In June, I spent a lot of time discussing why dividend growth stocks are the way to generate long-term outperformance in an article dedicated to Nasdaq Inc. (NASDAQ:NDAQ). In this article, I’m going to do two things. First, I will explain why quality stocks are so important – also, what’s “quality”? Second, I will update the Nasdaq bull case as the company continues to perform very well thanks to improving fundamentals.

It’s a perfect big picture for investors and I am convinced that NDAQ is a terrific way to generate long-term outperformance for both income-seeking and dividend-growth-oriented investors.

Now, let’s dive into the details!

“Quality” Is Important, Nasdaq Offers It

I want to start this article with some theoretical background. In my last article, I made the case that dividend growth stocks are able to outperform the market. That’s based on dividends offering “quality”, which gives investors downside protection in tough times. If stocks are able to keep up with the market (or even outperform) during bull markets as well, investors own the perfect mix for long-term wealth generation. Back in June, I wrote:

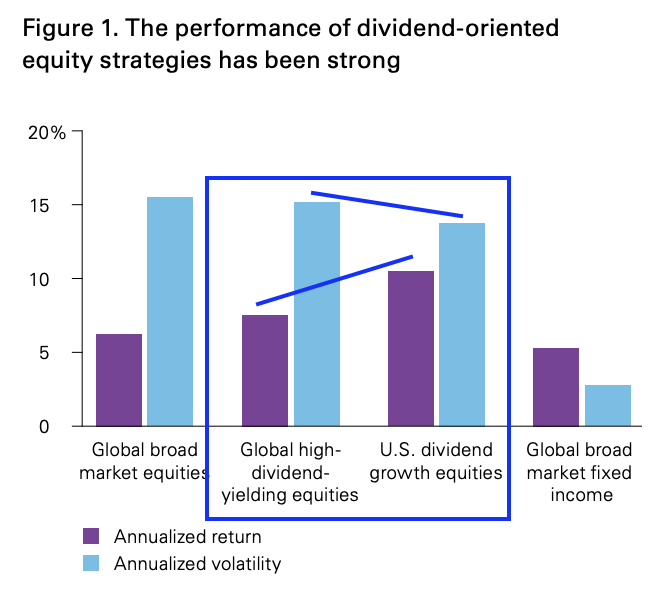

To put all things together, I found the chart below (and modified it a bit). Vanguard found that between 1997 and 2016, both high yield and dividend growth stocks outperformed global equities. Moreover, dividend growth outperformed high yield. And, on top of that, dividend growth stocks did it with lower volatility.

Vanguard

Quality is hard to define. In the case of dividend growth, it’s a stamp of approval because making a profit isn’t easy. Letting shareholders benefit from one’s profit is even harder. Doing it consistently and increasing the dividend on a consistent basis is the hardest. Moreover, it protects investors against inflation in a lot of cases. That’s what I consider to be quality.

If you’re able to find a stock that offers consistent dividend growth, you often also get low volatility on long-term outperformance as the chart above shows.

In this case, I’m going a bit beyond “recycling” the information I gave you in my last article as I found more interesting evidence that explains why Nasdaq is a good stock.

In July of 2020, WisdomTree published a report making the case for quality stocks. A part of its takeaway was:

Out of all the equity factors, Quality is one of the most consistent. It has a proven track record of outperformance and it typically delivers steady returns across most market regimes. It is ideal for prolonged periods of uncertainty when a bear market rally or a deep drawdown are as likely and it is, therefore, an ideal candidate to consider for a strategic, core investment in equities

At this point, you’re probably wondering how WisdomTree defines quality. Well, this is the answer:

Quality Investing is defined as investing in companies that have some or all of the following characteristics: good management, strong balance sheet, economic moat, sound dividend policy, stable earnings, and profitable and efficient operations.

There are a million ways to interpret this. However, what I get from this are a good dividend (growth) policy and high margins. In this case, I believe that high margins cover good management, stable earnings, profitability, efficiency, and the economic moat. After all, no moat means no pricing power.

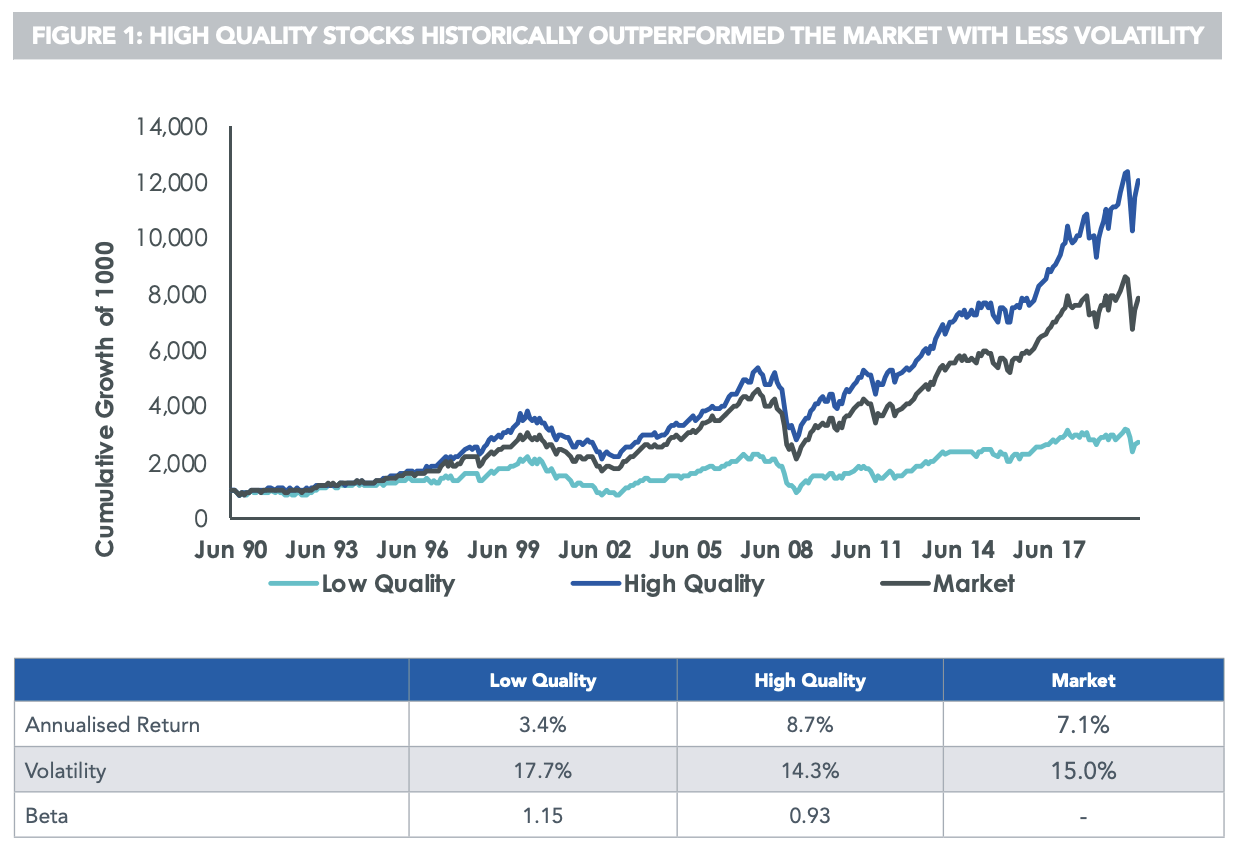

The chart below shows what the difference in performance looks like. Between 1990 and May of 2020 shows that the market has returned 7.1% per year with a volatility of 15.0%. Low-quality stocks have returned 3.4% per year with a volatility of 17.7%. That’s a terrible result. High-quality stocks have returned 8.7% per year with below-market volatility.

WisdomTree

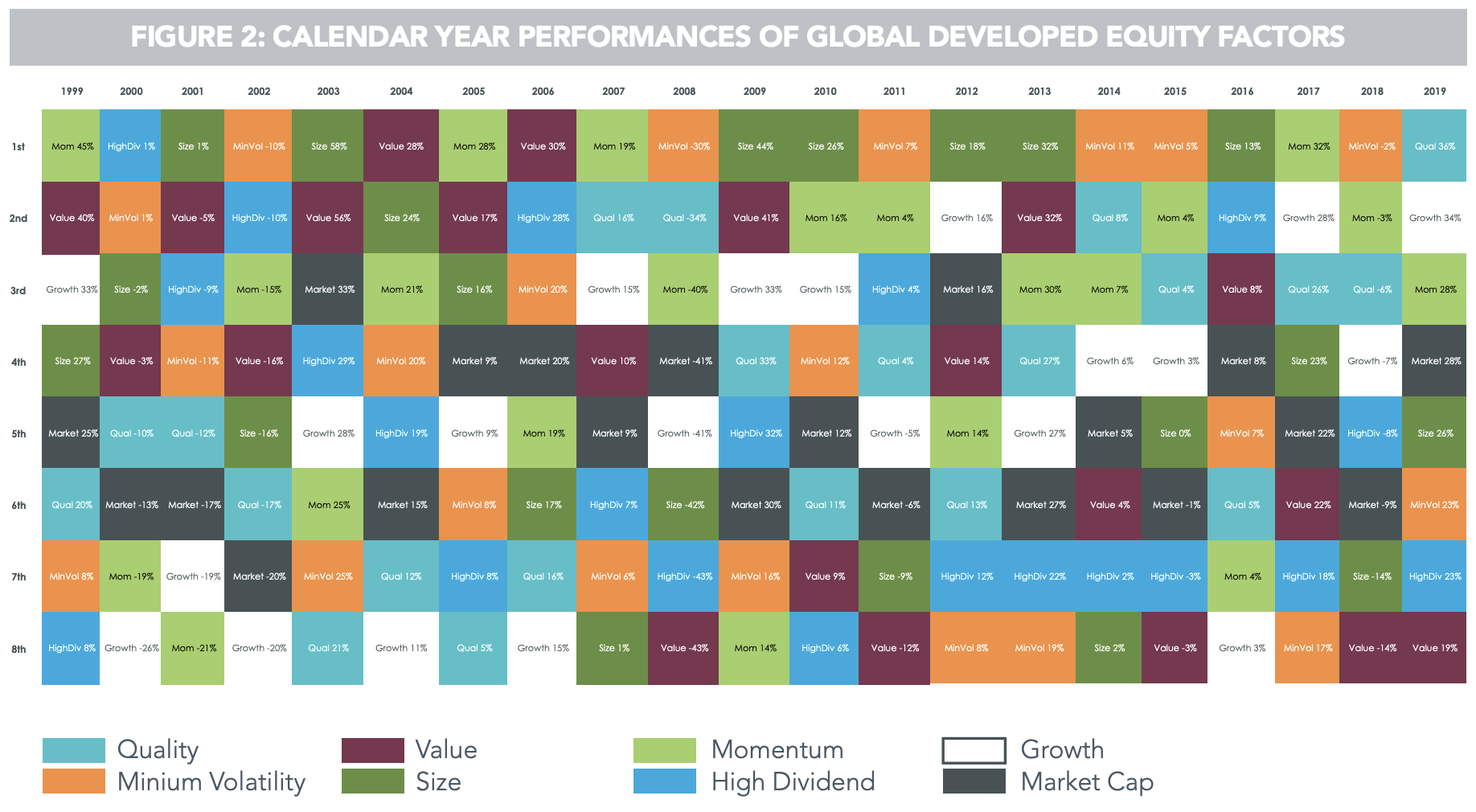

Moreover, WisdomTree included a very interesting figure in its report showing the best and worst performers per year going back to 1999. It excludes 2020, 2021, and 2022 YTD, but that’s OK for the sake of what we’re trying to accomplish here.

WisdomTree

While the performances vary per year, there are a few things worth mentioning here with regard to minimum volatility, size, and value, as these are building blocks for our definition of “quality”. According to WisdomTree:

– Min Volatility was best in negative years like 2002 or 2008 but it was last in strong equity years like 2009 or 2017. Overall, Min Volatility outperformed in 11 out of the 21 years but was top 2 or bottom 2, in 14 of them.

– Value and Size behave in an opposite way (doing well in positive years for equity and bad in bad years) but are similarly unstable. Value and Size were top 2 or bottom 2, in 14 and 13 years respectively out of 21 years.

In other words, buying quality means playing the long-term game. It means doing better in (most) bear markets and either keeping up with the market or outperforming during bull markets, depending on which stocks one buys.

Quality investing isn’t the most interesting thing to do if you like to go with the crowd for the “fun” factor. However, it makes sense and I believe that Nasdaq is a fantastic quality play.

Here’s why.

Buying Nasdaq For Quality Total Returns

Nasdaq is a company flying under the radar. When people think of Nasdaq, they think about the company-owned stock exchange in New York, or the Nasdaq Composite index.

Also, the fact that its yield isn’t very high is a reason why the company isn’t a staple in the dividend “community”.

With a market cap of $30.4 billion, Nasdaq is the third-largest stock exchange operator behind Intercontinental Exchange (ICE) and the CME Group (CME).

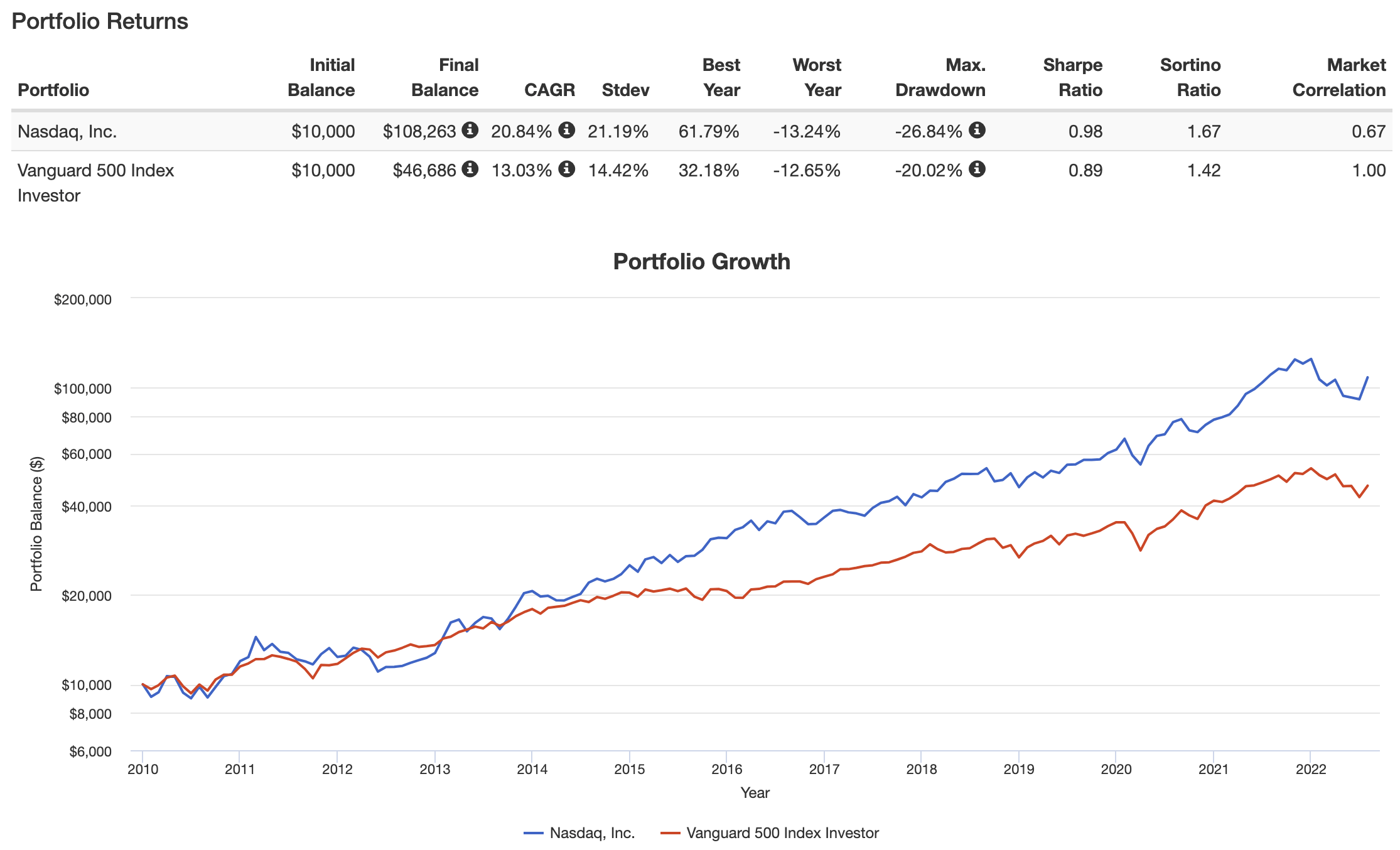

Over the past 12 years, Nasdaq has outperformed the S&P 500 by roughly 780 basis points per year, turning $10 thousand into $108 thousand. The standard deviation was higher at 21%, which is almost 700 basis points higher. However, due to the performance, the stock still did better on a volatility-adjusted basis (Sharpe/Sortino ratios).

Portfolio Visualizer

In this case, people can accuse me of cherry picking as I didn’t go back more than 12 years. I made that decision based on one reason only: Nasdaq has matured a lot during the period above, becoming a company that goes well beyond trading-dependent income.

The company checks all boxes that make it a quality stock (definition in the first part of this article), which has resulted in outperformance in almost every single year since 2008. Especially in years like 2015 and 2016 when a manufacturing recession pressured the US, Nasdaq did great. The same happened after the global growth peak in 2018 when the stock outperformed. This is all based on high margins, a stable business model, and the fact that lower rates/inflation benefit the company tremendously.

Portfolio Visualizer

Even in the challenging year of 2022, the stock is down “only” 11.5%. The S&P 500 is down 13.0%. The outperformance isn’t a lot, but it’s still remarkable given NDAQ’s huge outperformance in prior years and the fact that investors have dropped most “tech” and “growth” stocks. While NDAQ combines growth and value, it’s an easy target for sellers given its name and exposure to growth and tech stocks.

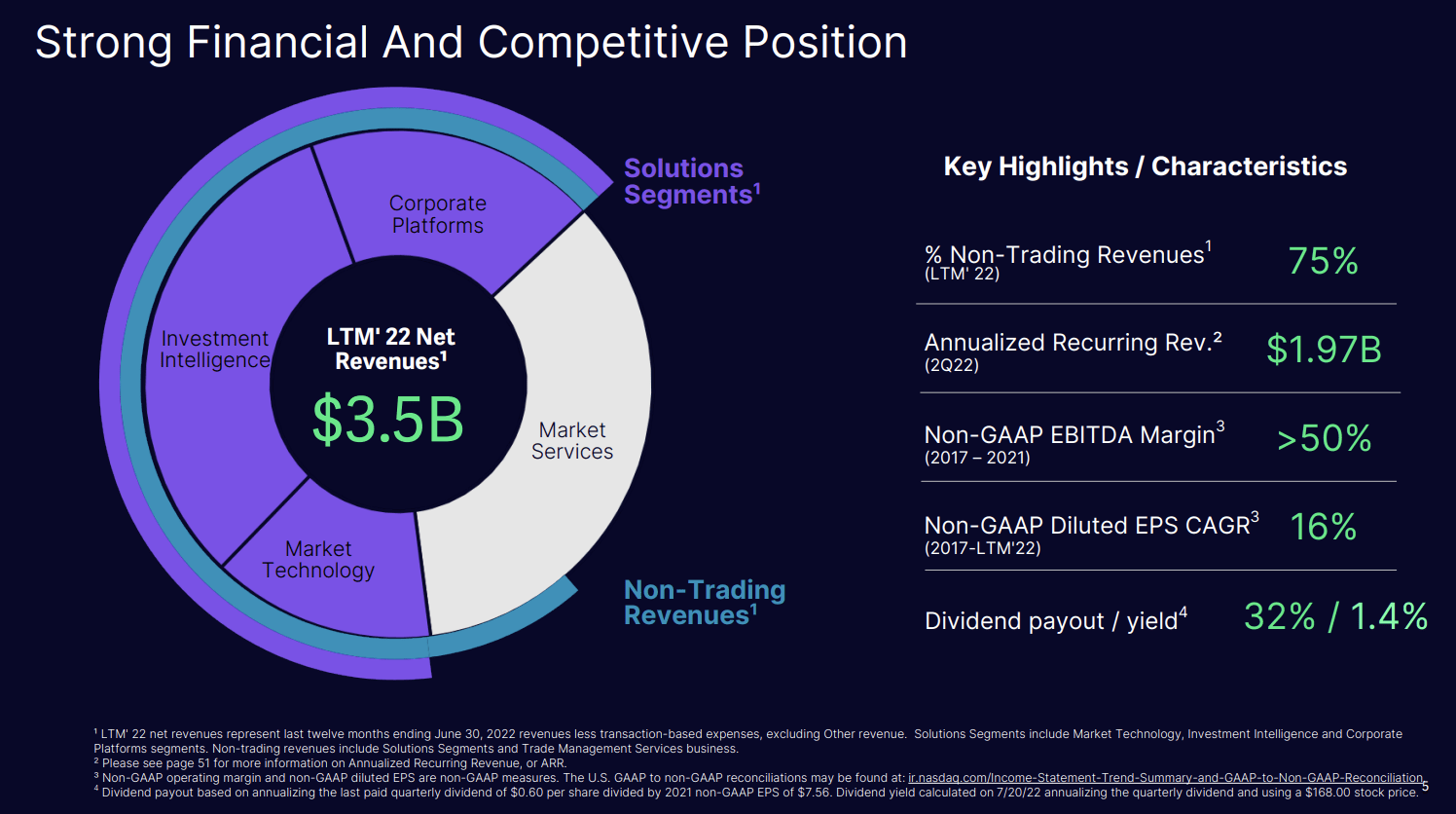

With that said, Nasdaq has become more than a company that benefits from listings, re-listings, and trading activity on its Nasdaq venues. As of 2Q22, 75% of revenues are non-trading revenues covering corporate platforms, investment intelligence, market technology, and a part of its largest segment, market services.

Nasdaq Inc.

