Zorica Nastasic/E+ via Getty Images

Amid the geopolitical storm involving the Chinese spy balloon and implications of national security, Georgetown University’s Center for Security and Emerging Technology (CSET) found that $40.2 billion of the total money raised by all Chinese AI companies between 2015 and 2021 had U.S. backing.

I read it with interest because this study referenced my Dec. 13, 2021, Seeking Alpha article entitled “Intel’s Mobileye: Strong Headwinds From Competitor SoCs, Particularly In China.” More on that later in this article.

Chart 1 shows the top 10 U.S. VC investors. Of primary interest in this article is Intel (INTC) through Intel Capital, its investment arm, which made 11 Chinese AI transactions between 2015 and 2021, just 8% of the 144 total transactions it made on AI-related deals.

CSET

Chart 1

One of Intel Capital’s investments was China’s Horizon Robotics. Horizon Robotics specializes in AI chips for robots and autonomous vehicles. The company’s Series A funding round in October 2017 was led by Intel Capital. Horizon’s latest generation automotive processor, Journey 5 — a high-performance automotive processor designed for Level 4 autonomous driving.

Horizon has now partnered with the top electric vehicles in China and Europe. Unfortunately, these auto-grade AI chips from Horizon compete directly against Intel’s Mobileye, which also enables Level 4 autonomous driving.

In May 2021, Chinese electric car firm Li Auto announced that it would be leaving Mobileye (NASDAQ:MBLY) in favor of Horizon Robotics. The EV model Li ONE is equipped with two Journey 3 autonomous driving chips from Horizon Robotics. The 2021 model uses the Journey 3 chip, which has 5 TOPS of computing power and 2.5W of power consumption, both better than EyeQ4.

Most importantly, older 2020 Li ONE models used the Mobileye EyeQ4 vision recognition chip, which has 2.5 TOPS of computing power and 3W of power consumption.

This article analyzes Mobileye’s technology and growth potential compared to a number of companies making autonomous driving SOCs (system on a chip).

Mobileye Metrics

Chart 2 shows the growth of Electric Vehicles, the prime type of vehicle for ADAS. EVs are projected to grow from 3.1 million units in 2020 to 25.8 million in 2026, a CAGR (compound annual growth rate) of 42%, according to our report “Global and China EV Batteries and Materials: Technology, Trends and Market Forecasts.”

The Information Network

Chart 2

Through 2022, Mobileye products had been installed in more than 800 vehicle models with 50-plus automakers worldwide. According to our report entitled “Hot ICs: A Market Analysis of Artificial Intelligence (“AI”), 5G, Automotive, and Memory Chips,” Mobileye products will be built into 42% of vehicles sold in 2022, with a 69% market share in advanced driver assistance systems (“ADAS”).

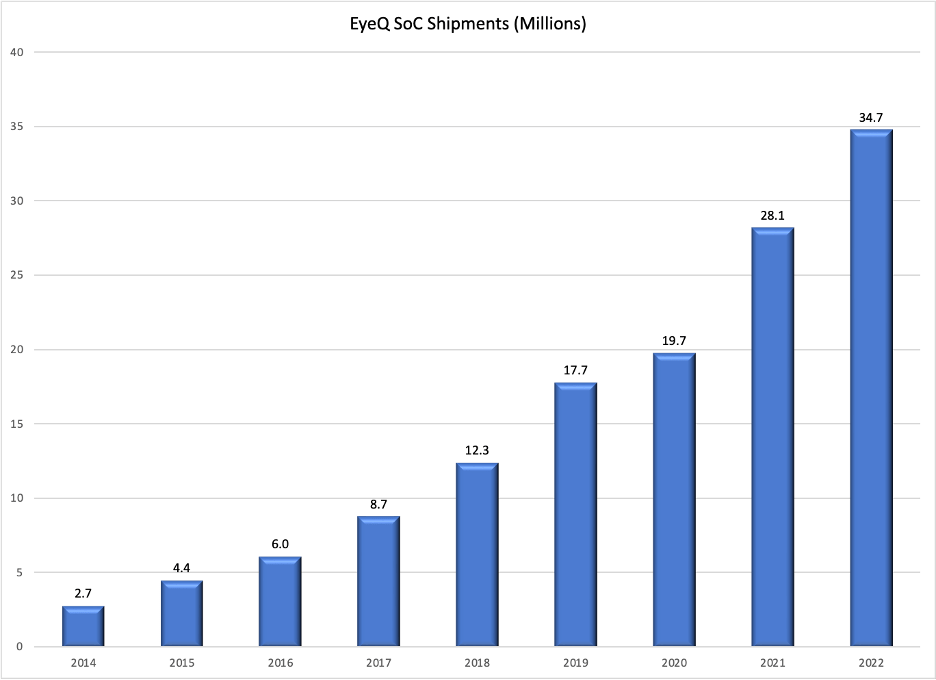

Chart 3 shows the growth of Mobileye SoC shipments between 2014 and 2022, reaching 34.7 million in 2022. For clarification, an SOC (system on a chip) is an integrated circuit that combines many elements of a computer system such as a GPU, CPU, and acceleration core into a single chip.

Mobileye

Chart 3

Competition from Alternative Automotive AI Chips

Autonomous driving systems require a lot of computing power because they have to process a variety of sensor data. Among them, the processing of visual image data from the camera consumes the most computing power.

For each level of autonomous driving, the required computing power increases by at least several times. For example: L2 level requires 10+ TOPS of computing power, L3 requires about 100 TOPS of computing power, L4 level may require about 500 TOPS of computing power, and L5 level even requires more than 1000+ TOPS of computing power.

In addition to theoretical hardware computing power, the actual computing power utilization is also crucial. The architectural design of different AI accelerators usually leads to different actual utilization of hardware computing power. Therefore, the same neural network model runs on two AI accelerators with the same hardware theoretical computing power. Different measured performances.

Most autonomous vehicles employ a system of cameras, radar, laser sensors and other technologies to assess road conditions and adjust driving behavior. These vehicles might have adaptive cruise control, traffic lane adjustments and automatic braking, steering and acceleration.

The level of autonomous driving and the computing power of the chip are inseparable. The autonomous driving industry generally believes that the chip computing power (Trillion Operations Per Second (“TOPS”)) required for L2 autonomous driving is below 10 TOPS, L3 requires 30 to 60 TOPS, L4 requires more than 100 TOPS, and L5 requires more than 1000 TOPS. It’s precisely because of this that chip computing power TOPS has become the core weight of various chip competitions.

If car companies use multiple chips to build autonomous driving domain controllers, they can reach a maximum of 1,024 TOPS, which can support L4 autonomous driving.

While a single chip’s computing power TOPS is a key indicator, it’s not the only one. Autonomous driving is a complex system that requires car-road-cloud-side collaboration. Therefore, in the competition of autonomous driving chips, in addition to the core, there’s also software and hardware collaboration, as well as platforms and tool chains.

At present, there are numerous competitors in the automotive AI chip market, presenting headwinds to Intel and Mobileye, including Qualcomm (QCOM) and Nvidia (NVDA), Tesla (TSLA) and Chinese companies Huawei, Horizon Robotics, Black Sesame Technologies, and Xin Chi Technology.

Table 1 shows a list of companies, their chip versions (current and planned), and TOPS for the chips.

The Information Network

Investor Takeaway

In the ADAS industry, Mobileye EyeQ series chips account for a 69% of the global market share of visual perception chips, and their position is unshakable.

The biggest advantage of the Mobileye chip platform is that the product cost is low, the development cycle is very short, the development cost is extremely low, and most of the functions have been verified and there’s no risk. The disadvantage is that the system is very closed, it is difficult to develop special functions, it’s difficult to iterate, and it’s difficult to improve or upgrade if there’s a problem.

Headwind #1

Although Mobileye provides car companies with a software-hardware integrated chip + algorithm solution, the EyeQ chip is like a “black box,” and car companies cannot inject their own algorithms on the chip. This “black box” approach has created an opportunity for ADAS SOC competitors detailed in this article.

There have been car companies trying to develop autonomous parking solutions based on Mobileye’s visual perception, but because Mobileye did not support customers to update their perception algorithms independently, development was blocked.

To a large extent, it’s for this reason that Tesla and Mobileye parted ways in 2016 and embarked on the path of self-developed chips.

Driven by this trend, I expect Mobileye’s “open” strategy is inevitable. In fact, after the EyeQ 5 chip was released, Mobileye tried to become open, allowing third-party code to be written into the chip.

Headwind #2

Intel acquired Mobileye for $15.3 billion in 2017, kick starting its move into autonomous driving. Mobileye shares were relisted in October 2022 and valued the company at about $21 billion.

Of interest is that Intel Capital invested in China’s Horizon Robotics in October 2017. Horizon Robotics raised $100,000,000 series A round from 5Y Capital, Harvest Investments, Hillhouse Capital Group, Intel Capital and Wu Capital.

That investment may have helped Horizon Robotics better compete with Intel.

Be the first to comment