Khanchit Khirisutchalual/iStock via Getty Images

A Quick Take On Montrose Environmental Group

Montrose Environmental Group (NYSE:MEG) went public in September 2021, raising $155 million in gross proceeds in a U.S. IPO.

The firm provides a range of environmental services for commercial and government customers.

Given the tailwinds the company sees from environmental regulatory actions in the U.S., MEG is positioned for further growth ahead.

I’m Bullish on MEG at around $48.00 per share.

Montrose Environmental Group Overview

Irvine, California-based Montrose was founded to provide environmental services through three business segments:

-

Assessment, Permitting, and Response

-

Measurement and Analysis

-

Remediation and Reuse

Management is headed by president and Chief Executive Officer Mr. Vijay Manthripragada, who has been with the firm since September 2015 and was previously CEO of PetCareRx and prior to that was a Senior Vice President at Goldman Sachs.

The firm targets customers in the following markets:

-

Power Generation

-

Chemical Manufacturing

-

Manufacturing

-

Oil & Gas

-

Natural Gas

-

Real Estate Development

-

Ethanol Production

Management has said it has ‘long-standing relationships with a number of Fortune 1000 companies and government entities,’ and many of its services were deemed ‘essential’ during the COVID-19 shelter-in-place guidelines.

Notably, the firm has acquired over 50 businesses in the last eight years, as management views the industry as still highly fragmented and it intends to continue ‘selectively acquiring companies’ in the industry.

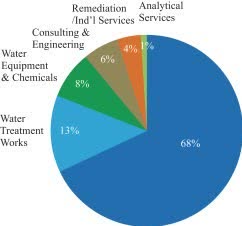

According to a 2019 market research report by Environmental Business International, the global market for environmental services is estimated to have a value of $1.25 trillion. The firm’s addressable market is believed to be approximately $395 billion and is expected to grow at a rate of 3.4% per year from 2018 to 2024.

A high growth rate is expected to occur in the Remediation and Industrial Services and Consulting & Engineering Services sub-markets, and a lower growth rate in the Wastewater Treatment Services and Analytical Services markets, as shown in the chart below:

Global Environmental Services (Environmental Business International)

Also, with the advent of the recent COVID-19 pandemic, there will be an increased focus on air quality and management expects ‘the WHO’s guidelines coupled with increasing pollution to catalyze local air quality regulations and therefore, demand for environmental services, particularly air quality services.’

Management has said its primary competitors are divisions of large companies and that few of its competitors provide the full range of solutions that it offers.

Montrose Environmental Group’s Recent Financial Performance

-

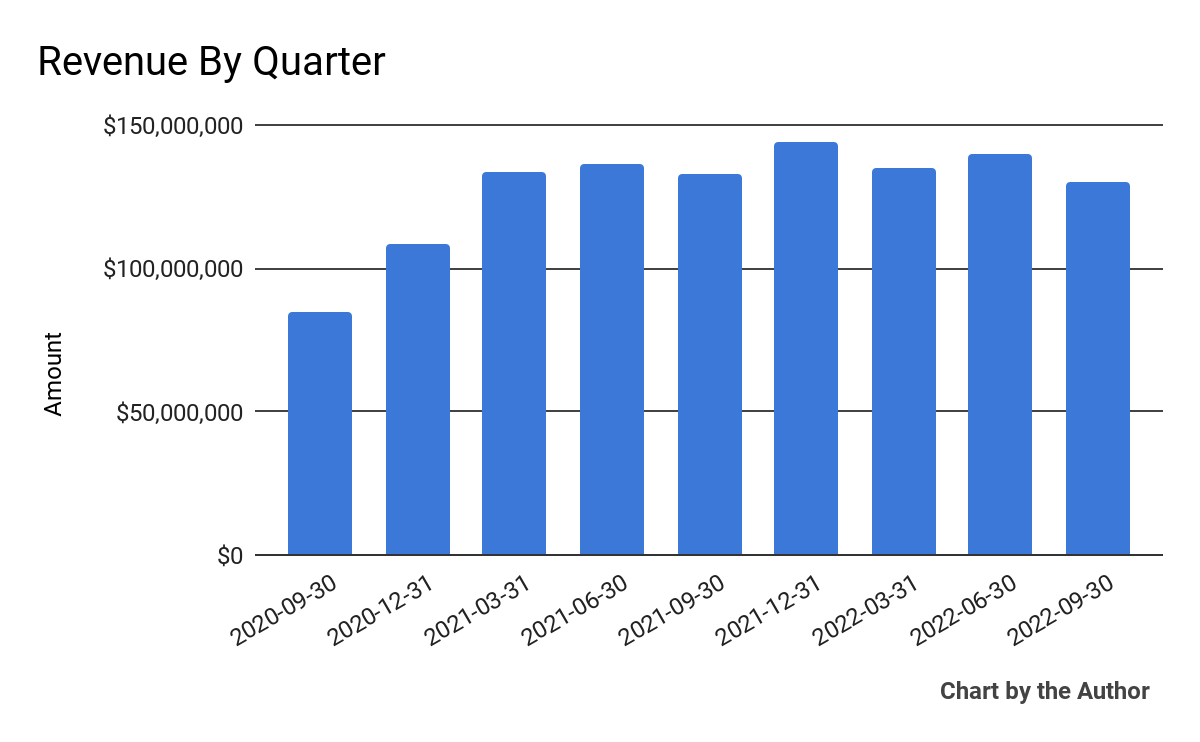

Total revenue by quarter has plateaued in recent quarters:

9 Quarter Total Revenue (Financial Modeling Prep)

-

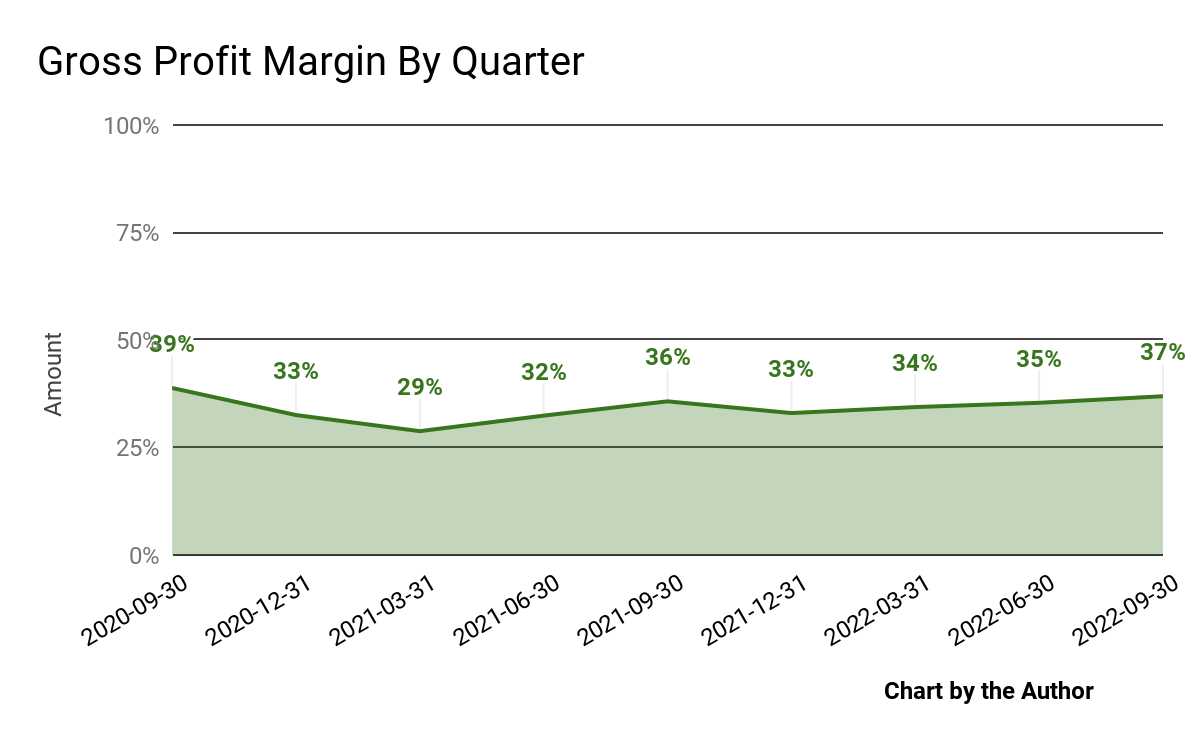

Gross profit margin by quarter has trended higher more recently:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

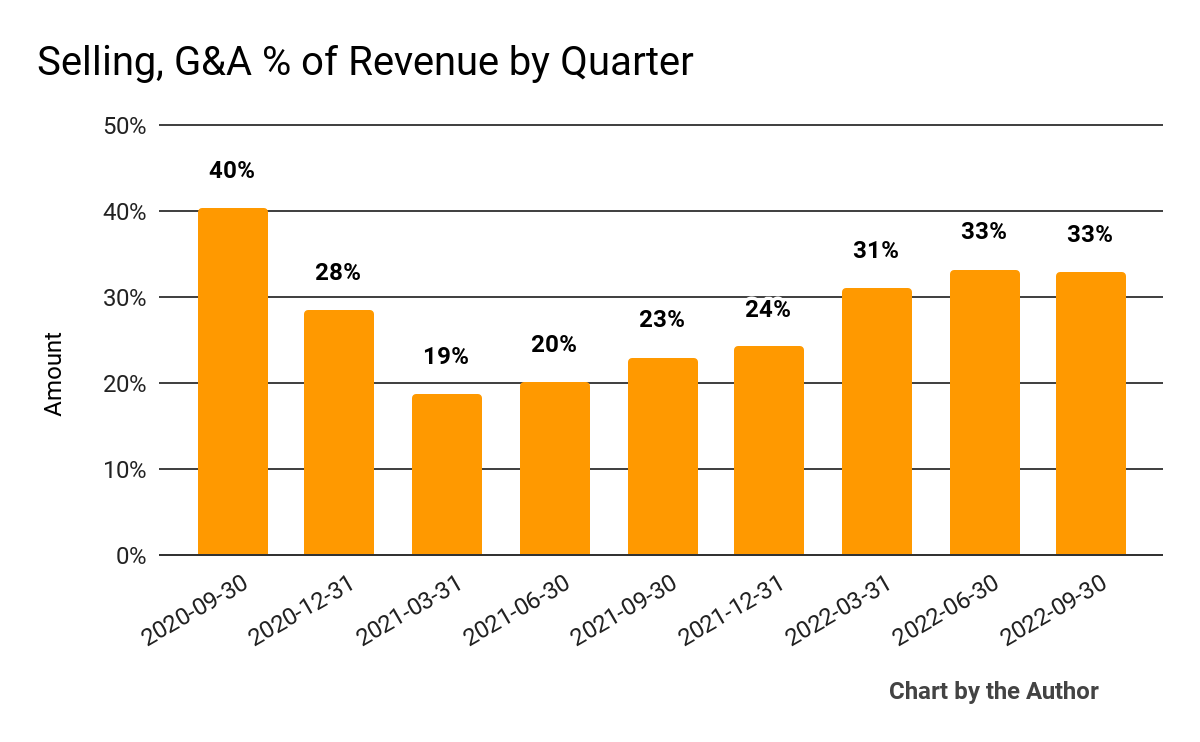

Selling, G&A expenses as a percentage of total revenue by quarter have grown in recent quarters, as the chart shows below:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

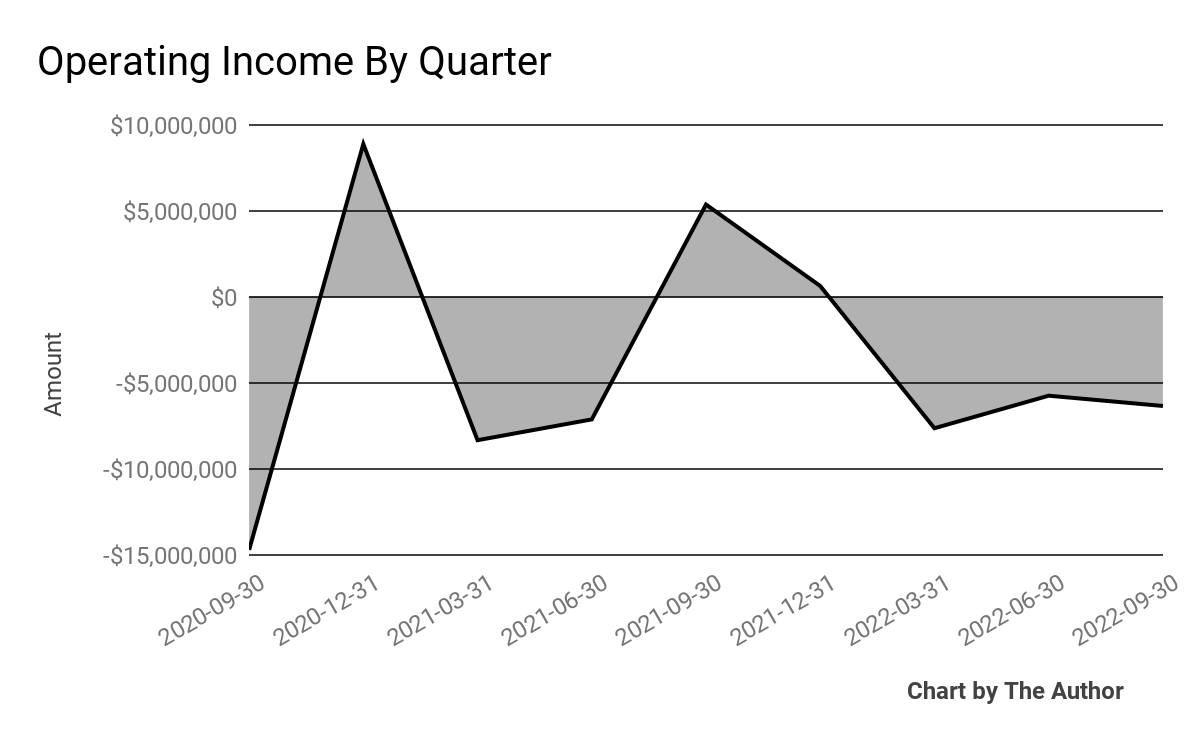

Operating income by quarter has varied between positive and negative results:

9 Quarter Operating Income (Financial Modeling Prep)

-

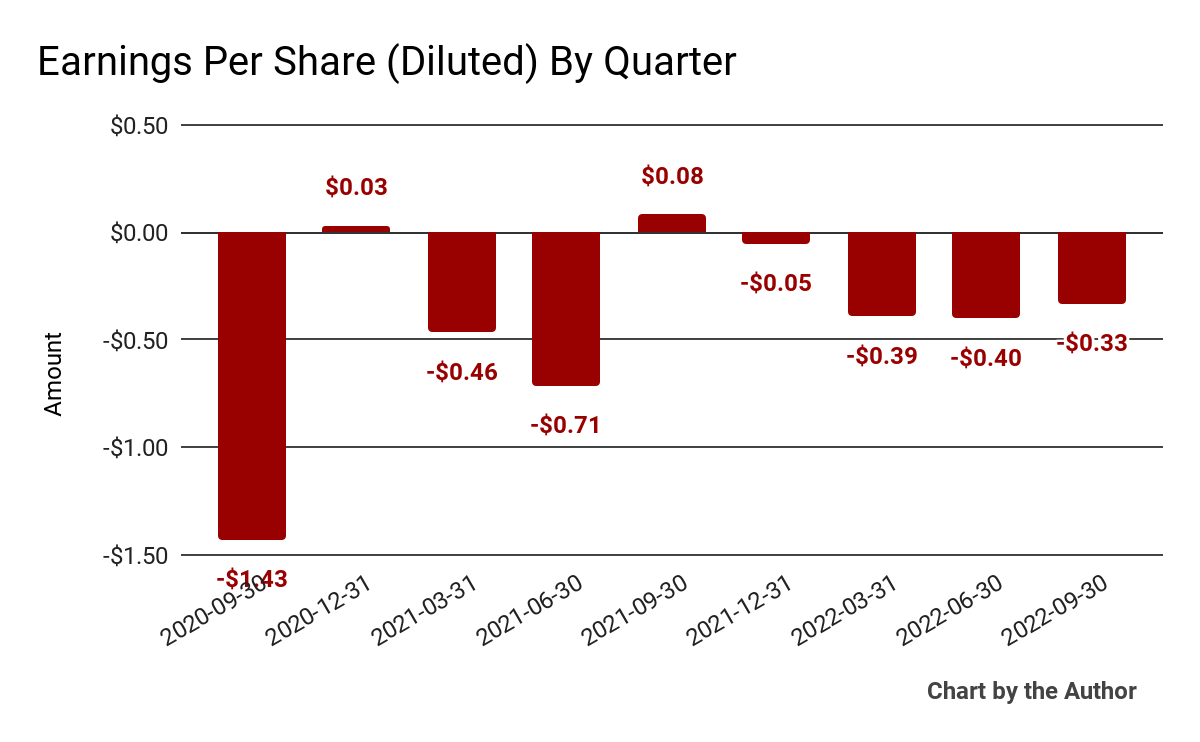

Earnings per share (Diluted) have remained negative in each of the last four quarters:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

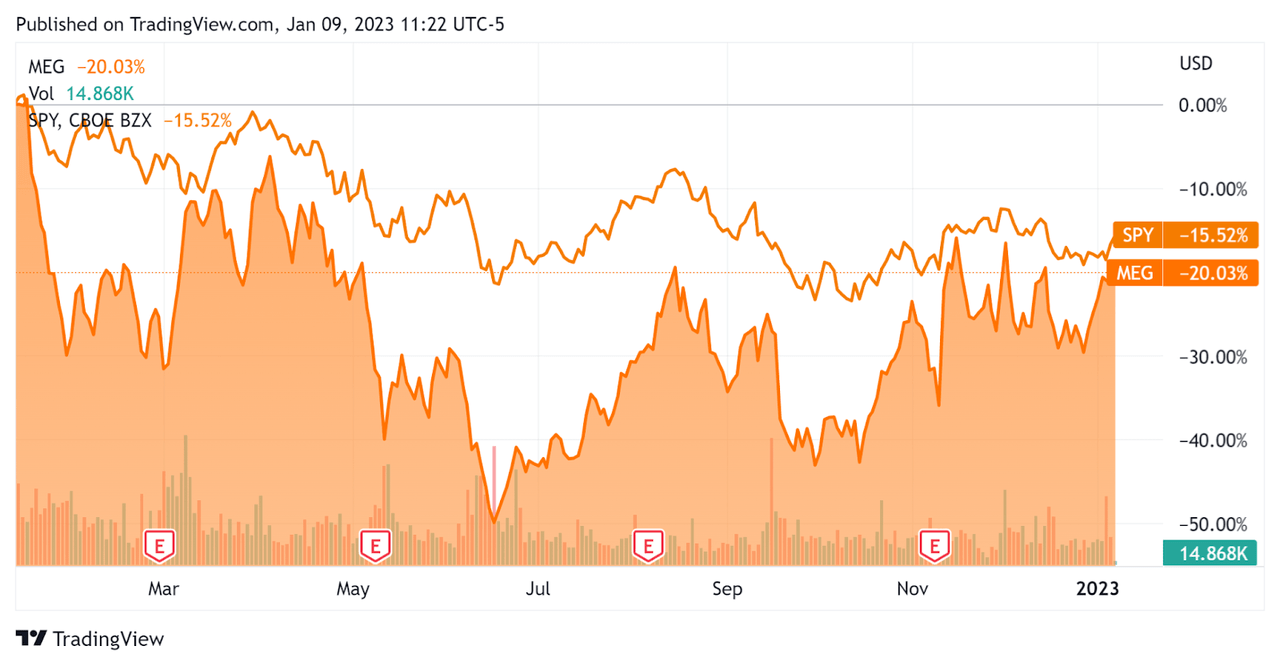

In the past 12 months, MEG’s stock price has fallen 20% vs. the U.S. S&P 500 index’s drop of around 15.5%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Montrose Environmental Group

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

2.7 |

|

Enterprise Value / EBITDA |

35.8 |

|

Revenue Growth Rate |

7.3% |

|

Net Income Margin |

-4.1% |

|

GAAP EBITDA % |

7.6% |

|

Market Capitalization |

$1,382,480,768 |

|

Enterprise Value |

$1,491,647,230 |

|

Operating Cash Flow |

$32,038,000 |

|

Earnings Per Share (Fully Diluted) |

-$1.17 |

(Source – Financial Modeling Prep)

Commentary On Montrose Environmental Group

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the growing demand for its PFAS water treatment, greenhouse gas measurement, & mitigation and renewable energy offerings.

Leadership also noted that it continues to seek a consolidated M&A strategy, albeit at a slower pace in 2022, with immediate accretion a typical feature of deals.

The company believes that U.S. regulatory actions will provide a ‘momentum for environmental protection’ that acts as a tailwind for the firm’s service offerings.

As to its financial results, revenue fell 1.7% year-over-year due in part to a sharp drop in the firm’s CTEH COVID-19 cleaning & disinfection segment.

Gross profit margin rose slightly year-over-year, while consolidated adjusted EBITDA fell from 15.3% of revenue to 13.1% of revenue due to a change in business mix, a cyber-attack, and greater investments in its operating infrastructure.

Earnings per share remained heavily negative for the third quarter in a row.

For the balance sheet, the firm finished the quarter with $93.6 million in cash and equivalents and $164.4 million in total debt.

Over the trailing twelve months, free cash flow was $25.1 million, of which capital expenditure accounted for $6.9 million. The company paid a hefty $36.1 million in stock-based compensation.

Looking ahead, management guided to full-year 2022 revenue of $545 million at the midpoint of the range and consolidated adjusted EBITDA of $70.5 million at the midpoint.

Regarding valuation, the market is valuing MEG at an EV/EBITDA of 35.8x.

However, the company is still twice its size at IPO but has more significant organic growth, higher margins, and better cash flow.

Although its gross revenue growth will likely continue to be challenged due to the drop off of COVID-19-related revenue in its CTEH unit, the firm’s other segments are producing impressive growth and gross margins are trending higher.

Given the tailwinds the company sees from environmental regulatory actions in the U.S., MEG is positioned for further growth ahead.

I’m Bullish on MEG at around $48.00 per share.

Be the first to comment