gerenme

Introduction

When the global energy shortage hit markets early in 2022, Natural Resource Partners L.P. (NYSE:NRP) played their hand very well. To give credit where due, they exceeded my expectations, as my previous article discussed. Subsequently, operating conditions have continued to perform better than envisioned and when looking ahead, they are transforming the appeal of their units as they push towards their zero-debt goal.

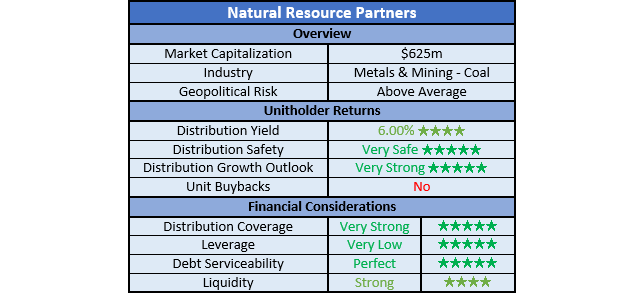

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

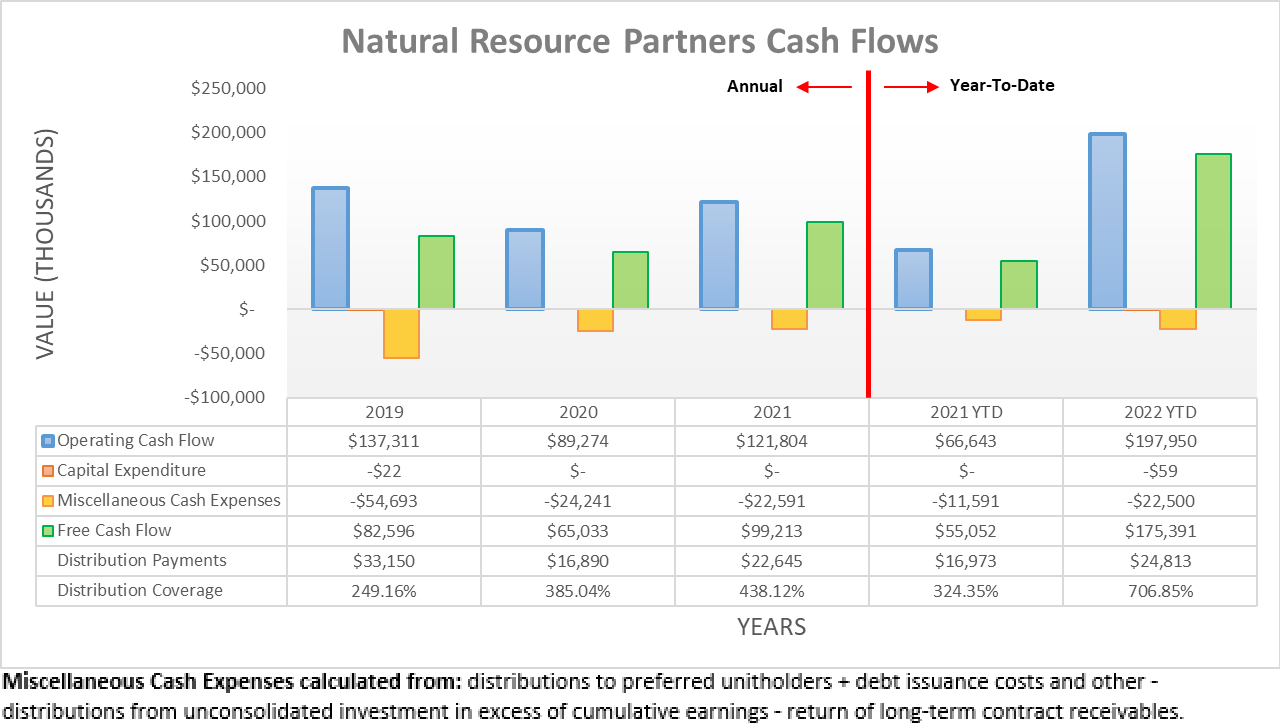

The start of 2022 was extremely strong for the energy sector, especially those with coal exposure, as the Russian invasion of Ukraine sent the world into a severe energy shortage, thereby lifting all proverbial boats from natural gas to oil and even the often-hated, coal. To my surprise, these booming operating conditions persisted well past the second quarter and thus, as a result, their operating cash flow surged ahead during the third quarter, thereby hitting $198m across the first nine months. This once again marks a massive change year-on-year against their previous result of $66.6m across the first nine months of 2021.

