Neustockimages/E+ via Getty Images

“If Santa Claus should fail to call, bears may come to Broad and Wall.”

I have been getting requests for my predictions for 2023. Before I go into that exercise, I have to address the fact that I was calling for a year-end rally these last two months. Let’s leave aside the militant Powell, who had a very big hand in repressing the bull this year. We also had huge tax loss selling, a rebalancing for pension and sovereign funds moving funds from equities to bonds. You might be shocked to learn that this quarter stocks did better than bonds. So these institutions still adhere to 60/40 equities to bonds. Finally, there was massive “window dressing”, fund managers wanted to minimize holding the “losers” in their portfolios, so they dumped the big-cap tech names. Yes, the stock market can rally without the big caps, it just isn’t as easy to do without them.

So where will stocks be in ‘23?

Let me start off by saying it is the height of folly to actually make a projection going out for 12 months. There are so many factors to weigh, and they don’t line up neatly. Is inflation falling, yes it certainly is.

This past Friday’s core PCE ex-food and energy fell to 4.7%, which is the same level we were at way back in July. The peak was back in September at 5.2%, there is no one saying that inflation isn’t falling. The complaints are that it isn’t fast enough or that it is “sticky” and that is because unemployment is so low. Not only that but there are too many open jobs per available worker. All this is well known, yet nearly every day we are hearing about massive layoffs that are not having the desired effect. The last weekly unemployment number was just 216K, which is not a recession-level number. To me, this means that these experienced workers are being eagerly snapped up by smaller companies that desperately need their talent. I have largely repeated similar statistics for months now and probably sounds like a broken record. These stats can’t be lost on Powell’s Fed, so the question must be why is Powell so militant? Even as he’s starting to ease (going from .75% to .50%), he needs to keep pressure on the money supply. We have to acknowledge the inconvenient truth, that the stock market can gush money. Powell feels that rising wealth will add more pressure on demand which in return pushes up wages (and then inflation). So the Fed plans to go to a normal rate regime of .25% from .50%, and arrive at +5% as a terminal rate. If the rate rises to the point of throwing the US into a recession, so be it; some think Powell WANTS a recession. So the danger of the stock market remains in a bear market for several months or even the entire 2023 the Fed could care less. Because the Terminal Fed Funds Rate is expected to be +5%, a number of commentators are now talking about the S&P 500 dropping to pre-pandemic levels. With a rate this high and a looming recession, the S&P earnings expectations are just too high. The fundamental analysts expect 2023 earnings to generate only $200, and at 15 times that gives us 3,000, the technicians aren’t much more generous as they are at 3200 for the S&P. So the conclusion is, 2023 will be another terrible year.

Not so fast

Last week we were treated to the news that the final revision of Q3 GDP was 3.2%. So even as Milton Friedman says “fiscal policy works with long and variable lags’ ‘, that means that the last several rate raises may not have had their full effect. Yet, the sentence “variable lags” may also mean that most of the rate raises have already made their mark. Yet, here we have a GDP of OVER 3%. What if we not only have a rising GDP, but earnings stand up to the onslaught or higher rates? My conjecture is, earnings for Q4 will remain stable and the earnings for 2023 will be more like $230 than $200, it will get us close to the current level of the S&P 500. The dollar is falling so all the big-cap tech will be able to report more favorable international earnings with the weaker dollar. My conjecture is that now that the rate rises are coming to the end, an earnings recession will take over and slam the indexes down from 3000 to 3200. The next piece is that as inflation moves back into the background, PE ratios will re-expand, getting us into the low-4000s. I also strongly believe that the treasuries are telling us that the actual terminal FFR will be close to 4.1% to 4.49%. The economy has been operating at these elevated rates for months now. Also, the infrastructure bill should be kicking in this year, so in spite of the long and variable lags of the rate rises, the economy can not only grow, but stocks can at least maintain the current range from 3800 to 4200. Add to that, the rarity of two years in a row of a bear market is exceedingly high, so the chances of 2023 resulting in losses for stocks are low.

So where do I stand?

I hate to leave you hanging, but I truly don’t know what will happen. It really all comes down to the psyche of one man. Will Jay Powell be satisfied by the gradual retreat of inflation? Or will he continue with successive rate raises, albeit in smaller increments? At some point, the economy will finally get the proverbial “straw that breaks the camel’s back”, and then the Fed will have to furiously back-pedal. Therefore I wouldn’t be terribly surprised to see one more rate rise, before the Fed halts. I see Q1 for stock as a continuation of Q4 trading. If earnings do relatively well, stocks will treat us better than expected. So I conclude with a tepid answer, Steady as she goes. Though with one caveat, let’s watch the earnings pre-announcements. If we don’t hear of any lowering of expectations from the likes of Microsoft (MSFT) because of foreign exchange, or from Adobe (ADBE) from longer contract cycles, then the notion of a sharp sell-off because of an “Earnings Recession” just will not be there. If we have a string of warnings, and any hint of the inflation dragon rearing up then 3200 here we come.

What to do

The first rule of the Cash Management Discipline is to start trimming positions as soon as we see a known risk. Earnings season is always fraught but this Q4 has a lot riding on it. Furthermore, we need to pay attention to lowering earnings expectations announcements. Are they more in number than usual? Are the revisions deeper than usual? I have been asking the Dual Mind Community members to begin trimming 1% to 3% of old positions daily into the first week of January. Our goal will be 20% to 30% cash. I also advocate hedging; it has never been so easy to hedge as it is now. There are many inverse ETF based on the major indexes. I would wait until earnings actually begin before I would build an appreciable amount of such equities. Please study the 3X inverse ETFs. The fine print urges you to only hold them for 24 hours, so I would minimize the length of time in them for as short a time as possible. If the market sells off hard, they will perform their protective mission. However, like any powerful tool, it can work against you if the market soars. Right now this is a highly unlikely scenario but not impossible. I will not give you the symbols, please do your homework and understand what it is you are putting your dollars into.

