Alex Wong

Introduction

When investors think of successful long-term investing, many think of Warren Buffett. After all, nobody has made more money investing in long-term investments than the Oracle of Omaha. When people think of Buffet, they may think of his stakes in Apple (AAPL), Coca-Cola (KO), and his massive investment company Berkshire Hathaway (BRK.A). One of the stocks people often overlook is the financial services giant Moody’s Corporation (NYSE:MCO). Due to its (dividend) growth characteristics and huge moat, this rating agency is one of Buffett’s core holdings and a tremendous source of wealth. This article will discuss all of this and dive into the pros and cons of owning this New York-based financial giant.

So, let’s get to it!

About Moody’s

A high-moat financial service giant

Buffett’s Berkshire owns close to 25 million shares of Moody’s. This makes him the company’s largest shareholder, as he owns 13.5% of all shares. In his portfolio, the company has a 2.0% weighting.

He did not buy these stocks recently, as the more experienced investors among us will know. Buffett has been a shareholder right from the start when the company spun off from Dun & Bradstreet (DNB) in 2000.

Since then, the company has grown into one of the two most powerful rating agencies in the world with its peer S&P Global (SPGI). MCO has a $59.4 billion market cap.

The company has two operating segments. Investor services is an independent provider of credit rating opinions and everything that comes with it. It’s what Moody’s is known for. Moody’s Analytics is a provider of intelligence and analytical tools which support management decisions and a wide range of objectives that rely on advanced data.

Moody’s

One of the benefits the company has is its moat. Being one of the two largest rating agencies in the world (top three if we include Fitch) comes with advantages as corporations trust companies with a good reputation.

When I dealt with ratings on a corporate level, people just relied on the data provided by the big firms – no questions asked. Becoming a new entrant in this industry is extremely hard, and I doubt a lot of companies are willing to spend the capital needed to get a shot at turning the top three into the top four.

It also helps the company’s moat that its services have become essential in global capital markets. A good credit rating is needed to get access to capital. It is not only a sign that the company is healthy, but it also shows transparency.

Moody’s

While we can debate whether ratings agencies are great at the timing of downgrades when companies go from investment grade to non-investment grade, there’s no denying that these credit ratings are greasing the wheels of global financial flows.

In 2010, the company came under fire due to its role in the Great Financial Crisis, which put tremendous pressure on Buffett to comment on the situation back then. According to the New York Times:

Moody’s rated Lehman Brothers’ debt A2, putting it squarely in the investment-grade range, days before the company filed for bankruptcy. And Moody’s gave the senior unsecured debt of the American International Group, the insurance behemoth, an Aa3 rating which is even stronger than A2 the week before the government had to step in and take over the company in September as part of what has become a $170 billion bailout.

[…] Mr. Buffett also seems to have said nothing about a problem that some contend is just as serious and endemic: because ratings are required in so many transactions, the agencies’ inaccurate ratings have no effect on their own bottom lines.

The good thing for MCO is that the recession wasn’t able to do lasting damage to the company. If anything, I believe it changed the way people trust ratings. Ratings are now part of the bigger picture instead of something people trust blindly.

That said, in 2021, the company had rated more than 35,000 organizations. Total debt outstanding with a rating from MCO exceeded $70 trillion back then.

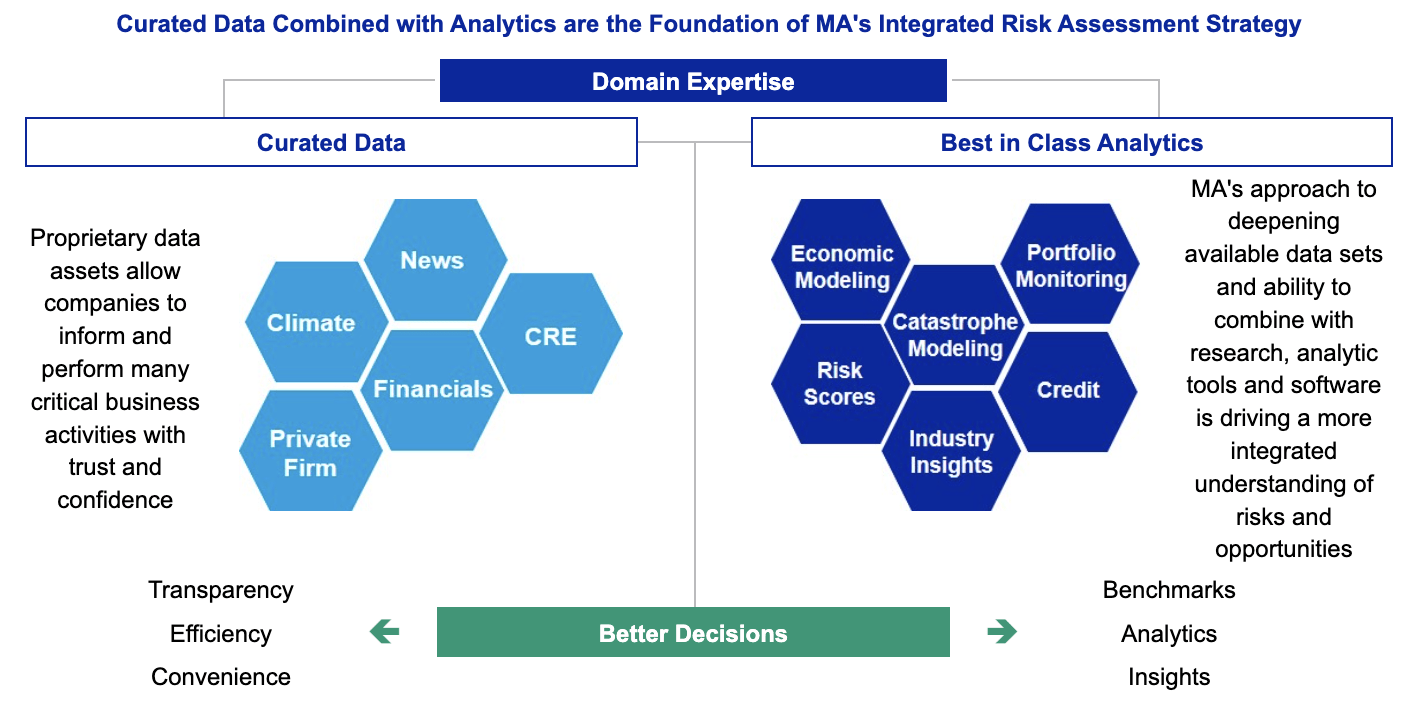

Its analytics segment adds value to the above-mentioned operations. These services combine research, analytic tools, and software to create an integrated system that improves decision-making. This includes economic modeling, portfolio monitoring, and catastrophe modeling using climate data.

Moody’s

Moreover, because MCO is so large, its numbers and comments tell us a lot about the state of the economy. That’s one major reason why investors often assess the company’s financials and comments, even if they do not plan to invest in the company.

Moody’s Fast-Growing Business

Fast growth with temporary macroeconomic headwinds

Moody’s is a financial company, which means it operates in a sector with a lot of banks and financial institutions that are mature and often come with slow growth rates.

Moody’s is different as its services allow for fast growth. For example, it benefits from a rapidly growing global financial industry, which requires rating services. It also benefits from an ever-increasing need for financial services based on the data it generates.

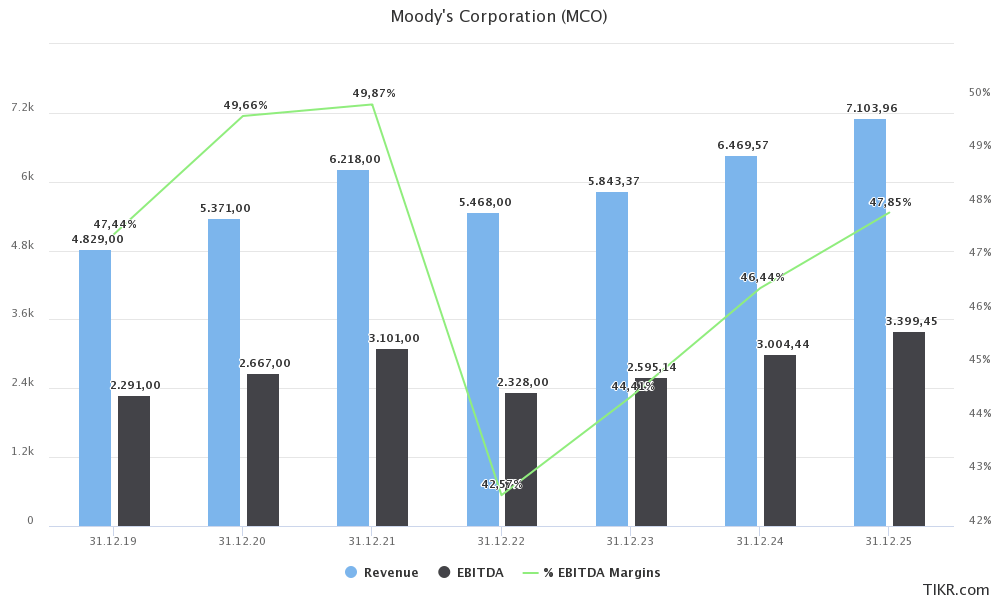

The following numbers show the compounded annual growth rates between 2013 and 2025E.

- Revenue: 7.5%

- EBITDA: 8.1% (outperforming growth as a result of higher margins)

- Normalized net income: 9.1%

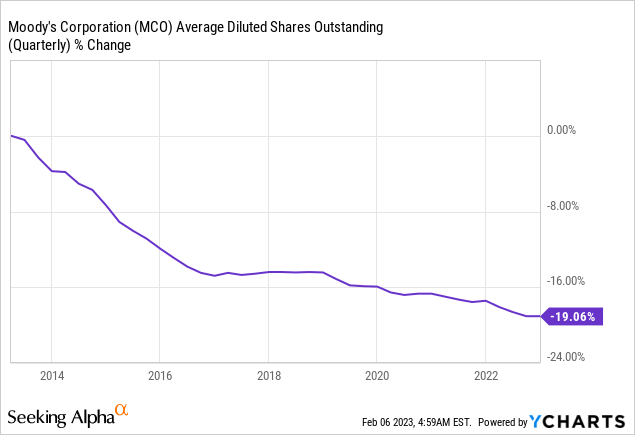

- Normalized EPS: +11.2% (the benefit of buybacks added 210 basis points per year)

- Free cash flow: 9.0%

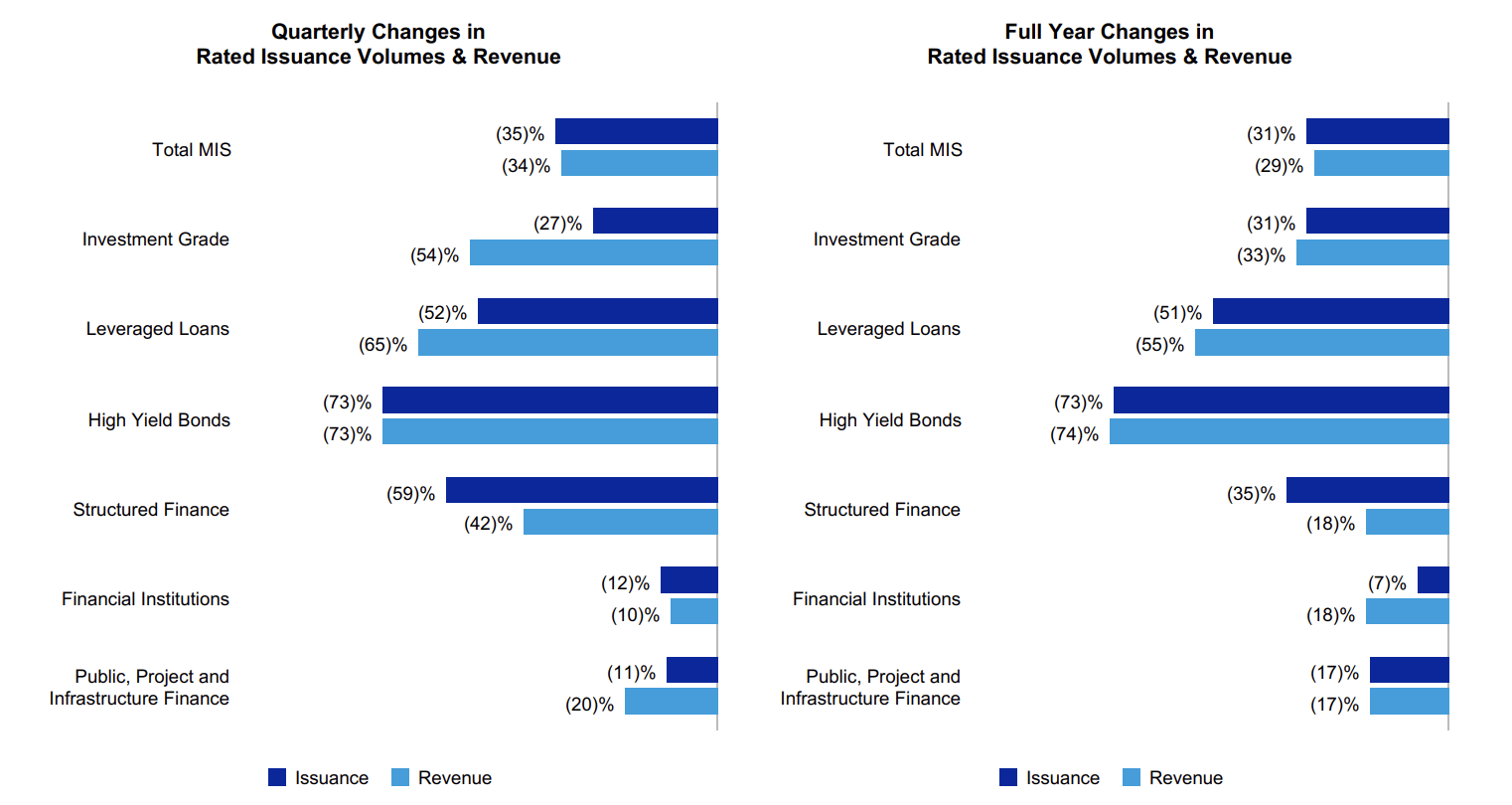

With that said, 2022 wasn’t a great year. Revenue declined by 12.1%. Adjusted EBITDA declined by 24.9% as a result of lower margins on top of lower revenues. Operating expenses rose by roughly $130 million, which is an issue a lot of service-oriented (and non-service) companies struggle with. During times of low inflation, tech/service companies are often able to generate higher operating margins. That becomes trickier in a high-inflation environment. Even worse, after two strong years, global demand for ratings is down.

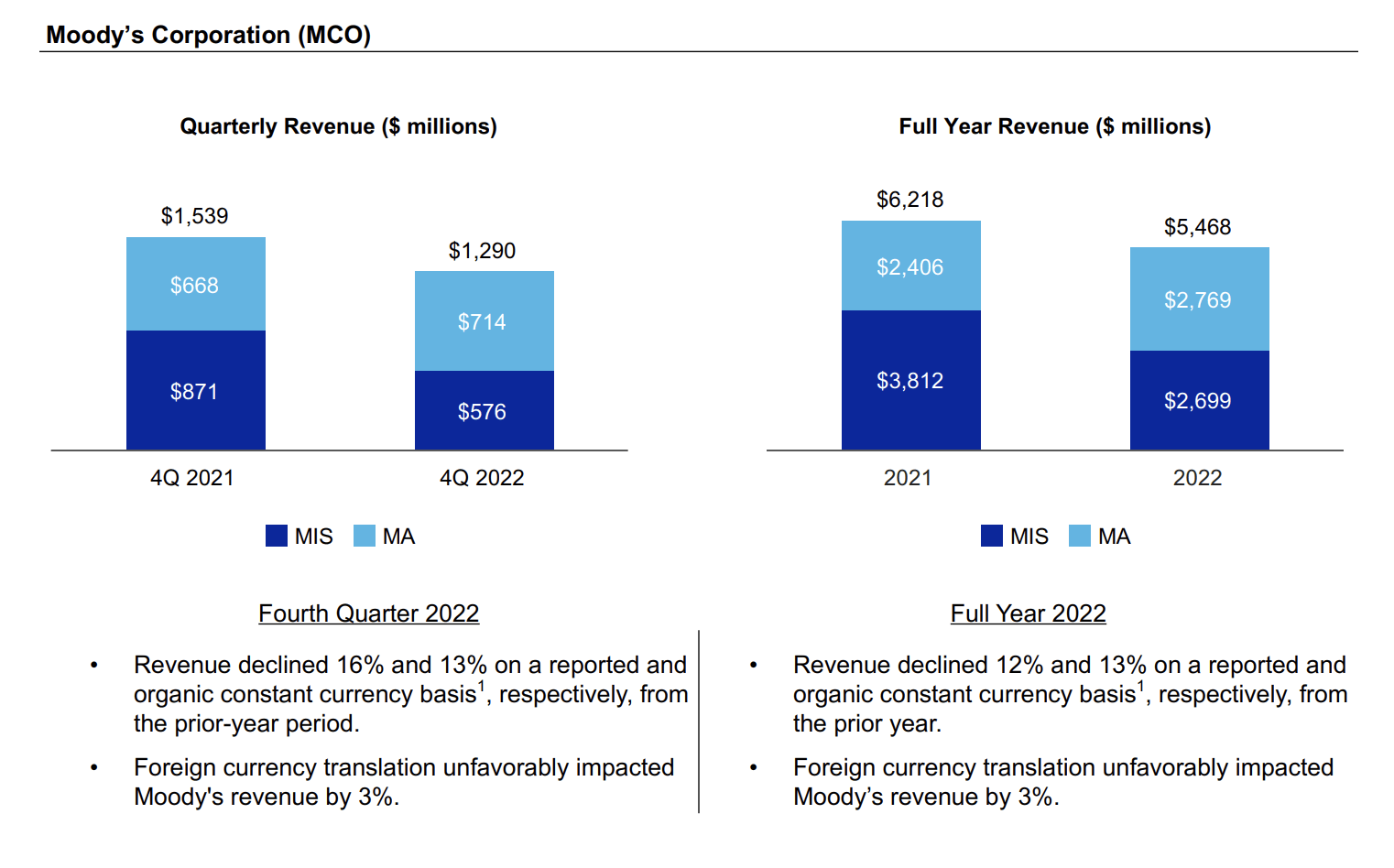

Last week, the company reported its 4Q22 earnings, which showed a revenue decline of 16.2% to $1.29 billion.

Moody’s

In investor services, transaction revenue dropped from 66% to 48%, as lower demand hurt non-recurring revenue streams the most.

When it comes to credit ratings, the company saw declines across the board. According to the company:

In contrast to the conducive issuance environment in 2021, inflationary concerns and geopolitical tensions significantly dampened issuance throughout 2022, particularly for leveraged finance.

Moreover, this did not change in 4Q22.

Credit market activity remained muted across all sectors due to ongoing market uncertainty, central bank actions, high levels of corporate cash, as well as persistent inflationary and recessionary concerns.

Leveraged loan, high yield bond, and structured finance issuance declined sharply from a strong prior-year comparable; revenue was also impacted by an unfavorable issuer mix, given the decrease in opportunistic activity

Moody’s

In 2023, the company expects to grow revenue in the mid-to-high single-digit percent range. The adjusted operating margin is expected to be n the 44% to 45% range. That number was 36.6% in 2022 and 46% in 2021.

Essentially, the bull case is a normalization in demand backed by improving growth rates. Revenue growth is expected to rise to 6.9% in 2023, followed by a surge of 10.7% in 2024 and 9.8% in 2025. Higher margins are expected to push EBITDA growth to at least 12% per year.

TIKR.com

So, what about the dividend? After all, it’s a dividend-focused article.

