iQoncept

I always try to write an end-of-year piece about my biggest winners and another one about my biggest losers.

Usually, that first category more than makes up for the second. But I’ll admit that this has been a different kind of year, where mid-term hopes and dreams – and even hard-core, careful, experience-based analysis – just didn’t pan out as expected.

2022 was a year for the books in so many ways. While there were still winners to be found in the larger stock market, the losers took the consistent spotlight.

This is evident by Yahoo’s Morning Brief published on Thursday, December 29: “The Dow Crushed Tech Stocks by the Widest Margin in 20 Years.” The title highlights how strange the past (almost) 365 days really were. And right from the beginning, too.

“The Nasdaq is down 35% so far in 2022, while the Dow is off less than 10%. And this Dow outperformance relative to the tech index is by far the biggest gap since the dot-com bubble peaked and unwound from 2000 to 2002.”

It goes on to list the following stocks and their year-to-date performance as of the closing bell on Dec. 28:

And you and I both know it gets worse from there.

Big Tech Lost Enormously This Year, and REITs Didn’t Fare So Well Either

Here are the real former rockstars worth noting… former rockstars who have fallen on some very hard times now:

- Amazon (AMZN) was down 50.9%.

- Nvidia (NVDA) was down 52.3%.

- Meta Platforms – i.e., Facebook – (META) was down 65.6%.

- Tesla (TSLA) was down 65.6%.

And every single one of those losers falls squarely into the tech category. That says something.

So do the clear categories – pharmaceutical and big oil – the year’s outperformers fit in, with:

- Eli Lilly (LLY) up 32.2%

- Merck & Co (MRK) up 44.9%

- Chevron (CVX) up 50.8%

- Exxon Mobil (XOM) up 77.1%.

To quote the Yahoo Finance article directly again:

“The explanation (for the losers) is relatively simple: The Fed is aggressively fighting inflation, which has clobbered tech and growth stocks this year. Meanwhile, energy names soared for most of 2022, while cyclical and defensive sectors like healthcare, industrials, materials, (and) staples saw investor interest pick up in the fourth quarter.”

So what the heck happened to real estate in that case?

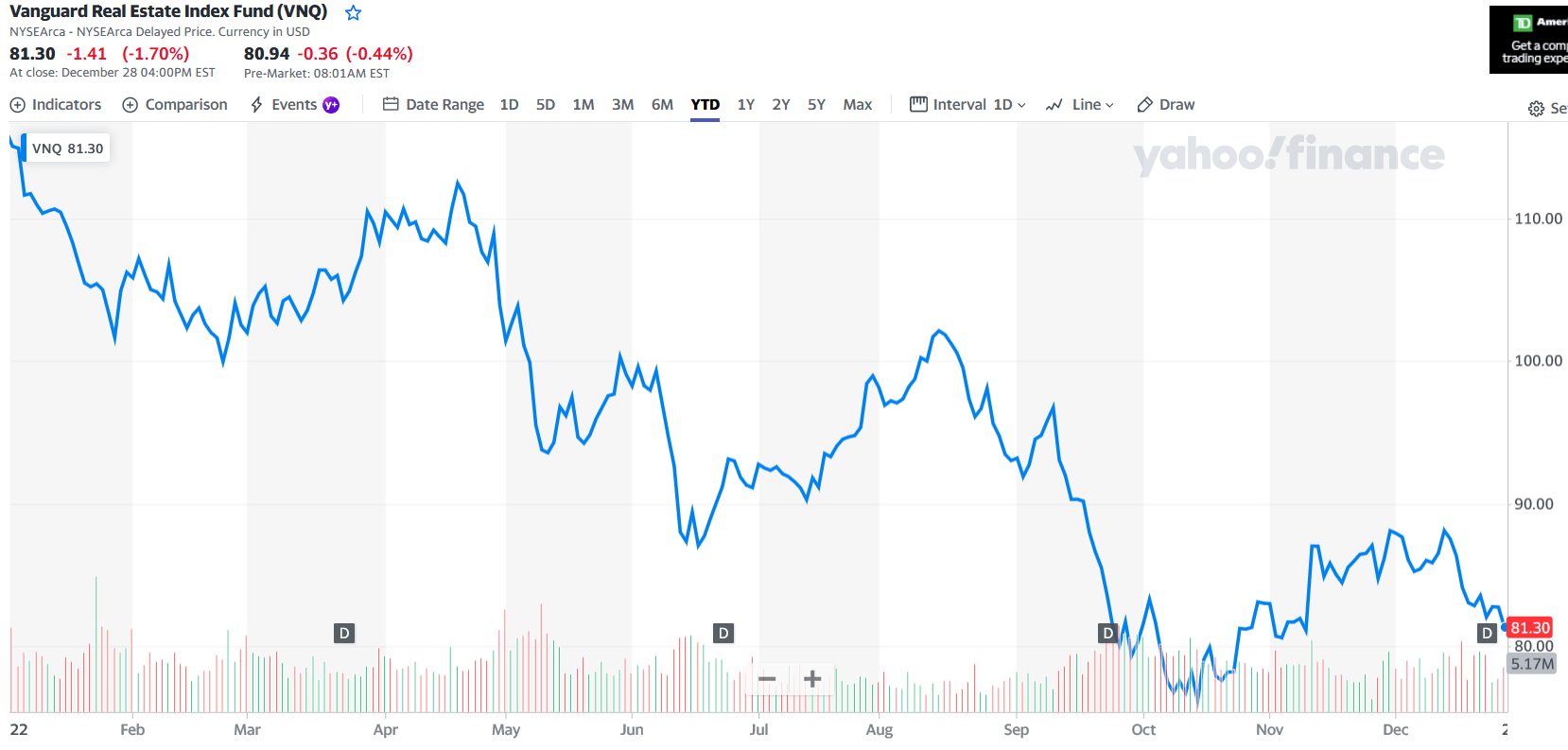

Because, as evidenced by the Vanguard Real Estate Index Fund (VNQ) – which I keep using to highlight overall real estate investment trust (REIT) performance – it looks more like a cratered growth stock than the stalwart value category it’s supposed to be.

Yahoo Finance

The answer is, once again, an easy one.

Typically known as steady-as-she-goes marathon winners, REITs always belong in a completely different category than high-flying, flashy growth stocks. But they do share one thing in common…

That would be a disproportionate antipathy toward rising interest rates.

Since REITs work with a definite degree of debt on their books, rising interest rates do affect them. So some stock-price pushback should have been expected going into 2022.

And, for the record, I did expect it.

Just admittedly not to the degree we’ve actually seen.

Comparing REIT Roadmaps From This Year and Next

I wrote about expected interest rates in my “2022 REIT Roadmap,” which was published on iREIT on Alpha last December (incidentally, the “2023 REIT Roadmap” is now available as well).

But before we go there, let me quote last year’s copy:

“Now, the Federal Reserve is supposed to accelerate its monthly tapering goals down to $20 billion of Treasuries and $10 billion of mortgage-backed securities (MBS) in January. That could change depending on whatever new economic data rolls in, but we’re already fairly certain that next year isn’t going to copycat 2021 regardless.”

Nailed it on that one, at least. And how:

“… rising rates equals higher borrowing costs. And higher borrowing costs can be a key risk for REIT valuations, especially the lower-quality ones with weaker balance sheets.”

Where I went wrong was in assuming that avoiding those shakier stocks would keep us from feeling the financial ground fall out from beneath us.

What happened this year to REITs wasn’t rational. I’m not just saying that to make myself sound better; it’s simply the truth.

Investors overreacted – intensely – focusing on a single factor (i.e., rising interest rates) instead of fundamentals. I’ve quoted Nareit before on the subject of overall REIT health, and I’ll quote it again in the upcoming “My Biggest REIT Winners of 2022.”

But for now, I’ll simply acknowledge the error of my ways…

Not in trusting REITs over the long-term, but certainly in thinking the following picks had upside to offer in 2022.

Transparency Is A Must!

2022 has been a rough year for most investors, that’s unless you only held energy stocks. As a matter of fact, 2022 was the first time in over a decade where my top picks lost money.

As most of you know, I’m proud to tout my winning years – like in 2021 when my top picks averaged a return of 40.8%, but I’m just as quick to point out my losing picks. Everyone has picks that go south, it’s inevitable, and you should be very skeptical of anyone that says anything different.

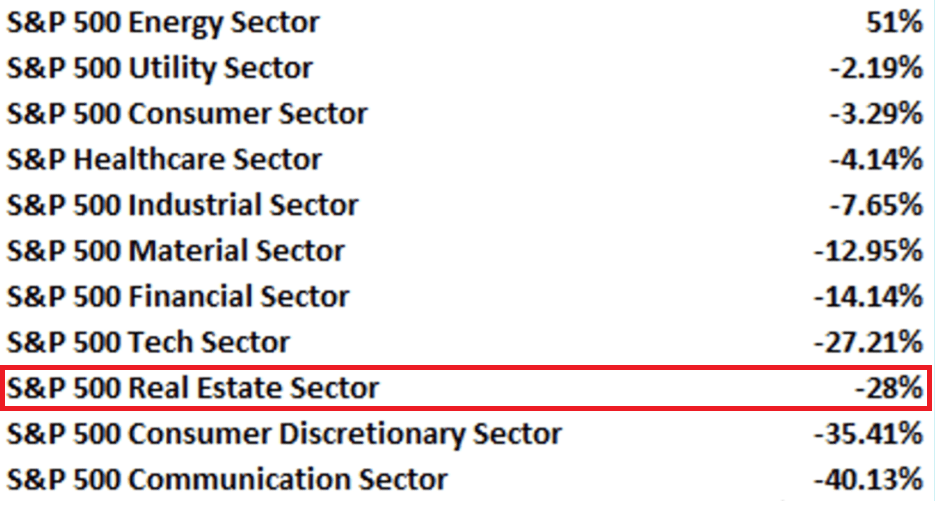

Nasdaq.com (as of 12/19/22)

Pretty much every sector has been down this year, with real estate being hit particularly hard with a -28% decline in 2022.

Misery loves company but a loss is a loss and I’m not one to make excuses. So, in the spirit of full transparency here are my biggest losers of 2022 –

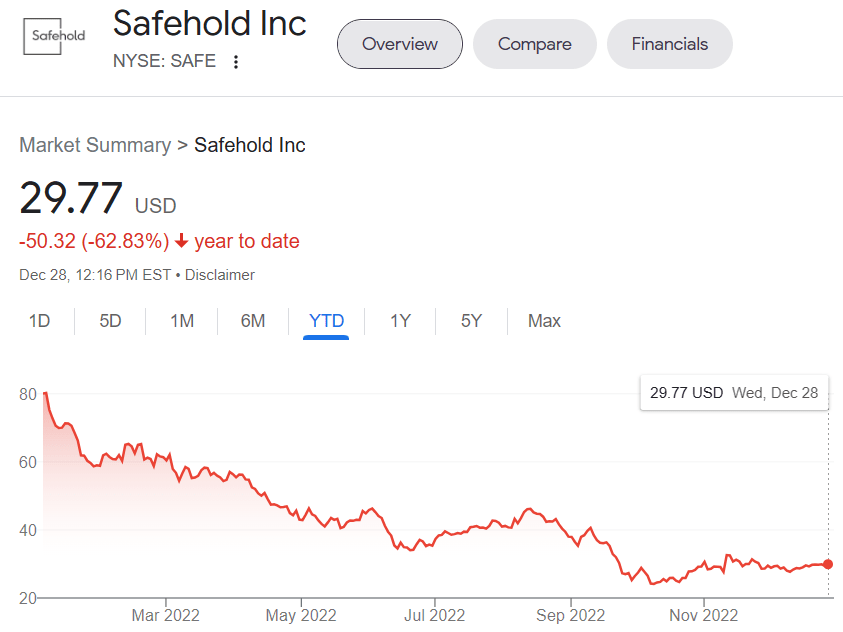

1. Safehold (SAFE) (-63%)

SAFE is a ground lease REIT that went public in 2017.

In 2022 SAFE made some significant changes to its capital structure when it internalized its management by combining with iSTAR. Prior to the merger iSTAR spun off its legacy non-ground lease assets so the combined company is now a pure-play ground lease REIT.

Ground leases have some unique characteristics when compared to REITs that invest in buildings. For one they have extremely long lease terms with 94% of their leases lasting more than 60 years. Additionally, their leases are structured so that in the event of a default, SAFE gets to keep the land and any improvements made to the land.

This gives the building owners a lot of incentive to pay the rent. If they don’t, they lose whatever structure they owned on the land they leased from SAFE. Due to the merger, the improved scale and internalized management really improved the profile of the business from an investment standpoint. Jay Sugarman, CEO of SAFE, addressed this in my interview with him earlier this year –

Nasdaq.com (as of 12/19/22)

Jay Sugarman – iREIT

However even with these positive catalysts at play, SAFE has lost ~63% YTD making it one of my biggest losing picks of 2022.

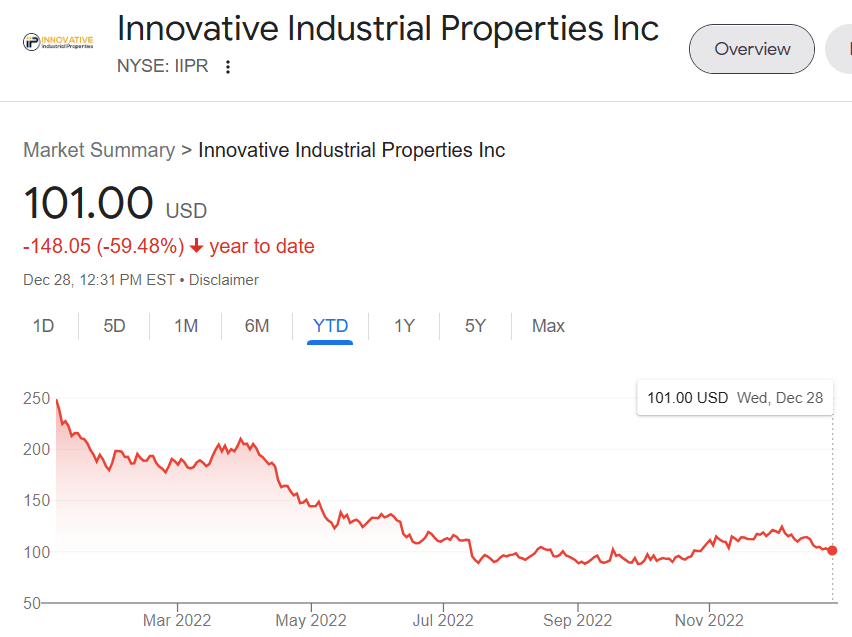

2. Innovative Industrial Properties (IIPR) (-59%)

IIPR is an internally managed REIT that owns and leases property to licensed cannabis operators. As of 9/30/22 They have 111 properties with a weighted average lease term of 15.5 years and no leases expire until 2029.

They target triple net lease structures so that they have no capital expenditures. All property expenses are paid by the tenant, including repairs and replacements.

IIPR debt metrics are exceptional, with a Debt to Gross Assets at ~12% and a Debt Service Coverage ratio of ~15.6x. IIPR doesn’t list their Debt/EBITDA, but with my back of the napkin calculation it stands at roughly 1.29x as of 3Q-22.

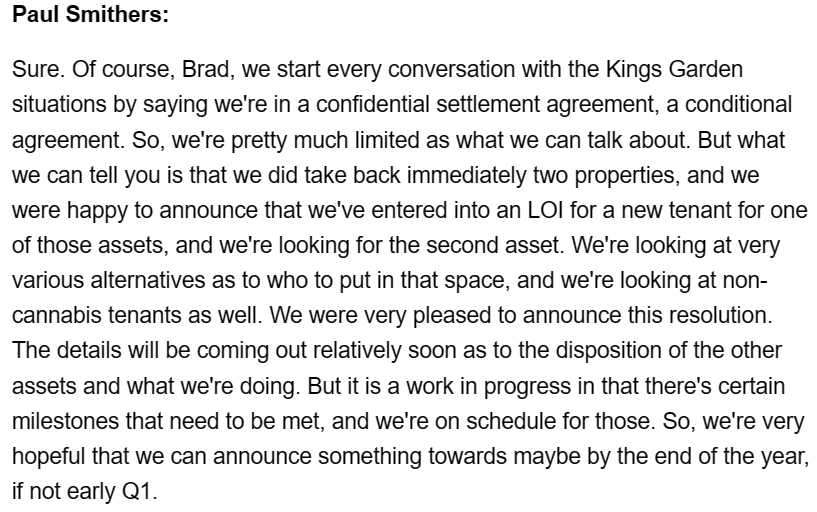

Along with the macro factors that have plagued the market in 2022, IIPR had an additional headwind when its tenant Kings Garden defaulted on its lease payments.

IIPR took aggressive action and sued Kings Garden and the two parties entered into a confidential settlement agreement. I asked the CEO of IIPR, Paul Smithers, about the situation when I last interviewed him –

The Ground Up: Innovative Industrial Properties CEO & CFO | Seeking Alpha

From the information they are allowed to disclose, it appears they are managing the situation well, but it has put pressure on the stock price which has not yet recovered in 2022.

Admittedly the stock was already under pressure prior to the default due to concerns over national legalization but the tenant default just added fuel to the fire. IIPR is another one of my biggest losers in 2022 with it being down 59% YTD.

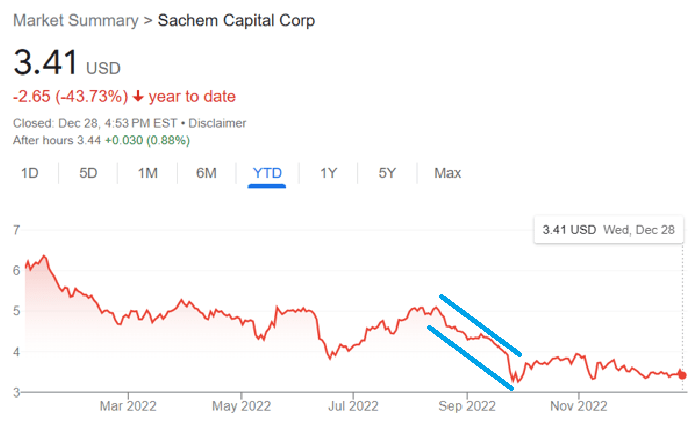

3. Sachem Capital Corp (SACH) (-42%)

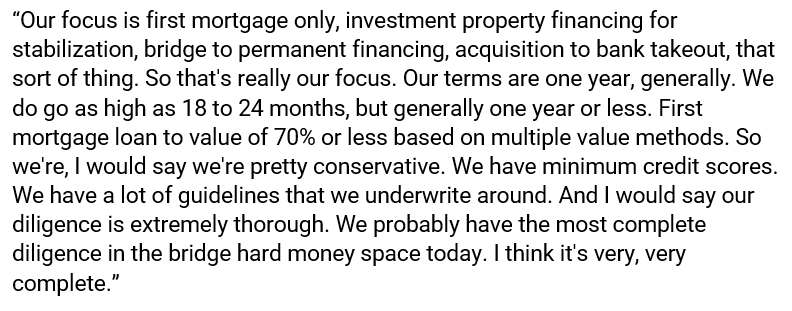

SACH is a mortgage REIT that specializes in originating, servicing, and managing first lien mortgage loans. They lend money on a relativity short-term basis for commercial and residential real estate and have a comprehensive underwriting process that considers credit scores, collateral value, and loan-to-value ratios.

Primarily though they focus on collateral value which enables them to close a loan in as quickly as 5 days. The nibble approach they take to underwriting gives them a competitive advantage and allows them to quickly adjust to market conditions. About a month ago I spoke with Bill Haydon, the CIO and COO of SACH, and he described their underwriting process in more detail.

Bill Haydon –

The Ground Up Podcast: Sachem Capital CIO and COO, Bill Haydon | Seeking Alpha

He went on to say –

The Ground Up Podcast: Sachem Capital CIO and COO, Bill Haydon | Seeking Alpha

Although there has been an increase in defaults this year, SACH fundamentals have held up reasonably well with 0.46 earnings per share expected in 2022 vs. 0.44 in 2021 or a 4.5% year-over-year increase.

Nevertheless the stock has been under pressure throughout 2022.

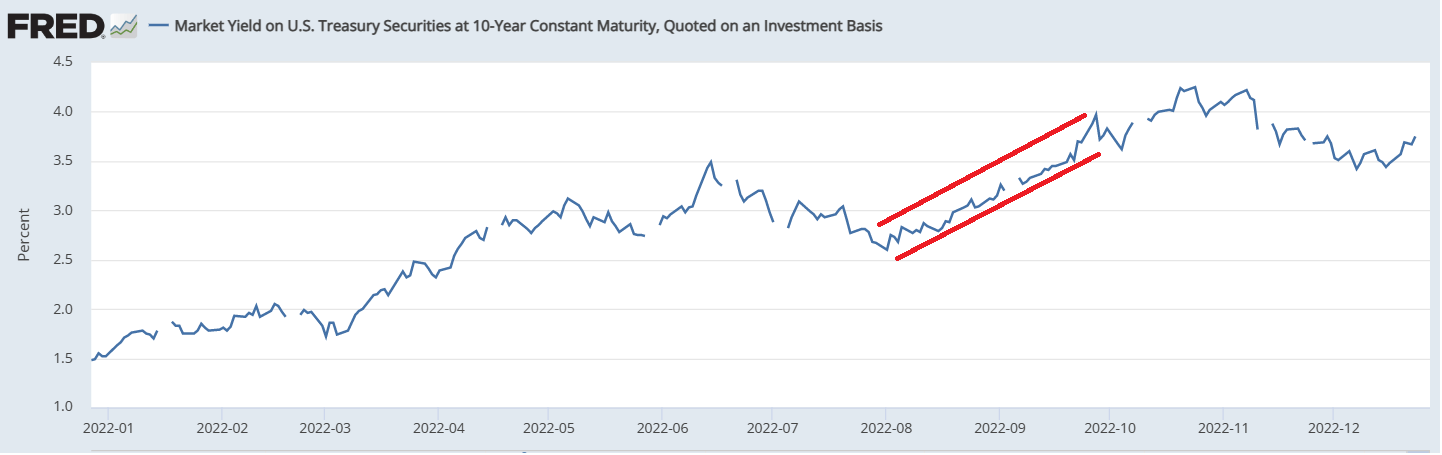

Much of this can be explained by the macro environment, in particular the volatility in interest rates which mREITs are particularly sensitive to. I pulled a chart of the 10-year treasury to compare it to SACH and you can see there is a strong negative correlation between rising rates and SACHs stock price.

In particular I highlighted the period from mid-August to the end of September. More specific to the company, SACH cut its dividend by -7.1% in late October. All in all, the stock is down -42% YTD and is one of my biggest losers in 2022.

FRED

4. Medical Properties Trust (MPW) (-52%)

MPW is an internally managed REIT that owns hospital properties subject to triple net leases. They have international exposure with roughly 400 properties found in the US, Portugal, Spain, Italy, Switzerland, and other regions across the globe.

Hospitals are considered mission-critical properties, they cannot shut down, and are a necessary component to society. MPW’s performance over the last decade has been outstanding, as they have delivered 356% total shareholder return since 2012.

MPW has had a rough year in 2022. It has been hit on multiple fronts including the macro environment, negative press, and a tenant bankruptcy. Much of the negative press surrounding MPW involves its largest tenant Steward, claiming the operator is near insolvency and accusing MPW of shady lending practices to keep them afloat.

