Getty Images

Thesis

Morgan Stanley (NYSE:MS) reported slightly better than expected Q4 results – and the stock has gained as much as 4% in pre-market trading. However, although results were solid, net income contracted by about 40% as compared to the same period one year prior. Needless to say, this is a very significant number. Moreover, investors should consider that Morgan Stanley remains negatively levered to higher interest rates, as compared to other bulge bracket banks such as JPMorgan Chase (JPM), or Citigroup (C), who reported business growth last Friday.

I slightly lower my target price for MS to $105.54/ share, as a consequence of continued weakness in investment banking and asset management. And accordingly, I continue to promote an underweight investment allocation to MS stock, as compared to C, JPM and BAC.

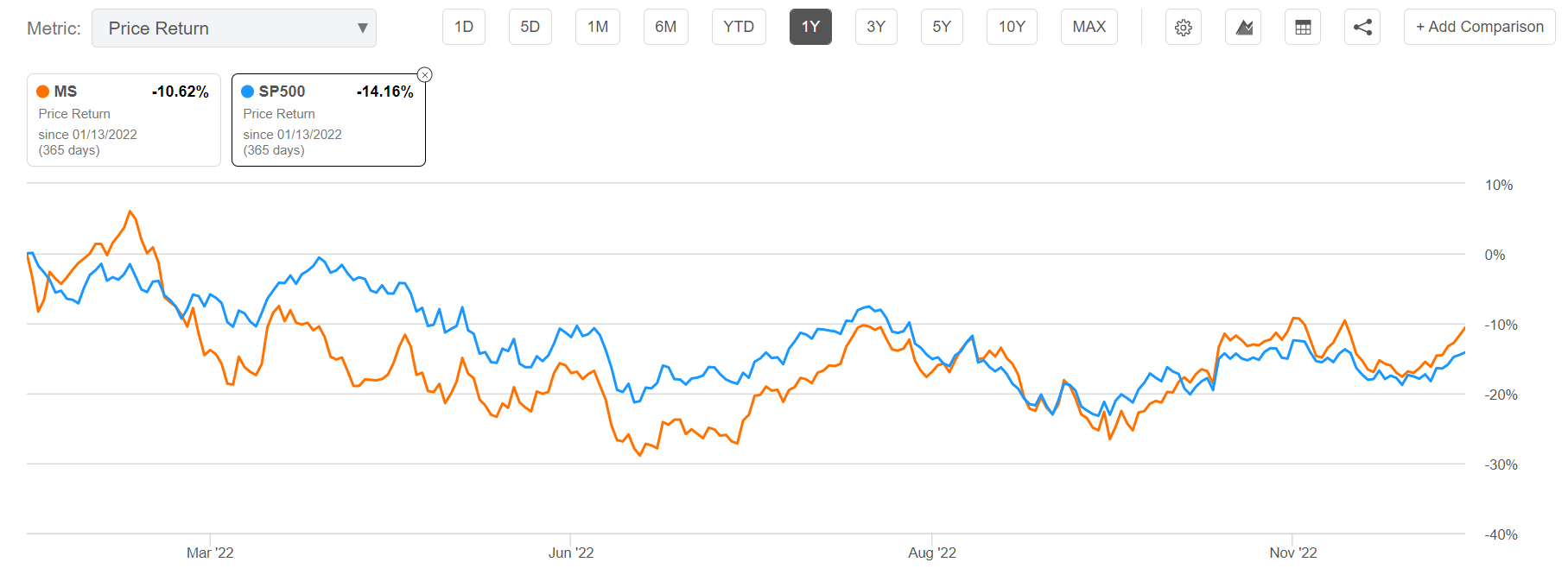

For reference, MS stock is down approximately 10% for the trailing twelve months, as compared to a loss of 14% for the S&P 500 (SP500).

Seeking Alpha

Morgan Stanley’s Q4 Results

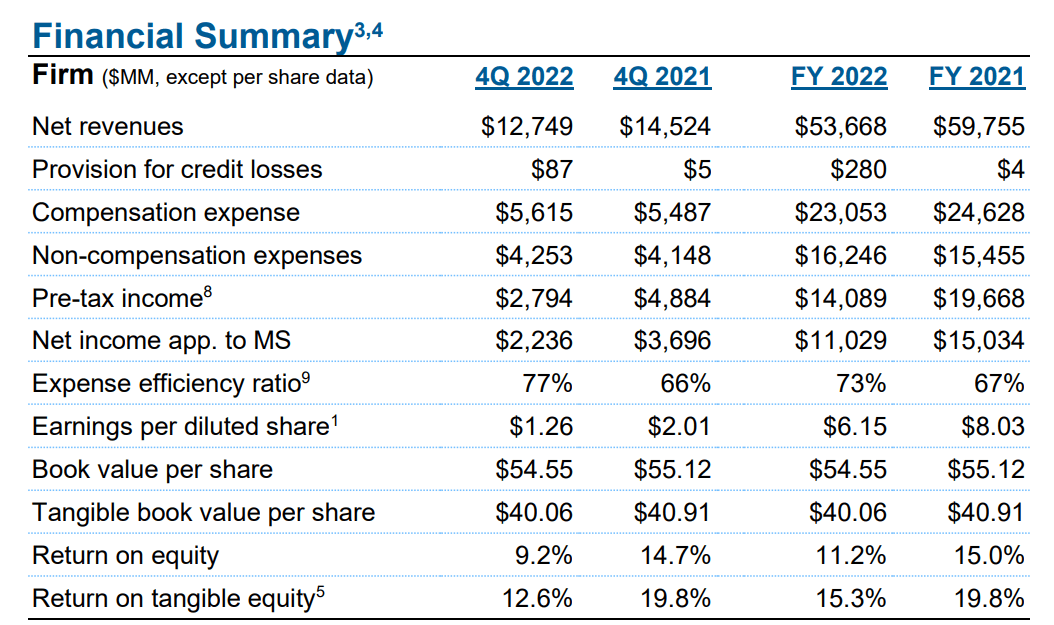

During the period from September to the end of December 2022, Morgan Stanley generated total revenues of $12.7 billion, which compares to $14.5 billion for the same period one year prior (12.5% year over year contraction). The firm’s net income came in at $2.2 billion ($1.26/share), versus $3.7 billion ($2.01) in Q4 2021. Notably, Morgan Stanley’s Q4 2022 net income slumped by more than 40% year-over-year.

For reference, analysts had expected revenues of about $12.4 billion and EPS of approximately $1.19/share (Source Bloomberg Terminal).

MS Q4 2022 Press Release

Why I Remain Underweight MS

I like Morgan Stanley management, and I believe it is an overall amazing investment bank that will continue to claim market share long term. However, the current environment is very unfavorable to MS. As compared to names such as JPMorgan, Citigroup and Bank of America (BAC), Morgan Stanley has very little positive exposure to higher interest rates. In fact, Morgan Stanley’s operations are most profitable if interest rates are very low and markets liquid. That is not the case currently; with the Fed continuing to hike rates, or at least keeping rates elevated, the global market for IPOs and other securities issuance is as good as frozen. And the M&A market has slumped in recent months. As a consequence, MS’s Q4 2022 revenues from investment banking came in at only $1.25 billion, reflecting a 49% contraction versus the same period one year prior. Like Goldman Sachs (GS), Morgan Stanley has tried to counter the slowdown in deal making through job cuts of about 2% of its staff in December — but it’s simply not enough to neutralize the loss of profitability.

A similar negative correlation for higher interest rates and Morgan Stanley’s profitability can be observed with regards to MS’ asset management business — with MS’ assets under management shrinking to $1.30 trillion, as compared to $1.57 trillion one year earlier, investment management revenues in Q4 fell to $1.5 billion (versus approximately $1.8 billion in Q4 2021).

Only Morgan Stanley’s wealth management business expanded as compared to Q4 2021: MS’ revenues from wealth management increased to $6.6 billion, up from $6.3 billion one year prior. The business expansion was mostly driven by an increase in the loan portfolio, growing from $129.2 billion in Q4 2021 to $146.1 billion in Q4 2022.

Valuation Update: Lower TP To $105.54/share

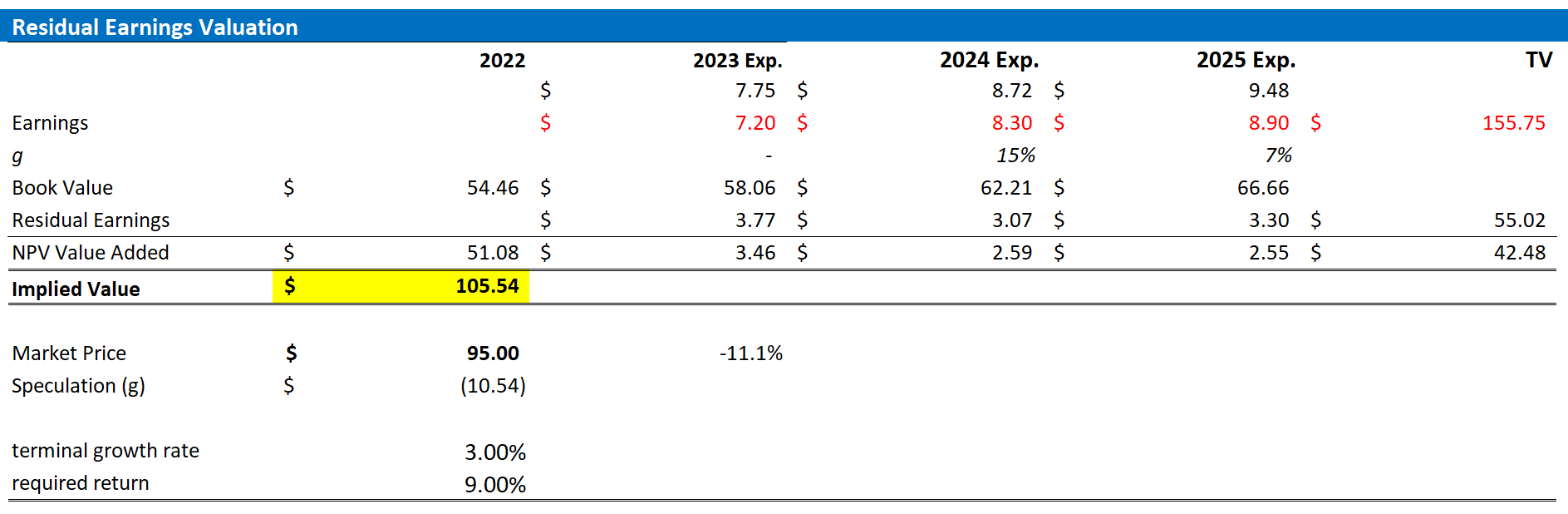

On the backdrop of a continued weakness in some of Morgan Stanley’s largest exposure verticals — investment banking and asset management — I lower my EPS expectations for MS in 2023. I estimate that Morgan Stanley’s EPS in 2023 will likely fall to somewhere between $6.9 and $7.5 Moreover, I also lower my EPS expectations for 2024 and 2025, to $8.3 and $8.9, respectively.

I continue to anchor on a 3% terminal growth rate (one percentage point higher than estimated nominal global GDP growth) and a 9% cost of equity requirement.

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price for MS of $105.54 as compared to $146.69 prior.

Author’s Assumptions & Calculations

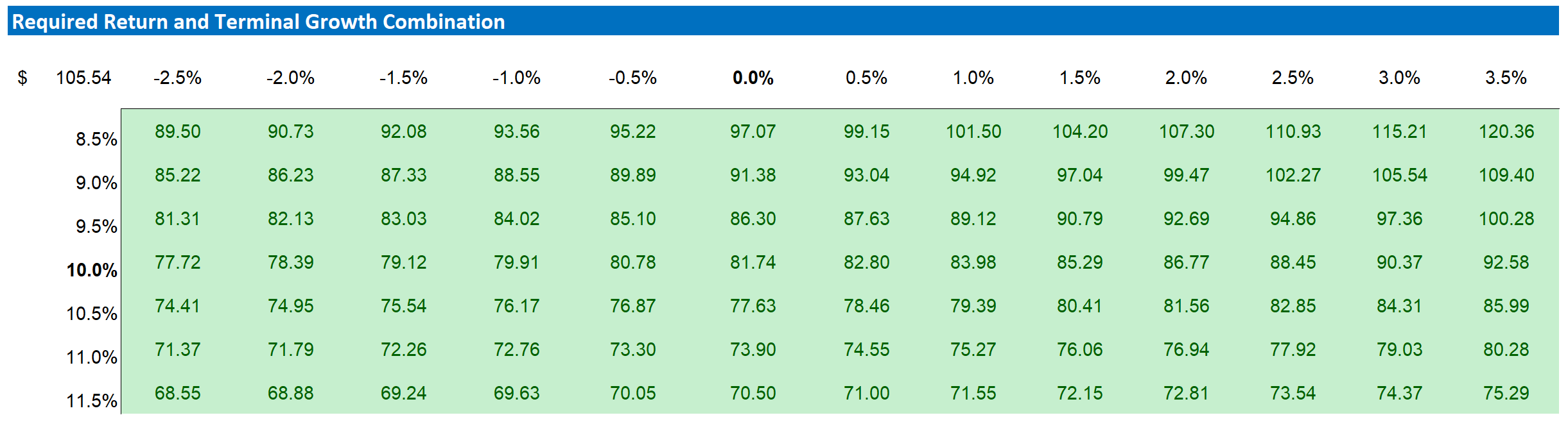

Below is also the updated sensitivity table.

Author’s Assumptions & Calculations

Conclusion

Morgan Stanley stock is currently valued at a one-year forward P/E of about 14.5x. This is not a bad risk/ reward multiple for such a high-quality bank. Investors should consider, however, that other banks, which are also much better positioned in context of rising rates due to a significantly larger loan portfolio, are trading much cheaper still.

On the backdrop of continued weakness in the demand for investment banking and asset management services, I lower my target price for Morgan Stanley to $105.54/ share. I continue to promote an underweight investment allocation to MS stock, as compared to C, JPM and BAC.

Be the first to comment