The Moody’s Dividend

The dividend as part of a total-return strategy

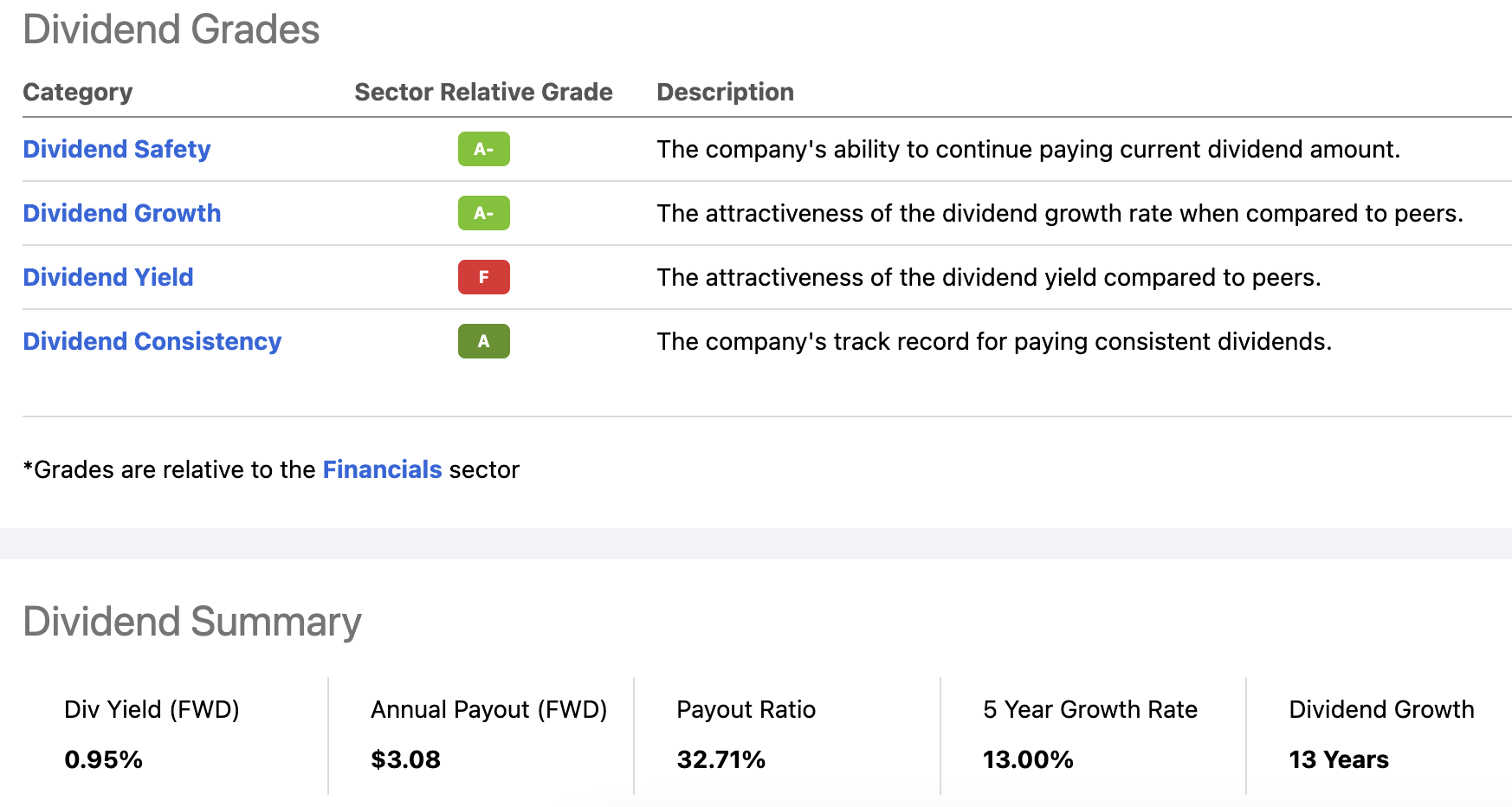

One big fat F and three As. That’s Moody’s dividend scorecard.

The company scores high on safety, growth, and consistency, as it has 13 consecutive years of dividend growth, a payout ratio of 33%, and a five-year annual average dividend growth rate of 13.0%. These numbers are great.

Seeking Alpha

2024E free cash flow is expected to be $2.1 billion, which implies a 27% cash payout ratio.

The problem is that the yield is low. It’s even lower than the number shown above, as the recent stock price rally has pushed the yield to 0.86%, which is based on a $0.70 per share per quarter dividend.

While dividend growth is high and very consistent, MCO will not offer new investors a high yield on cost anytime soon.

Let’s say the company can maintain a 13% annual dividend growth rate for ten years. It would turn a 0.9% yield into a 3.0% yield on cost in 2033.

Hence, the power of MCO is its total return. The company has a few key characteristics that allow it to generate outperforming total returns:

- The company is able to pay a dividend.

- This dividend is consistently raised, as MCO has a proven business model.

- Its growth rates beat inflation.

- The company is standing the test of time.

These characteristics are what allow dividend growth stocks to beat the market over time.

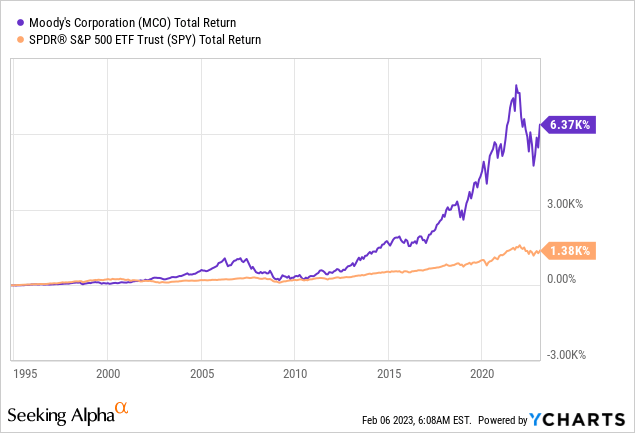

Going back to 1995, MCO has returned close to 6,400%. The market has returned roughly 1,400%, which isn’t bad either.

Moreover, these returns are consistent. These are the total returns of Moody’s and the market using different intervals.

- 3Y CAGR: MCO 8.8%, Market 9.7% (underperformance due to post-pandemic growth slump).

- 5Y CAGR: MCO 15.9%, Market: 9.4%

- 10Y CAGR: MCO 20.8%, Market 12.5%.

That said, I see one problem. As strong as MCO’s business model is, it is prone to steep declines in demand during recessions. While recurring revenue streams are increasingly dominant, the company cannot avoid much lower debt issuance volumes during recessions.

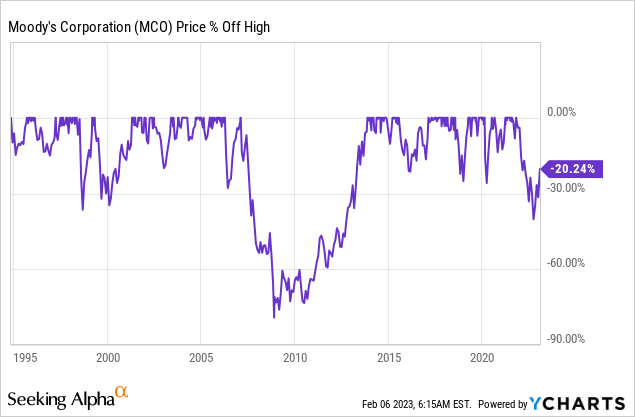

During the Great Financial Crisis, MCO lost close to 80% of its market cap. Excluding dividends, the stock price fully recovered from the recession in November 2013.

Since then, we haven’t dealt with a recession of that magnitude. However, the stock is still prone to “regular” 20% declines when investors bet on weakening demand and supply for debt.

This brings me to the valuation.

Valuation

MCO is one of the companies that never seems to be “cheap”, which is often the case when a company has a strong business benefiting from high secular growth providing high growth rates.

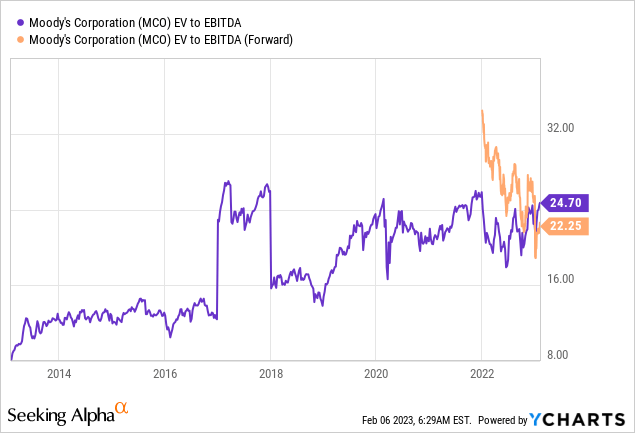

The company is trading at 22x 2023E EBITDA, which is still a lofty valuation and a result of subdued post-pandemic growth.

Using 2024E numbers, we’re dealing with a 21x EBITDA valuation, which is a bit better, yet still not an attractive valuation.

The problem for investors on the sideline is that MCO shares are up 16% year-to-date. Stocks have surged in anticipation of a more dovish Fed.

TIKR.com

As I explained in a recent gold-focused article, I believe that this move is too dovish. I expect the market to provide us with new buying opportunities in the months ahead.

Hence, I would welcome it if MCO shares were to drop toward $260 again. At that point, I believe the risk/reward warrants an investment in the company.

Takeaway

There are pros and cons when it comes to investing in MCO.

The pros are that MCO has a huge moat, strong secular growth, high free cash flow, increasing recurring revenue, and a history of consistent and high dividend growth.

The cons are a high dependency on a healthy global debt market and a low dividend yield.

While I expect MCO to generate outperforming total returns, the stock is not suited for income-dependent investors.

However, dividend growth investors looking for high-quality financial exposure may enjoy adding MCO to their portfolios. Given the valuation and my macroeconomic outlook, I prefer waiting for a correction to at least $260 per share.

(Dis)agree? Let me know in the comments!

Be the first to comment