Other stories involve excessive spending by management, in particular the use of 3 planes. I recently spoke with MPW CEO Edward Aldag and discussed many topics including the planes, the financial health of Steward, and the bankruptcy filing of its tenant Pipeline Health –

The Ground Up: Medical Properties Trust CEO, Edward Aldag | Seeking Alpha

While it is true that hospital operators have been under pressure since Covid which has impacted their financials, it’s important to remember that MPW owns the hospitals and in the event of a default or bankruptcy MPW can re-lease the property to a different tenant. But between the negative press and general market conditions, MPW’s stock price has fallen -52% YTD making it one of my biggest losing picks of 2022.

I Saved the Best for Last

As a stock analyst, my job is to work hard to make recommendations so investors can protect principal at all costs. Needless to say, these recommendations did not adhere to this fundamental rule.

More importantly, the objective for any intelligent investor is to buy shares in high quality companies when they’re trading at a discount... and now all four of these REITs are trading at substantial discounts.

Earlier this summer I opened an account for my new grandson, Asher, and let me share with you several of his top picks (I picked the names for the portfolio):

- IIPR: +11.9%

- SAFE +9.1%

- MPW 3.3%

One of the most valuable lessons I’ve learned over the decades is that you must always focus on fundamentals and the margin of safety.

In 2020 I was able to aggressively add shares to my REIT portfolio which has resulted in once in a lifetime returns. Even after the selloff in 2022, my portfolio has returned an average of 15% annually since inception.

Also, in addition to the margin of safety, I have constructed a highly defensive retirement blueprint that has crushed the competition. How did I do that?

Tactical diversification

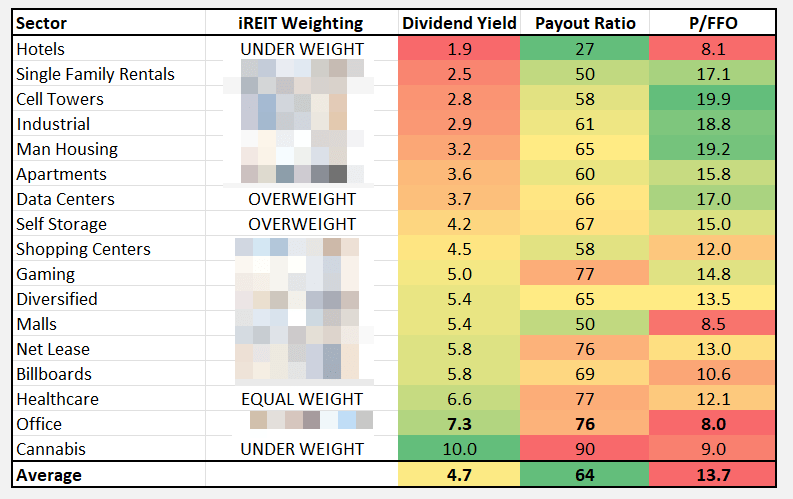

At iREIT on Alpha we provide members with our recommended sector weightings (as per the 2023 REIT Roadmap):

2023 REIT Roadmap (iREIT on Alpha)

By smartly allocating capital to the best sectors and the best REITs (in these sectors), and by limiting exposure to one or two REITs, you can avoid catastrophic meltdowns and protect principal at ALL costs.

We strongly encourage diversification – and not just within the REIT sector – but across all asset sectors. As I explain in my 2023 REIT Roadmap,

“…we are allocating capital to the OVERWEIGHT and EQUALWEIGHT categories and as REITs enter this recessionary period in a relative position of strength (tight supply and healthy cash flow) we recommend high quality names that should remain resilient.

Supply and demand remains the biggest catalyst and most of the sectors identified (as OVERWEIGHT) have solid demand driving future earnings.

REITs have performed remarkably well when rate-hiking cycles have ended. The pace of Fed hikes has moderated, and the point at which the Fed stops raising rates has historically been a critical inflection point; on average, REITs have returned 15.8% in the first six months after the Fed has stopped raising rates.”

As always, thank you for reading and happy SWAN investing!

PS: Next up… the biggest winners in 2022!

Be the first to comment