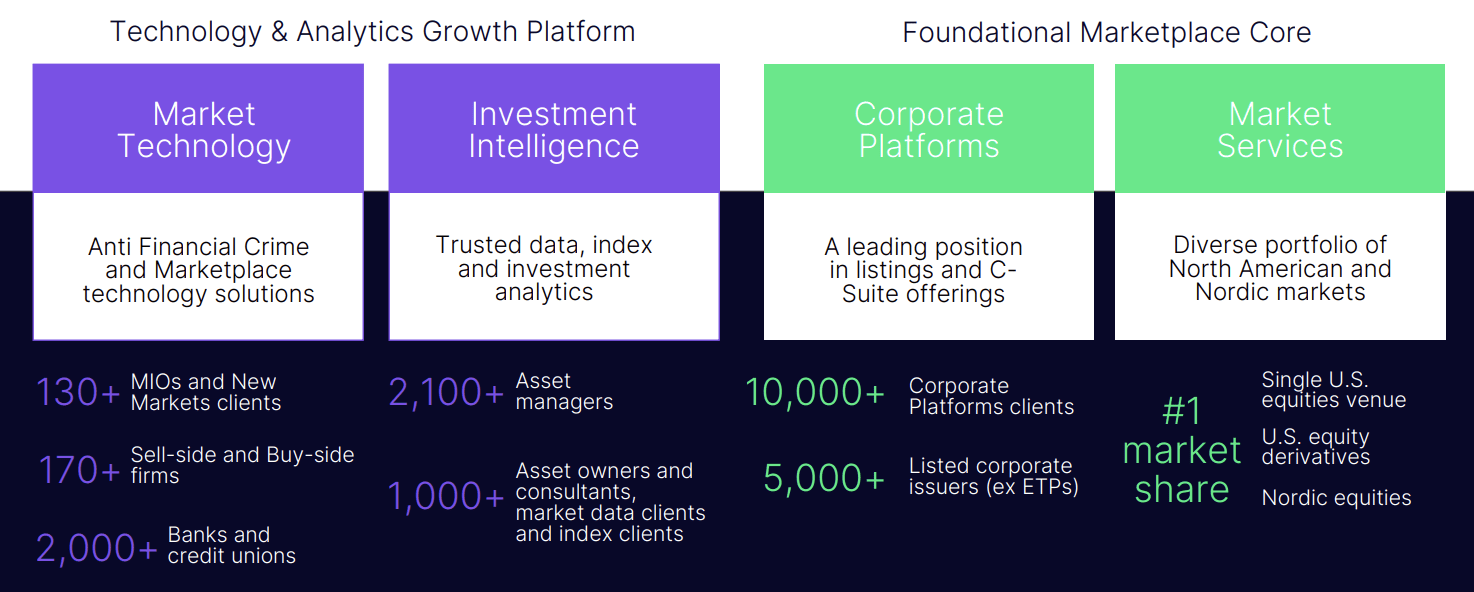

The company has now built a product portfolio that reaches major asset managers, sell-side firms, banks, corporate clients, and private customers.

Nasdaq Inc.

Since 2017 (until LTM ending 2Q22), the company has grown total revenues by 9% per year. During this period, higher-margin services have pushed adjusted operating margins up to 52%, which is 500 basis points higher compared to the starting point in 2017.

This provided the company with 16% annual compounding diluted EPS growth during this period.

Needless to say, the company is actively pushing to turn its “traditional” capabilities into high-margin services. Since 2017, market technology revenues have more than doubled. This includes anti financial crime and marketplace technology solutions. Spending on market technology and investment intelligence (including R&D) has increased 2.3-fold in 2018-2020 compared to 2015-2017.

Last year, Nasdaq completed the acquisition of Verafin, an anti-financial crime leader with 18 years of experience serving more than 2,200 customers generating 30% annual organic revenue growth (2017-2021) with 97% recurring revenue and a 98% client retention rate.

Moreover, the company did $679 million in annualized software as a service (“SaaS”) revenues in 2Q22. That’s up from $244 million in 4Q16. Total SaaS reached 35% of annual recurring revenues. The goal is to get that number to at least 40% (40-50% range) in 2025.

The good news is that the company is not seeing weakness in its progress after years of strong growth. 2Q22 earnings were a good example of that.

We delivered record quarterly revenues, 12% organic revenue growth in the Solutions segment and a 54% non-GAAP operating margin, resulting in what we see as strong momentum thus far in 2022 that we can build upon moving forward.

Now, all of this is not just good news in general, but it also supports the company’s dividend.

The Nasdaq Dividend

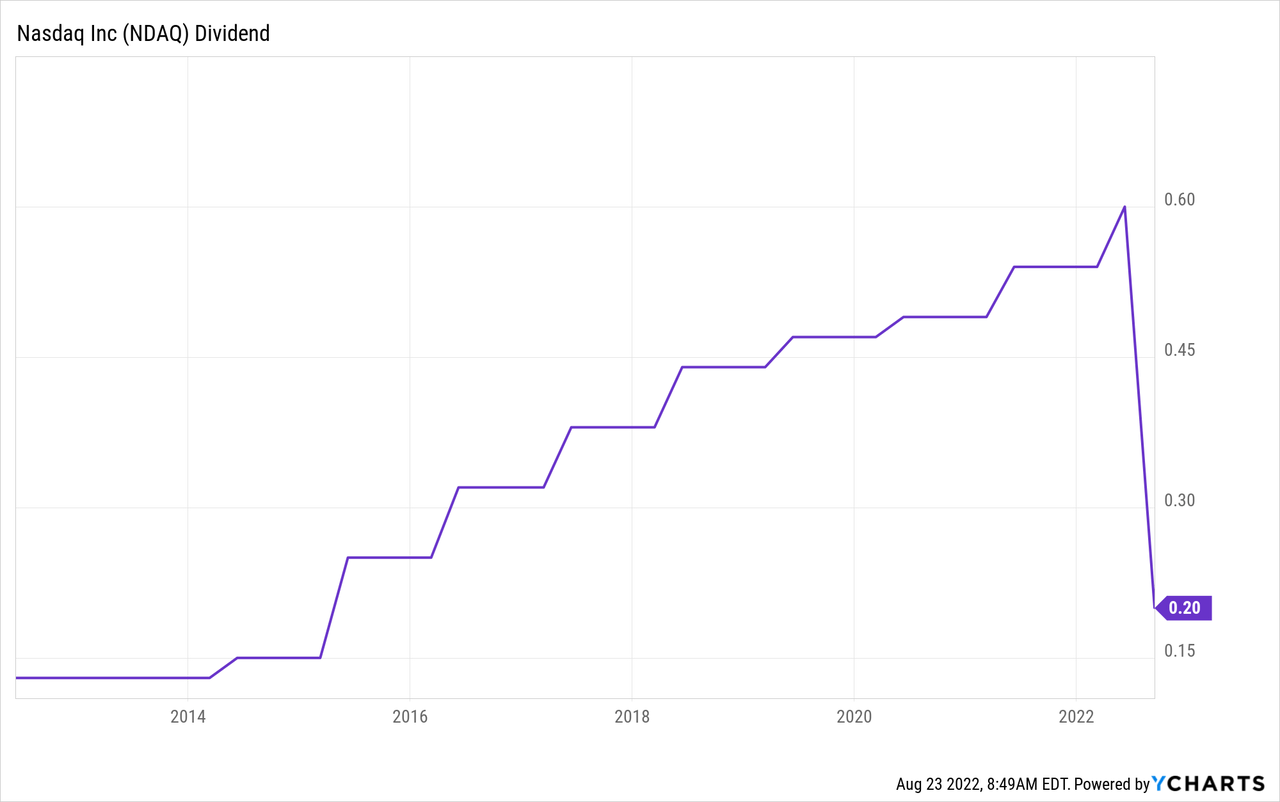

Nasdaq currently pays a $0.60 per share quarterly dividend. This translates to $2.40 per year or 1.3% of the current stock price. Now, before I continue, please be aware that the company will execute a 3-for-1 stock split in September. Meaning that existing shareholders get 3x more shares and a $0.20 quarterly dividend. Other than that, nothing changes. The yield remains unchanged.

When looking at the company’s dividend scorecard, provided by Seeking Alpha, we see that the company scores high on everything except for its yield. While I haven’t shown you the dividend growth rates yet, the 1.3% yield isn’t as bad as it may look. The problem here is that the grades below are relative grades compared to the industrial sector. That sector is known for high-yielding banks, which makes a comparison tough.

Seeking Alpha

Nasdaq initiated its dividend in 2012, since then, there have been no cuts. The decline in the chart below is caused by the upcoming stock split, which I briefly mentioned in this article. It is NOT a dividend cut.

Nasdaq has a clear capital plan as it not only aims to grow its business but also to let investors benefit from its success. As I wrote in a prior article:

First of all, it invests in growth, which is already included in free cash flow. It then maintains a 32% dividend payout ratio, which means dividend growth and earnings growth should be fairly in line. Buybacks are also used but they are NOT resulting in a lower share count. The company buys back shares to offset dilution caused by i.e., stock-based compensation.

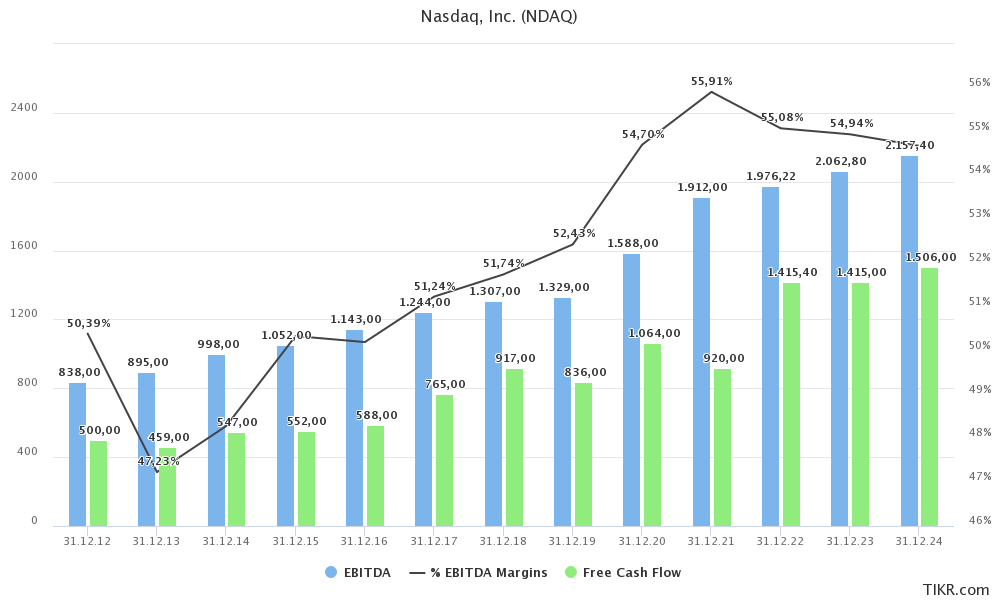

In the 2012-2024E period, free cash flow is expected to grow by 8.9% per year to $1.5 billion in 2024. Next year, FCF is expected to be similar to this year’s expected number of $1.4 billion due to slightly higher investment needs. Yet, using the company’s $30.4 billion market cap, we’re dealing with an implied FCF yield of 4.7%, which not only covers the company’s 1.3% yield, but also provides a lot more upside, especially if the company can maintain the uptrend in margins, which caused FCF to take off after 2015. Note that the company accelerated investments in its services after 2015, which provides the uptrend in fundamentals we’re witnessing below.

TIKR.com

Thanks to improving fundamentals, these are the most “recent dividend hikes”:

April 20, 2022: 11.1%

April 21, 2021: 10.2%

April 22, 2020: 4.3%

April 24, 2019: 6.8%

The Nasdaq Valuation

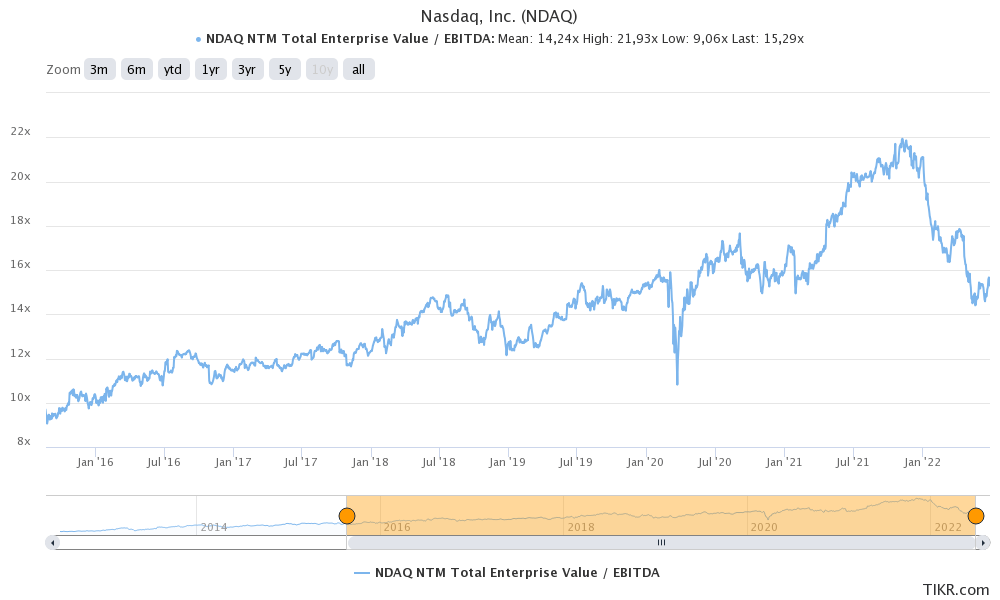

Nasdaq shares have rallied 27% from their 2022 lows as confidence in the market has (somewhat) returned. Now, the company is trading at 16.7x 2023E EBITDA of $2.1 billion, based on its $30.4 billion market cap and $4.6 billion in expected net debt.

FINIVZ

I believe this valuation is fair, but it’s not great for new (large) entries. I think new investors should start small and add on weakness whenever it occurs, or wait for weakness and start a larger position.

TIKR.com

While I remain long-term bullish, I do believe that we could encounter more weakness given that the Fed is still dedicated to aggressively hiking to fight inflation. Oil has come back up, agriculture crop prices are rising, and wage growth is heating up.

Meanwhile, economic growth is weakening, which means the Fed is forced to hike into weakness.

I’m not predicting a huge crisis, but I think we’re at a point where it makes sense to wait for 10-15% more weakness. At least, that’s my strategy. A way to avoid missing upside is buying now and adding on weakness whenever it occurs. That way, investors are not missing upside in case I’m wrong.

Takeaway

Last year, I started to push my portfolio a bit more towards lower-yielding dividend growth stocks. Nasdaq is one of the companies that perfectly fits my portfolio as it has a fantastic business model thanks to a huge footprint in trading-related activities and numerous (new) services that have emerged since then. The company is now mainly making money from recurring services.

In other words, it is a true quality stock. Like my theoretical study in this article shows, that’s a great foundation for low-volatility outperformance, which is what Nasdaq has done in almost every single year in recent history.

Moreover, the company has a 1.3% dividend yield, which I believe is a great deal for a company looking to sustain double-digit long-term dividend growth.

With regard to an entry strategy, I believe that breaking up a new investment is the way to go. For example, buy 25% now and add gradually over time. If the stock falls due to elevated economic risks, investors can average down. If the stock suddenly takes off, investors have a foot in the door.

Other than that, there isn’t much to it other than buying and waiting for Nasdaq to do the rest.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment