Art Wager/E+ via Getty Images

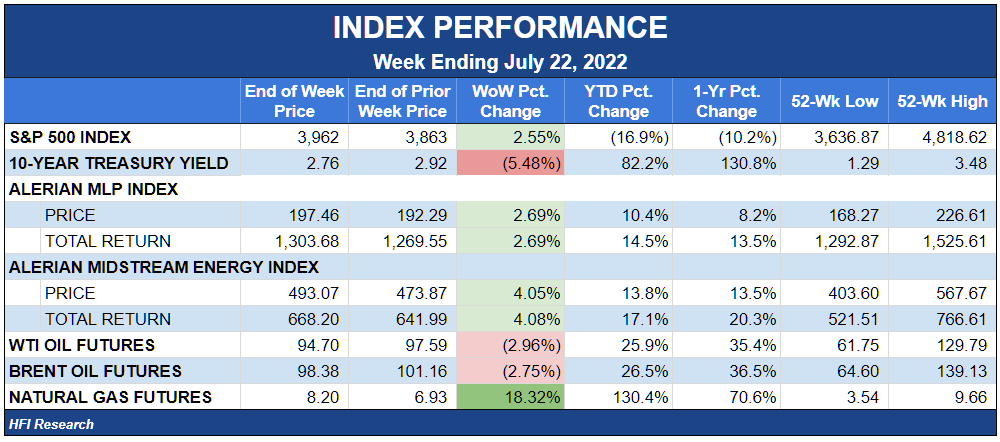

Midstream Sector Performance

Midstream edged out the S&P 500 with a 2.7% gain during the week. The index followed the XLE and XOP higher, bucking the trend of falling oil prices.

HFI Research

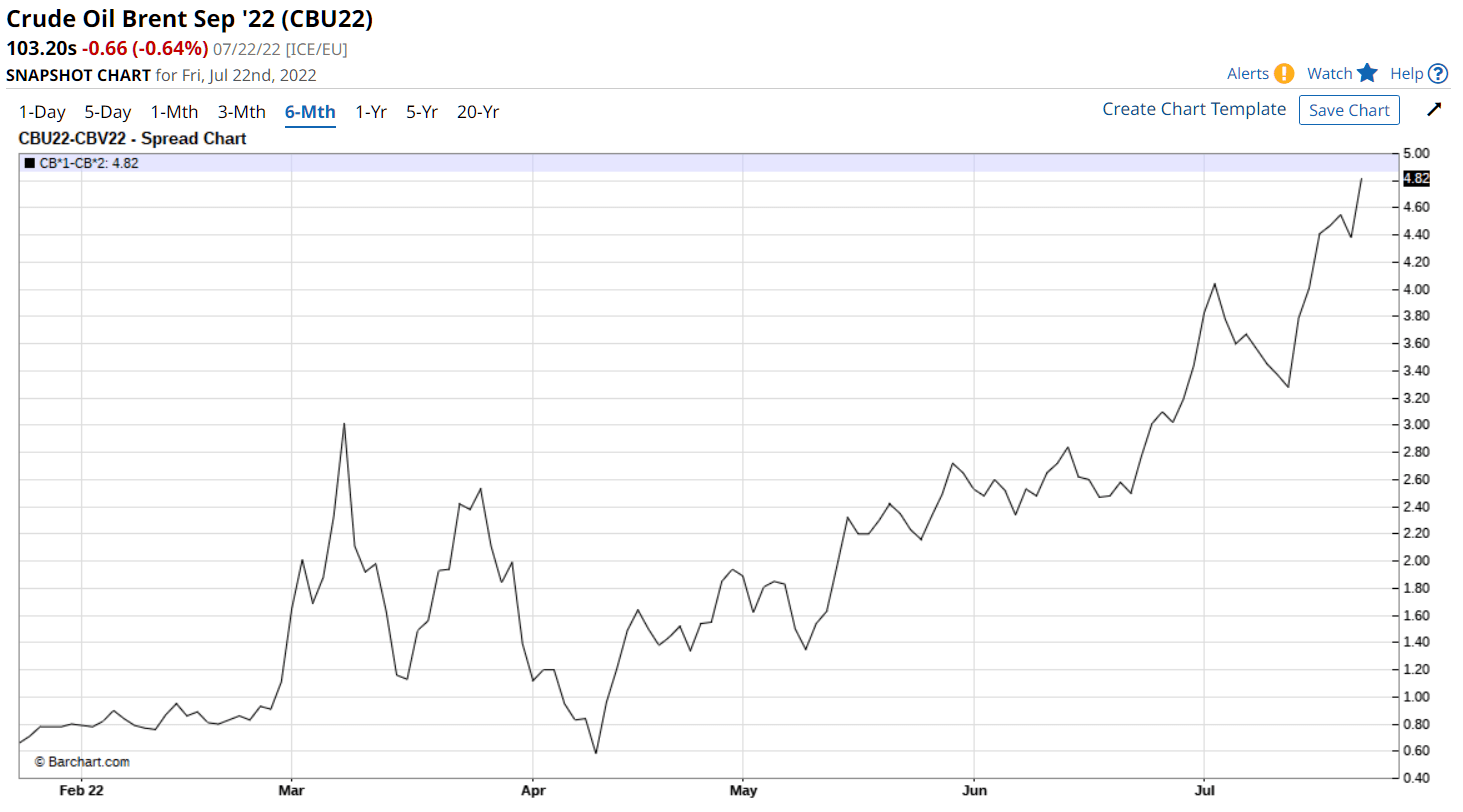

Despite oil’s fall, the physical market remains extremely bullish. Backwardation soared higher even as front-month crude prices fell.

Barchart.com

Source: Barchart.com.

We believe it’s only a matter of time until the tightness in the physical oil market and the strong demand for near-term barrels push prices higher.

Energy Earnings Come In Strong

Kinder Morgan (KMI) kicked off the midstream earnings season with a big beat on the top and bottom lines. Management raised its EBITDA guidance 5%. The stock was up 5.3% for the week and was one of the sector’s strongest performers. KMI has clearly benefitted from surging natural gas production, consumption, and prices. We’ll have an update on KMI’s quarterly report and the market’s reaction on Monday.

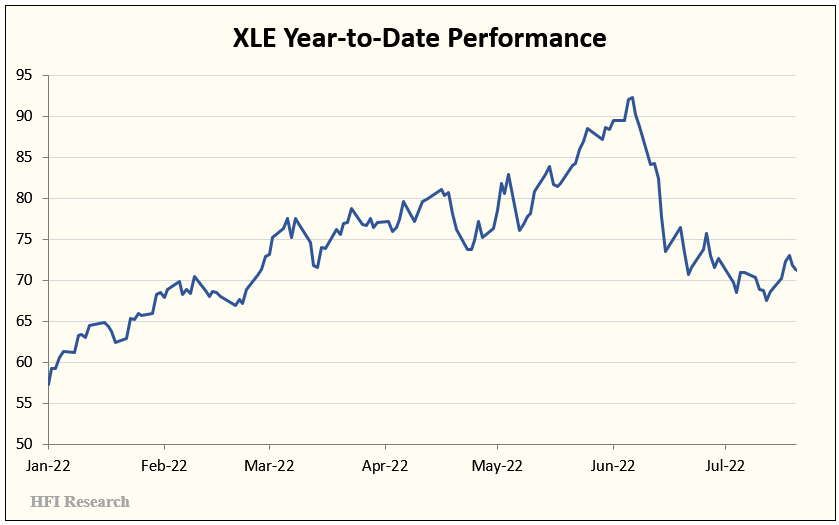

We believe KMI’s earnings report was a harbinger for the midstream sector, which is set to benefit across the board from a bullish domestic energy backdrop, from booming LNG exports to NGL price increases to record high refinery throughput. The improving fundamentals are likely to translate into strong performance for energy equities, which have declined by 19.7% since June 1.

HFI Research

Additional evidence of a strong second quarter for midstream came from earnings reports from Halliburton (HAL) and Schlumberger (SLB). Both reported historic strength in their domestic oilfield services business, suggesting that gathering and processing results should continue the bullish trajectory they’ve followed for several quarters.

