tortoon

In 2022, we largely rid financial markets of the speculative excesses built up from years of monetary policy largesse. Near-zero interest rates and the steady medicinal drip of liquidity fueling risk asset prices became a staple for a generation of investors. That came to an abrupt end when a tsunami of fiscal stimulus combined with the war in Ukraine, and an economically-stifling pandemic policy in China, fueled a surge in inflation not seen in 40 years. Interest rates soared at a record pace, leading to the worst performing year for stocks and bonds since 2008. We saw a steady decline in the share prices of the largest technology stocks that still dominate the weightings in the S&P 500 and Nasdaq Composite. A collapse in the most speculative segments of the market included meme stocks, SPACs, and cryptocurrencies, which culminated in the demise of the FTX exchange. Lastly, Cathie Wood’s ARK Innovation fund, which is the poster child for expensive growth, lost 70% of its value.

Edward Jones

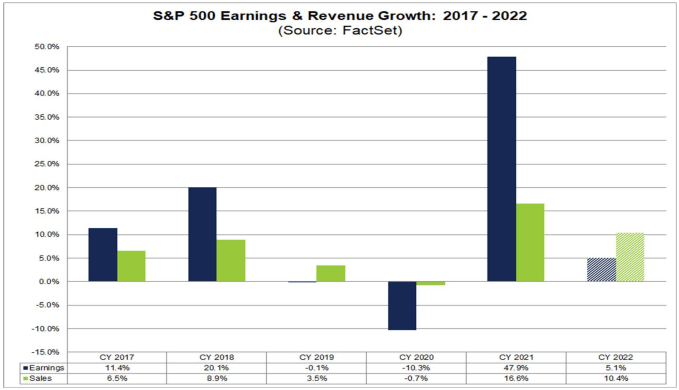

Meanwhile, the economic expansion continued in 2022 on the back of steady consumer spending growth, and the economy looks to have ended on a high note, as the Atlanta Fed’s GDPNow model estimates growth of 3.7% in the quarter just ended. According to FactSet, corporate revenues increased 10.4% last year, while profits rose 5.1%. This is impressive, given the circumstances.

FactSet

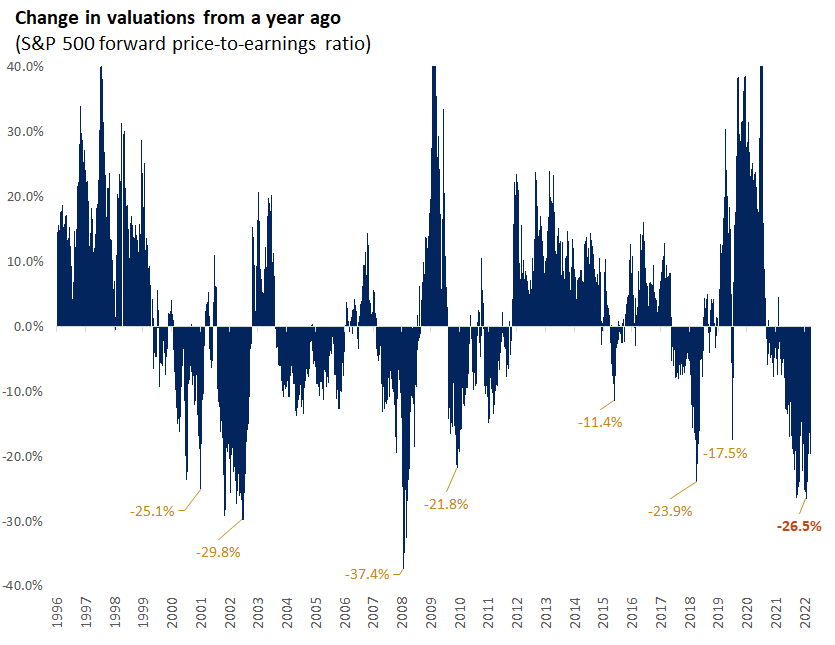

Despite this economic and corporate performance, higher interest rates and the increase in inflation weighed heavily on valuations. Yet as valuations for the majority of stocks have fallen in line with historical averages, inflationary pressures have receded, and the peak in short-term interest rates rapidly approaches, fear of a recession this year mounts. The reason is that inflation is expected to remain elevated in 2023 to the extent that the Federal Reserve continues tightening financial conditions. This could lead to a rise in unemployment and a decline in wage growth that depresses consumer spending to the extent that we realize a prolonged contraction in economic activity.

