linearcurves/E+ via Getty Images

What a Difference a Quarter Makes

Following a tough Q2 FY ‘23 that saw shares pummeled in part due to subdued guidance for Q3 FY ‘23 and the full-year FY ‘23, document-based storage leader MongoDB (NASDAQ:MDB) posted a strong rebound following the release of their Q3 earnings earlier today. As I write this, shares are trading north of $183 in after-hours trading, up more than 26% based on today’s market close of $144.69.

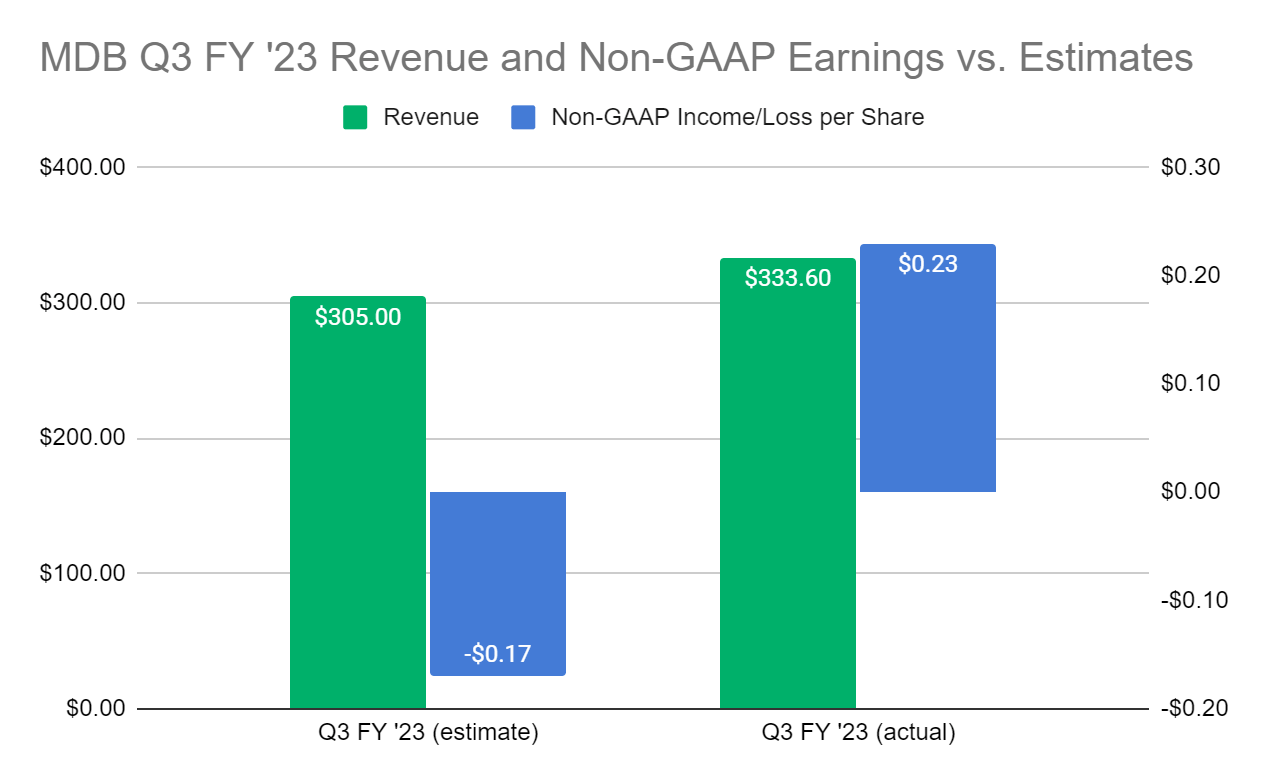

Investors are clearly very happy with MDB’s top-line result of $333.6M which crushed the ~$305M estimate. MDB also posted adjusted non-GAAP net income of $0.23/share versus the estimate of a ($0.17)/share loss.

Figure 1: MDB Q3 FY ‘23 Revenue and Non-GAAP Earnings vs. Estimates (Yves Sukhu/Seeking Alpha)

Notes:

-

Revenue and non-GAAP earnings estimates data from Seeking Alpha.

