ArtistGNDphotography/E+ via Getty Images

The following segment was excerpted from this fund letter.

The TL;DR version is that I spent 6+ months buying the most expensive $20 bottles of wine in the world. If we were to amortize our losses on this investment per bottle, I would have been far better off just buying First Growth Bordeaux.

The original investment thesis was predicated on the following points:

- Competitively advantaged business model with economies of networks from connecting niche winemakers with customers at a lower price to each party

- Aligned and competent management

- Pristine balance sheet with net cash and no debt

- Large addressable market, especially in the U.S.

- Stock that was meaningfully undervalued due to market participants overreacting to cyclical weakness in demand stemming from post-COVID reopening temporarily reducing demand for at-home wine consumption

Since I last wrote to you about Naked Wines, the following information has either come to light or become clear to me:

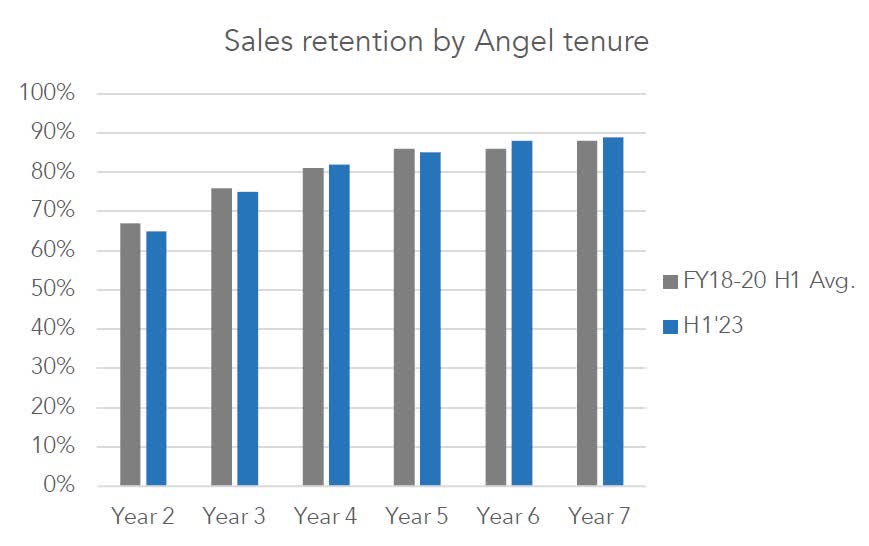

1.) It is hard for the company to demonstrate its value proposition to its customers. This is in part responsible for its low returns on marketing spend and its inability to develop a good marketing funnel outside of its mailed discount coupons. I do believe the value proposition is there – the business model removes unnecessary markups and allows consumers to buy decent wine cheaper. However, unlike some other models based on passing through of lower costs (e.g., Costco), it’s much harder for the consumer to see the value. This is because when they walk into a Costco and buy something, they know it’s cheaper than the same thing elsewhere. The value proposition is clear. On the other hand, when buying a bottle of wine that’s not sold elsewhere, it’s much harder to demonstrate to the consumer that it’s a much better deal than the alternatives as there is no direct comparator. One chart that the company recently released is how its customer retention doesn’t increase all that much the longer a customer has been with the company. That is a negative sign. In theory, if the value proposition is great, customers who have been with the company for 5+ years should be much more loyal and less likely to churn than those who have only been there for a couple of years. “To know them is to love them” if you will. That is not what the data in the following chart shows, given the very small improvement in retention as a function of customer tenure:

Source: Company H1 2023 Presentation

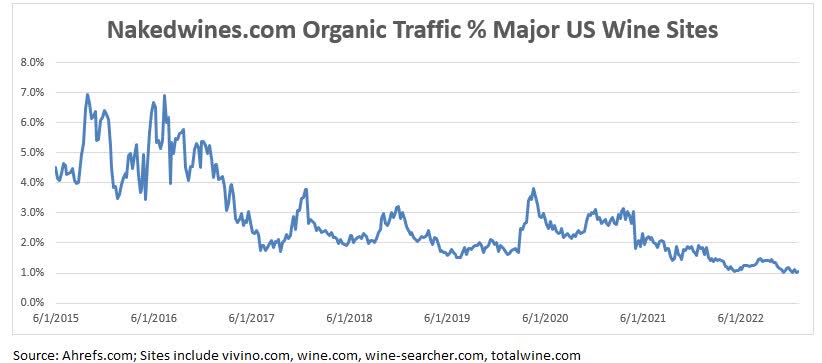

2.) The company has a meaningful competitive disadvantage in the organic reach of its U.S. website vs. major competitors. What’s more, that disadvantage is getting worse, not better. The company hasn’t shown that it can fix that, compounding its problems with building a cost-effective top-of-funnel marketing system. NakedWines.com appears to have organic traffic that’s roughly 1/5th that of Wine.com and 1/15th that of Vivino.com.

3.) The balance sheet is not as pristine as its net cash position would suggest. Given the company’s funding of its winemakers’ inventory, if there were a severe recession, the company could easily run into funding trouble and require external capital. Management has negotiated a credit line that it thinks will be sufficient, but the company hasn’t gone through a real consumer recession in its history. In other words, whether intrinsic value might be diluted or not is likely a function of things outside of the control of the management team.

4.) There have been a number of management-related developments that have not, shall we say, shown them in their best light. This doesn’t mean that they are bad or that there is necessarily something sinister afoot, but they haven’t painted themselves with glory in 2022:

- Unforced errors in communicating with shareholders, such as going radio-silent after a period of being easily available and bungling communication with the markets (e.g. pre-announcing a pre-announcement, the first time I have seen this in 20+ years as a public market investor).

- Firing of the CFO (probably the right move, but never a great sign).

- The board member representing the largest investor quitting the board after well under a year on the board. Given that this is a shareholder who is a rational value investor, that’s particularly troubling.

- The chairman resigning after “visiting” the board for about a year

I have no problem holding investments through adversity. If anything, I am frequently guilty of holding on for too long. However, in this case the problems are many and directly contradict the main points of my original investment thesis. Yes, I might look like a fool twice if it turns out that management can overcome all of these issues and restore the company on a path of growth, or if someone comes along and buys the company, which I admit is possible.

However, I have to make decisions based on the information that I have at the time. On that basis, there was material evidence that my thesis was no longer correct, and I sold our shares during Q4. I plan on following the company, and am open to coming back to it, even at a higher price, if the fundamental concerns are addressed, since I think that at its core the business model makes economic sense for consumers and for winemakers.

IMPORTANT DISCLOSURE AND DISCLAIMERSThe information contained herein is confidential and is intended solely for the person to whom it has been delivered. It is not to be reproduced, used, distributed or disclosed, in whole or in part, to third parties without the prior written consent of Silver Ring Value Partners Limited Partnership (“SRVP”). The information contained herein is provided solely for informational and discussion purposes only and is not, and may not be relied on in any manner as legal, tax or investment advice or as an offer to sell or a solicitation of an offer to buy an interest in any fund or vehicle managed or advised by SRVP or its affiliates. The information contained herein is not investment advice or a recommendation to buy or sell any specific security. The views expressed herein are the opinions and projections of SRVP as of December 31st, 2022, and are subject to change based on market and other conditions. SRVP does not represent that any opinion or projection will be realized. The information presented herein, including, but not limited to, SRVP’s investment views, returns or performance, investment strategies, market opportunity, portfolio construction, expectations and positions may involve SRVP’s views, estimates, assumptions, facts and information from other sources that are believed to be accurate and reliable as of the date this information is presented—any of which may change without notice. SRVP has no obligation (express or implied) to update any or all of the information contained herein or to advise you of any changes; nor does SRVP make any express or implied warranties or representations as to the completeness or accuracy or accept responsibility for errors. The information presented is for illustrative purposes only and does not constitute an exhaustive explanation of the investment process, investment strategies or risk management. The analyses and conclusions of SRVP contained in this information include certain statements, assumptions, estimates and projections that reflect various assumptions by SRVP and anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies and have been included solely for illustrative purposes. As with any investment strategy, there is potential for profit as well as the possibility of loss. SRVP does not guarantee any minimum level of investment performance or the success of any portfolio or investment strategy. All investments involve risk and investment recommendations will not always be profitable. Past performance is no guarantee of future results. Investment returns and principal values of an investment will fluctuate so that an investor’s investment may be worth more or less than its original value. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment