Manuta/iStock via Getty Images

Overview

Investors need a long-term perspective to take advantage of the Mohawk Industries (NYSE:MHK) share price mispricing today, but they also need to be wary of the near-term dangers, so the 4Q22 result is pretty mixed all around. The risk is that management does not meet their guidance or mis-executes, even though they have indicated that they expect things to begin to improve in 2H23. While the 8% FCF yield and possible multiple re-rating once we emerge from this period of weakness are compelling, I believe it is prudent to take no position until 2Q23, when we will have more information from management regarding performance and insights into early 3Q23.

Earnings update

MHK’s operating EPS in 4Q22 was $1.32, which was slightly higher than the high end of guidance and above the consensus estimate of $1.27. Gains in global ceramic margins were the primary driver, followed by gains in flooring ROW margins, a lower adjusted tax rate, and decreased corporate expenses. MHK forecasts 1Q23 operating EPS of $1.24-1.34, which is significantly lower than consensus estimate of $1.69.

Demand

My guess is that the unfavorable global situation – consumers reacting to inflation and industry players adjusting strategies to counteract the pull-forward demand from the previous year – is to blame for the sluggish demand in the first few months of 2023. Destocking, waning demand, and tougher comparisons should put a damper on 1H23’s volume. However, management guided for a rebound in demand in 2H23 as a result of falling energy prices and rising wages, especially in Europe. Overall, volume is expected to be down low single digit % in the current environment, with volumes possibly inflecting positively in 4Q23 due to the much easier comps. Specifically for flooring, being a more expensive discretionary purchase, has experienced a more rapid and severe correction in demand than other categories of building products; but I expect the decline in 2023 to be more moderate and the recovery to be quicker. All in all, I anticipate that this year’s revenue will remain under pressure from both lower volumes and pricing (due to mix). Nonetheless, I am optimistic about efforts to reallocate resources toward product lines that can sustain growth in the long run – as such, I am more positive about the long-term outlook.

Margins

As raw material costs fall and production slows and pricing and product mix shift as volume declines, I believe the path to margin reversion is what investors are paying attention to. Management believes that the tailwind of slowing global energy prices, especially natural gas, which peaked in 3Q22 and is now declining, will become a tailwind in 2Q23. A rise in production rates will further solidify the path to margin expansion, as it will bring output out of its current slump and into line with the broader housing and R&R sectors. My guess is that the 2Q operating margin will improve sequentially by more than usual thanks to the increase in utilization rates, which also leads me to believe that if the volume were to recover as expected, margin should continue to improve sequentially.

Overall, I anticipate FY23 to be the low point for MHK margins/earnings as operating conditions gradually stabilize, including moderating energy headwinds. As of today, MHK is still clearing out high-cost stockpiles and realigning production to meet consumer demand, as such output has been relatively flat so far this year. But I anticipate a sequential improvement in 2H23, with the potential for further margin expansion, should order rates revert to higher levels. The path of margin expansion is also supported by MHK’s ongoing efforts to boost efficiency and cut costs through consolidation and the development of new, high-growth markets.

Valuation

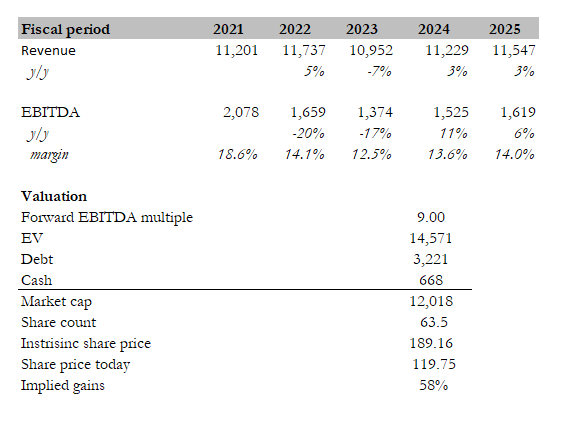

As previously stated, I believe the catalyst here is improved margin reversion following a weak 1H23. Assuming margins expand as expected and top-line growth is slightly slower than historical rates (being conservative), EBITDA growth should be in the mid-single digits to low-teens. As this occurs, I anticipate the market attaching a higher multiple to MHK stock (at the very least reverting to the 10-year average), as investors anticipate further margin improvement and growth. All of this adds up to a market cap of $12 billion (FY21 levels), or $120 per share.

In addition to earnings growth and multiple revaluation returns, shareholders benefit from MHK’s current high FCF yield (8% yield). This could be used to repurchase shares, boosting EPS growth.

Own estimates

Conclusion

While there are some mixed factors affecting the company’s performance in the short term, I believe the long-term outlook for MHK is positive. Still, I think investors should exercise caution and wait until more information is available before taking a position.

Be the first to comment