wilpunt

Investment thesis

Naked Wines (OTCQX:NWINF) experienced incredible growth rates during the pandemic like many others online retail businesses around the world and now it’s time for them to tackle the negative impacts of the 2020 and 2021 excessive demand, which is now winding down. I believe the company to be undervalued on an asset basis, but the fact that Naked Wines built up inventories at a much faster pace compared to revenue should point to a slow-down in the company’s top line metric over the incoming quarters. Nevertheless, I assign a buy rating to the company because its current price doesn’t reflect the true nature and value of the business in my view.

Business Overview

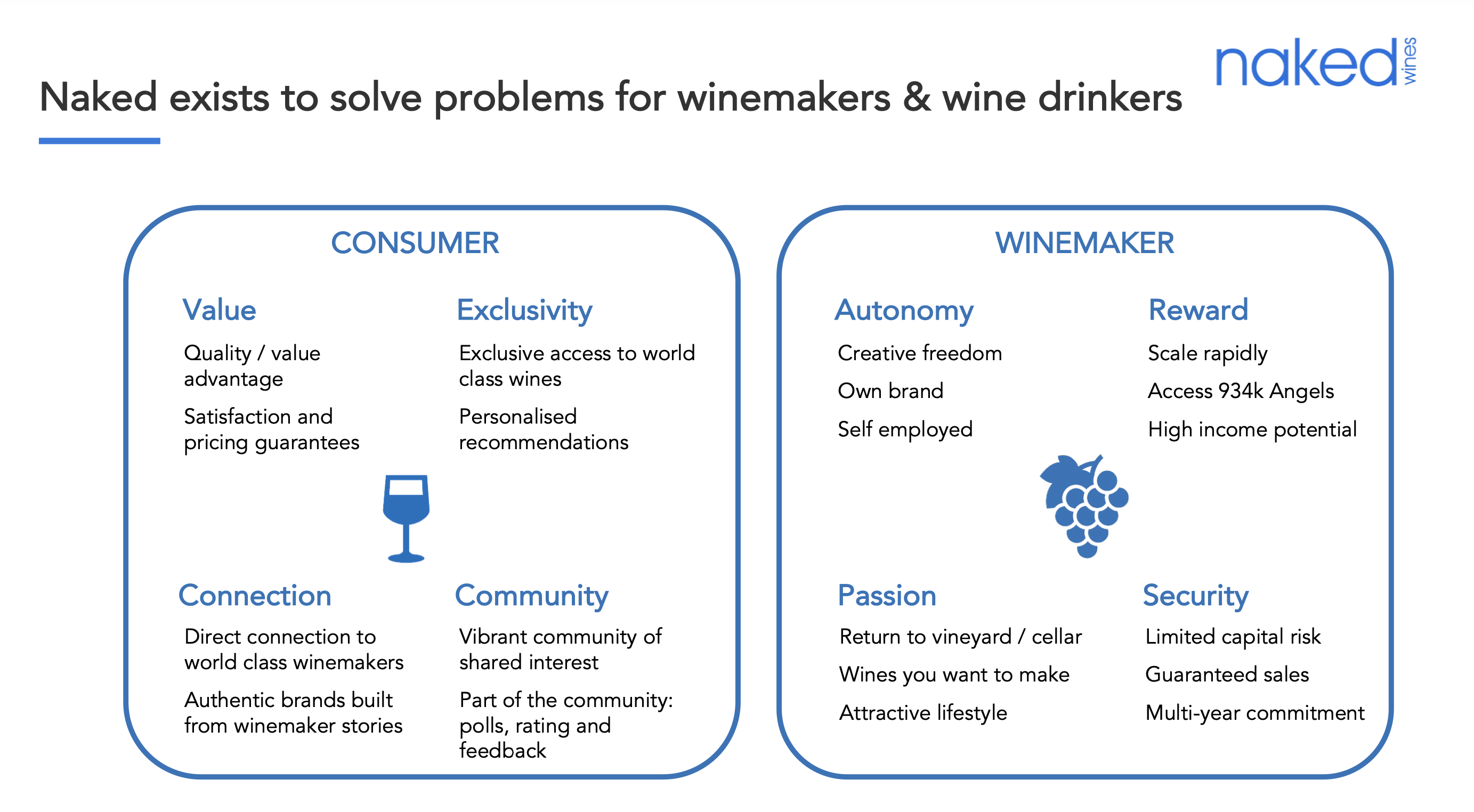

Naked Wines Plc is a vertically-integrated e-commerce retailer that operates through a unique business model that aims to bring value to all stakeholders. The company relies on a crowdfunding model to collect monthly deposits from its “Angels” (subscribers) in order to fund winemakers’ operations and cover their costs. By laying out money upfront, I believe Naked Wines allows winemakers to focus on their main activity: winemaking, without having to compromise on quality in order to cut costs.

