bjdlzx/E+ via Getty Images

Various industries, including the energy, industrial, and gas utility and markets, require significant amounts of pipes, valves, and fittings in order to continue functioning and in order to grow. One company dedicated to these types of products is MRC Global (MRC). You would think that with the general trend of energy consumption being a positive one, that financial performance for the company would be consistently positive as well. But the fact of the matter is that this business has proven to be extremely volatile on both its top and bottom lines. At least in recent years, cash flows for the business have been positive. But even those have been subject to extreme volatility. This is why shares of the firm are trading at rather low levels at this moment. And while the company might offer attractive upside in an environment where demand for its services is on the rise for an extended period of time, more likely than not, the low price shares are trading for are justified.

An important niche player

Today, MRC Global operates as a global distributor of pipe, valves, and fittings that services the diversified energy, industrial, and gas utility end markets. When I talk about diversified energy, I am particularly talking about companies all across the spectrum of the energy space. These include, but are not limited to, downstream and energy transition firms such as crude oil refining companies, petrochemical firms, and chemical processing businesses, as well as upstream production companies like exploration and production firms, and midstream pipeline operators.

According to management, MRC Global offers over 250,000 SKUs that include not just the basic pipes, valves, and fittings, but that also include oilfield supplies, valve automation equipment, measurement, instrumentation, and other general and specialty products, and more. It does all of this through a network of over 10,000 suppliers and it services its over 10,000 customers through both its digital commerce applications and the 210 service locations that it has in operation.

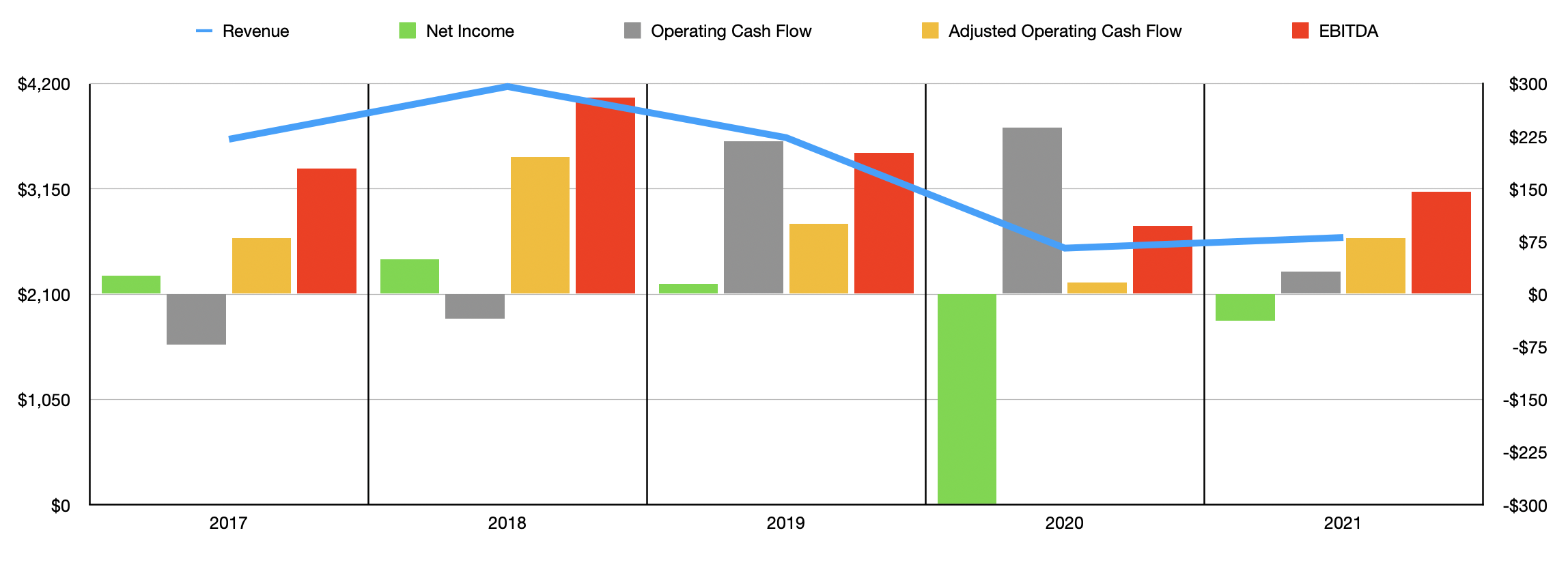

Author – SEC EDGAR Data

Over the past few years, the financial performance of MRC Global has been all over the place. After seeing revenue jump from $3.65 billion in 2017 to $4.17 billion in 2018, it then proceeded to plummet, eventually hitting $2.56 billion in 2020. Then, in 2021, revenue increased slightly, coming in at $2.67 billion. We do know that some of the company’s performance is tied to the international energy exploration and production market. This is because management stresses the importance of certain industry indicators such as the drilling rig count in the US and abroad. And, to an extent, revenue does seem to be related to this rig count. As an example, back in 2019, when revenue was $3.66 billion, the total worldwide rig count in operation was 2,175. As revenue dropped to $2.56 billion in 2020, we saw the rig count decline to 1,347. A modest increase to 1,365 rigs took place in 2021 as revenue also increased modestly to the $2.67 billion we saw that year.

Looking deeper into the numbers, we can see that during this three-year window, the revenue associated with the downstream, industrial, and energy transition category of customers dropped from $1.15 billion to $783 million. Upstream production revenue took an even larger beating, this directly related to the rig count, falling from $1.11 billion to $542 million. And the midstream pipeline category saw revenue drop from $593 million to $333 million. The only area in which the company actually fared well was when it came to its gas utilities business. Sales associated with this sector expanded from $857 million to $1.01 billion.

Just as revenue has been volatile, profits for the business have also been volatile. In both of the past two years, the company generated net losses. And in the years prior to that, profits were rather slim. The best of the past five years was in 2018 when the company achieved net income of $50 million. Operating cash flow has been only marginally better. But at least it was positive for each of the past three years. If we adjust for changes in working capital, the picture has been slightly more consistent, with a positive reading in all of the past five years. But this has ranged from a low of $17 million in 2020 to a high of $196 million two years earlier. Meanwhile, EBITDA has jumped around a rather significant range, moving from a low of $97 million to a high of $280 million. Given all of this volatility, investors should be surprised that management is able to give any guidance covering the 2022 fiscal year at all. However, they anticipate that for the year, the company should generate revenue of around $3 billion and EBITDA of around $190 million. If this comes to fruition, it would imply operating cash flow likely in the range of $111.3 million.

Author – SEC EDGAR Data

Taking this data, we can price the company, with the obvious understanding that the volatility of the business makes the evaluation process rely on the assumption that such volatility will not continue. Using the 2021 figures, the company is trading at a price to adjusted operating cash flow multiple of 10.4. This drops to 7.5 if we rely on 2022 estimates. Meanwhile, the EV to EBITDA multiple with the company is 9.9, with that declining to 7.6 if we rely on the 2022 estimates. To put this all in perspective, I decided to compare the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 3.4 to a high of 33.9. Two of the five companies were cheaper than MRC Global. Meanwhile, the EV to EBITDA multiples of these firms ranged from a low of 2.7 to a high of 26.1. And, once again, our prospect was cheaper than all but two of the firms.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| MRC Global | 10.4 | 9.9 |

| BlueLinx Holdings (BXC) | 7.9 | 2.7 |

| NOW (DNOW) | 33.9 | 17.9 |

| Titan Machinery (TITN) | 3.4 | 8.7 |

| Global Industrial Company (GIC) | 23.6 | 12.3 |

| Transcat (TRNS) | 28.2 | 26.1 |

Takeaway

Given what we know, MRC Global looks like an interesting prospect but it’s not for the faint of heart. The company is extremely volatile and has a history of negative earnings in recent years. That includes the most recent 2021 fiscal year. Fortunately, cash flows have been consistently positive. However, the range makes valuing the company rather difficult. It’s likely because of this uncertainty that shares are priced where they are today. And all those shares do look cheap at current levels, it is telling that the company is around the midpoint of what the other similar firms that I looked at are trading for. These types of firms warrant some sort of discount on valuation on an absolute basis because we don’t know what fundamental performance might be from year to year.

Be the first to comment