RZ/iStock via Getty Images

Preamble

The kind of business I like is the boring type because I find it easier to find mispricing in an under-the-radar, uninteresting industry. Mueller Industries (NYSE:MLI) fits the bill. More about what it does in the Overview section below.

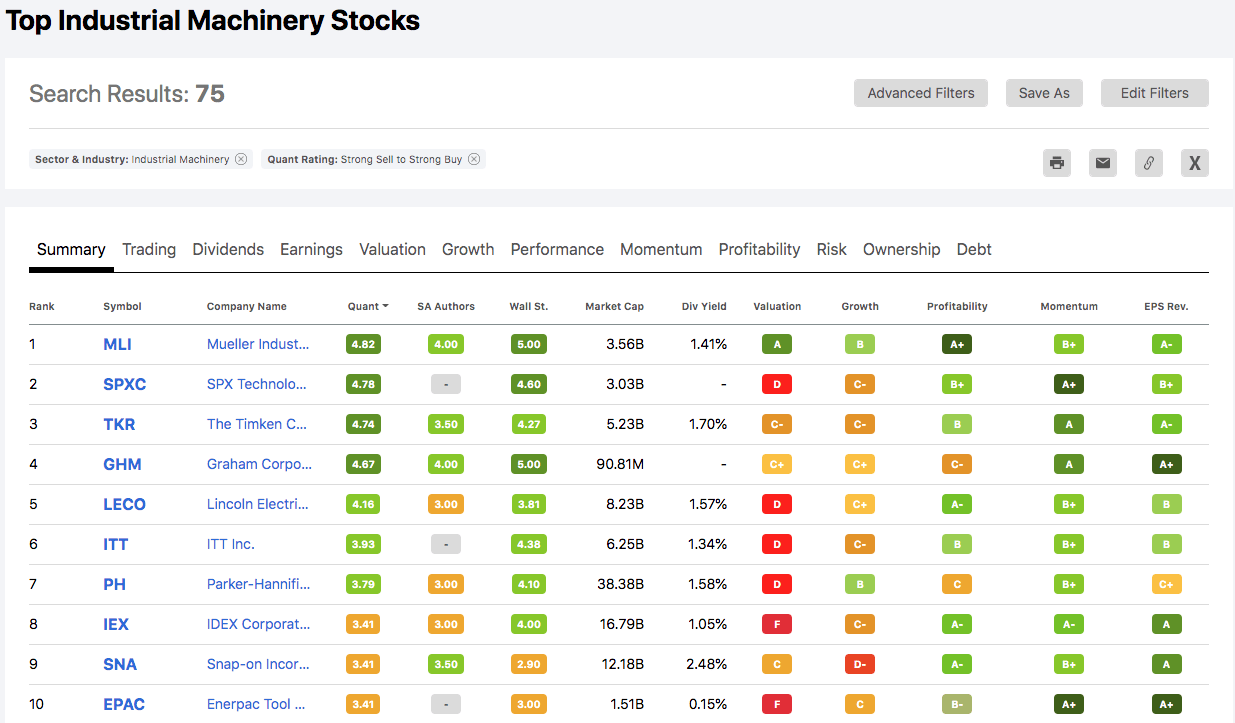

How did MLI come across my lap? Like many stock-pickers out there, I use different screens to surface investment ideas. One such tool that I use is Seeking Alpha’s Premium offering called the “Top Rated Stocks”. Using that tool, 54 top-rated stocks according to Seeking Alpha’s rating system surfaced. Mueller Industries, Inc is one of them.

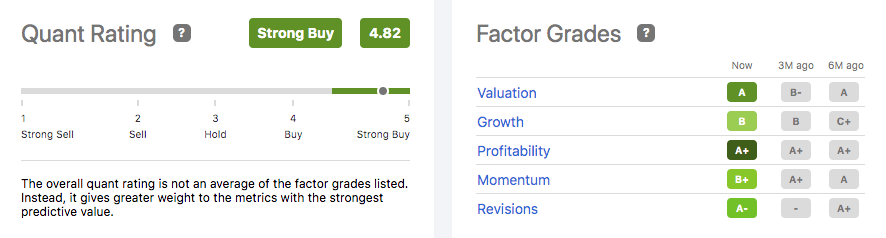

Seeking Alpha (MLI Rating)

MLI gets a “Strong Buy” rating of 4.82 out of a maximum score of 5. It is also ranked first place among its peers in the Industrial Machinery Stocks category.

Seeking Alpha (Top Rated Stocks)

Now, I do not rush out to buy any stock that has a “Strong Buy” rating from Seeking Alpha but a rating certainly serves to intrigue me to dig deeper. And on the surface, Mueller Industries, Inc looks like a dream stock at the moment. Based on numerous analysts’ fair value calculations as well as traditional valuation metrics like the price-to-earnings ratio, MLI is a bargain at the closing price of $62.58 trading only at a PE of 5.5 when historically, it has traded at an average PE of 18.48 between 2012 to 2020.

For investors seeking to de-risk their portfolio, MLI looks like a good fit. The company is a financial fortress that is ready to weather a rising interest rate environment. It just completed servicing the bulk of the debt outstanding and the total debt remaining is a mere $2.3 million so interest obligation on that debt load is insignificant. Plus, the company does not have any variable-rate debt outstanding. As of September 2022, MLI has $483 million of cash and cash equivalent, and dividing that by the total number of shares outstanding (56.8 million shares) leaves MLI in the enviable position of having net cash of $8.50 per share.

In the past year (and we all know how bad it has been for our portfolios), MLI’s outperformance makes it a superior outlier. It beat the S&P 500 by 34.7% and led its peers in the same industry by 27.7%. MLI’s great performance is not just restricted to just 2022. Its earnings from continuing operations increased 7.7 times from $83.7 million in 2012 to $649.3 million in 2022 (‘TTM’). Operating income soared 6.6 times between 2012 to 2022.

Copper and brass represent the largest component of MLI’s variable costs of production and with copper prices falling, gross margins have improved markedly. As a result, gross margin as a percentage of sales was 30.7% compared with 26.4 percent in the prior-year quarter.

MLI seems to have it all for an investor like me who likes to invest in good, boring businesses with strong balance sheets and pays decent dividends.

- Low debt? Check.

- Improving revenue? Check.

- Does it pay a dividend? Check.

- Trounced the 2022 market? Check.

- Improving operating income? Check.

- Undervalued based on analysts? Check.

- Net cash per share balance sheet? Check.

MLI looks great, no? Hold your horses! Investors must not simply look to the past. Even the most recent quarter’s result is a report based on past performance. We should also examine the future prospects of the company based on the best available information at hand to make a determination.

By the end of this article, I hope to address the following questions, and the answers should help me (and I hope you as well) make an informed decision.

- What does this company do?

- Is this a pandemic-induced growth story that is not sustainable in the near future?

- Is it really undervalued? Is it a buy, hold or sell at the current price?

1. Overview of the Company

Mueller Industries, founded in 1917, manufactures and sells products made of copper, brass, aluminum, and plastic. The operations are located throughout the United States and in Canada, Mexico, Great Britain, South Korea, the Middle East, and China.

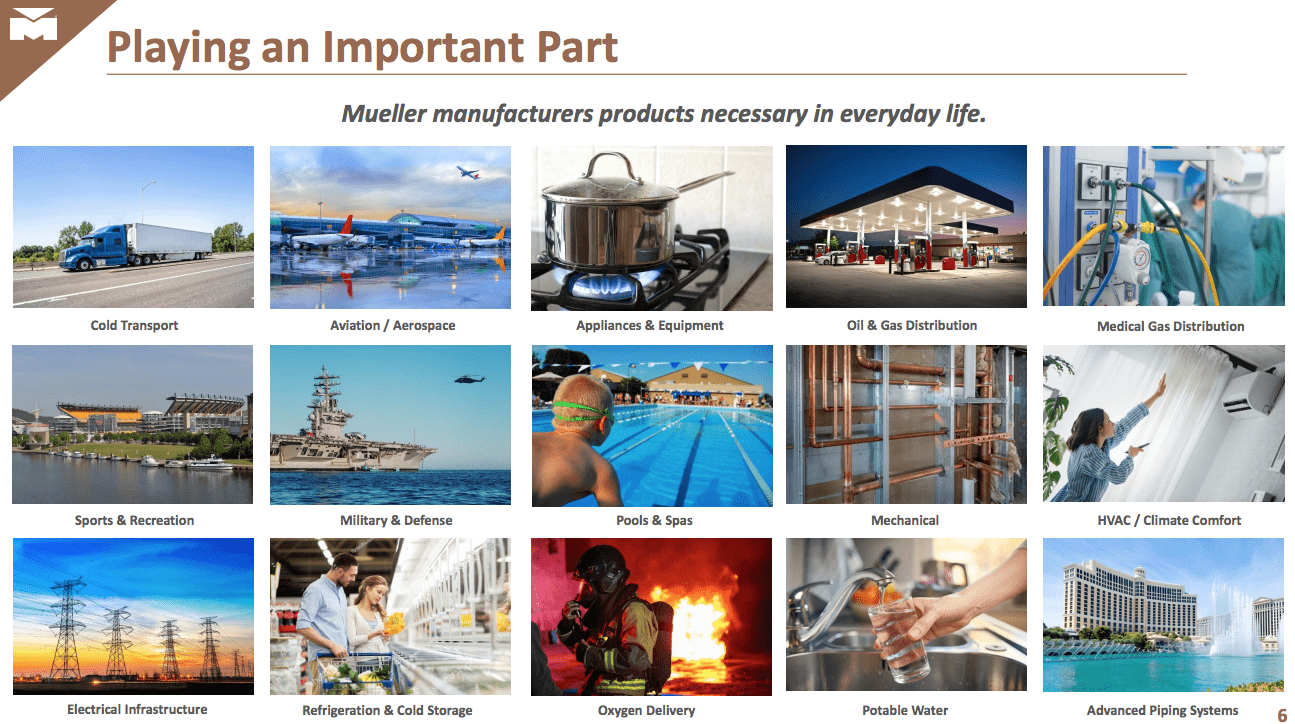

The products MLI makes have numerous use cases across multiple industries.

2022 Q3 Presentation Slides ((MLI))

The company reports its earnings in three main segments, namely Piping Systems, Industrial Metals, and Climate.