Beyond total sales and earnings, management offered investors quite a bit of news to cheer about, including a number of very bullish market signals:

-

MDB’s Atlas cloud database-as-a-service (“DbaaS”) revenue grew 61% versus the prior period and comprised ~63% of Q3 FY ‘23 revenue.

-

The company ended Q3 with more than 39,100 customers, reflecting ~6% growth versus ~37,000 customers following the end of Q2 FY ‘23.

-

MongoDB’s open source Community Server edition was downloaded more than 150 million times over the last 12 months ended October 31, 2022, reflecting greater download volume than MDB’s entire company history through the beginning of 2020.

-

In Q3 FY ‘23, MDB recognized more than 300,000 sign-ups for Atlas’ free-tier, reflecting a 15X increase over the last 5 years.

When we put MDB’s performance in the context of the macroeconomic conditions that the tech industry operated under exiting the summer, it is easy to understand why shares are up 26% after-hours. What a difference a quarter makes…

Time to Change My Tune?

As with many other tech players, I love MDB as a company. I think their implied mission to turn the database market on its head, and give legacy players like Oracle (ORCL) a “run for their money”, is an important one; and perhaps even a vital one whereby players like ORCL could and should see their power/influence diminished in the marketplace.

I want to love MDB as an investment. In the past, I’ve struggled to get there. Is it time for me to change my tune?

In my last article on the firm following their Q2 FY ‘23, I described 5 concerns leading me to make a bearish call on shares. I summarize each below in a slightly different order from my original report with some additional elaboration on certain points:

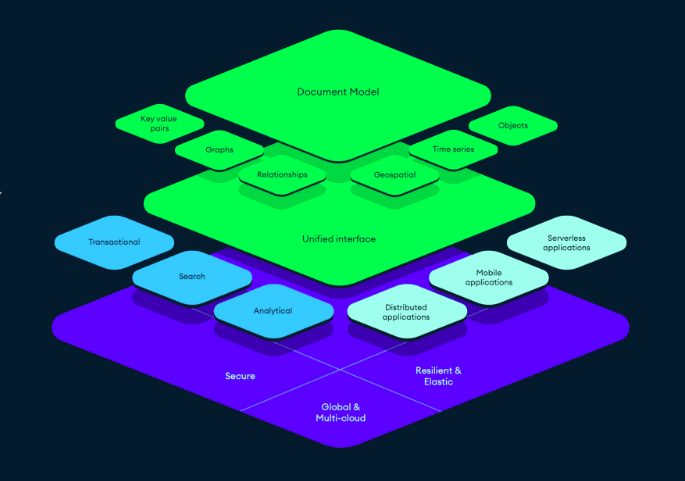

1. Their technology is not necessarily a good fit for all use cases. MDB argues that since document models are a superset of all other data models (e.g. relational, graph, etc.), their platform is extensible to a variety of use cases.

Figure 2: MDB Product Presentation FY ‘23

Management is not wrong with their general suggestion, and they note MongoDB enjoys adoption across application types. But, the whole reason there is an ecosystem of database providers is because no technology solves every problem.

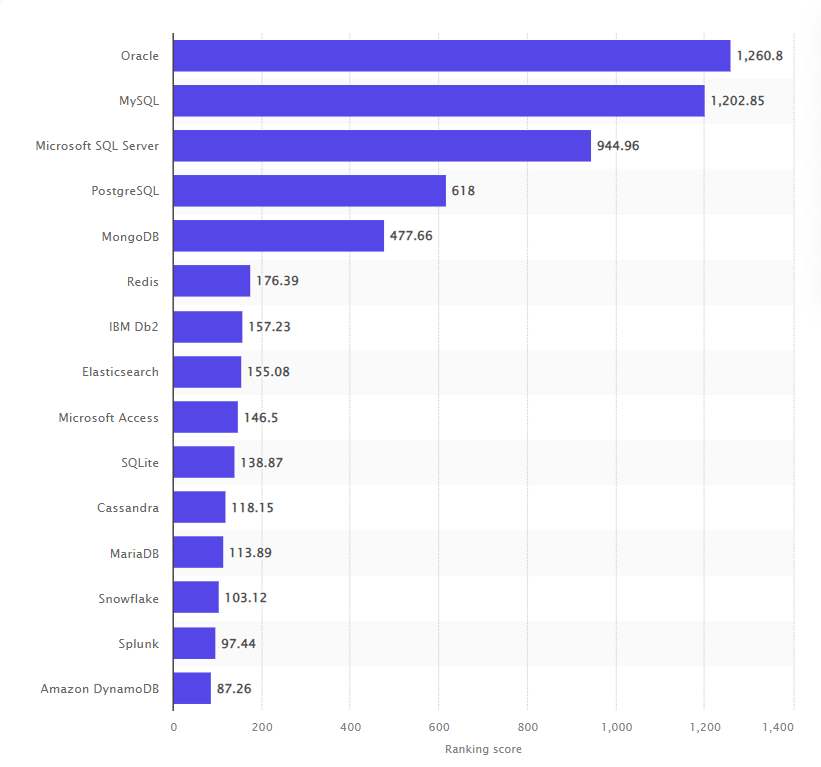

2. They have competition from every angle. Up and coming, smaller document storage players like Couchbase (BASE) are nibbling at MDB from the bottom while heavyweights like ORCL and Microsoft (MSFT) push from the top.

Figure 3: Most Popular Database Management Systems 2022 (Statista)

3. Their total addressable market (“TAM”) is tough to nail down. MDB’s TAM is certainly very-billions-of-dollars large and growing. But, with the database market sliced up every way to Sunday based on the subtleties of different technologies, and with the acknowledgment from the previous two points that MDB is not “all-things-to-all-people” and competition is intense, it’s not so easy to lasso an accurate estimate of their TAM and therefore future opportunity.

4. Legacy technologies are like religion. Legacy database technologies – the ones MDB wants to replace like Oracle – can be costly to maintain and develop. But, change is painful for many organizations. When a company is used to doing something a certain way, it’s incredibly difficult to change that pattern of behavior.

5. Valuation. Of course, MDB’s valuation is not as insane as other tech players. But, prior to today’s quarterly results, the firm sported a “D-” for valuation on Seeking Alpha with a P/B (trailing 12 months) of 15.29 and a P/S (trailing 12 months) of 9.26.

However, with today’s Q3 results in hand, I will argue against myself. Consider:

-

As mentioned, MongoDB Community Server Edition was downloaded more than 150 million times for the 12 months prior to the quarter end, and more than 300,000 Atlas free-tier accounts were opened during the quarter. Of course MDB has a lot of competition as I pointed out above because every tech company has a lot of competition. But, the volume of interest in MongoDB technologies suggests MDB is growing exponentially in terms of mindshare. That, in turn, suggests they are “winning” in the market against the competition.

-

A corollary to the download and Atlas account statistics above is that management may have been spot-on with their TAM assessment which relies upon IDC data suggesting a $121B market size by 2025. After all, if so many potential users are demonstrating interest in the technology, they must arguably reflect a very large TAM.

-

MDB turned out an incredible performance in a tough macroeconomic environment; and CEO Dev Ittycheria specifically highlighted during today’s earnings call that “cost-conscious IT decision makers” are increasingly turning to MongoDB as they modernize legacy apps and/or move to the cloud. He noted the firm as having particular traction among financial services firms – an ideal customer vertical for the business. This tells us that even the religious “stickiness” of legacy platforms can be overcome by MongoDB technology, which the firm generally positions as offering better scalability, affordability, and developer productivity. If we assume that macroeconomic conditions in 2023 (i.e. MDB’s FY ‘24) will continue to be challenging, then the company appears set to capitalize on growing interest among senior IT decision makers to retire legacy database technologies in favor of MongoDB.

-

Q3 FY ‘23 data could hint that MDB is at an inflection point in its growth where its next stage could be explosive. If we imagine the market opportunity to displace legacy technologies as a snowball rolling down a snow-covered mountain, perhaps MDB’s first ~decade of existence has been spent nudging that snowball downward, laying the groundwork so that they will be ready to grasp the opportunities that result when that snowball turns into an avalanche in their next decade of operation.

Is MDB’s Q3 FY ‘23 performance the sign that the firm is ready to take off like a rocket?

More to Like But More to Be Concerned About Also

There is a lot to like with MDB even beyond my bullet points in the previous section; and I should have included some of these discussion points in my prior (bearish) article to be more balanced.

-

MDB knows very clearly who they are selling to. They are a developer-centric organization and they market to that group. For example, in their MongoDB World Product Presentation, they note the need for business users in organizations to have access to data for analysis purposes, search, etc. However, they also note that these “[constituents] who need the data (analysts, data engineers, data scientists) are not MongoDB’s target customers.” Too many tech companies waste time, resources, and money trying to sell to organizations without truly understanding who their target customer is. MDB has no issue in this regard.

-

They are ramping up their tooling to push more legacy migrations. MDB is introducing a software tool called Relational Migrator to facilitate migrations from relational databases (e.g. Oracle, Microsoft SQL Server, etc.) to MongoDB. The company notes the software will initially be utilized by their pre-sales team in 2023 during customer engagements, but will be eventually offered to customers directly who can then leverage the tool to (better) automate the transition from their legacy database platforms to MongoDB.

-

Their “lower-friction” approach to the market allows them to play across customer buckets. Mr. Ittycheria explained that MDB is winning new workload opportunities in all kinds of customer accounts, from start-ups to Fortune 500 companies. MDB’s technology and market approach make their offerings accessible to small, mid-size, and large customers. Granted, this strategy is true of many tech companies today. But, it is still a point of differentiation for MDB and other newer database players. Are you going to find a start-up leaning towards Oracle or IBM Db2 (IBM) for their database technology? Probably not…

With my bull points laid out, I wouldn’t be me if I didn’t now outline my additional areas of concern.

1. Downloads and free accounts don’t equal revenue. Developers, MDB’s target customer, are always keen to “kick the tires” of a new technology. Hence, even though MDB’s download and Atlas free account statistics are very impressive – and I tend to think meaningful – we should not get too carried away thinking the data will necessarily translate into explosive top-line and/or bottom-line results.

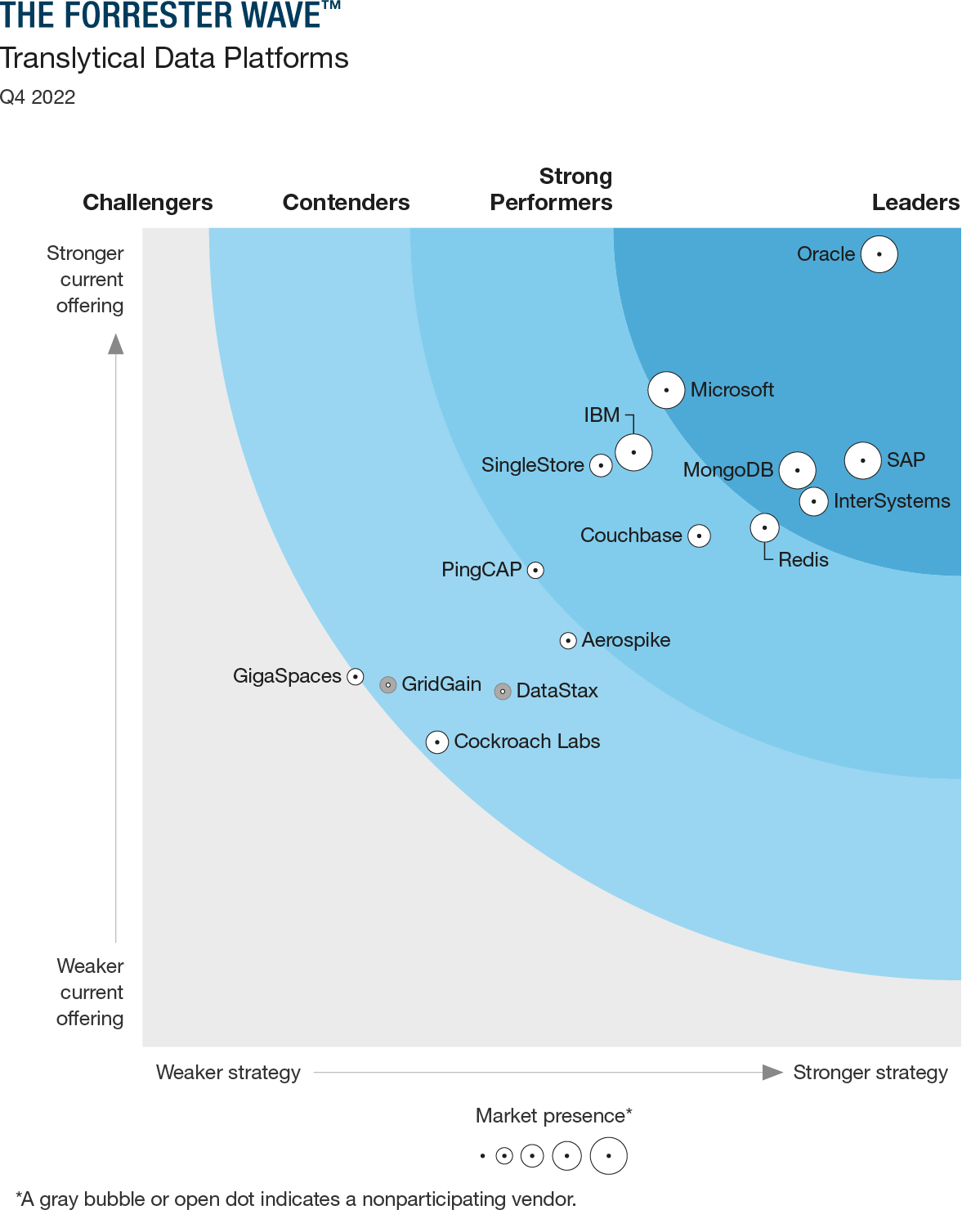

2. MongoDB is a database platform leader, but still lags the king. Forrester recently published their Forrester Wave for Translytical Data Platforms Q4 2022, naming MongoDB as a leader.

Figure 4: Forrester Wave Translytical Data Platforms (Forrester)

But, as we can see from Figure 4, there is still quite a large gap between MongoDB, and other leaders like Microsoft SQL Server, and Oracle. Moreover, the report scores MDB’s current offering significantly lower than Oracle on Forrester’s 5-point scale. Now, we are comparing a ~13 year-old organization versus a nearly ~50 year-old organization. We should expect a big gap; and to MongoDB’s credit, they are recognized as a leader after ~1 decade of existence. But, it implies there are nonetheless application use cases where MongoDB is not the best choice, with Forrester remarking that “…MongoDB’s [database] platform lags in extensibility…[and] reference customers had concerns around ‘handling a high volume of data’ and ‘ultra-low latency.’” Again, no technology solves every problem.

3. Legacy players will discount aggressively to protect their market share. Oracle and other legacy players are not, generally speaking, going to be displaced without a fight. Firms like ORCL, IBM, and MSFT, because of their size and maturity, can absorb large discounts to maintain and protect their market share. While I can’t name the company, I would offer that when I was selling enterprise software, one of my employers would sometimes apply discounts in excess of 90% on certain software just to protect the install base because it was considered so strategically important to the business. So, while MDB management makes overtures of ripping legacy players out of accounts, you can be sure that it is still going to be an uphill battle in 2023 and beyond as legacy providers do their best to accommodate customers from a pricing perspective.

4. I’m a little surprised Relational Migrator is only coming out now. MDB has long driven a sizable portion of its revenue from legacy migration opportunities. I would have thought they would have developed tooling to support those efforts some time ago. Although, migrations – generally speaking – are never easy and MDB may have needed time to develop software that is sufficiently sophisticated while maintaining (presumably) some degree of ease-of-use. Still, I find it curious that the tool is only coming out now.

5. It can be dangerous to follow the herd. The after-hours action which has sent MDB stock soaring may introduce a feeling of FOMO. I get that. But, I think the worst thing an investor can do is jump on a stock just because everyone else is jumping on it. Did anything change materially with MDB’s operation as a business in Q3? Well, obviously, they beat on their top and bottom lines; but let us remember they are still an unprofitable enterprise and, at the moment, there is no guidance from management on when the business will turn positive.

Humming the Same Tune

As mentioned, I want to love MDB as an investment. But, I find myself humming the same tune. I just can’t get there yet and still recommend the stock as a “sell”.

Management has issued bullish guidance for Q4 and for the full-year, but will not offer any forecast for FY ‘24 until March of next year.

Figure 5: MDB Q4 FY ‘23 and Full Year FY ‘23 Guidance (MDB Earnings Release Q3 FY ’23)

Customers who are using MongoDB strategically certainly won’t be moving off the technology anytime soon; and the install base alone will provide the company with opportunities to grow for years to come, as evidenced by the firm’s net retention rate of ~120% in Q3. However, as I argued, if 2023 turns out to be a challenging year from an economic point-of-view, MDB investors may find legacy players stepping up their discounting game to hold onto their market share. They, effectively, will bet on making up the “loss” when the economy recovers.

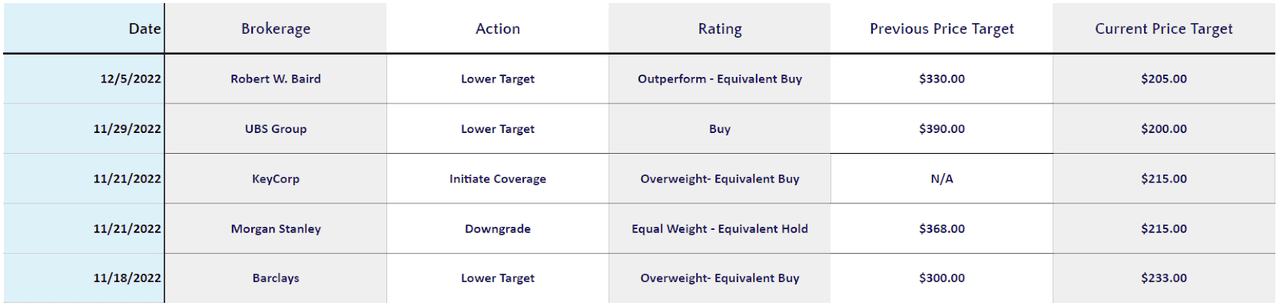

As is often the case when I make a call on a tech firm, my position is at odds with other analysts.

Figure 6: MDB Selected Analyst Ratings (MarketBeat)

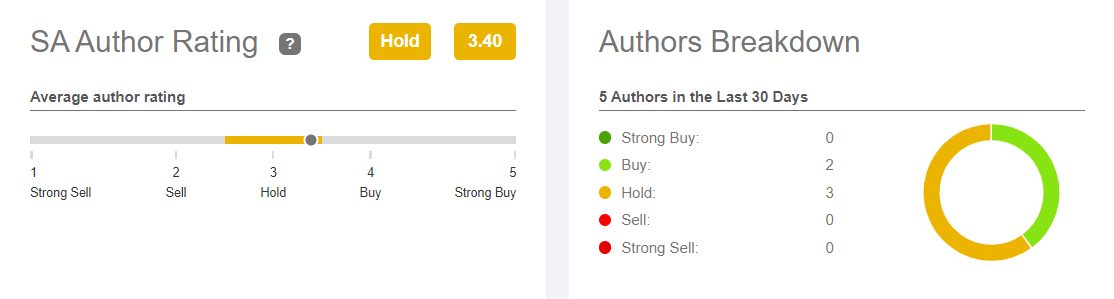

Seeking Alpha authors also lean in generally bullish direction toward the company.

Figure 7: MDB Seeking Alpha Analyst Ratings (Seeking Alpha)

As with anything, I may be proven completely wrong on MDB – an outcome I would be happy to accept since, as I mentioned, I think their implied mission to unseat the incumbent database vendors may not just be important, but vital. As a prospective investor, I would welcome more data from management with respect to migration activity by quarter, as well as more insight into the growth rate of strategic workloads running on MongoDB quarter-over-quarter. I think that level of detail would provide greater clarity into the ongoing adoption (or lack thereof) of the platform.

Be the first to comment