In addition to the upfront funding, Naked Wines also offers winemakers 5-year contracts, which provide them with guaranteed order volume and long-term revenue commitments. I think this allows winemakers to work with the same suppliers, vineyards, and raw materials, leading to a closer integration across the whole supply chain.

The 5-year contracts also bring benefits to Naked Wines’ Angels, as they offer huge volume, exclusivity, lower prices for wines with the same quality (compared to competitors), and higher price discounts. I believe the lower prices are made possible by Naked Wines’ unique business model, which allows winemakers to sell their products directly to the consumer (DTC), cutting out the middleman.

A customer-centric business model

Naked Wines is a customer-centric company because it relies on its customers, or “Angels,” to fund talented winemakers, giving them the freedom to make wines the way they want to. This commitment from customers is achieved through a subscription-like model, where Angels commit to funding an “angel” account with a minimum of $40 per month. This commitment allows Angels to access discounted pricing on Naked Wines’ unique inventory.

Naked Wines

The $40 per month commitment serves several purposes that benefit both Naked Wines and its winemakers. First, it allows Naked Wines to operate with minimal working capital, as the $40 comes in before actual expenditures on the platform, enabling the company to fund inventory investment for the business. Second, it gives Naked Wines very good visibility into its forward demand, allowing the company to efficiently manage its operations.

For winemakers, the $40 per month commitment allows Naked Wines to pre-commit to a certain level of demand, giving winemakers a level of security previously unavailable in this market. It also enables winemakers to sell their wine directly to the consumer without having to persuade distributors or retailers to buy their product, which can be ineffective and time consuming.

Overall, I think Naked Wines’ customer-centric approach benefits all stakeholders, as it allows the company to efficiently manage its operations, gives winemakers a degree of security and freedom, and provides Angels with discounted pricing on high-quality wines.

Naked Wines

According to Cialdini’s commitment principle, people are more likely to be consistent and go along with a bigger idea later if they have already agreed to something small. In the case of Naked Wines, I believe the $40 per month commitment from its customers, or “Angels,” serves as a small agreement that leads to a larger commitment to purchase at least a portion of the wine they consume from Naked Wines.

This principle is based on the idea that people tend to want to be consistent with their past actions and decisions. When someone agrees to something small, they are more likely to continue to act in a way that is consistent with that agreement. In the case of Naked Wines, the $40 per month commitment serves as a small agreement that leads to a larger commitment to purchase wine from the company.

Competitive advantages

Naked Wines’ business model has several competitive advantages that contribute to its success. One of these advantages is the shared economies of scale, which allows the company to pass on cost savings to the consumer, resulting in lower prices. I believe this, in turn, leads to more subscribers and positive feedback, creating a virtuous cycle. Another advantage is the network effects that occur as the number of subscribers increases, leading to stronger connections between Angels and winemakers, a more powerful brand, and increased exposure to the best winemakers. These factors contribute to Naked Wines’ reputation, which brings in even more subscribers.

Finally, I think Naked Wines’ ecosystem control allows all stakeholders to gain value from being part of the same ecosystem. Winemakers benefit from the certainty of commitment and lower SG&A expenses, while consumers enjoy higher quality, lower prices for comparable wines, and higher price discounts. Employees at Naked Wines are also shareholders of the company through the company’s share scheme, which aligns their interests with those of the company. In addition, employees are eligible for the annual Share Incentive Plan awards and have a direct connection with the management team, which allows them to have a greater impact on business processes. The median annual salary at Naked Wines is $228,854, while the average is $87,759. In comparison, the median annual household income in the US is $63,668 and the average salary at Virgin Wines is $31,000. Finally, shareholders of Naked Wines benefit from a high return on invested capital.

Valuation

I believe Naked Wines is currently undervalued from a net current asset value standpoint. As of September 26, 2022, the company had £41.6 million cash and cash equivalents; £1.35 million in financial instruments; £9.16 million in account receivables and lastly £209.4 million in inventory, which was recorded with the FIFO accounting method. To them we need to subtract the company’s term loan of £18.7 million, bond financing of £35 thousands and £3.89 million in lease liabilities. If we divide the total net current asset value of £238.3 million by the number of total shares outstanding (74 million) we obtain £3.22/share. Compared to the current company’s market price of £1.7/share, there is a 47% margin of safety or an 89.4% upside based on the company’s net current asset value.

Risks

I believe one of the main risk the company is facing is represented by the company’s inventory trending up, which I think will be reflected in a revenue slowdown in the near future. Moreover, if the company experiences higher churn rates in the future, that might bring down both its top line and the company’s unit economics. From a macroeconomic standpoint, increasing interest rates will likely bring economies in recession by the first half of next year, translating into further short-term pain for the company.

Conclusion

Overall, I think the company looks undervalued with a 47% margin of safety. Moreover, the company has strong competitive advantages, which helps Naked Wines create a cohesive ecosystem for its stakeholders. Going forward, the management team needs to reverse the recent upward trend in inventory and starts to better handle operating expenses and its overall cost base.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment