Sakorn Sukkasemsakorn

(This article was co-produced with Hoya Capital Real Estate)

Introduction

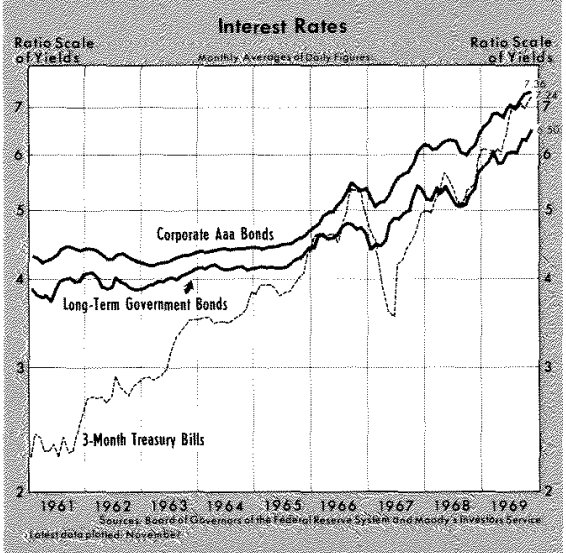

The year 2022 saw inflation take off with the FOMC attacking it with seven rate hikes, the money supply continued to grow, and we had Putin’s war in the Ukraine; causing both stocks and bonds to suffer. Broad stock and bond market indexes had not both posted large losses in the same calendar year since 1969. Then there was the Vietnam war, the US was experiencing its worst inflationary period since WWII, and the money supply was expanding. Sound familiar? Some charts from that era.

files.stlouisfed.org/files/htdocs/publications/review/69/12/Battle_Dec1969.pdf files.stlouisfed.org/files/htdocs/publications/review/69/12/Battle_Dec1969.pdf

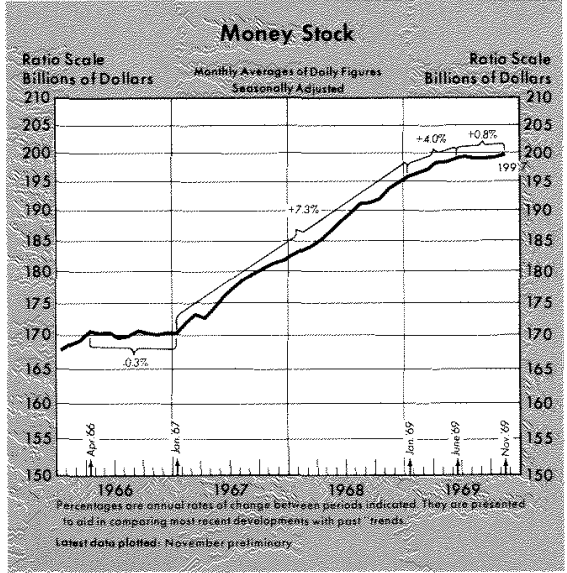

The recent chart looks like this.

fred.stlouisfed.org

A look back at 2022

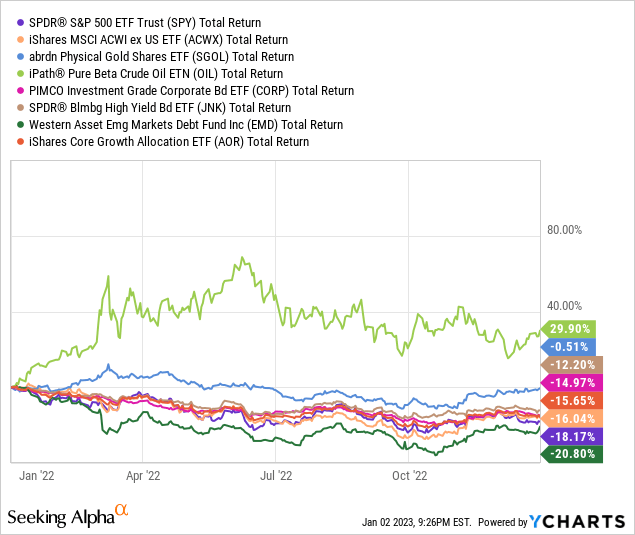

Just a reminder of how bad 2022 was for most investments. Yes there were winners in niches.

I included the iShares Core Growth Allocation ETF (AOR) as it is a 60%/40% targeted ETF, the historic suggested allocation. With both stocks and bonds down, it fell in the middle. The only positive one listed is the iPath Pure Beta Crude Oil ETN (OIL).

Portfolio year-end allocations and annualized ROIs

Author’s Investing XLS

The Green boxes are when that account outperformed the “My allocation” composite benchmark. Overall, that was the case at 1- and 3-years; but not 5-years. Option premiums really helped in 2022.

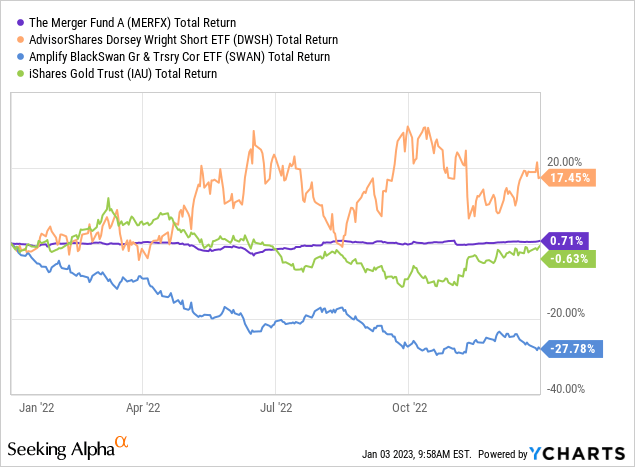

Assets I sold out of

Many of these were bought to either reduce my overall portfolio volatility, for bear market protection, or inflation. Last year showed how poor they were in achieving the goal I held them for.

Merger Fund (MERFX): With CDs now yielding more than MERFX’s 5-year CAGR, this was let go. That said, it was very stable, having a 3.14% StdDev over the past five years.

AdvisorShares Dorsey Wright Short ETF (DWSH): This ETF shorts individual stocks and did great going into the COVID crash, up 56% that quarter. Since then it has been a disaster (down an annualized 37%). I took advantage of 2022 to exit the small position I had not already sold in prior years.

Amplify BlackSwan Growth & Treasury Core ETF (SWAN): The ETF’s strategy showed its weakness when both stocks and bonds drop simultaneously, thus eliminating why I held, less Bear market downside.

iShares Gold Trust ETF (IAU): Inflation up 8+%, IAU underwater. Since I held for that protection, I sold and expanded my Treasury Direct I-bond exposure.

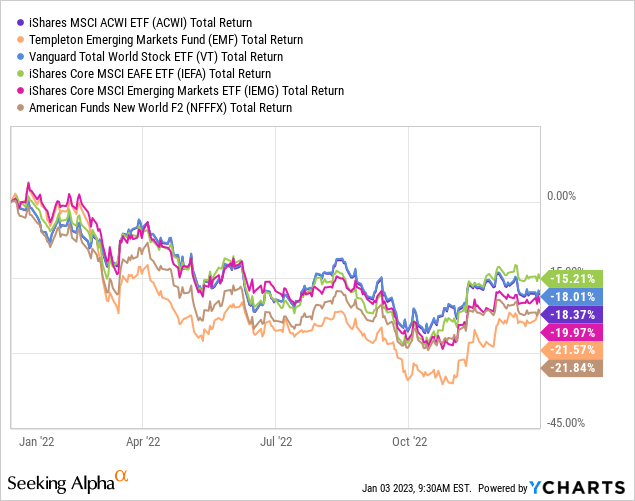

International equity exposure reduced

With international stocks losing their diversification benefit, coupled with their poor performance, I sold the following assets to reduced my exposure by half.

- iShares MSCI ACWI ETF (ACWI): 60% US stocks

- TEMPLETON EMERGING MKTS FD (EMF)

- VANGUARD INTL EQUITYINDEX FDS TT WRLD (VT)

- ISHARES CORE MSCI EAFE ETF (IEFA)

- ISHARES CORE MSCI EMERGING (IEMG)

- FIDELITY EMERGING MARKETS DISCOVERY (FEDDX)

- AMERICAN NEW WORLD (NFFFX): 25% US stocks

I did offset those sales by adding to my iShares MSCI Global Min Vol Factor ETF (ACWV) for the lower volatility and expanded my hedged exposure with the WisdomTree Europe Hedged Equity ETF (HEDJ). I also lost my only EM Debt exposure when the NUVEEN EMERGING MKTS DEBT 2022 was liquidated.

Fixed Income adjustments

Late to the game, I adjusted my Fixed Income holdings to shorten the durations of my portfolio. In the process I went down on the quality scale and more toward floating versus fixed bonds.

- PIMCO INV GRADE CORP BD (CORP): sold

- ISHARES 0-5 HY CORP (SHYG): bought

- PIMCO Access Income Fund (PAXS): bought after review

- Apollo Senior Floating Rate Fund (AFT): bought after review

I added the Apollo Senior Floating Rate Fund (AFT) after reviewing it last spring hoping its floating-rate would shield it some from FOMC actions: its price is down 16% since then.

If its performance doesn’t improve, my shares in the VanEck Africa Index ETF (AFK) will be sold at a loss that will offset some of my option writing premiums. In the same situation is the iShares MSCI Frontier and Select EM ETF (FM). I also reduced my allocation to municipal bonds as their long durations would suffer more than other funds with shorter ones.

Laddered Fixed Income strategy review

One benefit from rising interest rates was only one issue was fully called in 2022, a big change from the previous years. The JEMD mentioned above was the only exit, offset by several additions. Overall, this strategy did great, only down a few percentage points. I allocated about $150,000 to this strategy. You can read details about what I hold here.

Option writing strategy review

Even by staying conservative, my assignment rate in the down stock market in 2022 was much higher than desired at 28%. Most were exited at a profit though. One calculation showed an overall 13.4% ROI for this strategy. I allocate $250,000 in cash to this strategy. You can read details here.

Portfolio strategy

Here I describe the primary purpose of each account. In the long run, they all have the same three goals:

- Give us a comfortable retirement

- Provide gifts to charities as we live and when we pass

- Do the same for our nieces and nephews, none of whom are financially well off.

Listed in no particular order:

ML 401k from work

As listed, this is by far my biggest account and its importance is covered in My 401(k) – The Linchpin Of My Retirement Investing Plan article. Currently is has both regular and Roth components, with small conversions happening annually to hopefully reduce my RMD to avoid the lowest IRMAA income limit. The plan was to move the Roth component before RMDs were required but my understanding is SECURE ACT 2.0 has eliminated that requirement: RMDs start upon my death now.

Fidelity joint taxable

This is our “go to” for paying bills, almost all, including credit cards, are on autopay thus, the cash balance is usually high. Last summer, I started writing deep OTM CSPs to enhance the income when Fidelity was paying us nothing on those funds; doing less now that the rate is close to 4%. This account is linked to all the others, plus our bank, for easy fund reallocations. For security purposes, we have asset movements between accounts on lockdown, which is a pain at times but blocks unauthorized withdraws.

Regular IRA: mine

We do not expect to ever need to touch any of our IRAs except to make required RMDs, which for us now start at age 73. This one differs from my wife’s two as I use it to fund part of my CSP option strategy. About 50% of the account is dedicated for that purpose, most of the rest is in equity ETFs. Any remaining balance will go to charity, as is the case with all the regular IRAs.

Regular IRA: wife

As my wife approaches 73 and withdrawal time, the high equity ratio might be reduced and more income producing assets added, which could include expanding the existing allocation to BDCs and REITs. How the withdraws are done, via RMDs or QCDs, will depend on the need to keep our overall income below IRMAA limits and the level of funding needed to meet our charity giving goal.

Inherited IRA: wife

Because it was inherited after her dad was taking RMDs, my wife had to continue doing so. She was finally able to switch from RMDs to QCDs in 2022, which leaves my Charitable Gift Trust more intact. When her father died we owed taxes on what he hadn’t taken yet, a $4000 difference as he owed very little in taxes. While not easy to accomplish, getting one’s parents to take their RMDs early in the year is a good strategy if they are in a lower tax bracket than those inheriting the IRA. I’m avoiding that as I have my parent’s IRAs going into my CGT discussed later.