Author

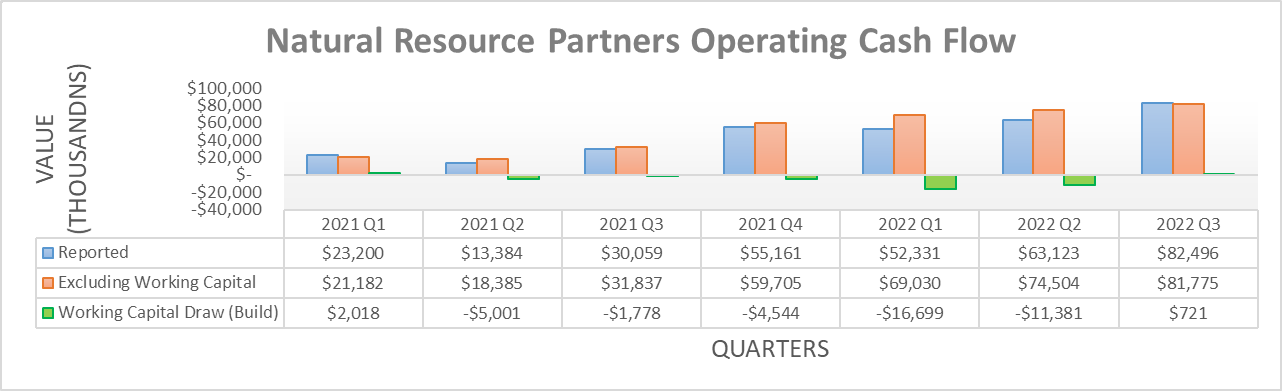

When moving to a quarterly basis, it shows the third quarter of 2022 marked the fifth consecutive sequential improvement at the underlying level that excludes working capital movements with a result of $81.8m. Since both thermal and metallurgical coal prices have remained strong throughout the recently ended fourth quarter and thus far into 2023, notwithstanding their usual volatility, Natural Resource Partners L.P. should continue seeing at least a few more quarters of booming cash flow performance, if not possibly longer as China reopens its economy.

Whilst this is undoubtedly positive, it does largely come down to luck because coal prices are not the actions of management. That said, Natural Resource Partners L.P. continues to play its hand very well. In light of these booming operating conditions persisting longer than I previously envisioned, it is actually transforming the appeal of their units as they push towards their zero-debt goal, as per the commentary from management included below.

“We have seized this opportunity to accelerate our plan to become debt-free and redeem all of our preferred units.”

“We look forward to becoming debt-free as our business continues to generate cash.”

-Natural Resource Partners Q3 2022 Conference Call.

Apart from obviously reducing risks, hitting their zero-debt goal would also provide a significant boost to their cash flow performance going forwards, thereby boosting the appeal of their units. Whilst this stands to help every year, the most notable benefit comes in years with normalized coal prices because during these times, their interest expense weighed down their operating cash flow far more significantly.

Take 2021 for example. Natural Resource Partners L.P. generated operating cash flow of $121.8m, but importantly, this was weighed down by interest expense of $38.9m. If removed, this would boost their result by almost one-third, which is a very impressive change, all without requiring either higher coal prices, higher production nor lower costs. This would translate into their accompanying free cash flow, thereby boosting it from $99.2m to $138.1m. Thus, even with these normalized operating conditions, they would see a massive free cash flow yield of over 20% at their current market capitalization of approximately $625m.

Whereas, take the first nine months of 2022, for example, they generated operating cash flow of $198m in conjunction with interest expense of $22.6m, which means it was weighed down a less painful circa 11%. Therefore, this highlights how the benefits of reaching their zero-debt goal boosts their appeal during normalized operating conditions and downturns more notably than during these recent booming operating conditions. Apart from increasing the scope for unitholder returns, this also reduces the downside risk, which in my eyes is equally as important as lifting upside potential and thus transforming the appeal of their units.

When it comes to operating cash flow, it can either be retained to boost their cash balance, utilized to deleverage via repaying debt, returned to unitholders via distributions and unit buybacks or if not, it can be invested in growth. Seeing as they are a mineral rights partnership, they run with virtually no capital expenditure and throughout their previously linked third quarter of 2022 conference call, I could see no discussions of acquisitions or mergers. Whilst this may change in the future, as it stands right now there do not appear to be any concrete plans in this regard.

Now circling back to the other paths, this leaves Natural Resource Partners L.P. unitholder returns as the most likely viable path once reaching their zero-debt goal, which is positive. That said, it remains unknown how these would be split between distributions and unit buybacks, the latter of which I hope they avoid. Apart from the inherent volatility of their industry making it more likely to see these weighted towards the top of the cycle when free cash flow is highest, along with their unit price, Natural Resource Partners L.P. also faces long-term threats from the clean energy transition given their thermal coal exposure.

Elsewhere, management noted an accompanying goal of redeeming the entirety of their preferred units, thereby also eliminating their preferred distributions. When it comes to this goal, it is done at a steady rate whilst they continue making the associated distribution payments and thus does not require additional consideration, as per the commentary from management included below.

“They are perpetual. And they are preferred equity and the liquidation price is 1.85x, which decreases as we continue to pay preferred unit distributions.”

-Natural Resource Partners Q3 2022 Conference Call (previously linked).

Author

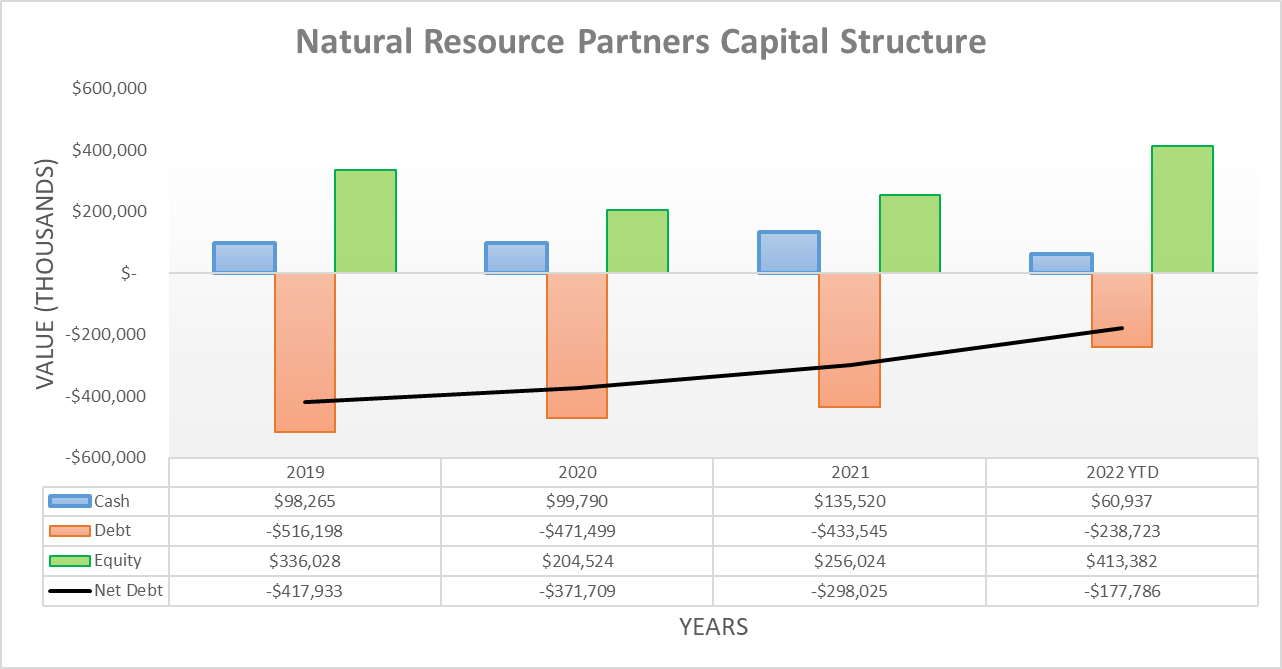

Unsurprisingly, their accelerating cash flow performance during the third quarter of 2022 translated into even faster deleveraging that as a result, saw their net debt plunge to $177.8m versus its previous level of $239m following the second quarter. It is very impressive to see one-quarter of their net debt wiped away during merely one quarter of a year and thus roughly indicates they may reach their zero debt goal following the third quarter of 2023 but obviously, it remains heavily dependent upon coal prices. Even if not this soon, it should be forthcoming not too much later and in the meantime, Natural Resource Partners L.P. interest expense should continue falling and thus unlocking more free cash flow as more quarters pass.

Since their financial position was no longer a point of concern following the previous analysis, it would be redundant to reassess their leverage and debt serviceability in detail, especially given their rate of deleveraging that could soon see these topics completely eliminated. The same can also be said for their liquidity given their cash balance of $60.9m following the third quarter of 2022 is essentially unchanged versus its previous balance of $59.4m following the second quarter.

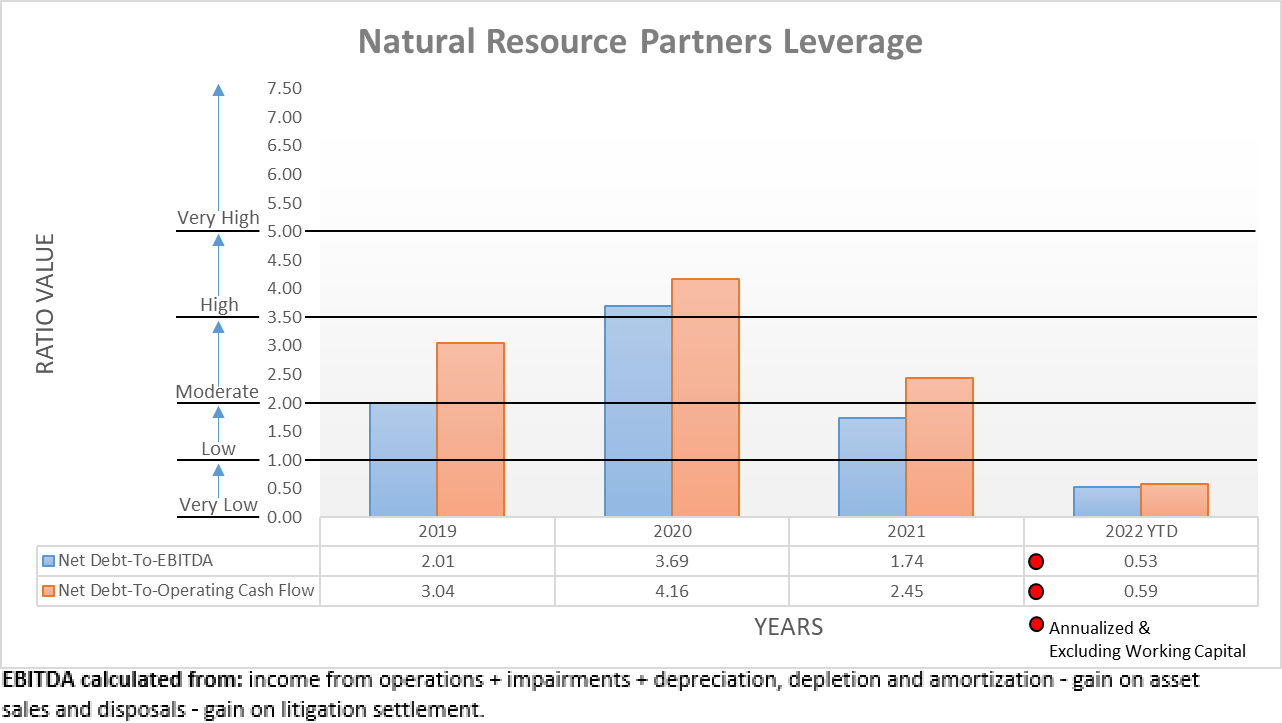

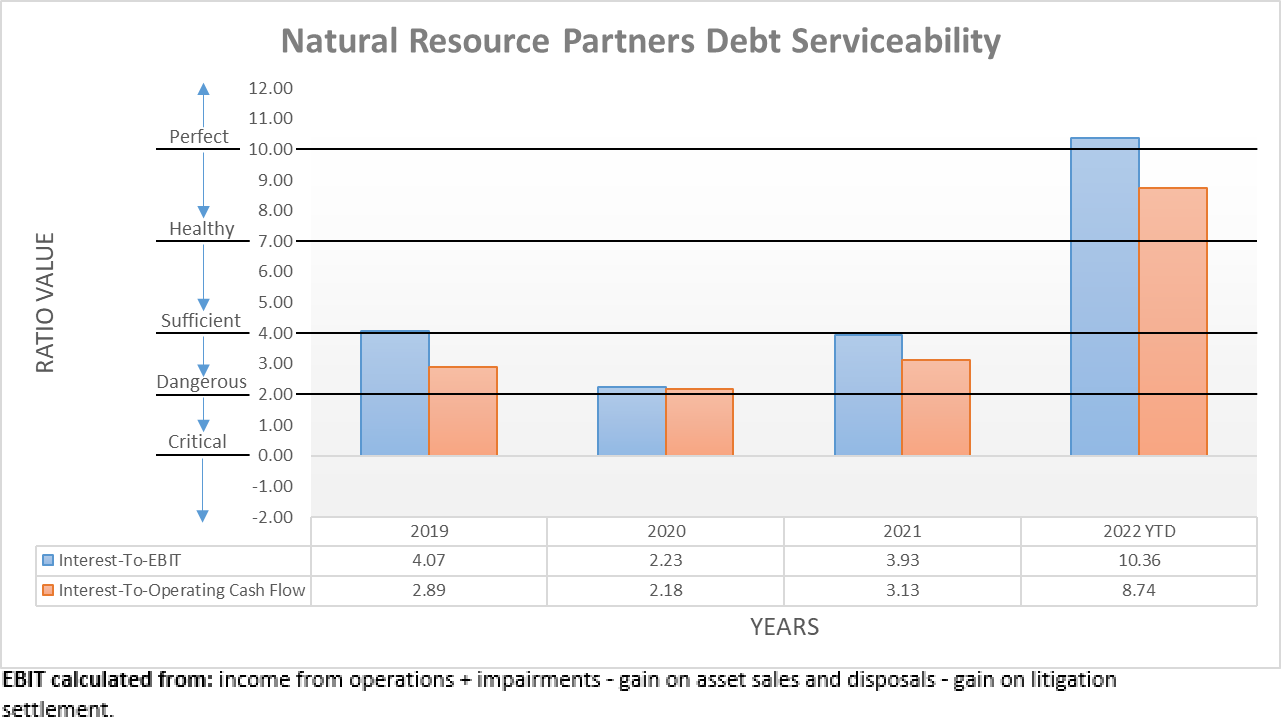

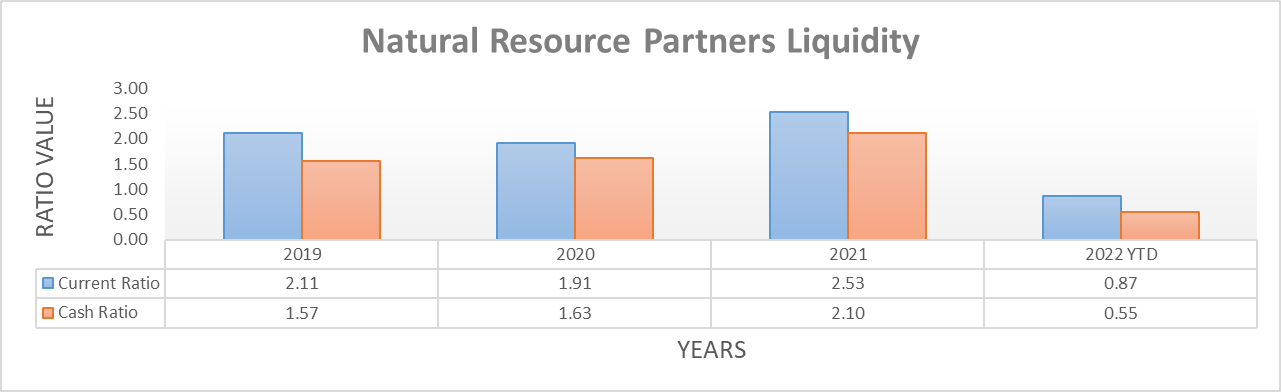

The three relevant graphs are still included below to provide context for any new readers, which to no surprise, once again shows their leverage plunging with their net debt-to-EBITDA and net debt-to-operating cash flow down to 0.53 and 0.59 respectively, thereby further beneath the threshold of 1.00 for the very low territory. Concurrently, they also saw their debt serviceability following in tandem with their interest coverage now perfect regardless of whether compared against their EBIT or operating cash flow, which yield results of 10.36 and 8.74, respectively. Elsewhere, their liquidity remains strong with a current ratio of 0.87 and more importantly, a cash ratio of 0.55. If interested in further details regarding these topics, please refer to my previously linked article.

Author Author Author

Conclusion

Once reaching their zero debt goal, quite possibly later in 2023, Natural Resource Partners L.P. will have far more cash available for unitholder returns. Not simply due to the lack of need to deleverage but more importantly, the removal of their interest expense that if utilizing 2021 as a basis, would have boosted their operating cash flow by circa one-third. Whilst this is transforming the appeal of Natural Resource Partners L.P. units even if operating conditions normalize with a massive 20%+ free cash flow yield, the question is how they will utilize this tidal wave of cash; distributions? unit buybacks? or acquisitions?

As an inherently volatile coal partnership, I hope for the first path whereby Natural Resource Partners L.P. management focuses on distributions. But, alas, until more certainty is at hand, I believe that maintaining my hold rating for Natural Resource Partners L.P. is appropriate as, in my eyes, a focus on unit buybacks would hinder their newfound appeal.

Notes: Unless specified otherwise, all figures in this article were taken from Natural Resource Partners’ SEC filings, all calculated figures were performed by the author.

Be the first to comment