Anna Koberska/iStock via Getty Images

Considering Russia and Ukraine are significant exporters of grain, Putin’s horrific war of choice in Ukraine has arguably broken a critical link in the global food supply chain. Since there appears to be no end in sight for the war, and since the reverberations will likely be felt long after there is an end to it, investors might want to consider allocating some capital to the frequently overlooked and taken-for-granted agribusiness sector. Today, I will take a look at the VanEck Vectors Agribusiness ETF (NYSEARCA:MOO) to see if it might be a good way for the well-diversified investor to benefit from what is otherwise a very sad, disturbing, and dangerous development on the global geopolitical front.

Investment Thesis

The WSJ recently reported that Russia and Ukraine combine to produce one-third of the planet’s wheat, 25% of the world’s barley, and ~75% of its sunflower oil. That being the case, the global food supply chain has arguably been severely damaged at best and broken at worst.

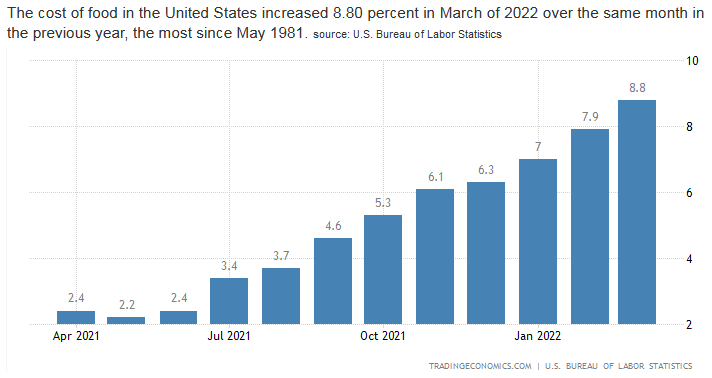

As the graphic below depicts, food inflation was already ramping up following the onset of the global pandemic and even prior to Putin’s invasion of Ukraine. Putin’s war simply kicked that trend into overdrive – driving up the cost of food in the US by 8.8% in March:

Trading Economics

However, note that the US is much (much) better positioned than many other countries due to its large and thriving agricultural sector.

In addition, knowing that natural gas is a critical feedstock for the production of nitrogen fertilizer, pesticides, and plastics for the global agriculture sector, and that the price of natural gas – specifically in Europe – has skyrocketed of late, investors should seriously consider allocating some capital to the agribusiness sector.

So, let’s take a closer look at the MOO ETF and see how it has positioned shareholders to benefit from these trends.

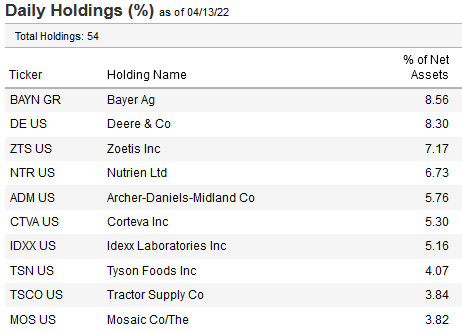

Top-10 Holdings

The top-10 holdings in the VanEck Agribusiness ETF are shown below and equate to what I consider to be a relatively concentrated 58.7% of the entire 54 company portfolio:

VanEck

The #1 holding with an 8.6% weight is the German conglomerate Bayer (OTCPK:BAYZF). Bayer is a global provider of life sciences and agricultural solutions which are primarily operated out of its Crop Sciences segment. In March, Bayer announced it was selling its pest control business to Cinven for $2.6 billion.

Bayer acquired agribusiness giant Monsanto in 2018 for $63 billion, and recently agreed to pay $80 million to settle allegations of environmental damage allegedly caused by PCBs manufactured by Monsanto. Bayer is up 35.6% YTD and currently yields 3.3%.

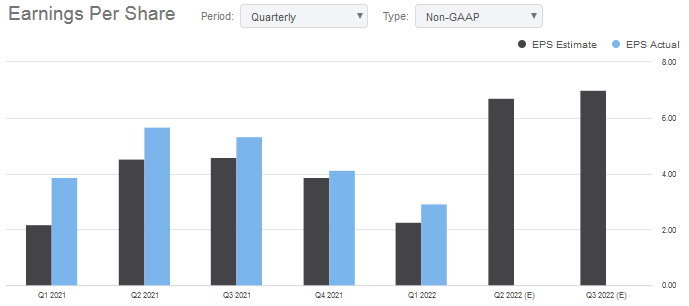

Deere (DE) is the #2 holding with an 8.3% allocation. Deere is a global provider of farm equipment and operates two segments directly targeting the agribusiness sector: Production and Precision Agriculture & Small Agriculture. Deere is expected to report significantly higher earnings in the coming quarters:

Seeking Alpha

The #5 holding with a 5.8% weighting is Archer-Daniels-Midland (ADM). ADM is a US-based agricultural giant ($53.7 billion market cap) that procures, transports, stores, processes, and merchandises food-based commodities, products, and ingredients for the global market. The stock is up 65% over the past year but trades with a forward P/E of only 18x.

Tyson Foods (TSN) is the #8 holding and is a global food company that operates through four segments: Beef, Pork, Chicken, and Prepared Foods. Tyson owns well-established brands such as Tyson (chicken), Jimmy Dean (pork sausage), Hillshire Farm, Ball Park, Wright, State Fair, Aidells, and Gallo Salame. The stock is up 8.7% YTD, trades with a forward P/E of only 11.3x, and currently yields 1.9%.

The top-10 list of holdings is rounded out by Mosaic (MOS) with a 3.8% weight. MOS operates through three segments: Phosphates, Potash, and Mosaic Fertilizantes that produces and markets phosphate and potash crop nutrients for the global agriculture sector. MOS has more than doubled over the past year yet trades with a forward P/E multiple of only 6.7x.

Risks

The MOO ETF is certainly not immune to all the typical investment risks as dictated by the macro environment investors are struggling to navigate. These include covid-19-related supply chain issues and factory closures, high inflation, rising interest rates, and the massive geopolitical risks associated with Putin’s invasion of Ukraine and the resulting sanctions placed on Russia by America and its Democratically free country NATO members. Any and all of these risks could reduce global economic growth and potentially a severe recession (or worse).

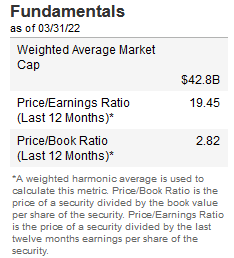

As can be seen by the examples cited above, many of these stocks have already had strong run-ups. However, also note that many are still trading at relatively low valuation levels in comparison to the market. Indeed, the overall portfolio still appears to be relatively undervalued in my opinion – sporting P/E and price-to-book ratios that are arguably below that of the broad market as measured by the S&P500 (P/E = 22.2x):

VanEck

There is always the potential for a settlement in Ukraine that would likely cause a swift pullback in many of the stocks in this portfolio. That said, it is my belief that the global food chain has been significantly battered enough for the reverberations to last at least a full growing season (i.e. a year) or longer (probably at least two years). That being the case, I think these companies will be reporting outsized earnings for many quarters to come.

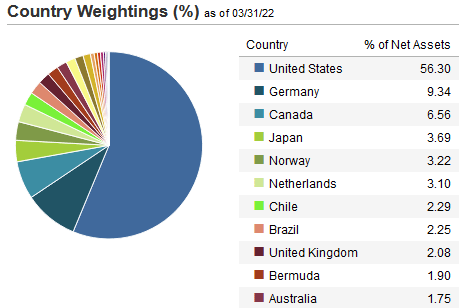

Regionally, the portfolio is very well positioned: it has only a 1.5% exposure to China, and 0.0% to Russia:

VanEck

More than 50% of the portfolio is dedicated to the materials and consumer staples categories, both of which have historically been able to pass through higher costs onto the consumers of their goods during times of high inflation.

Summary & Conclusions

I like this portfolio and I like the top-10 positions, their relative weightings, and the manner in which the portfolio has allocated capital on a global basis (0.0% to Russia, and a very small and insignificant position in China-based companies).

The 30-day yield is only 0.82%, so the investment opportunity here is clearly capital appreciation. Meantime, the expense ratio is 0.55% – which is relatively high for an ETF. However, it is not outrageous given the fact that the fund holds many foreign stocks, and for the diversity, those holdings give US investors (both regionally and on a currency basis).

I like this ETF and am thinking about opening a position that, combined with my iShares MSCI Global Metals & Mining Producers ETF (PICK), should give my portfolio some additional protection against inflation over the coming year – and perhaps much longer.

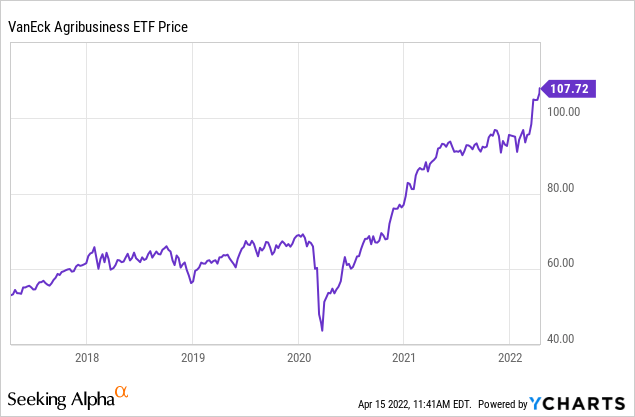

I’ll end with a five-year price chart of MOO and note the leg higher since Putin invaded Ukraine:

Be the first to comment