Getty Images

What if I told you that Morgan Stanley (NYSE:MS) now sports a dividend yield of over 4%? Or that their return on equity is in the teens while keeping leverage low enough to see their credit rating upgraded? The big news on Morgan Stanley lately was that they passed the Fed’s latest stress test with flying colors, and were able to raise the quarterly dividend to $0.775 per share and announce a $20 billion buyback. The bank’s acquisition of E-trade gives them access to a variable rate margin loan book paying them up to 10% and the potential to benefit from increased trading fees in a market selloff. As crazy as it sounds, I believe Morgan Stanley’s prospects today aren’t completely different than Apple’s in the early 2010s (AAPL), with a low PE, a solid growth plan, and a stock market that doesn’t get it yet.

MS stock trades for 9.6x 2023 earnings estimates. That’s cheap. Interestingly, there are actually quite a few companies trading for single-digit P/E ratios right now: homebuilders (ITB), automakers like Ford (F), shipping stocks like ZIM (ZIM), and oil stocks like Exxon (XOM). Historically, when stocks in cyclical industries trade for low P/E ratios they can be value traps because the rosy earnings estimates will never be hit. Whether these low these P/E stocks are a great buy for investors or a gigantic trap is one of the most vexing questions in the market today.

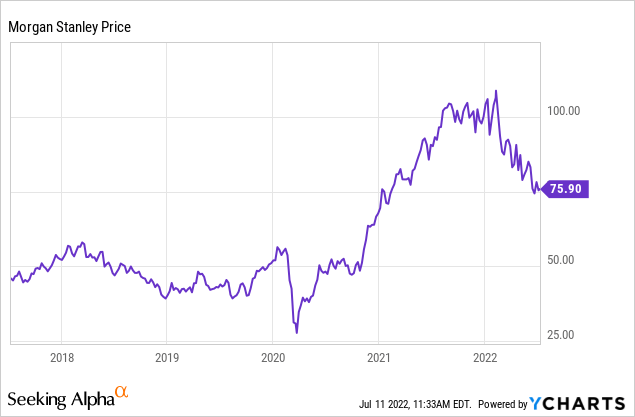

If you look at the 5-year graph of MS stock, the hot take is that it’s just another stock that got ahead of itself during COVID. But post-GFC Morgan Stanley isn’t nearly as cyclical as some of these other companies, and MS has a much better credit rating and less retail/meme trader interest. MS’s better position is easily verified by comparing Morgan Stanley’s income statements and balance sheet with other single-digit P/E stocks. The bears aren’t coming from nowhere here – the capital markets business is very cyclical, particularly investment banking. The IPO market has pretty much ground to a halt. And loan reserves are a perennial problem in recessions.

I recently saw some young investment bankers on social media posting about hanging out at the pool and playing video games! Last year, people in IPO and SPAC groups were featured in the news for 100-hour workweeks. Layoffs are coming down the pike for young investment bankers who aren’t generating much revenue anymore. Reducing inefficiencies is an ongoing process for Morgan Stanley, which is in the process of integrating a dozen or so acquisitions. But worrying about capital markets revenue is overdone.

The E-Trade acquisition will be very helpful for the stability of their earnings, as trading rises in down markets, while they can pass through higher interest rates to margin customers. Morgan Stanley’s credit rating was recently upgraded to A-, echoing the Fed in confirming the stability of the company. And management’s push to expand their business in wealth management diversifies their revenue streams further.

As I wrote last year, the game plan for Morgan Stanley is pretty simple:

- Find cheap sources of financing.

- Generate recurring revenue to grow the overall earnings power of the company.

- Return capital to shareholders via dividends and aggressive buybacks.

Morgan Stanley’s cost of capital relative to what they can earn by lending continues to decrease– E-trade has tens of billions in deposits, and despite the Fed hikes they’re still paying 0.01%. Morgan Stanley overall noted in their last conference call that they had $352 billion in deposits paying an average rate of 0.09%. Meanwhile, margin rates are increasing, dropping down straight to MS’s bottom line.

Generating recurring revenue is the second part of the game plan. While I don’t think asset management or wealth management have been a wire-to-wire success for Morgan Stanley (how many Morgan Stanley ETFs can you name?), they continue to push and make incremental improvements. Management is building the infrastructure they need for this. They bought Eaton Vance in 2021, and they subsequently sold the RIA business as well as E-trade’s RIA business that competed with the bank. Asset management is very attractive to management for the recurring revenue it provides and can help push MS’s multiple higher over time, perhaps to 15x or higher. One nugget that Morgan Stanley scored from the deal was Parametric, a direct indexing provider that offers services like tax-loss harvesting and custom indexing. Asset management revenues were up 14% as of April for Morgan Stanley, which is despite markets being lower. If they can keep this up, they’ll clean up when the current down-cycle is over. They acquired $75 billion in retirement assets in Q1 by buying Cook Street Consulting, and are looking at international acquisitions as well.

Returning capital is the last piece of the puzzle, and the Fed was the main obstacle that slowed down management’s capital return ambitions. But the latest stress test was great for Morgan Stanley, and the company was able to raise the dividend by 11% and announce a $20 billion buyback. Morgan Stanley’s market cap is only $134 billion as of my writing this, so this is a 2010s Apple-Esque buyback they’re intending to execute.

MS Stock Forecast

MS trades for 9.6x 2023 earnings estimates. Is it possible that these estimates are too high? I think it’s probable that they are. The market in general is seeing a much more unfavorable valuation and macro backdrop at the moment than was the case 5-10 years ago. But even if the true P/E is more like 11-12x next year’s earnings, that still implies an earnings yield of 8-9% for MS shareholders. If you believe, as I do, that the company can grow earnings by 4-5% annually over the next 10 years by a combination of organic growth, buybacks, and bolt-on acquisitions, then this implies a total return of 12-14% annually with upside from there if the market reprices Morgan Stanley the way it did for some other low multiple companies that have had business success.

The upside is not 25-30% annually like it has been for formerly underappreciated stocks like Microsoft (MSFT) and Apple over the last 10 years. But Morgan Stanley is a dirt-cheap value stock, has a legitimate plan for growth, and has a dividend yield over 4% with a payout ratio well under 50%. On the other hand, your downside is not so severe here compared with many other low P/E stocks, with book value for the company around $54 per share.

Morgan Stanley reports Q2 earnings before the market opens on Thursday, July 14th. Investors should pay attention to management guidance and the analyst Q&A, and look for new information on loan loss reserves, interest rates, and management’s insight into where the U.S. and global economies are headed.

Bottom Line

MS stock has been cheap for a while, and it has recently gotten even cheaper. You can buy the recently hiked 4% dividend yield and be paid to wait for the company’s business plan to take full effect, and look to nibble more if recession fears take the company lower. If you can find enough of these cheap companies with decent growth prospects and high yields to buy, you’re likely to succeed in the markets no matter the direction of the economy.

Be the first to comment