hapabapa

Moderna, Inc. (NASDAQ:MRNA) presented at the closely-watched 41st Annual JPMorgan Chase (JPM) Healthcare Conference on January 9, following the successful release of its personalized cancer vaccine (PCV) study with Merck’s (MRK) Keytruda.

CEO Stéphane Bancel & his team answered our call with aplomb as we questioned the clarity of Moderna’s pipeline with COVID having entered an endemic phase. While still early, Moderna’s partnership with Merck’s leading drug, Keytruda, demonstrates the promise and potential efficacy of the company’s platform.

We believe that under Bancel’s leadership, Moderna seems ready to continue its push to capitalize on its COVID success, with the company projected to post $18.4B in COVID vaccine revenue for FY22. However, Bancel also highlighted ahead of its Q4 and FY22 earnings release (estimated for February 24) that the company expects just $5B in confirmed COVID vaccine revenue for FY23, excluding additional booster contracts.

Hence, we believe Moderna investors have the right to know whether the company’s platform technology could be relied upon to deliver success over the medium- to long-term.

Early MRNA investors have continued to outperform the market, as it posted an all-time total return CAGR of 76.7% from late 2018. MRNA also beat the S&P 500 (SP500) over the past year, notching a 1Y total return of -8.7%.

But, could arch-rival BioNTech SE (BNTX) do one better over Moderna, as both companies aim to develop a successful PCV platform that could significantly impact their long-term buying sentiments?

BioNTech relies on a different trial set in applying its mRNA technology to its melanoma cancer vaccine development with Roche Holding AG (OTCQX:RHHBY). Bloomberg reported that “it’s harder for BioNTech to shine,” given the trial set parameters.

BioNTech set up its study “treating patients whose tumors have spread and who haven’t yet had other treatment, whereas [Moderna] gave its medicine to people who’d had surgery to excise their cancer.”

Yet, the challenge has not unfazed BioNTech CEO Ugur Sahin. He articulated that the company’s approach is akin to a “proof of concept,” as it “is a much higher hurdle [to cross than Moderna’s approach].” As a result, the company believes that it could provide a stronger justification for the efficacy of its vaccines if proven successful.

It could also cause consternation among investors if BioNTech fails to execute accordingly, with Bloomberg cautioning that “if first-line melanoma doesn’t work out, the stock could get badly hit.”

Notwithstanding, BioNTech has proved the success of its COVID platform, as its partnership with Pfizer led to its global dominance in the COVID vaccine market ahead of Moderna. As such, Moderna shouldn’t rule out the potential for BioNTech to run ahead of it again, even as MRNA grapples with its transition to a private market for its COVID vaccines.

Accordingly, Bancel & his team have drawn the ire of the White House and the incoming Chairman of the Committee on Health, Education, Labor, and Pensions in the United States Senate, Sen. Bernie Sanders.

Moderna highlighted that it considered the price range of $110 to $130 promulgated by Pfizer, Inc. (PFE) for its private-market COVID vaccines, as “reasonable.” However, the White House demurred, stressing the move as “hard to justify.” Sen. Sanders also took umbrage with Moderna’s management as he discussed how the COVID vaccines had enriched its top management and investors.

He also reminded Moderna that:

The purpose of the recent taxpayer investment in Moderna was to protect the health and lives of the American people, not to turn a handful of corporate executives and investors into multi-billionaires. – Bernie Sanders government website

Thinking back, Pfizer’s decision not to accept the U.S. government’s money for its COVID R&D has likely shielded the company from unnecessary drama and debate as the company transits to the commercial market. Will Moderna’s decision to accept government funding for its R&D return to haunt the company?

We think it’s still too early to tell. Pfizer-BioNTech’s price range as the market leader makes sense for Moderna to follow. But, if Moderna was “compelled” to lower its prices, we believe Pfizer-BioNTech will likely need to respond accordingly to secure its commercial interest. Hence, we urge investors to continue watching this space as it could determine the trajectory of Moderna’s COVID revenue moving ahead.

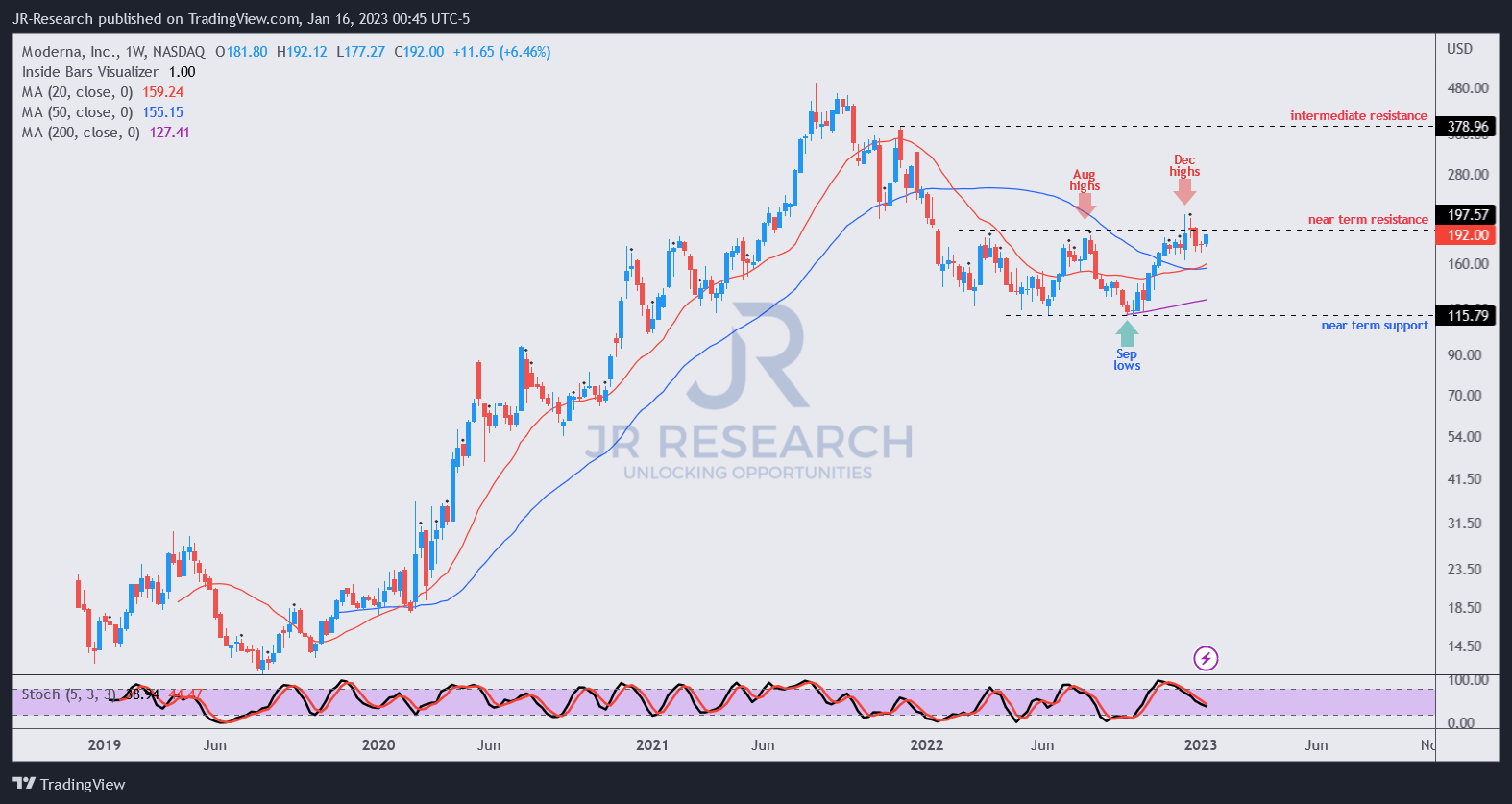

MRNA price chart (weekly) (TradingView)

Moderna, Inc. has continued to consolidate robustly within its trading range. Its December bull trap highs also acted as a significant resistance zone, allowing investors who picked its lows in late September to take profit, as it knocked back the buying momentum from over-zealous investors who bought into the Moderna-Merck PCV news in mid-December.

Notably, it seems Moderna, Inc. has increasingly shrugged off its consolidation zone, with buyers looking to form higher lows and help recover its upward bias.

Therefore, we urge investors to watch Moderna, Inc.’s pullback closely and assess whether the consolidation is robust. A further fall back toward its September lows can be used to add Moderna, Inc. exposure more aggressively.

Rating: Hold (Reiterated).

Be the first to comment