2022 Q3 Presentation Slides ((MLI))

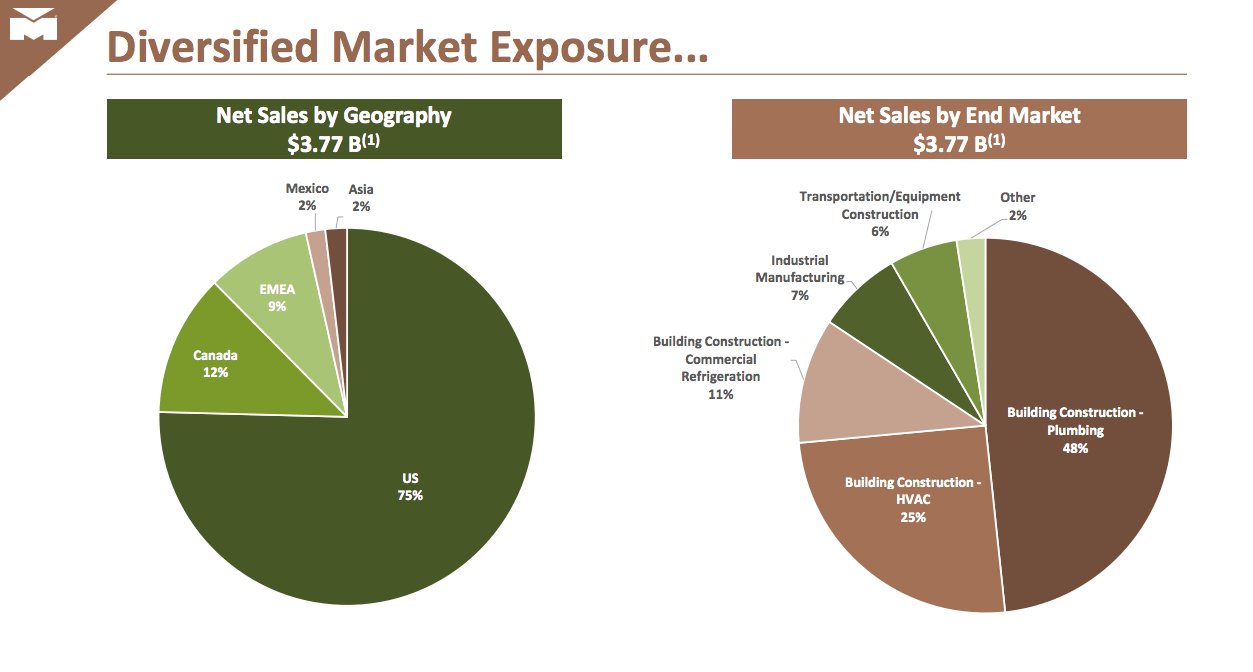

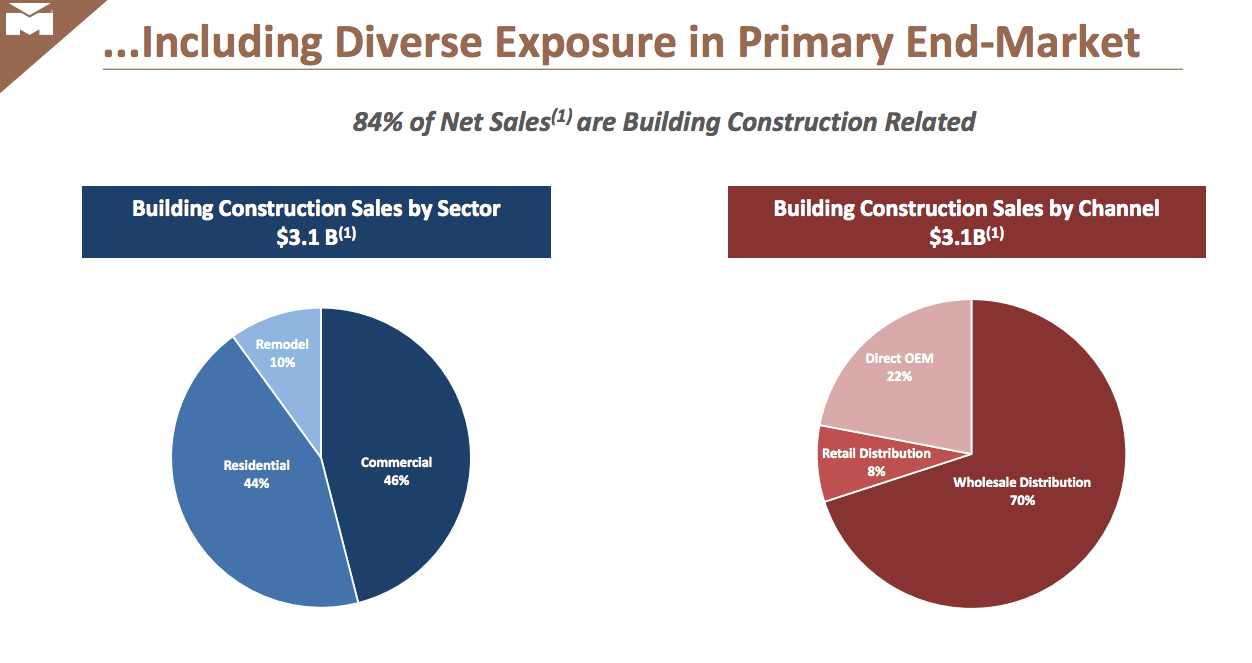

Although the company sells its products worldwide and in many industries, it is not as diversified as it claims. There are concentration risks geographically (87% of the sales originate from North America alone) as well as by end market (82% come from Building Construction – Plumbing, HVAC, and Commercial Refrigeration).

Of course, the plus side is there is less currency risk. And zero-covid measures in China (with Asia contributing just 2% of the total sales) and the war in Ukraine (EMEA makes up 9% of net sales) have less adverse impacts on both the top and bottom lines.

2022 Q3 Presentation Slides ((MLI))

Since most of the sales come from Building and Construction, and from the US, I will use that as a proxy to discuss the next segment.

2022 Q3 Presentation Slides ((MLI))

2. Is this a pandemic-induced growth story that is not sustainable in the near future?

As can be seen from the revenue, net income, and normalized diluted earnings per share results below dating from Dec 2012 to 2022 (‘TTM’), MLI’s revenue almost doubled in the 10-year period from 2012 to 2022, while its net income increased almost 8 times and the normalized diluted earnings per share jumped by more than 9 times.

Seeking Alpha Financials ((MLI))

Seeking Alpha Financials ((MLI))

Seeking Alpha Financials ((MLI))

The astute reader will no doubt observe that the major jump occurred from December 2020 to 2022. Revenue barely inched up 11% from 2012 to 2019, translating into a revenue growth rate of just 1.1% per year. Yes, net income increased by 24% in that 10-year period but that is hardly impressive.

However, revenue jumped by 69% or an average of 34.5% per year from December 2020 to 2022. Net income and earnings per share exploded by 362% and 345% respectively in the same 2-year period.

Management acknowledged in the 2021 annual report that

New housing starts and commercial construction are important determinants of our sales to the heating, ventilation, and air-conditioning, refrigeration, and plumbing markets because the principal end use of a significant portion of our products is in the construction of single and multi-family housing and commercial buildings…

According to the U.S. Census Bureau, actual housing starts in the U.S. were 1.60 million in 2021, which compares to 1.38 million in 2020 and 1.29 million in 2019. Mortgage rates remain at historically low levels, as the average 30-year fixed mortgage rate was approximately 2.96 percent in 2021 and 3.11 percent in 2020. The private nonresidential construction sector, includes offices, industrial, health care, and retail projects.

However, the tailwind situation described above which contributed to the residential construction boom in 2020 and 2021 and increased demands for Mueller Industries’ products has reversed drastically in the past 11 months. The strong tailwind in that period that contributed to MLI’s outstanding market-beating performance has dissipated in 2022.

Simply put, the housing situation has worsened in the past year. That can be examined from four angles – housing starts, number of houses sold, mortgage rates, and recession.

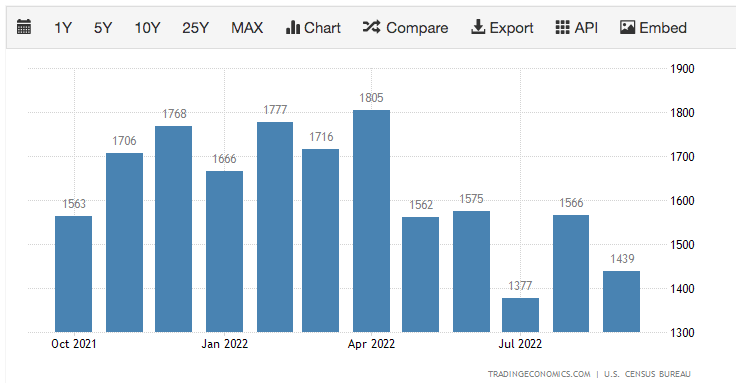

Firstly, housing starts in the US slid 8.1 percent to an annualized rate of 1.439 million in September 2022, well below the market consensus of 1.475 million. Fewer houses being built means demand for MLI’s products in the Building Construction Segment.

Housing Starts (Trading Economics)

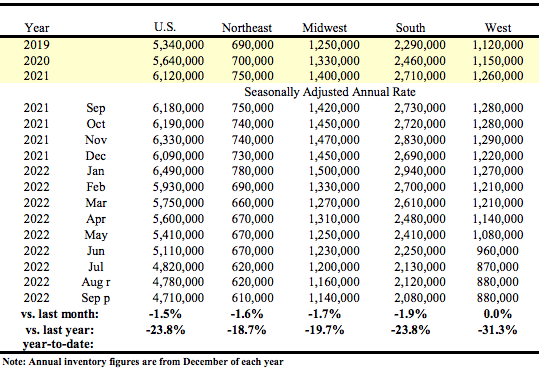

Secondly, the number of houses sold, after peaking in January 2022, has declined 23.8% on a year-to-date basis to 4.71 million. Fewer houses sold means more houses are left unsold, reducing demand for new houses and hence reducing demand for MLI’s products in the Building Construction Segment.

Existing Home Sales (National Association of Realtors)

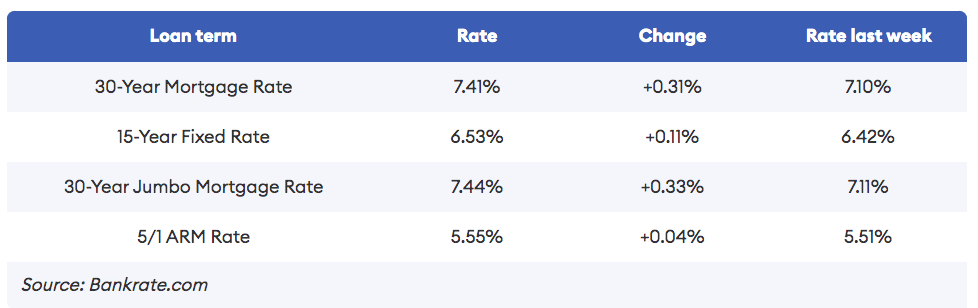

Thirdly, as the Federal Reserve continues to raise the federal fund rate, that had increased the cost of borrowing. Mortgage rates just reached their highest level since 2002. As of 4 November 2022, the 30-year mortgage rate in America hit 7.41%, compared to 7.10% just a week earlier; it was only 2.96% in 2021. The 15-year fixed mortgage rate is not much better at 6.53% up from 6.42% in the previous week.

Mortgage Rates (Bank Rate)

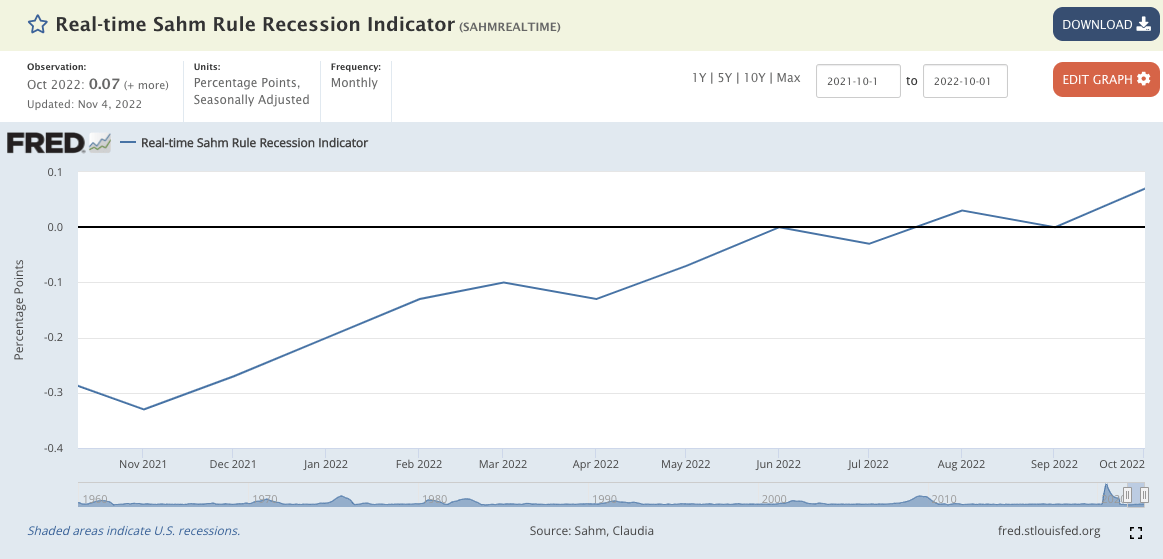

Fourthly, the dreaded “R” word is not yet official but most economic commentators are certain that recession is either here or is approaching in 2023. The Sahm Rule Recession Indicator is an accurate recession predictor. It signals the start of a recession when the three-month moving average of the national unemployment rate (U3) rises by 0.50 percentage points or more relative to its low during the previous 12 months. The lowest point in the past 12 months was in November 2021 at -0.33. The figure in October 2021 is 0.07, an increase of 0.40 percentage points, just 0.10 shy of hitting 0.50. I would say we are pretty close to a recession based on the Sahm Indicator.

Sahm Recession Indicator ((FRED))

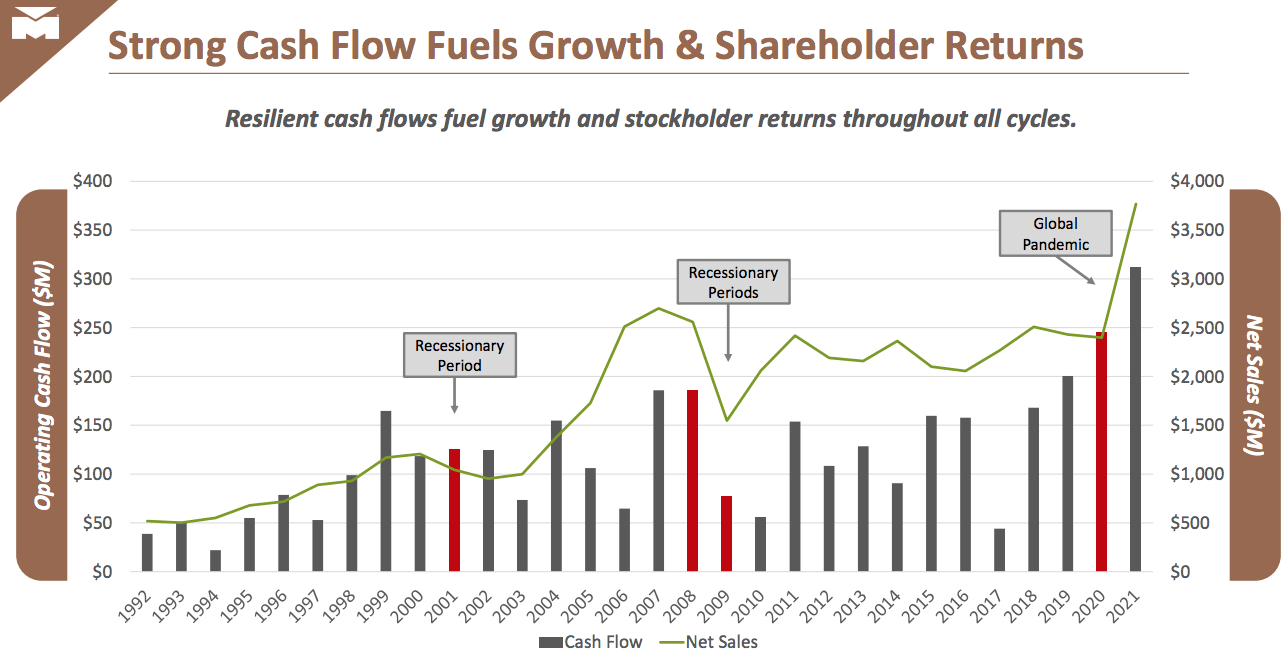

According to MLI’s own investor presentation slides, the company’s net sales (green line) always decreased during the previous recessionary periods from 2000 to 2003 and 2008 to 2010.

2022 Q3 Presentation Slides ((MLI))

After looking at the above data, I have to conclude that the fantastic growth in revenue, net income, and earnings per share from December 2020 to 2021 was fueled by the unique circumstances (low-interest rates and red hot property market) of the early pandemic years, and the changes in these circumstances in 2022 means that such growth cannot be sustained. In fact, the expectation should be for MLI’s growth to fall off a cliff in 2023.

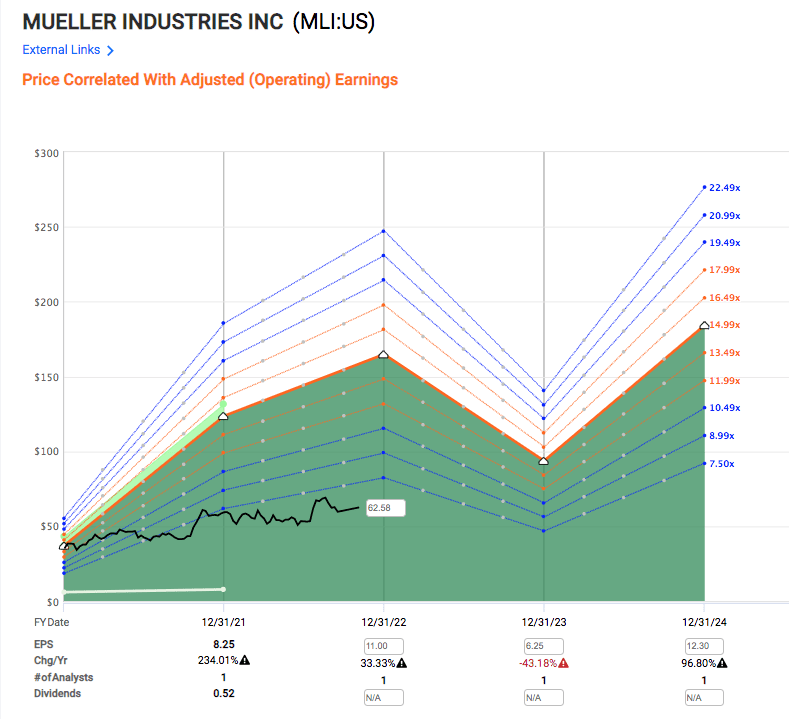

The analyst from FactSet believes that Mueller Industries’ adjusted operating earnings will fall as much as 43% in 2023 from $11 in 2022 to just $6.25 in 2023. Interestingly, the same analyst also thinks that earnings will recover sharply in 2024 to $12.30.

Earnings Estimates by Factset (Fast Graph)

That optimistic projection for 2024 is probably based on new home sales forecast projecting long-term new home sales in America to trend upwards from the expected 550 thousand units by end of 2022 to 600 thousand units in 2023 and 690 thousand units in 2024.

I am less optimistic about Mueller Industries making a recovery in sales by 2024. Assuming that we are already in a recession, Mueller Industries’ own history showed sales declined for 2-3 years before the downward trend reversed. Can MLI really recover in just one year?

Then, could the saving grace come from a boom in the Building Construction of Commercial properties? After all, this segment of the business is responsible for 46% of MLI’s total revenue.

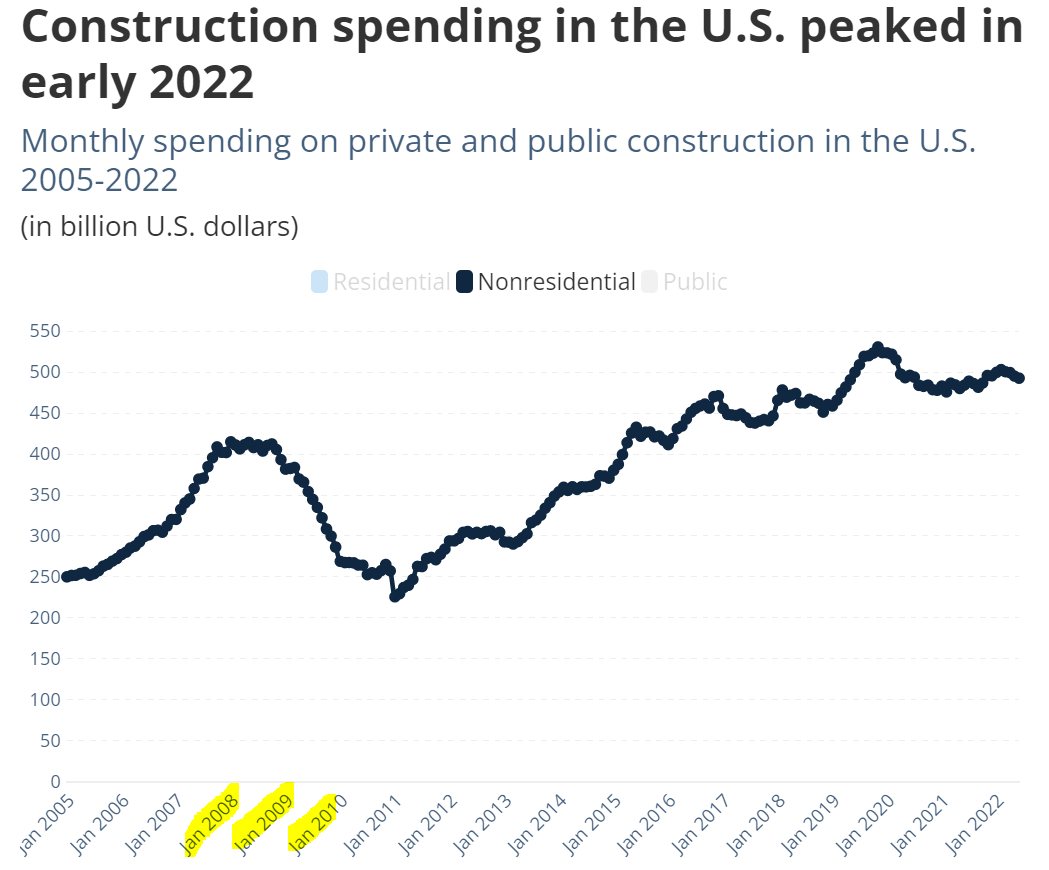

The following chart from Statista shows the amount of money spent on non-residential construction from 2005 to 2022. In the three years of the Great Recession from 2008 to 2010, spending on non-residential construction plummeted close to 50% from $414 billion in May 2008 to $225 billion in January 2011. The spending in non-residential construction did not recover to the 2008 peak until 7 years later in 2015. With a recession on the horizon, I do not expect any form of recovery in the near term.

Construction Spending on Non-residential (Statista)

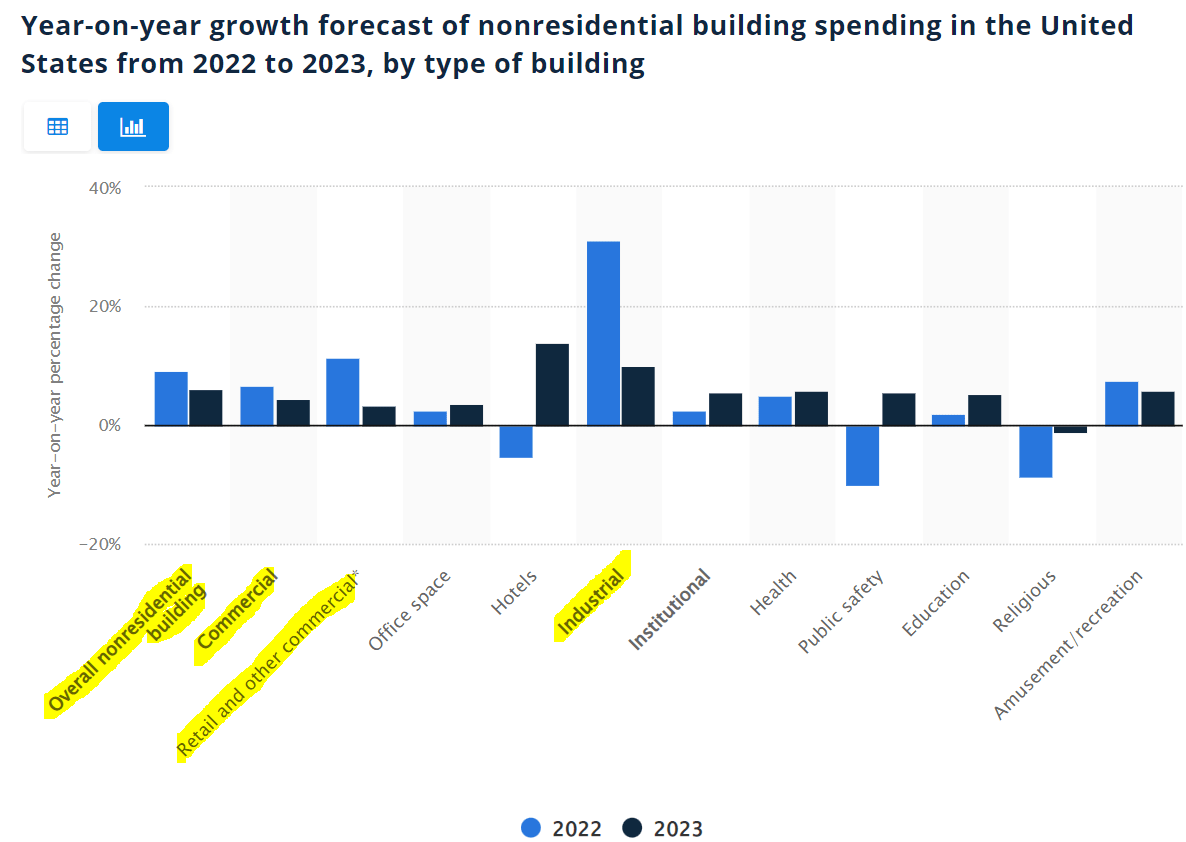

In fact, the forecast for non-residential building spending in the United States for 2023 is expected to decline overall, with the majority of the decline coming in from Commercial, Retail, and Industrial related construction.

Non-residential construction forecast for 2023 (Statista)

Statista figures are corroborated by research from other sources. According to the following research on commercial construction in the United States from Mordor Intelligence,

The annual growth rate in revenue from 2016-2020 has been 8.47%, 5.15%, 3.43%, 2.66%, and 2.07%. There has been a clear decline in the growth rate of construction industry as a whole, with further impacts of COVID-19 clearly coming into picture in Q2, 2020, which would obviously be following the trend. At the same time, specialized construction activities are expected to depict a rise of 2.1 % in 2020 as against 8.47% reported in 2016…

Commercial space occupancy has shown a decline in growth, after a consistent increase until 2019…

Do you think MLI can continue to post record revenue and earnings growth in 2023 in the face of an almost certain decline in revenue due to unfavorable macroeconomic forces that are beyond its control? I do not think that is possible and it is from that position that I do my valuation of MLI. And with this, I move into the third and final question.

3. Is it really undervalued? Is it a buy, hold or sell at the current price?

As mentioned in the Summary bullet points and the Preamble, Mueller Industries seemed to be undervalued in the eyes of professional analysts.

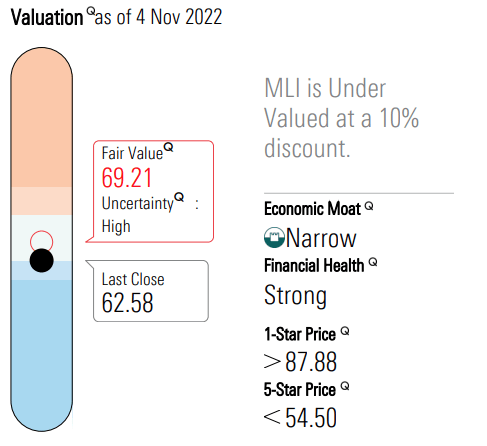

Morningstar analyst valued MLI at $69.21.

Morningstar (Fair Value for MLI)

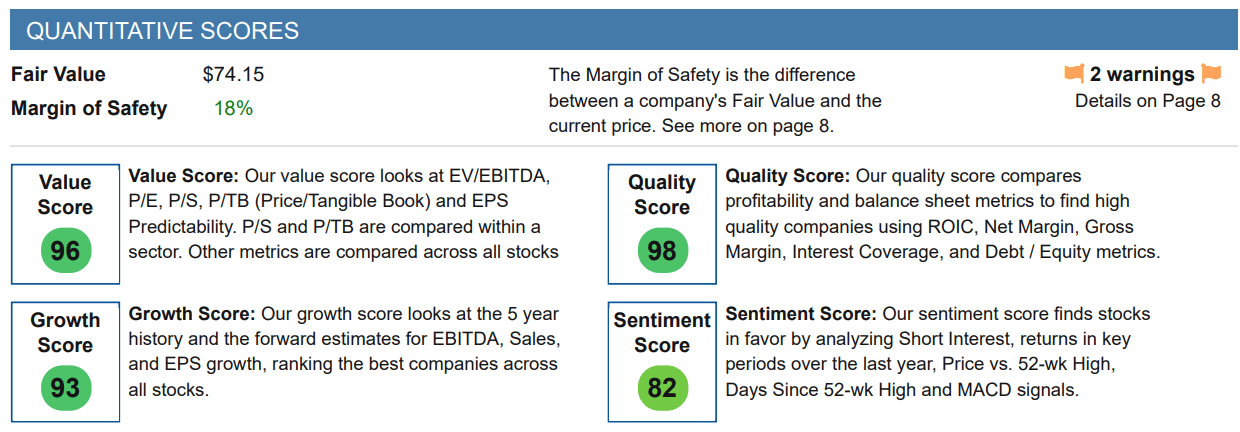

The analyst at Stock Rover gave MLI a fair value of $74.15.

Stock Rover (Fair Value for MLI)

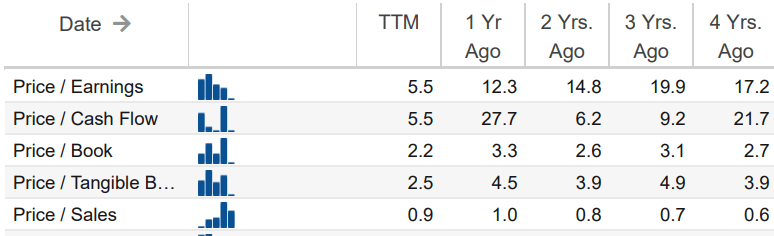

Based on price multiples such as price-to-earnings, price-to-cash flow, price-to-book value, and price-to-tangible book value, Mueller Industries is the cheapest it has ever been in the last 4 years.

Stock Rover (Price Multiples)

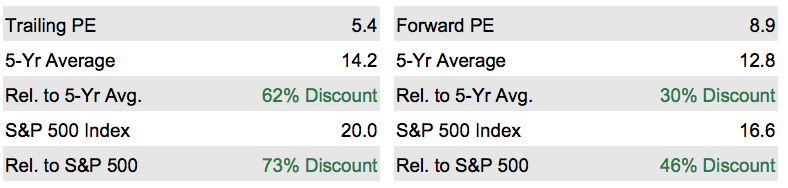

The analyst from Refinitiv believes that MLI is trading at a huge discount to its own 5-year average as well as relative to S&P 500 and assigned a price target of $100 for the stock. As a price target is not the same fair value, I will not be using it in my subsequent calculations.

Refinitiv (Relative Valuation)

However, looking forward to 2023 and beyond, if we are expecting the economy to enter into a recession that will extend for at least 1 to 2 years, and expecting the residential housing market to do poorly at least in 2023 due to the abovementioned reasons in Part 2 (fewer housing starts, higher mortgage rates, declining home sales, impending recession), and the non-residential market to also decline in growth, some cautious tempering of exuberance is warranted. Extrapolating MLI’s recent successes to the future cannot be the right way to approach the valuation of this company. Instead, a more reasonable valuation model has to factor in a decline in revenue at least in 2023, which was what I did in my “guesstimate” fair value for MLI.

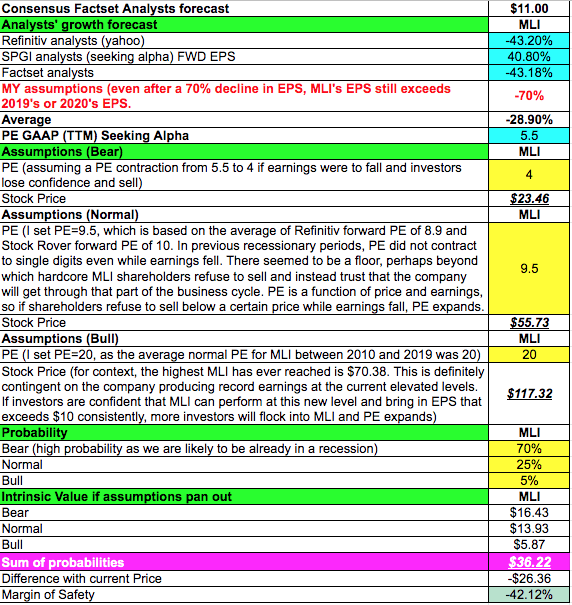

My “guesstimate” at a possible fair value for MLI is $36.22. My input considerations are described in the table below.

Fair Value Guesstimate (Author)

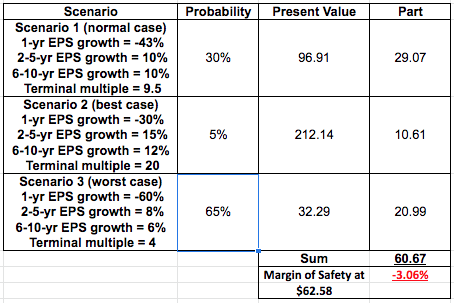

For a more layered model, I used my DCF model, factored in different possible earnings growth rates over a 10-year period, and I arrived at a fair value of $60.67.

DCF for MLI (Author)

In the worst-case scenario of my DCF calculations, I assumed a 65% chance that a recession is either already here or is coming soon. The 65% figure came from many reports such as Forbes and NY Post stating nearly two-thirds of economists surveyed believe that recession is soon upon us if not already. In this worst-case scenario, I also considered a longer recovery period (as per MLI’s own history) and that earnings growth would resume at 8% from 2024 to 2028, which may slow to 6% from 2029 to 2032 by factoring another slowdown in the business cycle.

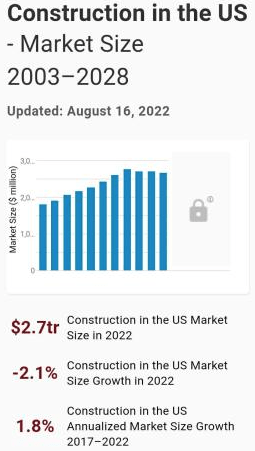

I do not think that my worst-case scenario is overly conservative. Bear in mind that the residential construction industry in the US grew only 1.8% per year in the past 5-years and in 2022 alone that growth has already contracted by -2.1%. Growth in the non-residential construction has already started showing a decline from as early as 2019.

Construction in the US (Ibisworld)

Admirably, MLI has been able to grow EPS by almost 50% from 2012 to 2019 despite having an average annual revenue growth of just 1%. The company achieved that through cost cutting, improved efficiencies, and share buybacks (71 million shares in 2012 to 56 million shares in 2019), but let’s be realistic – there is only so much a company can squeeze out in EPS when revenue does not grow as much.

What is the final fair value of Mueller Industries?

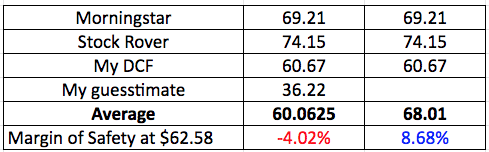

I do not assume that I am right so I aggregated the different fair value figures and when I averaged out these I arrived at a fair value price of $60.06 per share which does not offer any margin of safety at all. Even when I removed the “outlier” result from my guesstimate, the margin of safety at the current price is but a narrow 8.68%.

Average FV for MLI (Author)

Conclusion

I will rate Mueller Industries as a hold for now.

Yes, it is a company that met my many criteria for a “good investment” based on its past performance but when the causes of the outperformance were examined more closely, I am simply not convinced that MLI can continue to perform as well as it did from December 2020 to 2022, in light of the negative macroeconomic conditions.

In the period before the pandemic from 2012 to 2019, the company underperformed against the S&P 500 even with dividends reinvested. Pre-pandemic, MLI had traded in the low $30 range ($33 on 1 Feb 2020) so for the stock price to revert to the $36.22 level based on the very conservative assumptions used for my guesstimate is entirely conceivable.

MLI Under-Performance 2012 to 2019 (Fast Graph)

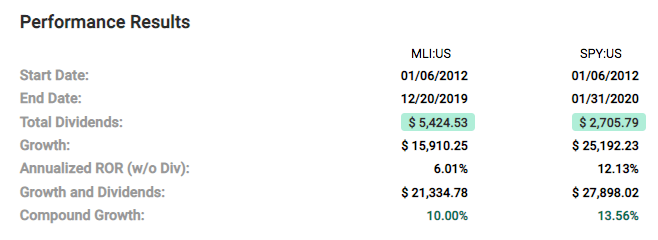

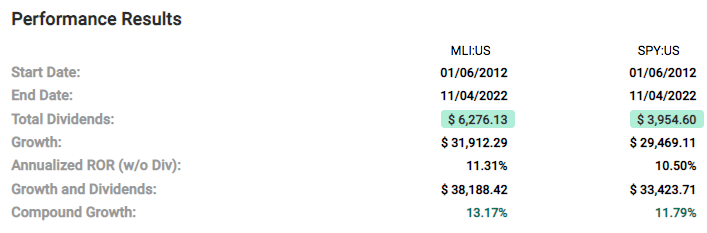

Yes, MLI did outperform the S&P but that slight outperformance of 11.31% versus S&P’s 10.50% (without dividends) came only after achieving amazing results from 2020 to 2022.

MLI Outperformance 2012 to 2022 (Fast Graph)

Therefore, I believe that MLI is fairly valued now at best. Even if the analysts at Morningstar and Stock Rover are correct in their fair value estimates of $69.21 and $74.15 respectively, the reward of waiting for MLI price to appreciate to those fair values, versus the risk of an almost certain recession at our doorstep leading to a subsequent fall in revenues that drags the stock down, is just not favorable.

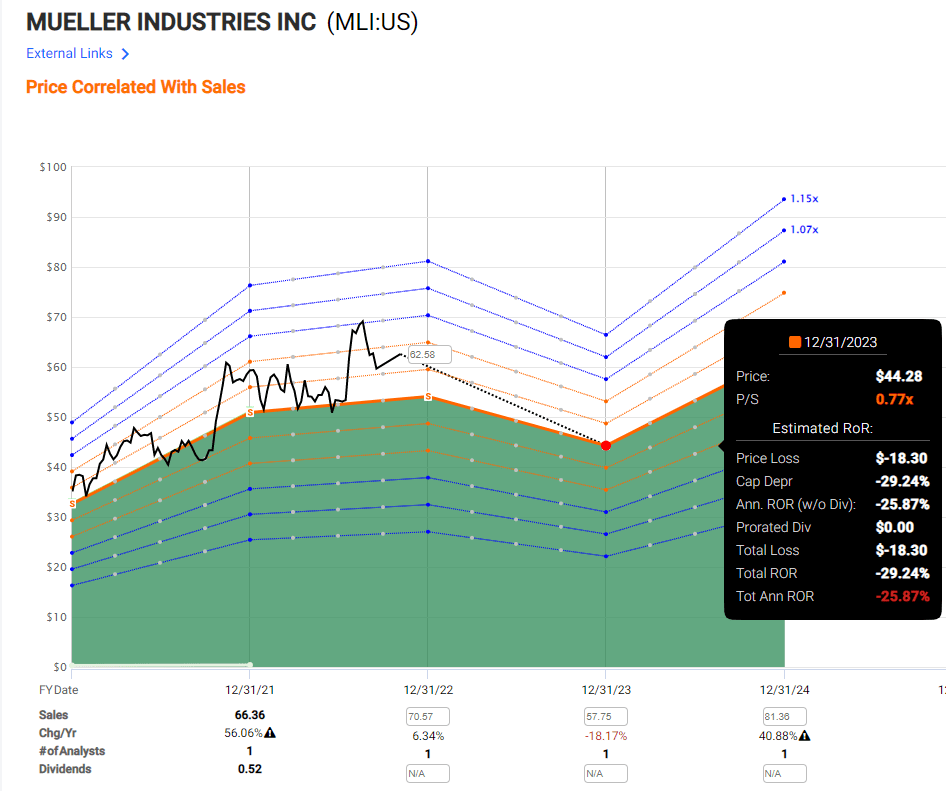

I have added MLI to my watch list and has set an alert at $44, which is how MLI might be priced at a P/S of 0.77. Below $44, I would be very interested in Mueller Industries.

Valuing MLI using Price-to-sales (Fast Graph)

Be the first to comment