promised profitability. It’s promised to deliver on orders – including the 200 MW orders it delivered on, and is currently forecasting more orders of this, and larger size, to come in. The market outlook is good, and the company’s pipeline is “maturing”.

However, the company argues it’s securing large-scale quality orders with attractive margins, to which I ask, attractive to whom?

Nel is currently spending an average of 73% of its sales revenues on SG&A alone, and this is not a TTM fluke, 40-80% of revenues is more or less the level it has held for over 4-5 years at this point. This is not attractive. It’s spending another 42% on other OpEx, and its COGS are 77% of revenues, coming to a total of 192% of TTM revenues.

Nel still has a hill to climb – and it’s not a small one.

Let’s move to valuation.

Nel Valuation

“Oh, but you don’t understand growing companies”.

No – I do understand growing companies, but I also want to make sure that investors understand what they’re investing in. Because the money you put into Nel, that’s not necessarily money you’re getting back soon in terms of positive earnings.

I wouldn’t call Nel a “gamble”. The company is too well-established for that, but it has yet to prove to the market that it can scale up and deliver positive earnings. It’s not as though its margins have been improving. Quite the opposite, actually. Also, interest expenses have been rising by more than 600% since 2018 – granted, this was from below 1MNOK, but the company is taking on debt, and more than 10M NOK will likely go to that expense this year, and if the company keeps this pace, this is likely to increase to 3-5% on a top-line basis as we move forward.

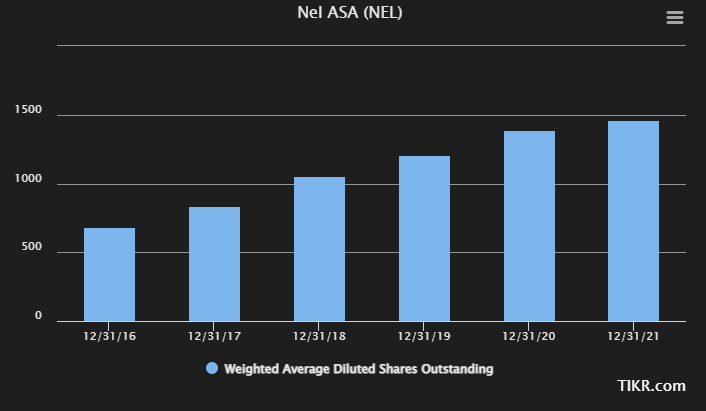

The company has also been issuing shares – quite liberally.

Nel Outstanding Shares (TIKR.com)

Liberally being more than doubling SO in less than 6 years. The reason for this being that millions of shares are being used in the company LTI-plan, using standard vesting schedules. This is for 2020, for instance.

Nel IR (Nel IR)

Watching this company’s various indicators and economic variables when it comes to valuation, how comp is being done as well as how the company’s SO is growing does not give me that much confidence, truth be told. S&P Global has 21 analysts following this company – it is a growth company after all and they give Nel targets of 7 NOK to 25 NOK, with an average of 14 NOK.

That’s a discount to the 16.5 NOK we currently have, and only 5 of the analysts give it a “BUY” rating, compared to much more positive numbers a year ago or so.

Because the company doesn’t generate profit, looking at EBITDA, P/E or other cash-based/profit-based multiples makes no sense.

We can look at BV and tangible BV as well as NAV, but this is mostly factories and other balance sheets assets. For that, the company currently demands a 5.22 x Tangible BV, and a NAV of around 5x as well.

However, now to the positive.

Analysts believe Nel will grow – and that the company will grow significantly.

We’re now in 2022. In 2023, we’re expecting almost 1.5B NOK in annual revenues, followed by over 2.3B NOK in a steadily growing trajectory towards 2026E.

Nel ASA revenues (TIKR.com)

If we look at those numbers, the analysts following the company believe that Nel is just 3-4 years before a massive growth spurt in revenues. Not only that, analysts believe this will trickle down and allow the company to actually generate profit.

How much and when?

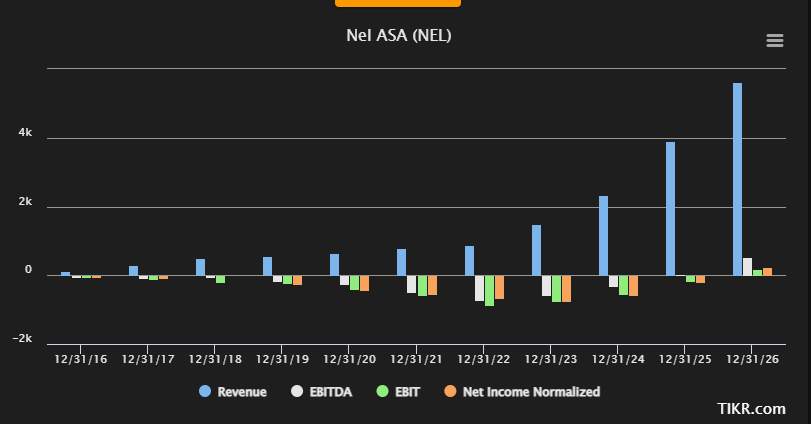

Nel ASA (TIKR.com)

Not much (compared to revenue) in 2026. That’s the year when analysts currently believe most relevant metrics will normalize to positive trends, or go positive in terms of EBIT for the first time. EBITDA will become positive, though just barely, they believe, in 2025E. Now, we don’t have accuracy statistics for these forecasts, nor can I glean any particular reason why this would be at this point, beyond the scale argument. Current calculations as these analysts have them seem to say that breakeven and when the company starts becoming profitable is at around 5B NOK and above.

To me, this is too thin to base a positive thesis on. The analysts essentially believe that GM’s will reverse to 40-45%, as the company takes on debt to fund its expansion to the tune of 4-7x EBITDA. I personally see only thin calculations for how SG&A is going to go down, or how the company is even going to turn more profitable in terms of COGS.

Nel is aware of its profit problems. The company believes that the rollout of larger factories from competitors is going to be weaker or smaller than the market expects.

Here’s a fairly telling quote from Hakon Volldal from 3Q22.

Yes. So I think when it comes to production capacity expansion, we have made a final investment decision on Line 2, which will be up and running early ’24. And then if we get additional orders, I think it’s a natural pathway to expand Heroya, the Norwegian facility to full capacity, 2-gigawatt.

We are expanding our PEM production capacity in the U.S. towards 200 megawatt initially and probably double of that for 500 megawatt over time in the existing location. But we’re also looking to establish a new gigawatt facility in North America given the high demand from North America. The exact timing will, of course, depend on site selection and funding processes. But I think we have a pathway towards during this decade, 8 gigawatt to 10 gigawatt of production capacity is what we have communicated as an ambition, and Heroya will deliver 2, maybe U.S. will deliver an additional 4 on top of the 500, so then you are at 6.5, and then you need another facility. And whether that’s in the European Union or in Australia or somewhere else, we have to come back to.

But the reason I’m saying that I think capacity, I don’t trust the capacity expansion plans is that well, if you look at what is actually installed, it’s limited, then you look at what is actually under construction, then it’s a bit more. But a lot of people just take what has been communicated as an ambition. So they put in all, Nel is going to have 10 gigawatt and it will probably be by 2025 and they do the same for our competitors. And that’s not the fact. That’s an ambition. So what is actually under construction is maybe 40% or 30% of that number. And then knowing the lead times on getting equipment, I don’t understand how all this capacity will be available. It takes time to get the equipment. It takes time to train the operators.

(Source: Hakon Volldal, 3Q22 earnings call)

I’m not arguing with any of these arguments, but to my mind, the company should already be in a position of being able to showcase at least a turnaround in margins and profitability – if not necessarily profit. Instead, record-high revenues are being balanced by record-low profits, and I’m not sure another line in Heroya will really be the differentiator here in terms of turning profitable.

I fear that Nel may be a company that’s done the hard R&D and done all the “mistakes”, which other manufacturers with scaling and efficiency experience will pick up on and “do it better”, regardless of what the company believes here.

Until I see a turnaround or a plan for profitability – and the company doesn’t disclose forward gross margin numbers because it wants to keep these a secret – I don’t see a good thesis for investors to be made here. The company’s answer that we’ll have to wait for the revenues and P&Ls from those is not good enough for me, because it calls for the faith I do not have even in a Norwegian company like this.

For that reason, this is my initial Nel thesis.

Thesis

- Nel is an interesting project – but unfortunately not yet a profitable business. As I currently judge my investments, I am unwilling at this time to put my money to work in this sort of investment.

- I’ll wait for the company to become interesting, meaning when it’s able to show me at least an indication of turning around and getting better margins. At this time, there’s too much opaqueness from the company and from the market for this.

- I don’t see Nel being worth 14 NOK – without profit, I’m unwilling to give it a PT, and I go “HOLD” here.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills none of my criteria and is therefore not to be considered a business to invest in here. I’m at a “HOLD”, but I will watch Nel for changes going forward.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment