JamesBrey

Since I last pitched The Necessity Retail REIT’s (RTL) two preferred stocks as a nice 8%+ yielding source of income back in July 2022, these two preferreds have continued to slide in price, rendering their yields even higher.

The two preferreds I’m referring to are:

Back in July, these two preferreds were trading around 10% below their par value of $25. Today, that discount is 16-19%.

RTLPO looks particularly attractive at nearly a 19% discount to par value (almost 23% upside) and a ~9.1% dividend yield. The call date is not until December 18th, 2025, compared to RTLPP’s March 26th, 2024, giving investors almost three more years of guaranteed income.

Of course, that “guarantee” comes from RTL and ultimately from AR Global, the external manager of RTL (along with a few other poorly performing REITs). While I would not touch the common stock of any REIT managed by AR Global with a ten-foot pole, the preferred stocks for RTL look very attractive as a source of high income.

Let’s get a brief overview of RTL’s portfolio and balance sheet before we explore why RTLPP and RTLPO are good and safe sources of high income.

Brief Overview of The Necessity Retail REIT

Formerly called American Finance Trust (AFIN), RTL recently completed a transformative acquisition of multi-tenant retail properties while simultaneously selling most of its office properties.

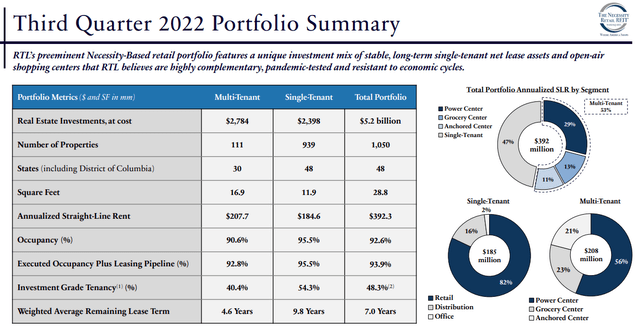

Today, slightly under half of its portfolio is in single-tenant net leased retail and logistics properties, while slightly over half is in various multi-tenant shopping centers.

RTL Q3 2022 Presentation

Around 57% of the portfolio by rental revenue is located in the Sunbelt, with 33% of rent coming from Georgia, North Carolina, Florida, Texas, and South Carolina. The vast majority of properties are clustered in the Eastern third of the United States, with very few on the West Coast.

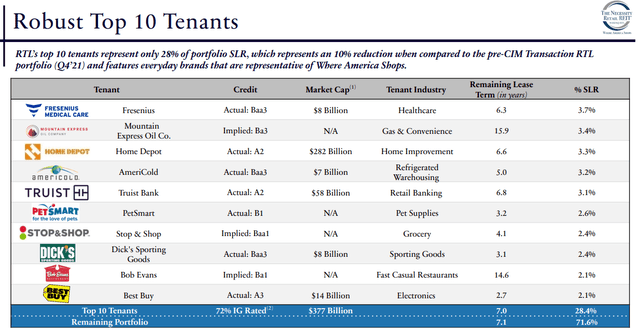

Though AR Global as the external manager is incentivized to issue shares and grow the portfolio (regardless of whether it produces AFFO per share growth), RTL’s portfolio really isn’t a bad one in terms of quality. The REIT has quite a few strong tenants in its roster, and the name “Necessity Retail REIT” does seem appropriate in terms of tenant industry concentration in essential retail.

RTL Q3 2022 Presentation

My gripe with RTL isn’t the portfolio. It’s the financial management.

The balance sheet is perpetually weak, loaded down with heavy leverage. This big debt load, combined with misaligned management, makes RTL’s common share perpetually weak. And with a sub-investment grade credit rating of BB+, RTL has neither a low cost of equity nor a low cost of debt.

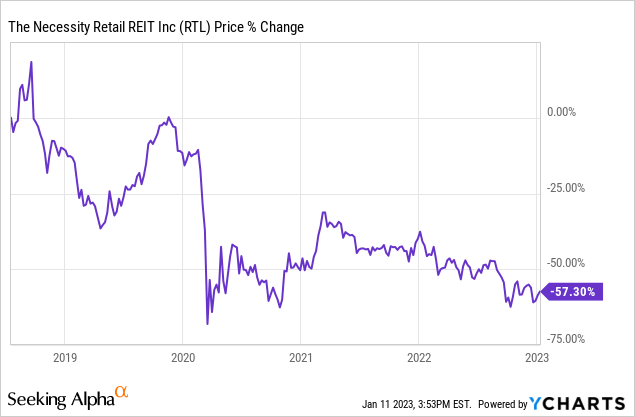

And yet, the company continues to issue plenty of equity and debt, because management is incentivized to do so in order to grow the portfolio. RTL shareholders don’t enjoy any sustained AFFO per share growth and instead are handed dividend cuts every several years. Hence the poor performance of RTL over its relatively short lifespan so far:

Let’s take a look at the following financial summary below to get a sense of what I’m talking about.

RTL Q3 2022 Presentation

Notice a few things:

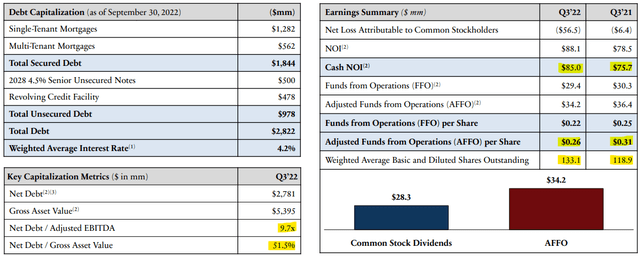

- In the lower left side, net debt to EBITDA of 9.7x is extremely high for a net lease or shopping center REIT. Most REITs in these sectors have net leverage ratios below 6x.

- Likewise, though net debt to gross asset value is 51.5%, total debt to GAV is a bit higher at 52.3%. While that would be low in the private equity real estate world, that’s pretty high for a REIT.

- In the bottom right corner, notice that weighted average common shares outstanding grew ~12% year-over-year. If RTL’s stock was valued high enough, this dilution would have been worth it, because it would’ve added to the bottom line. But RTL shares were not valued highly – even less highly now.

- On the right side, notice that cash NOI of $85 million rose 12.3% YoY. Nice! But given the growth in common shares outstanding, cash NOI per share of $0.64 remained perfectly flat YoY. Not so nice.

- Likewise, notice that AFFO per share actually shrank YoY, despite the huge acquisition of shopping centers from CIM.

- Actually, total AFFO declined YoY as well due to higher interest expenses and G&A expenses.

Any value created by the big acquisition in the last year was claimed by the external manager.

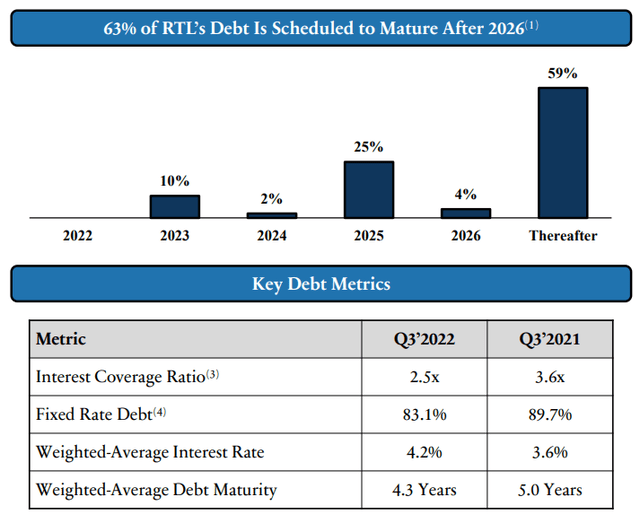

Fortunately, RTL has relatively little debt maturing this year – 10% of the total. That will almost certainly need to be rolled over at higher interest rates, but it should remain manageable.

RTL Q3 2022 Presentation

Another casualty of the big portfolio transformation over the last year has been RTL’s interest coverage ratio. That’s not a good sign for preferred stock shareholders, as debt service has to be paid before preferred dividends.

The good news is that management plans to sell over $250 million of assets and use the proceeds to deleverage.

Hopefully some of the proceeds will go toward paying down the $478 million in borrowings on the floating rate credit facility, making up about 17% of total debt. The rest of RTL’s debt (83% of the total) is fixed rate. Perhaps instead it will go towards repaying the 10% of debt maturing this year.

RTL Preferreds Look Safe

Wading through RTL’s financials just makes you want to take a shower, doesn’t it?

Well, I promise you’ll feel much cleaner looking at the preferred stocks. While the common stock dividend looks perpetually on the knife edge of being cut (pardon the pun), the preferred dividends are much better covered.

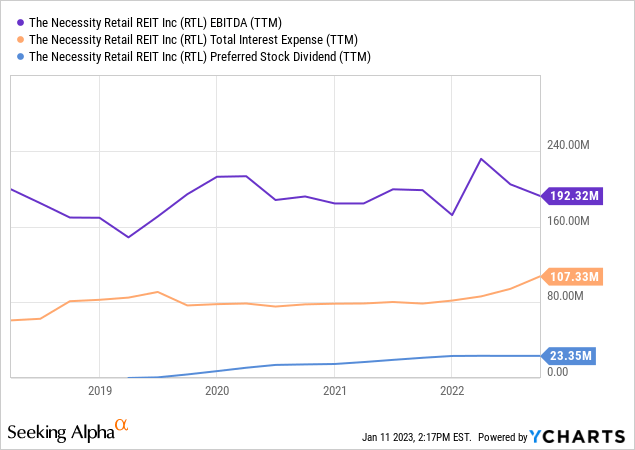

Take a look, for instance, at this chart (maybe not precisely accurate but generally truthful):

Over the last twelve months, EBITDA has comfortably covered interest and preferred dividends.

Though interest costs are rising along with interest rates, RTL still had ~$85 million in earnings after interest with which to cover $23.35 million in preferred dividends over the last twelve months. That’s a coverage ratio of 3.6x, or a “preferred payout ratio” of 27%.

Let’s use some actual numbers from the company, zooming in on the most recently reported quarter:

- In Q3 2022, adjusted EBITDA rose 17% YoY from $91.9 million to $116.2 million.

- Subtracting $32.4 million in interest expense in Q3, we arrive at $83.8 million in adjusted EBITDA minus interest costs.

- Compare that to $5.84 million in quarterly preferred stock dividends for both Series A and Series C.

The external manager’s empire building actually benefits preferred shareholders. You see, a larger portfolio almost certainly translates into higher EBITDA. If the company grows the portfolio using a combination of common equity and debt, then interest costs almost certainly won’t rise as much as EBITDA.

Thus, since preferred dividends have to be paid before common dividends, the prefs benefit from the EBITDA growth generated by portfolio expansion, even if said portfolio expansion is not accretive to RTL’s AFFO per share.

Now, interest expenses almost certainly rose in Q4 2022 and into Q1 2023, but I highly doubt it will be enough to threaten the safety of the preferred dividends, given the 2.5x interest coverage from Q3 2022.

Given the fact that only 12% of RTL’s debt matures through 2024, as well as the fact that the company plans to sell some assets in order to deleverage (hopefully reducing interest costs more than EBITDA in the process), RTLPP and RTLPO should only get safer going forward.

RTLPO in particular looks attractive for the high-income seeker, as it offers a safely covered 9% dividend yield as well as 19% upside to par (compared to RTLPP’s slightly less than 9% yield and 16% upside to par).

Be the first to comment