Edward Jones

In a recession, corporations would look to cut more costs in an effort to protect profit margins, resulting in additional job losses and a deeper contraction in consumer spending. Consensus revenue and earnings expectations for the S&P 500 in 2023 would be way too high in this scenario. The consensus of analysts see revenues growing 3.3% and earnings growing 5.3%. If both were to decline, instead of grow, it would significantly raise the odds that we retest, if not fall below, the October lows in the major market averages. While this is still a reasonable possibility, there are countervailing forces arguing against it, but they are being largely ignored in what has become an obsession with recession.

FactSet

The Recession Obsession

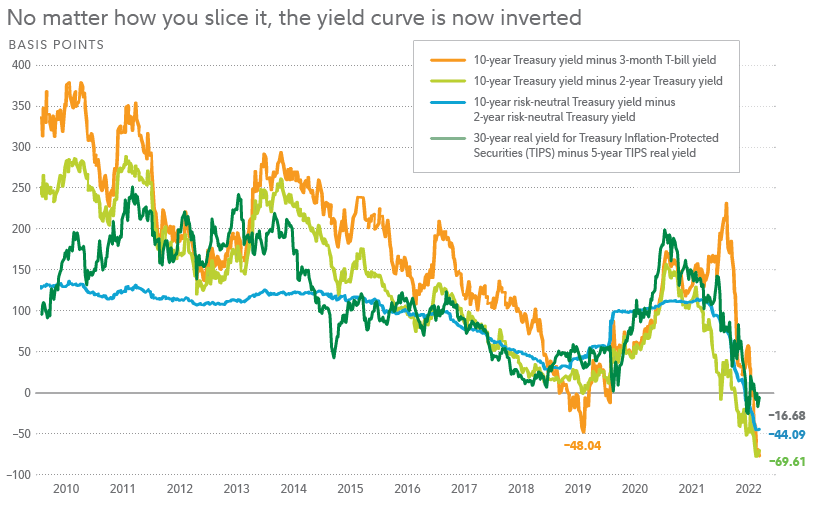

It seems like everyone has penciled in a recession for 2023, as though it is a foregone conclusion. This is because there are a handful of historically reliable economic indicators that are flashing red. The most glaring of these is the inversion of the yield curve with both 3-month and 2-year Treasury yields well above the 10-year yield, indicating that the Fed has already raised short-term rates to levels so restrictive that an economic contraction is likely to follow over the coming year.

Fidelity

We have also had a collapse in home sales, which fell 35% in November over the prior year. Sales have fallen for ten consecutive months. Home prices are starting to decline month-over-month in certain markets, and the annualized gains have been halved from earlier in the year. Additionally, the manufacturing sector looks to be on the verge of contracting modestly, as evidenced by the latest Purchasing Managers Indexes (PMIs) from ISM and S&P Global. Lastly, the Conference Board’s Leading Economic Index (LEI) is in recessionary territory, due to the deterioration in the housing, manufacturing, and consumer sentiment components. These are stark warning signs, but something is amiss.

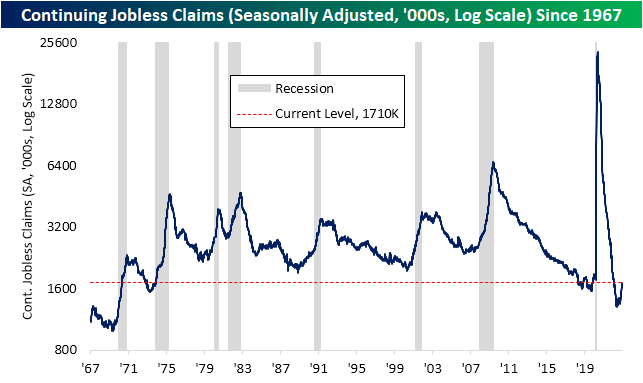

We have seen unprecedented swings in the high-frequency economic data over the past two years, due to the economic shutdown in 2020 and enormous amounts of stimulus that followed. I think this has thrown a monkey wrench into what have otherwise been reliable models for forecasting the business cycle. In many cases, standard deviations have soared. For example, look at the staggering surge in continuing jobless claims that resulted from the economic shutdown, which was followed by an equally staggering plunge. We have now seen a 25% increase in continuing claims over the past three months. Every time we have seen a 25% increase in claims a recession has followed. Yet this increase, which is entirely due to the magnitude of the decline, brings us back to what is still a historically low level. This is more of a return to normal or a revision to the mean than a sign of meaningful economic deterioration.

Bespoke

I think we are seeing similar dynamics in housing and manufacturing where supply and demand have been thrown so far out of kilter that they are distorting models for economic forecasting. We are still in the process of returning to normal, as evidenced by the dramatic shift we have seen from spending on goods to services by consumers. There is something else that is extremely unusual.

Past recessions have taken the consensus of investors and economists by surprise, which is why they are typically over by the time they are officially recognized. Consider that the Great Recession starting in January 2008 lasted 18 months and was more than half way over before the consensus realized it. If one occurs in 2023, it would be the most anticipated event on record. That has never happened before. Still, removing the surprise factor should greatly diminish additional downside in the market from what has already occurred. Remember that the stock market is a discounting mechanism in that its movements typically precede developments in the real economy by 3-6 months. Investors have been selling stocks and other risk assets in anticipation of a recession. Are they waiting to sell more once the recession is upon us? I am not convinced, but the obsession with recession is clearly blinding many to the underlying strengths of our economy today.

An Unprecedented Economic Recovery

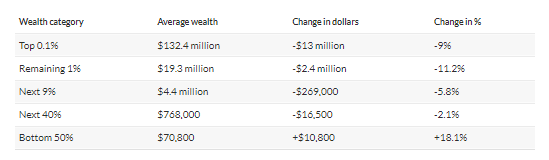

The most unique aspect of this economic recovery and ongoing expansion is that it was built from the bottom up. Recessions typically hit the working class harder than anyone else, as they are fired first, hired last, and have very little savings as a buffer in between. The post-pandemic government relief was far more meaningful for the lower class from an income and wealth standpoint than any other demographic. According to Federal Reserve data, the net worth of the bottom 50% of households rose 123% from the beginning of 2020 through the first half of 2022 compared to a 22% gain for the top 10%. Wolf Richter of the Wolf Street blog came to the same conclusion in his own analysis of Fed data, as seen below, but focused more importantly on the first nine month of 2022.

MarketWatch

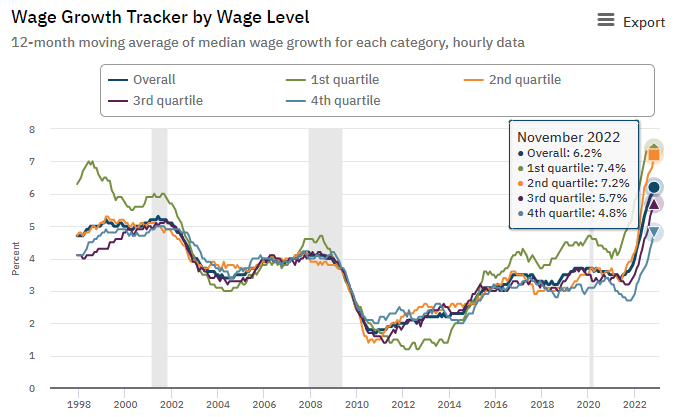

Wealth creation is not the only anomaly, as the lowest paid workers have also realized the highest percentage increase in wage gains to the extent that they are starting to realize real-wage gains as the rate of inflation falls. The information below comes from the Atlanta Fed’s Wage Growth Tracker.

Atlanta Fed

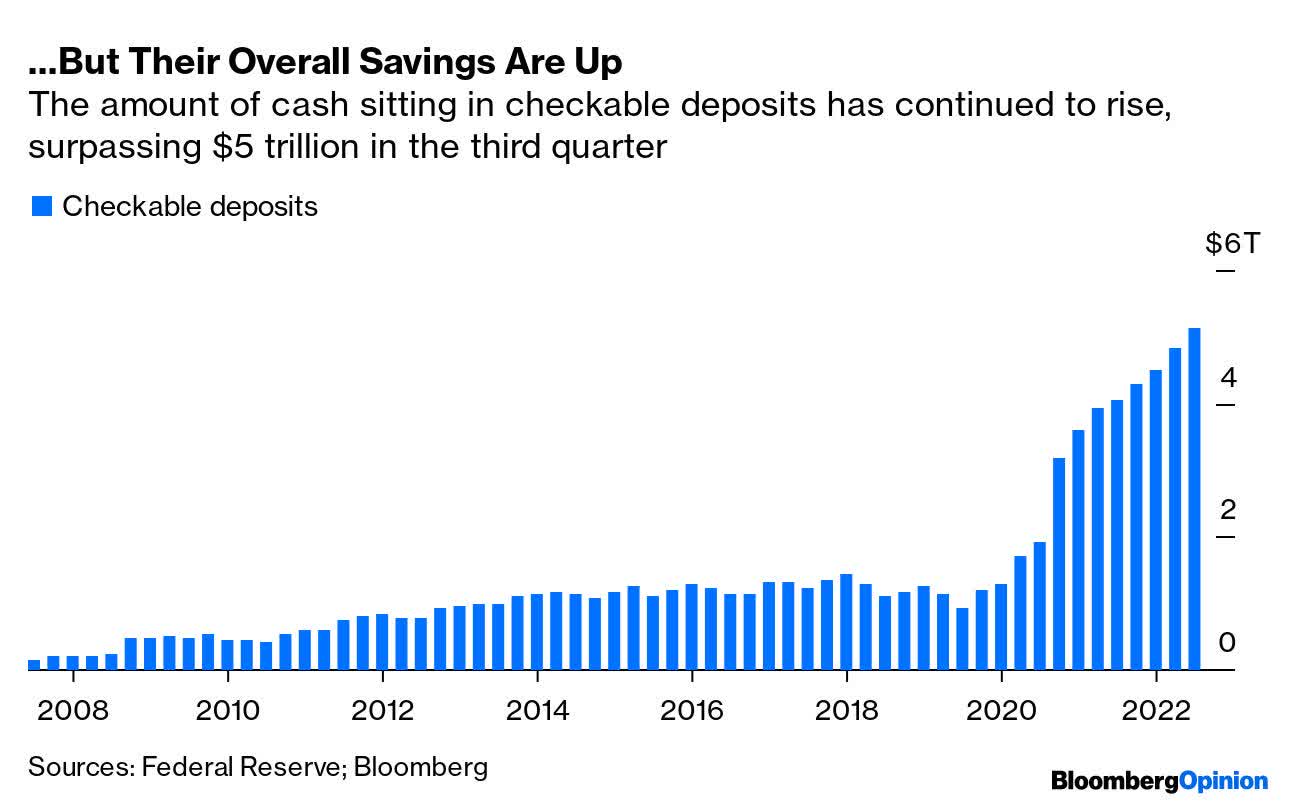

We have also continued to see a surge in overall savings, which is extremely unusual for an economy that is supposedly months away from a recession. The Fed’s latest quarterly Flow of Funds report shows that checkable deposits for households and nonprofit organizations rose to a record $5.12 trillion at the end of September.

Bloomberg

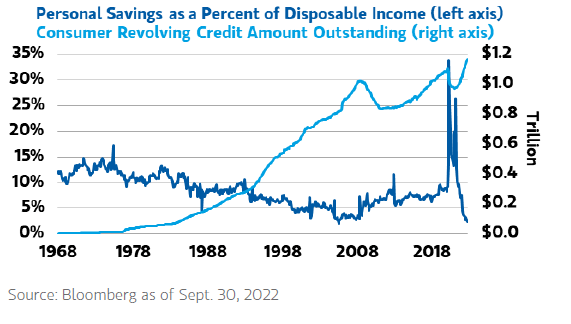

Those who are more pessimistic point to the increase in revolving credit card balances above pre-pandemic levels and the drop in the savings rate to a 17-year low of 2.7% as indications consumers are strapped. First of all, it is normal to see credit card balances rise along with increases in wealth and income, as the economy grows. Regardless, the debt-to-disposable income ratio remains near historic lows, and that is what is most important.

FRED

As for the saving rate, it has taken the same unprecedented swing up and down that we have seen in continuing jobless claims. Both are anomalies that should revert to their means.

Bloomberg

The bottom line is that the foundation for this ongoing expansion has never been stronger, because it was built from the bottom up. In addition, corporations have solid balance sheets, and the banking system has never been better capitalized. This is why the expansion continued in the face of soaring interest rates and inflation. It is also why I think the economy can navigate a soft landing, despite the fact that financial conditions continue to tighten.