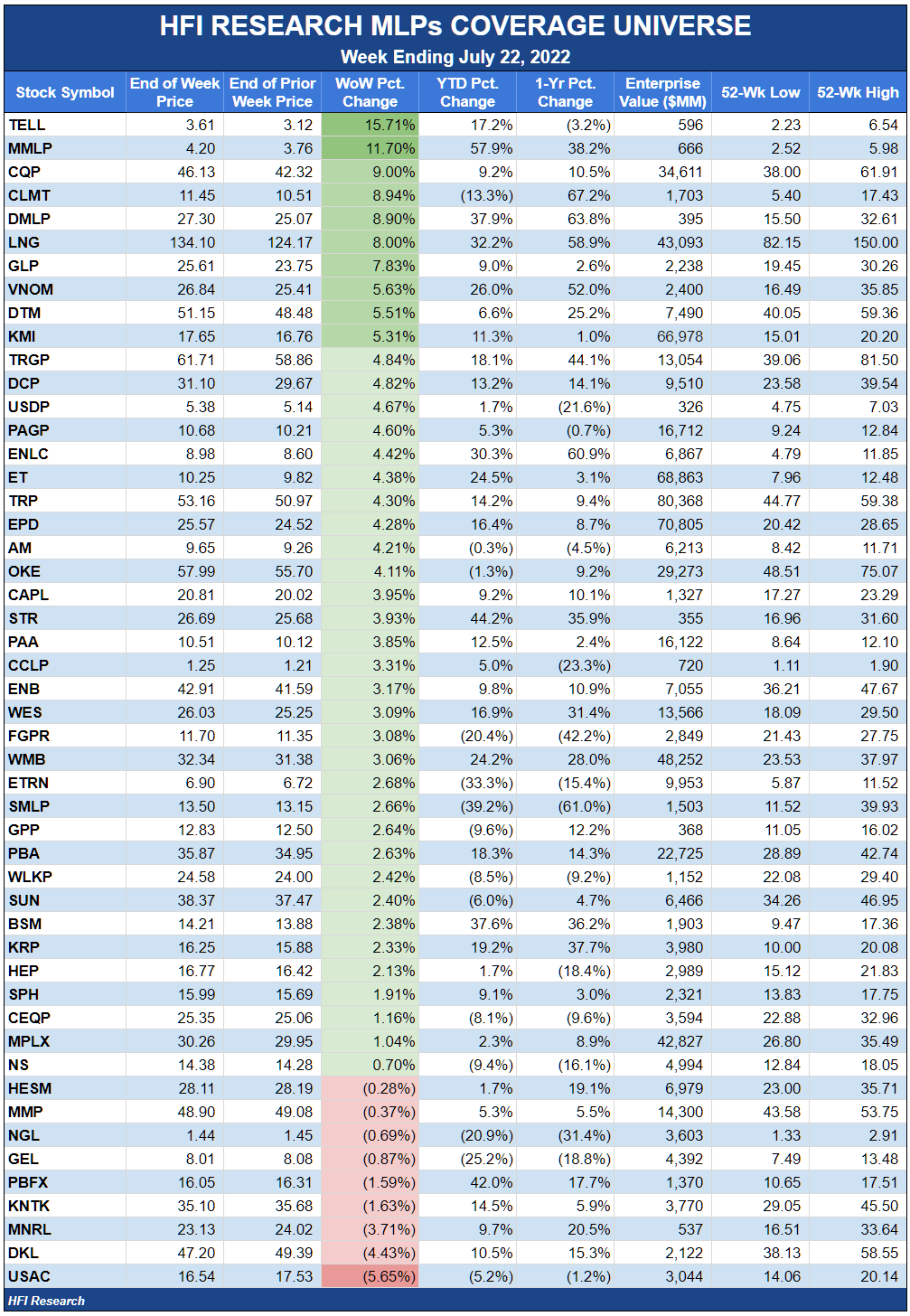

Long-Haul Liquids Lag

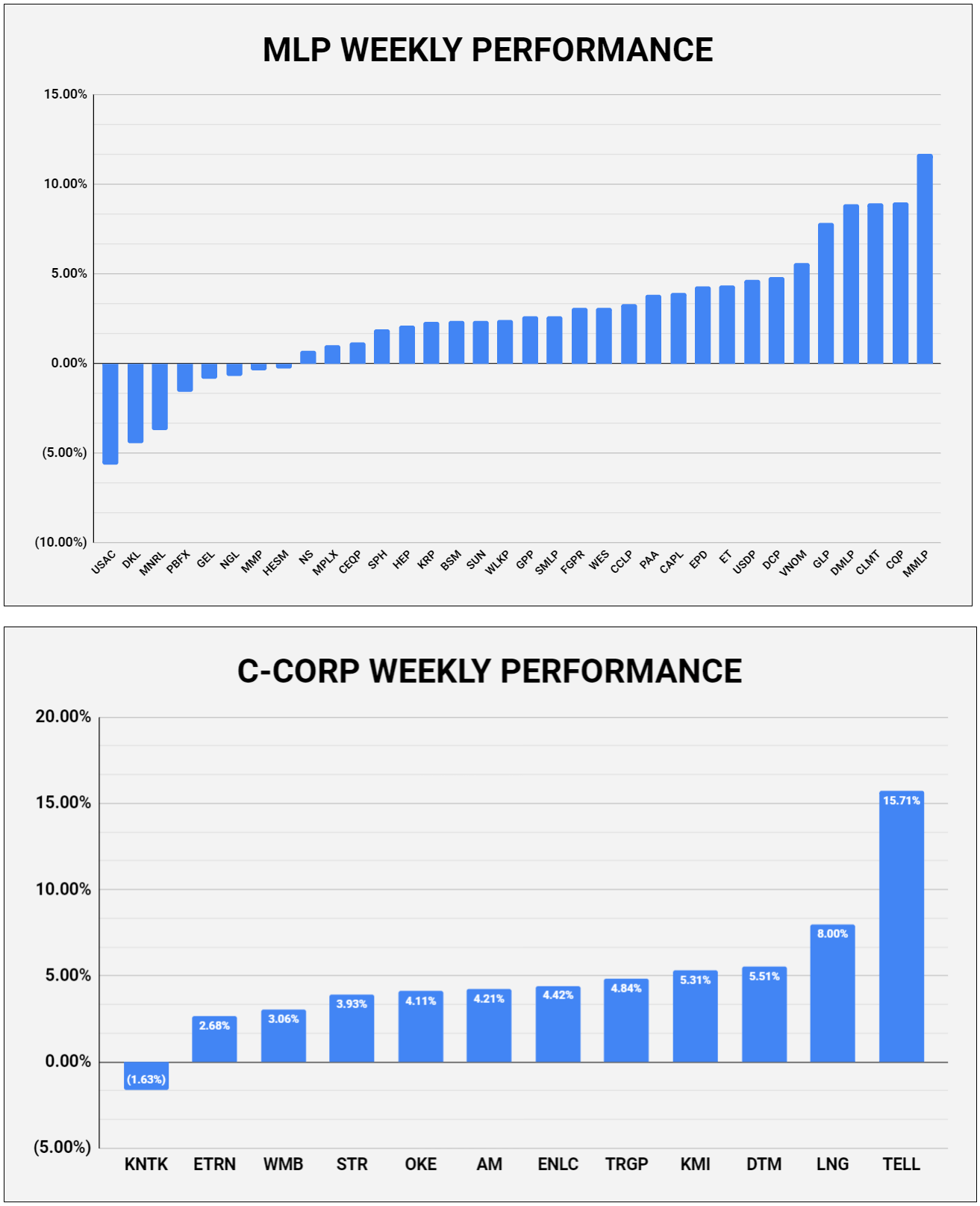

During the week, gathering and processing companies were unusually strong in the face of volatile and ultimately lower crude oil prices. Mineral/royalty interest owners also showed surprising strength. Meanwhile, there were only nine decliners in the sector, with USA Compression Partners (USAC) the weakest despite the positive read-through it received from HAL’s and SLB’s reports of extreme tightness in the oilfield service equipment market.

C-Corps dramatically outperformed MLPs. Eight of the nine decliners were MLPs, with only Kinetik (KNTK) trading lower among the C-Corp group.

HFI Research

MLPs were held back by their heavier weighting in long-haul pipelines that transport crude oil and refined products. Liquid pipeline equities – such as Magellan Midstream (MMP), MPLX (MPLX), and NuStar Energy (NS) – were particularly weak, as their units were correlated with the weakness in crude oil.

These MLPs are not directly affected by crude oil price changes, so the high correlation between their equities and crude makes little sense, particularly in light of how undervalued they are. We believe the bearishness on these names is misplaced. Firstly, we do not think these moves imply anything about future crude oil prices. Falling refined product prices are reducing refining margins more than crude oil prices and are stimulating end-user demand. The market remains supply constrained and will encounter bullish catalysts later this year.

Second, and more importantly, each liquids pipeline operator is set to benefit from rate increases on their interstate pipelines. The rate increases are effective as of July 1. Those set by reference to the FERC Index are set to see increases of as much as 8.7%, which will deliver a big boost to EBITDA. We’d note that KMI put through an 8.7% rate increase on all its refined product pipelines, as management reported on the company’s earnings conference call. These depressed liquid-heavy MLPs are clear Buys at current prices.

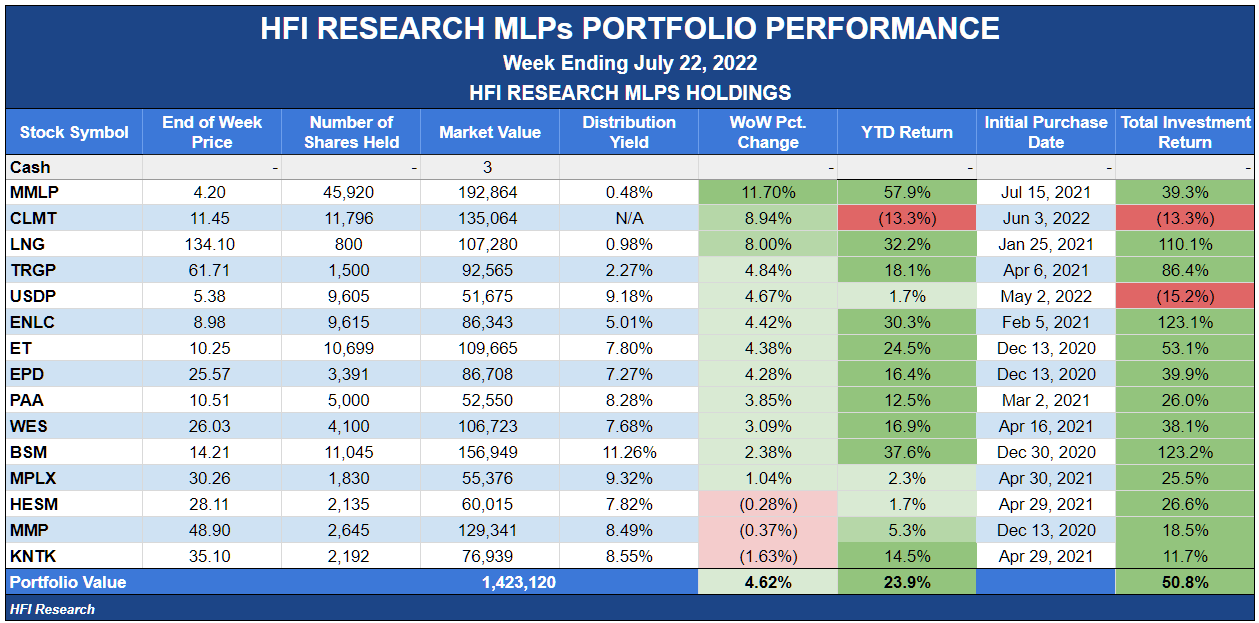

Weekly HFI Research MLPs Portfolio Recap

Our portfolio outperformed its benchmark, the Alerian MLP Index, by 1.9% during the week.

HFI Research

Martin Midstream Partners (MMLP) was our biggest gainer during the week after it blew away expectations. The results show that our investment thesis for MMLP is playing out as we had expected. We reviewed the quarter’s results here. The units popped 12% to $4.70 immediately after results were released but then cooled off to end the week at $4.20, which we believe is a very attractive price to buy MMLP units.

Calumet Specialty Products Partners (CLMT) was our second best performer on no news, though its units may have received a boost from BlackRock’s (BLK) acquisition of a renewable natural gas company, illustrating that the deal market for renewables companies remains active.

Our third biggest gainer, Cheniere Energy (LNG), surged as the global LNG market remained supply constrained. Cheniere’s other bullish news was that it signed a deal to supply PetroChina with LNG through 2050. Half the volumes in the deal are subject to Cheniere making a final investment decision to construct additional liquefaction capacity at its Corpus Christi LNG terminal beyond its Corpus Christi Stage 3, illustrating management’s intent to grow Cheniere’s production capacity further after Stage 3 is complete. This points to additional growth in the late-2020s and is bullish for Cheniere shares.

Our worst performer was Kinetik (KNTK), which was likely held back after it redeemed its onerous Series A preferred primarily by borrowing on its credit facility. The move made its credit metrics slightly worse, even though it was the right one for shareholders. Redeeming the preferreds eliminated restrictions pertaining to common dividends, saved by converting higher distribution rate to lower interest expense, avoids the future reset to a higher distribution rate, and eliminates the risk of future conversion to common units.

News of the Week

July 20. TC Energy’s (TRP) Keystone oil pipeline could return to full capacity this week if the company can secure the replacement parts to repair an electric substation. The 590,000 barrel per day pipeline has been operating at reduced capacity since July 17, when a transformer at one of the pipeline’s electric substations was damaged by vandals. TRP declared force majeure on the pipeline. The outage isn’t likely to have a material impact on TRP’s results. The impact from the outage is more likely to be seen in crude oil differentials between Western Canadian Select and WTI due to storage builds attributable to reduced egress from Western Canada. A significant decline in WCS could negatively impact Canadian E&Ps in the near term. If crude volumes are shifted from Keystone to Enbridge’s (ENB) Mainline and/or Express Pipeline network, ENB could see a benefit.

Capital Markets Activity

None.

HFI Research

Be the first to comment