I covered how QCDs can be beneficial in several articles:

- The Tax Code Provides A Strategy IRA Converters Should Consider: QCDs

- Reasons To Estimate Your Future RMDs

One investment decision when you are in RMD mode is funding them. Do you try generating the cash or stay fully invested and sell assets to cover the RMDs? Our preference is trying to never sell, especially in a down market. There is no right or wrong strategy, just a preference, probably geared toward one’s overall investment philosophy.

Roth IRA: mine

This account has a large cash allocation as it’s the main one I use in my CSP strategy. The rest is a mixture of equity and fixed income funds. Since the option strategy is outperforming the income oriented assets, a change for 2023 will be selling those assets and expanding the funds available for my CSP strategy. Assuming Congress doesn’t change the rules again (highly wishful), the three Roth accounts (2 IRAs, 1 401(k)) are designated for the next generation.

Roth IRA: wife

I have been slowly moving this account to a higher equity allocation since no RMDs (so far) are required until it’s inherited, thus income generation to meet those payments isn’t required.

Just after I retired in 2019, I penned the following which go into more detail of managing our IRAs accounts.

- Now Retired – Setting Investment Strategy For Our IRA Accounts

- Now Retired – Adjusting My Roth Accounts For The Long Haul

Charitable Gift Trust

I set this account up for two reasons:

- Maximizing tax deductions: By alternating years I made contributions, I would either itemize or use standard deduction. This worked even better after the SD was increased.

- Maintain charity giving at pre-retirement levels afterwards. This is happening and became easier once we could start using QCDs.

My Using A Donor Advised Fund As Part Of My Retirement Investing Strategy article covers this part of my retirement strategy. Since this is all going to charity, it holds my exposure to Sustainable Investing, plus some inflation protection assets.

Treasury Direct

Once inflation took off and the rate on I-bonds broke 7%, I opened and fully funded this account as a means of hopefully breaking even with inflation. I had three paper I-bonds from 1993 that I was able to move into the account. The plan is to add another $10,000 this year and if I get a tax refund, that too.

Morgan Stanley taxable

My Why I Hired Morgan Stanley To Manage 10% Of My Portfolio article goes into depth about why this was step up, but in brief there were two reasons:

- See if a professional could manage funds better than me.

- Provide a live advisor if I die before my wife.

So far, the first point has not been the case which allows me to minimize the fees I pay to have my accounts managed. I look at the “costs” the same as the premiums I pay on my 20-year Term Life policy. We are at the minimum the firm accepts but closing the account is an option if performance doesn’t get closer to the other accounts. I have recently gotten my advisor more active in managing this money.

Wife’s taxable

My home state has two possible tax strategies for married couples: file jointly or file jointly but separate. There are income exemptions that are met separately or lost. Since Social Security is exempt from state income taxes, this account is heavy into income generation, up to the point we meet the exemptions. 2022 will be a test year as my wife reached 70.5 and was able to use the QCD, not RMD, as needed for the IRA she inherited, which also filled most of her exemption. I believe TurboTax will suggest we file Jointly for 2022. If so, this account will be merged into our Joint taxable account at Fidelity.

Health Savings Account: mine

This was funded when my employer finally offered it late in my career. That, plus misusing it has the balance small. My mistake was withdrawing funds when I did not need it to meet my medical bills. Since it is small and has restricted uses without a penalty, I’ve chosen to mainly use baby bonds here, and conservative equity ETFs, like the JPMorgan Equity Premium Income ETF (JEPI), which I recently reviewed. Why everyone should set up an HSA was covered in my Funding A Health Savings Account As Part Of My Retirement Strategy article.

Final thoughts

I agree, this is a lot of accounts to keep track of, but there are limits to consolidating, such as:

- Legal: Except for draining an IRA, we are at the minimum. Yes, we could convert a Regular to a Roth, but why pay the taxes when we can liquidate them tax-free via QCDs.

- Stable Value Fund: Currently this type of fixed income product must be held in a 401k. That asset is the heart in providing stability to our overall strategy. With rates rising, it should start earning more, on a lag.

- Taxable accounts: Here I mention we hope to close my wife’s this year. We might pull the plug on the Morgan Stanley account as we have established a relationship now with two firms as one of the original managers changed firms but stays in touch hoping to get the MS account.

Be the first to comment