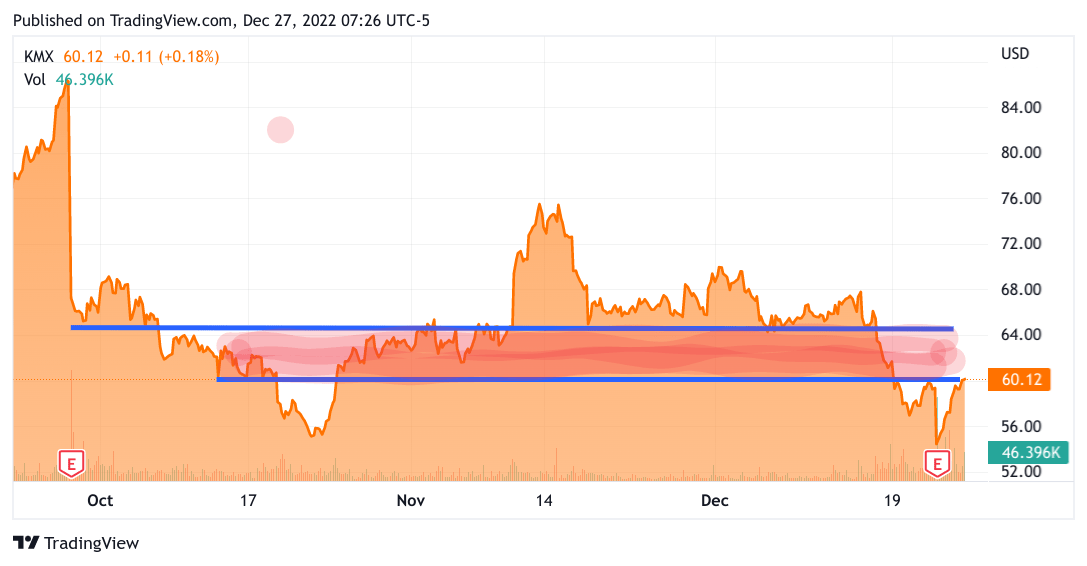

The next level is to seek out vulnerable stocks that are likely to go down anyway. It takes some getting used to but if you are comfortable with stock picking you just have to train your mind to look for the opposite of what you would normally invest in. Will the fear of recession come to reality? Hard to know, but there might be stocks that could be vulnerable to higher costs, or sharper competition, or waning consumer interest. Here’s an example, used cars. Not too long ago some recent model used cars were selling at prices higher than when they were brand new! No longer, used car prices have cratered. So if you sell used cars, you’ve already taken a hit on the expensive cars you bought just this past Fall. Moreover, new cars are finally becoming plentiful, and being offered for 1.9% financing. Imagine competing with new cars for cheap financing. It’s not just cars, of course, it’s just the best one I can think of. Maybe going after a Nordstrom (JWN) will be a better downside play. That just flew into my head but it actually sounds like a good idea, I am going to look into the “aspirational” retailers as something to go on the short side. I use Put options to generate alpha on stocks that I think are vulnerable right now. Maybe there is more of a downside to the FANG names, I will look for a way to express that with Puts. Why? This is a form of hedging as well. If I am correct and the market trades sideways or even down, the pressure on stocks that I believe are vulnerable will hopefully more than make up for the stocks I am long in. Why not just hedge on the indexes? I do both. I do both because I tend to hate being a bear. So I tend to close out my hedges on the indexes too quickly. So by looking for vulnerable sectors and stocks in those sectors, I can hold on using my conviction on a particular name. So the used Car company I mentioned is CarMax (KMX). They had a terrible ER. Strangely the stock rose after the dismal earnings report. I believe it was short covering. So today I executed some Puts on that name with a February expiration and a $60 Strike. There is no shortage of candidates to go after, unfortunately.

Below is a chart of KMX. This is a 3-Month chart and as you can see there are two parallel lines over that 60 level. This is what we call “congestion”. It is showing there is a huge supply of stranded buyers in this name anxious to be made whole. The moment the stock gets into that area there will be a deluge of willing sellers. On the other hand, there are buyers that got into KMX at under 56 just a few days ago that might want to get out while they can. All this points to selling pressure, and that is why I have Puts on it. I have no ill will to the management, nor to used car salesmen, or the used car industry. I am just trying to create some balance in my portfolio to deal with the bearish possibilities. The great thing about looking for vulnerable companies is that if the market turns toward the bulls, you may still make money on bearish bets.

TradingView

These are tough times. You can choose to close your portfolio and not look at your stocks or you can take an active hand and navigate to calmer waters. I only trade with a small portion of my portfolio. I have a long-term account that I have a completely different approach with, There I look for good dividend-paying stocks and ETFs. There are a smaller number of long-term bets that I am willing to hold and see what happens. I favor income generation most of all. Studies have shown that in times of slower economic growth, stocks with dividends generate most of their gains through income. So if my suggestion of taking an active role is not your cup of tea, there is a great opportunity in holding stocks for the long term as well.

Be the first to comment