Without question, 2020 Q1 will go down as the most destructive quarter for the stock market in history. While the coronavirus pandemic has unleashed havoc across the board, mortgage REITs (MORT) join the ranks of airlines, energy among the worst hit sectors. Indeed, a supposedly overvalued correction turned into an obliteration, as MORT collapsed from $25 by more than 70% before a reprieve back to $10:

Source: WingCapital Investments

The causes behind the unforgiving sell-off have been well covered by fellow SA authors. To wit from Colorado Wealth Management:

Uncertainties surrounding their ability to survive led to most of MORT’s top holdings trading well under their book value. Although many look seemingly cheap with price-to-book ratios deep under 1.0x, this is largely due to stale book values that have not taken into account of impact from margin calls, hedge losses, etc.

| Symbol | Name | % Weight | Price |

Price-to-Trailing Book Value |

| NLY | Annaly Capital Management Inc | 16.31% | 5.13 | 0.53 |

| AGNC | AGNC Investment Corp | 13.07% | 10.45 | 0.56 |

| STWD | Starwood Property Trust Inc | 7.21% | 10 | 0.61 |

| NRZ | New Residential Investment Corp | 5.64% | 5.1 | 0.31 |

| CIM | Chimera Investment Corp | 5.39% | 9.1 | 0.43 |

| BXMT | Blackstone Mortgage Trust Inc A | 5.23% | 18.65 | 0.67 |

| HASI | Hannon Armstrong Sustainable Infrastructure Capital Inc | 4.45% | 20.45 | 1.49 |

| ARI | Apollo Commercial Real Estate Finance Inc | 4.26% | 7.42 | 0.43 |

| PMT | PennyMac Mortgage Investment Trust | 3.90% | 10.63 | 0.50 |

| BRMK | Broadmark Realty Capital Inc Ordinary Shares | 3.78% | 7.53 | 0.84 |

| ABR | Arbor Realty Trust Inc | 3.57% | 4.9 | 0.49 |

| TWO | Two Harbors Investment Corp | 3.21% | 3.85 | 0.26 |

| LADR | Ladder Capital Corp Class A | 2.85% | 4.81 | 0.35 |

| IVR | Invesco Mortgage Capital Inc | 2.46% | 3.4 | 0.21 |

| NYMT | New York Mortgage Trust Inc | 2.61% | 1.57 | 0.27 |

| ARR | ARMOUR Residential REIT Inc | 2.26% | 8.8 | 0.36 |

| CLNC | Colony Credit Real Estate Inc Class A | 1.90% | 3.91 | 0.24 |

| MFA | MFA Financial Inc | 2.02% | 1.52 | 0.20 |

| RWT | Redwood Trust Inc | 1.80% | 5.2 | 0.33 |

| KREF | KKR Real Estate Finance Trust Inc | 1.56% | 15.01 | 0.77 |

| MORT Top 20 | Weighted Average | 93.48% | 0.53 |

As of 2020/03/31. Source: TIKR.com

We will first admit we are not experts in mREITs, but will chime in on why MORT is not a compelling buy at these seemingly fire-sale prices based on a macro and historical analysis of some of its top holdings’ price trajectory during the 2008 Great Financial Crisis.

Long & Tough Road Ahead For mREITs If 2008 GFC Is Any Precedent

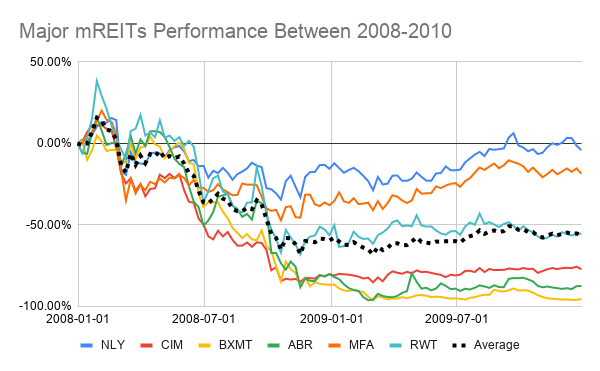

Without a doubt, today’s viral-turned-financial crisis is unlike any other, but mortgage-backed securities once again being a focal point draws eerily similarities to 2008. The 6 major mortgage REITs that existed back then and remain top holdings of MORT today likewise collapsed close to 70% on average from beginning of 2008 into the peak of the crisis in November:

Source: WingCapital Investments

Source: WingCapital Investments

NLY and MFA were the notable outperformers, with the former actually climbing all the way to unchanged by end of 2009. On the other hand, CIM, BXMT and ABR remained mired near their lows despite a reinvigorated stock market and economy. On average, the group collectively gained an anemic 20% off the lows and remained down over 50% from beginning of 2008, due to the polar opposite recovery pictures of the individual names.

Next we take a look at 6 mREITs’ book values between end of 2007 and 2009:

| Symbol | Name | 2007 Book Value | 2008 Book Value | 2009 Book Value | Chg % | 2007-2008 | 2008-2009 |

| NLY | Annaly Capital Management Inc | 12.51 | 13.27 | 17.64 | 6.08% | 32.93% | |

| CIM | Chimera Investment Corp | 71.45 | 11.70 | 15.85 | -83.62% | 35.47% | |

| BXMT | Blackstone Mortgage Trust Inc A | 237.80 | 181.90 | -77.61 | -23.51% | -142.67% | |

| ABR | Arbor Realty Trust Inc | 19.26 | 11.18 | 3.81 | -41.95% | -65.92% | |

| MFA | MFA Financial Inc | 7.32 | 5.73 | 7.74 | -21.72% | 35.08% | |

| RWT | Redwood Trust Inc | 23.18 | 9.02 | 12.50 | -61.09% | 38.58% | |

| Average | -37.64% | -11.09% |

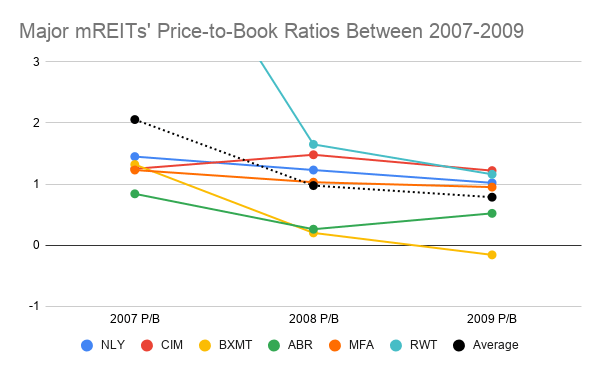

Aside from NLY being the exception, the mREITs’ book values plummeted not only during 2008, but into 2009 as well for certain names like ABR. The price-to-book ratios generally converged to 1.0x by 2009, though a couple remained suppressed deep under 1.0x:

Source: WingCapital Investments, TIKR.com

| Symbol | 2007 P/B | 2008 P/B | 2009 P/B |

| NLY | 1.45 | 1.23 | 1.02 |

| CIM | 1.25 | 1.48 | 1.22 |

| BXMT | 1.32 | 0.2 | -0.16 |

| ABR | 0.84 | 0.26 | 0.52 |

| MFA | 1.23 | 1.03 | 0.95 |

| RWT | 6.25 | 1.65 | 1.16 |

| Average | 2.06 | 0.98 | 0.79 |

To summarize our observations:

- mREITs suffered heavy declines resembling recent times during the 2008 GFC and rebounded only slightly as a group after the crisis drew to a close

- Book values plunged in a wide range between 20-80% during 2008 with some dropping even into end of 2009

- Price-to-book ratios generally converged to 1.0x, but those trading in deep discount continued to stay depressed

Buying A Pool of mREITs Is Not Worthwhile

The above analysis shows that while some mREITs like NLY were able to weather the storm well during 2008, others would remain in distressed mode even after broader markets and economy started getting back on their feet. Indeed, for an industry essentially facing an existential crisis, it becomes a matter of survival of the fittest in our opinion, and as such it would not be surprising if some would end up headed for bankruptcy.

This brings to our conclusion that the reward-to-risk of buying an ETF with a pool of mREITs is not compelling, as the bifurcation in the performance between superior and inferior names will most likely lead to an overall subpar return in the ETF itself. In other words, diversification could end up being detrimental in our opinion. Given the dividend cuts, their leveraged nature that does not cope well in a financial crisis, combined with profound economic uncertainties, a turnaround in the sector as a whole appears highly unlikely for the foreseeable future. Hence, we would avoid MORT or other ETFs, and instead focus on robust individual names that have a good chance of coming out on top once the dust settles.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment