bymuratdeniz

Have you ever invested in a Royalty Trust? These are entities within the Exploration & Production Energy industry, which earn money via an arrangement with an E&P company that handles the operations on the Trust’s property and pays the Trust a % of the income.

MV Oil Trust (NYSE:MVO) is a pure play on crude oil.

Company Profile:

MVO’s earnings are based upon a profits interest of 80% of the net proceeds attributable to the sale of production from the underlying properties during the term of the Trust. The net profits interest will terminate on the latter to occur of (1) June 30, 2026, or (2) the time when 14.4 million barrels of oil equivalent (“MMBoe”) have been produced from the underlying properties and sold (which amount is the equivalent of 11.5 MMBoe with respect to the Trust’s net profits interest), and the Trust will soon thereafter wind up its affairs and terminate.

As of September 30, 2022, cumulatively, since inception, the Trust has received payment for 80% of the net proceeds attributable to MV Partners’ interest from the sale of 13.3 MMBoe of production from the underlying properties (which amount is the equivalent of 10.7 MMBoe with respect to the Trust’s net profits interest).” (MVO Q3 ’22 10Q)

Earnings:

The revenues from oil production are typically received by MV Partners 1 month after production.

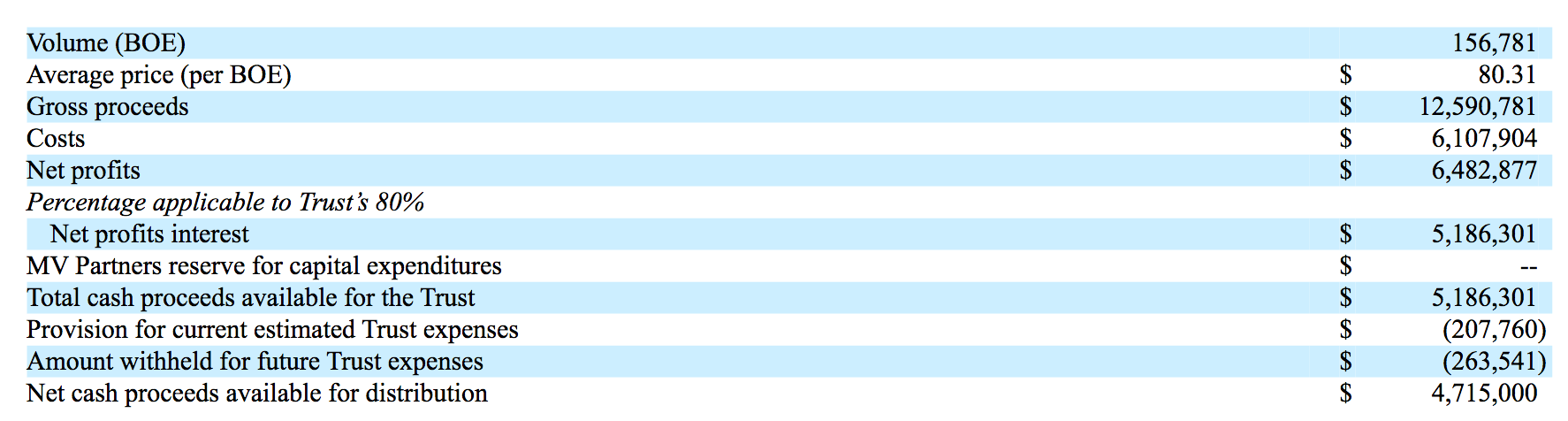

For the quarterly payment period ended December 31, 2022, Unitholders of record on January 17, 2023 will receive a distribution amounting to $4,715,000 or $0.410 per unit payable January 25, 2023.

Net Profit Interests, NPI, totaled $5.186M. After deducting $207K for Trust expenses, and %263K for future Trust expenses, MVO had Distributable Income of $4.715M available for its unitholders:

MVO site

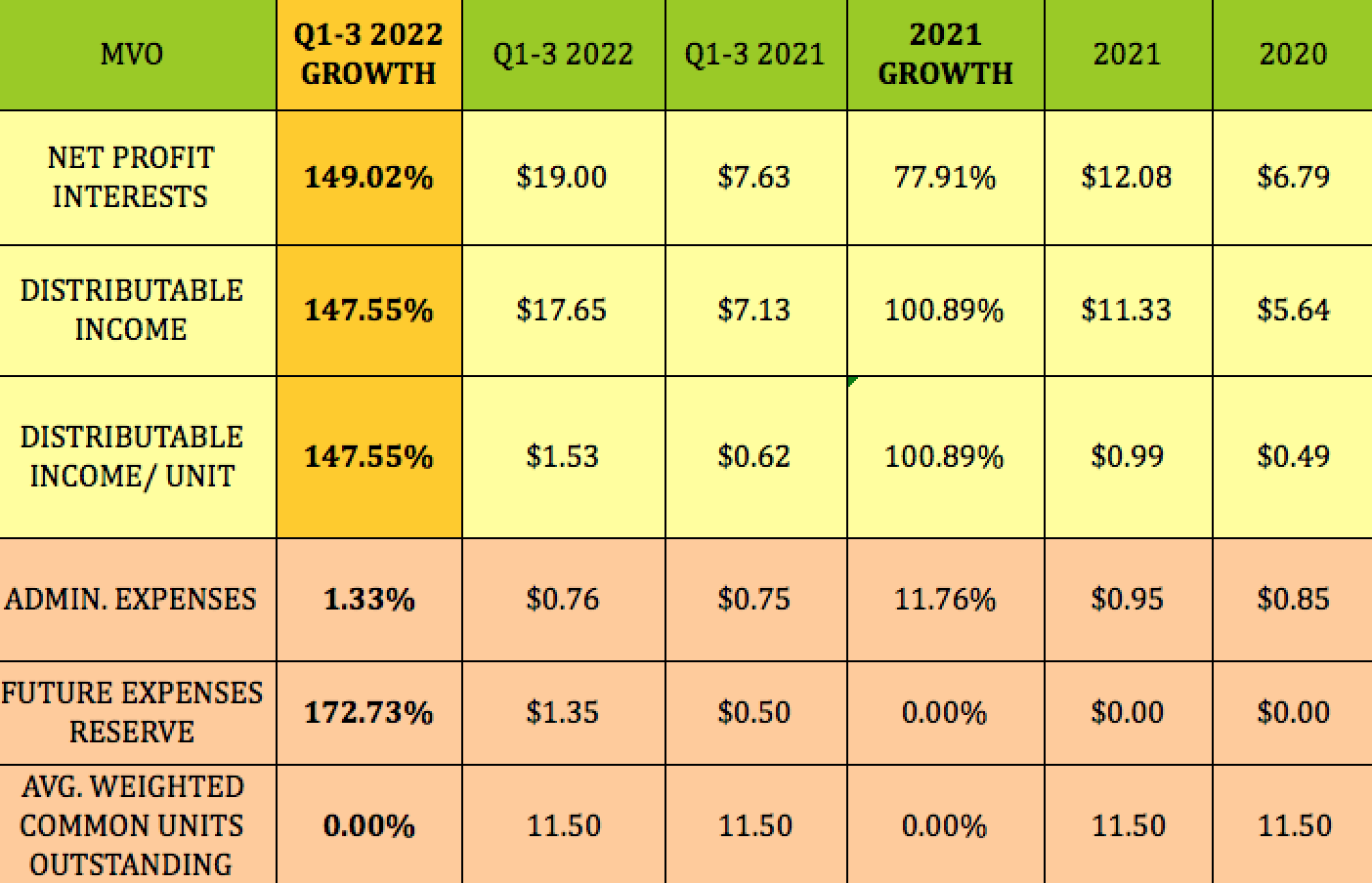

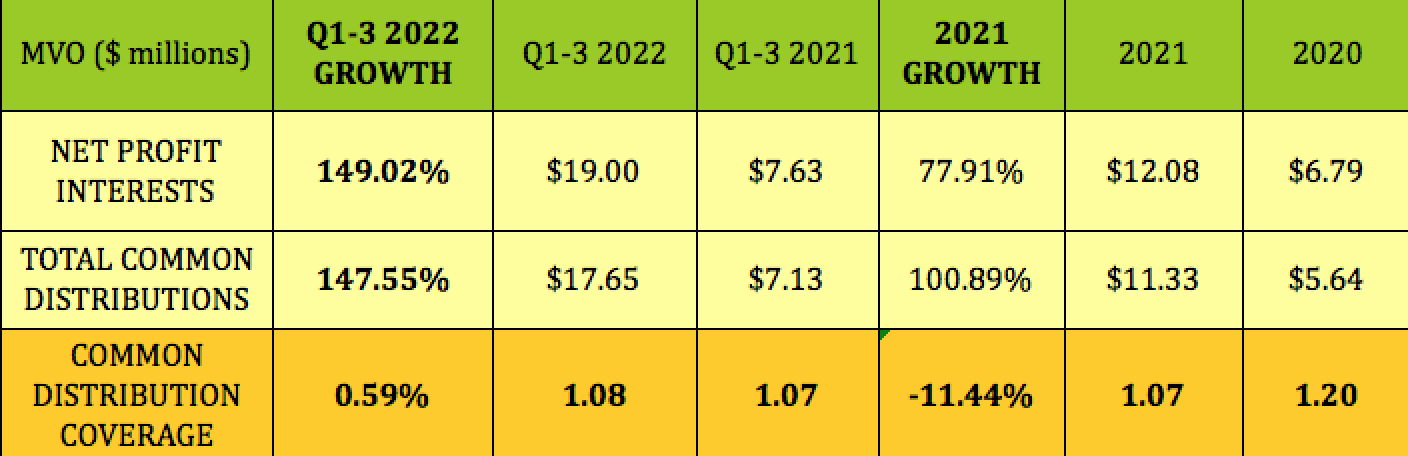

In Q1-3 ’22, MVO’s Net Profit Interests, NPI, surged 149% in Q1-3 ’22, to $19M, vs. $7.63M in Q1-3 2021; and Distributable Income rose 147.55%. Administrative expenses ran at 4%, up slightly vs. Q1-3 ’21, whereas the Future Expenses Reserve rose 173%, to $1.35M.

Full year 2021 had a 78% rise in NPI, with Distributable Income rising ~101% vs. a pandemic-challenged 2020.

Hidden Dividend Stocks Plus

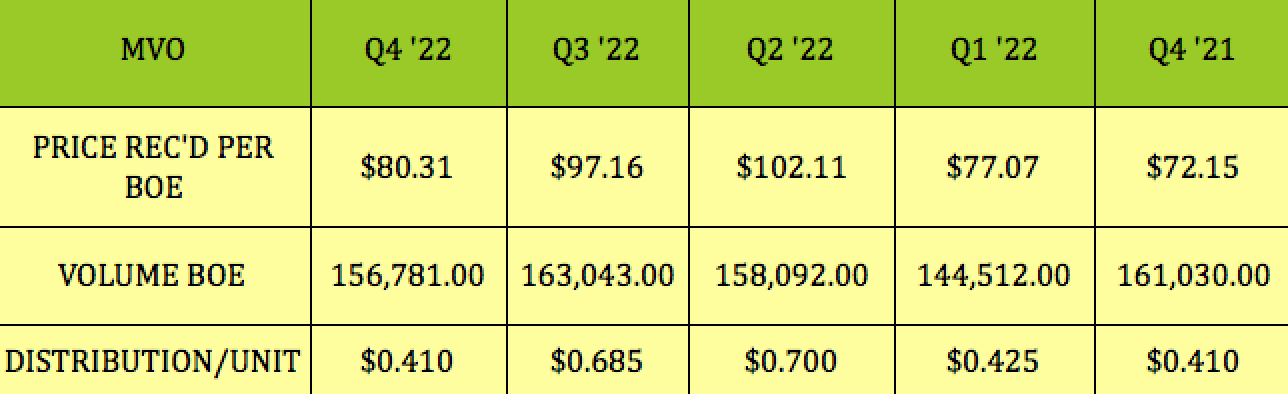

Although MVO issues reports detailing income on a quarterly basis, the distribution amounts don’t always tie directly to oil prices on a quarterly basis.

For example: “The cash received by the Trust from MV Partners during the quarter ended September 30, 2022 substantially represents the production by MV Partners from March 2022 through May 2022.” (MVO site).

BOE, (Barrel of Oil Equivalent), prices peaked in Q2 ’22, at $102.11, as did MVO’s distribution, which hit $.70. Excepting Q1 ’22, when volume dipped to 144K, the BOE quarterly volume has run in a range of 156K-161K:

Hidden Dividend Stocks Plus

Dividends:

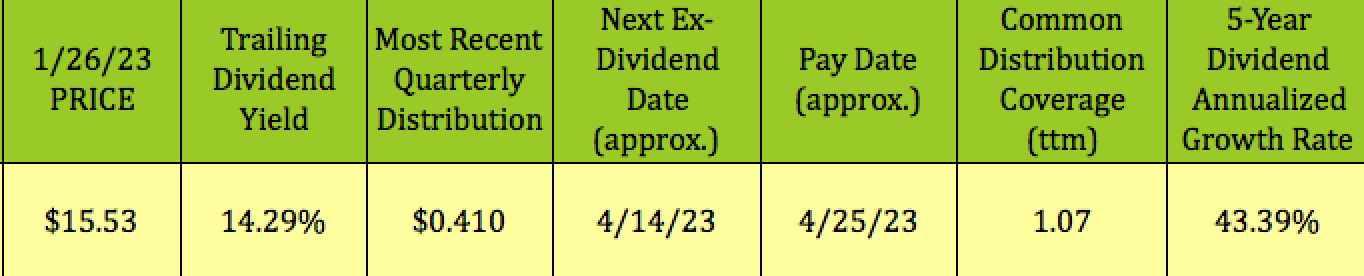

At its 1/26/23 intraday price of $15.53, MVO had a trailing yield of 14.29%, and a forward yield of 10.56%. However, since MVO pays a variable distribution, it’s impossible to calculate a correct forward yield.

Its most recent payout was $.41 in January, and it should go ex-dividend next on ~4/14/23, with a ~4/25/23 pay date.

Hidden Dividend Stocks Plus

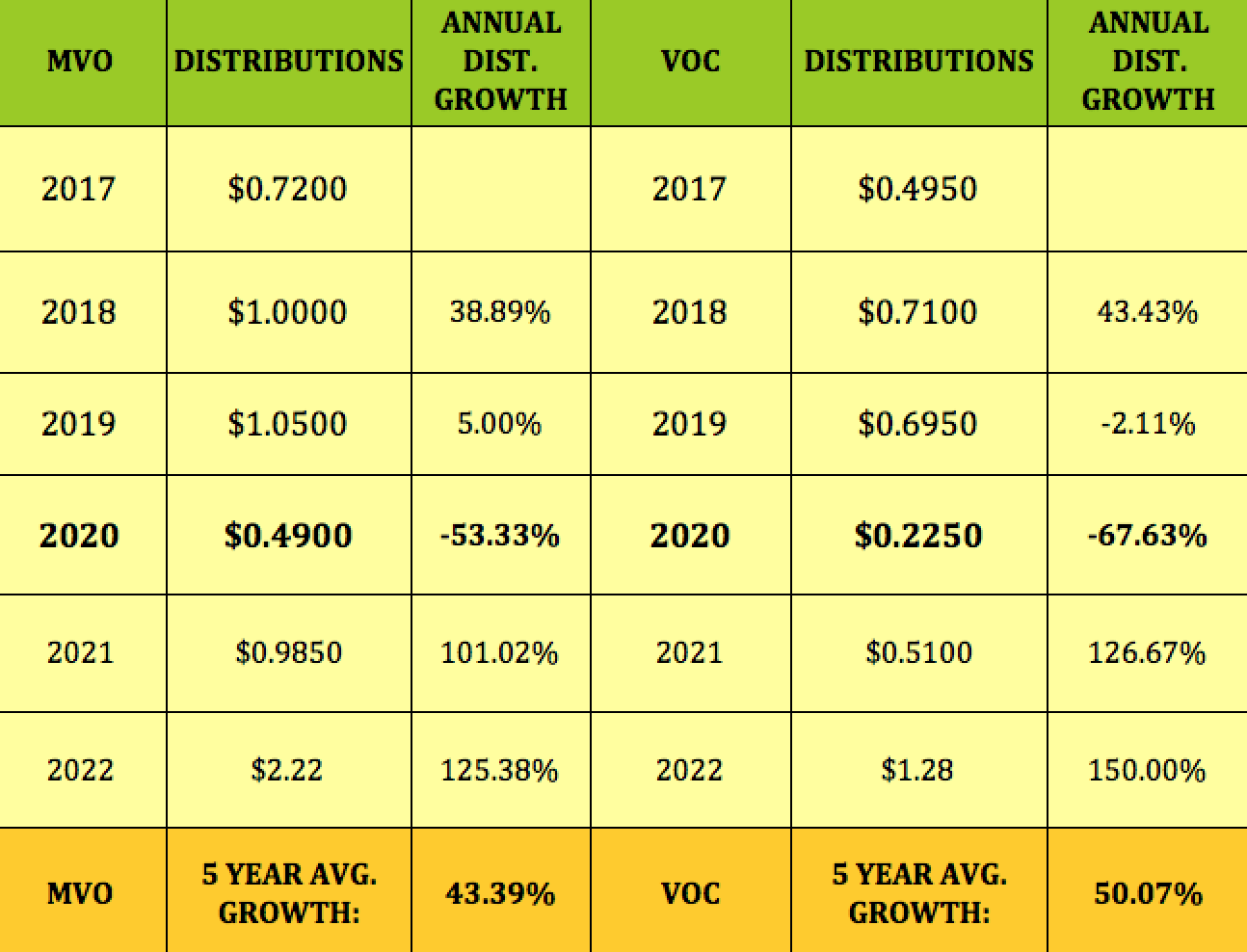

MVO has a strong five-year dividend growth average of 43.39%. We wondered if that was an outlier, and looked at VOC Energy Trust’s five-year dividend growth also – it was a bit higher, at ~50%. 2020 of course was a negative growth year for both trusts, due to the pandemic. However, both trusts bounced back in the past two years with three-digit dividend growth:

Hidden Dividend Stocks Plus

As noted above, MVO’s Net Profit Interests, NPI, surged 149% in Q1-3 ’22, to $19M, vs. $7.63M in Q1-3 2021, with distributions jumping by ~148%. NPI covered the distributions by a 1.08X factor, similar to Q1-3 ’21 and full year 2021, when there was a 1.07X factor.

Hidden Dividend Stocks Plus

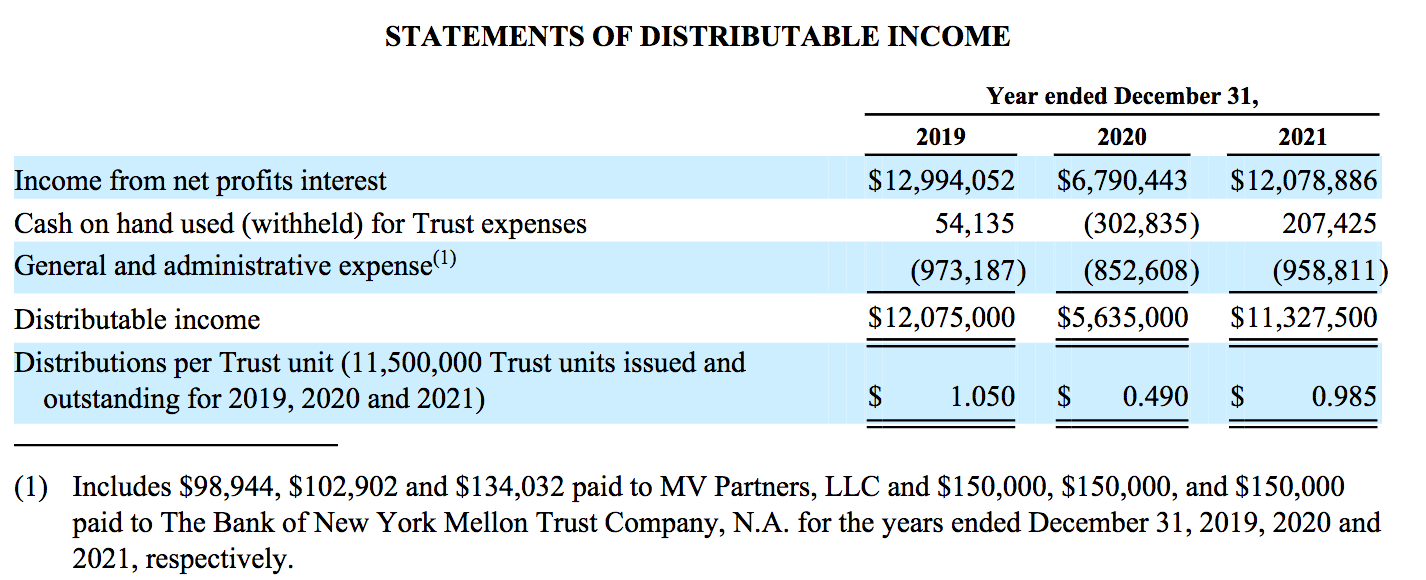

MVO’s Distributable Income is calculated via deducting Cash on Hand used for Trust expenses, G&A expenses, and future Trust expenses. In full year 2019, Distributable Income hit $12.075M, before plunging to $5.635M in 2020, and then bouncing back to $11.237M in 2021:

MVO site

Debt and Liquidity:

MVO has no debt. However, “Under the terms of the Trust Agreement, the Trustee is allowed to borrow money to pay Trust expenses. During the three months ended September 30, 2022 and 2021, there were no borrowings or amounts owed for money borrowed in previous quarters. MV Partners has provided a letter of credit in the amount of $1.8 million to the Trustee to protect the Trust against the risk that it does not have sufficient cash to pay future expenses.” (Q3 ’22 10-Q).

Performance:

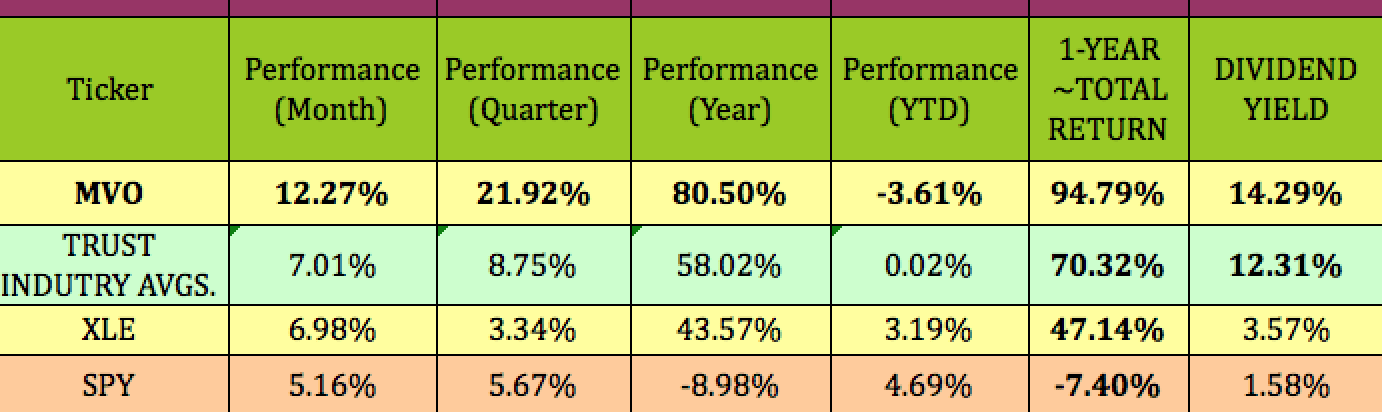

MVO outperformed the Trust industry, the Energy sector, and the S&P 500 over the past month, quarter, and year. It also outperformed on a total return basis over the past year. It’s lagging a bit so far in 2023, down -3.6%.

Hidden Dividend Stocks Plus

Valuations:

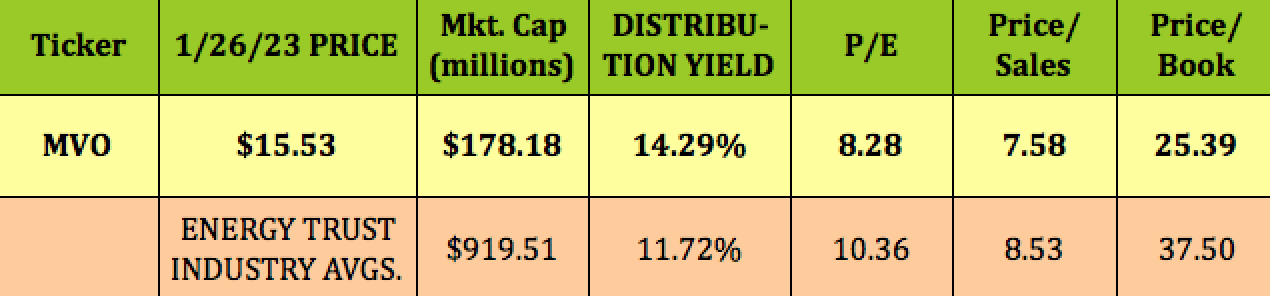

MVO is a small player in the Energy Trust industry, with a $178M market cap, vs. the $920M average. Its 14.29% trailing dividend yield is higher than average, and its trailing P/E and P/Sales are both lower than average, as is its Price/Book.

Hidden Dividend Stocks Plus

Parting Thoughts:

MVO’s fortunes are tied to the price of crude, so keep that in mind when deciding whether to invest in it. For example, if you think that crude oil prices will continue to be strong in 2023, given the existing supply chain changes in Europe, MVO could be a good way to go, but just be prepared for ups and downs in your quarterly distributions.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

Be the first to comment