Rates Of Change Are Improving

Markets respond more to rates of change than absolute numbers. The most important variable in the markets today is the rate of inflation, and the peak is well behind us. A more rapid decline in inflation than what the Fed is expecting should allow it to stop raising short-term interest rates sooner than the consensus expects. The Cleveland Fed’s Inflation Nowcasting model sees the core PCE falling to 4.5% in December, which is well below the Fed’s estimate of 4.8%.

Cleveland Fed

The rate of decline is accelerating, as every measurement of inflation in the fourth quarter on an annualized basis is significantly below the annualized rate. These numbers are closer to the Fed’s 2% target than the peaks of 7-9% last summer. This should take pressure off the Fed in terms of how aggressive it feels it needs to be in 2023. The peak in the Fed funds rate should come in either February or March, if we have not seen it already. As inflation falls at a faster rate than wage growth, workers should start to see real-income gains. That is what I am relying on to sustain real consumer spending growth in 2023.

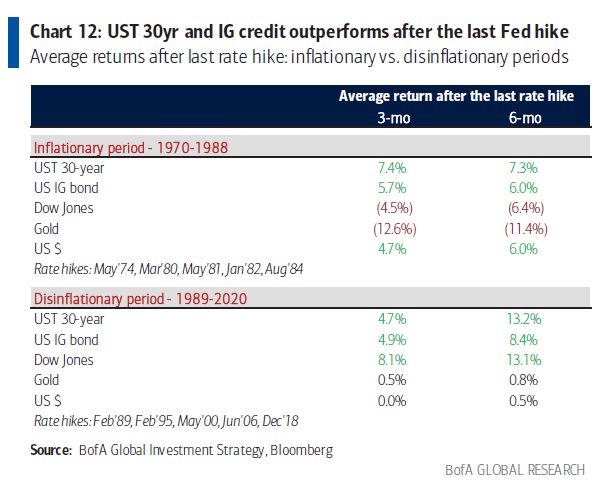

Cleveland Fed

The peak in the Fed funds rate during the first quarter of this year should be the pivot point for markets, as stocks and bonds have performed well in the 3- and 6-month periods following the last rate hike during deflationary periods. I think Wall Street strategist mistakenly assume the end of rate hikes to be a headwind for markets because they also assume us to remain in an inflationary period like 1970-1988.

Bloomberg

Sentiment Can’t Get Any Worse

For the first time in the history of the AAII survey, which dates back to 1987, bullish sentiment did not rise above its historic average for a single week the entire year. Clearly, sentiment can’t get any worse. Sentiment can have as much to do with valuations as the hard economic data, so I view sentiment as a positive to start the year from a contrarian standpoint.

Bespoke

This reminds me of an important fact about being bearish. As a bear, you are on the clock. This is because things simply get better over time. Markets spend most of the time rising, while corrections and bear markets are relatively short lived. Therefore, if the S&P 500 is going to plunge to new lows, it better start its descent sooner rather than later. because the macroeconomic landscape should gradually improve as this year progresses.

The Path To Victory

There are two countervailing forces at work in the economy and markets today. The tailwind is a fortress of wealth, savings, and income, while the headwind is a combination of rising interest rates and an elevated rate of inflation. I think a soft landing in 2023 is more likely than a recession because the tailwind should outlast the headwind. This would be a rare victory for the Federal Reserve, which is why so few hold this view.

That said, I do not expect to see the outsized gains for the stock market 2023 that we saw from 2019-2021. Even after interest rates peak and inflation falls, the stock market must contend with the Fed’s quantitative tightening program, which drains liquidity from the financial system as the Fed reduces the size of its balance sheet. That will be an ongoing headwind for those investing in the broad market indexes, but not for tactical and diversified investors.

I think it results in a continuation of the rotation from expensive growth to more value-oriented investments. Small- and mid-cap companies trade at much lower multiples to earnings than the largest, which is where I think the best opportunities are today. The profitable companies in the Russell 2000 index have an average price-to-earnings multiple of approximately 12.5 compared to the multiple of 17.7 for the S&P 500. I also think this will finally be the year we see emerging markets outperform the US on the tailcoats of a weaker dollar. Therefore, my strategy is to focus on the market of stocks in search of quality and value that will outperform and not the stock market. A new bull market is bound to start in 2023, but we won’t know it until the best opportunities are behind us.

Be the first to comment