AlbertPego

Mid-America Apartment Communities (NYSE:MAA) is a large US apartment equity REIT with around 102k apartment units focused on the Sunbelt. Its top markets mainly lie in Texas and Florida. The company is a member of the S&P 500, sports an A- credit rating from S&P and has proven its worth in 28 years since the IPO. MAA’s business model obviously is very stable and resistant to disruption, but the stock price still is more than 30% off highs, in stark contrast to MAA’s dividend action.

MAA’s Recent Dividend Increases

In May 2022, MAA increased its quarterly dividend by 14.9%, to $1.25 per share. A very large increase for an apartment REIT, but somewhat to be expected based off the strong rent growth beforehand. Surprisingly, MAA was not done for the year. In December 2022, they announced another dividend increase, this time by 12%, to $1.40 per share. In total, that works out to be a 28.7% increase YoY. At current prices, the dividend yield is around 3.6%.

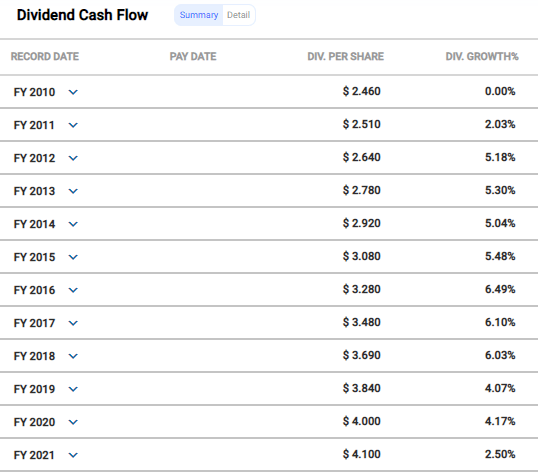

To show just how extraordinary this dividend increase is, here’s a comparison to MAA’s historical dividend increases:

MAA Dividend History (F.A.S.T. Graphs)

You can see that each of the two dividend increases this year on its own easily surpasses the largest increase in the last decade, which clocked in at 6.49%. The fact that there’s two of them is remarkable.

The dividend growth also compares very favorably to the dividend increases of the other large apartment REITs: AvalonBay Communities (AVB) hasn’t increased its dividend for years. Equity Residential (EQR) delivered a 3.7% raise in May 2022. The most recent increase by Essex Property Trust (ESS) in February 2022 was 5%. UDR‘s increase also came in at around 5%. Only Camden Property Trust (CPT) delivered a double-digit increase: 13.3% in February 2022. MAA obviously distinguishes itself as a clear leader here and shows a lot of confidence.

What has enabled such significant dividend growth? It is well known that 2022 was a generally very good year for landlords as stimulus benefits coupled with the reopening allowed for soaring rents. But there is also another important factor which is more specific to MAA: In contrast to many coastal markets (e.g., San Francisco) which have seen move-outs, the Sunbelt region in which MAA operates has benefitted from move-ins and population as well as job growth.

Are the dividend increases reckless? I don’t think so. The annualized dividend ($5.60) is covered by $8.45 of Core FFO (at least that’s the midpoint of MAA’s expectations). The payout on this basis is 66%, which certainly seems manageable even in times of rising interest rates. MAA’s guidance implies a 20.5% growth in Core FFO this year, which is not very far below the dividend growth in 2022 (and the dividend growth in FY2021 was very muted at 2.5%). Moreover, MAA has a record of 115 consecutive dividend payments and didn’t even reduce its payout during the great recession which hit residential real estate very hard.

It needs to be said, however, that at least the general rent growth trend is normalizing quickly. A double-digit average effective rent per unit growth, which MAA has achieved in 2022, is obviously not sustainable over a longer term in the apartment sector or, more generally, for residential properties. The impacts of high inflation, rising interest rates, recent strong multifamily construction which will then fade, moving activity, household formation, and other factors are difficult to weigh and time, but a return to low-mid single-digit rent growth, as common before 2020, can be assumed as the base case. This also means that MAA’s dividend increases will probably return to the old pattern of 3-6% in 2024 at the latest (and not stay above 20% as in 2022). In my opinion, none of these developments are worrisome; it will just be a return to normal growth in FFO/dividends coming from extremely high growth.

Comparison to other Apartment REITS

We have already seen that MAA increased its dividend in 2022 much more significantly than peers. How does it compare to its peers on other metrics? The companies selected for comparison are once again AvalonBay Communities, Camden Property Trust, Essex Property Trust, Equity Residential, and UDR. All of these companies operate in the apartment REIT sector, focus on high-quality properties and tenants, and are reasonably comparable to MAA.

| MAA | AVB | CPT | EQR | ESS | UDR | |

| Market Cap | $18.7B | $22.7B | $12.2B | $23.4B | $14.4B | $13.5B |

| P/FFO (fwd) | 18.8 | 16.6 | 17.1 | 17 | 14.8 | 16.7 |

| Div. Yield | 3.6% | 3.9% | 3.3% | 4.2% | 4.1% | 3.9% |

| 5y Div CAGR | 6.1% | 2.3% | 4.6% | 4.4% | 4.7% | 4.2% |

| Div. Growth | 12y | 0y | 1y | 1y | 28y | 12y |

| S&P Credit R. | A- | A- | A- | A- | BBB+ | BBB+ |

Source: Seeking Alpha, FASTGraphs

The table shows that, as expected, the companies do not differ wildly with respect to market cap and current dividend, but MAA has the highest 5-year dividend growth rate and the second-lowest current yield. All of the companies have a solid S&P credit rating at BBB+ or A-.

When seeing the numbers, it is important to consider that ESS, AVB and EQR mainly operate in coastal markets, with ESS focusing on California and Seattle in particular, which hasn’t helped their operations and rent growth recently. With respect to the displayed dividend growth streak, it is also notable that ESS was the only major apartment REIT to increase its dividend throughout the great recession, while MAA and AVB just maintained or even reduced (EQR, CPT, UDR) their payout.

The comparison also reveals that MAA is trading at a premium compared to the other apartment REITs. In my opinion, a premium is reasonable due to a) the attractive geographic region of MAA’s apartments, in particular compared to the much cheaper ESS, b) the overall quality of the company, in particular with respect to the dividend history, c) the recent strength in FFO growth and dividend increases.

This is not to say that the other apartment REITs are bad choices. In fact, around two years ago, I wrote bullish articles on ESS and AVB and I’m still happy with my picks which performed very well in the following months. Especially taking their lower valuation into account, they may well produce higher returns than MAA. In fact, right now, my personal ESS position is larger than my MAA position (and I have added to both recently). Yet, it needs to be said that MAA has outperformed operationally recently.

Future Expectations and Total Return Potential

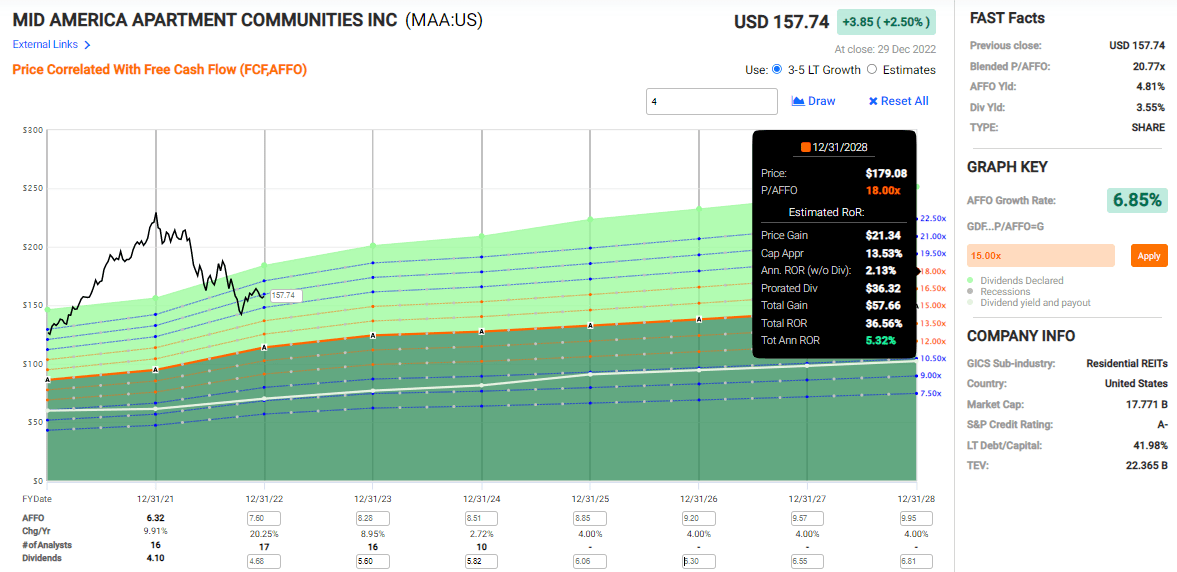

The following forecast (built in FASTGraphs using custom settings) uses the following assumptions:

- AFFO growth in 2023 and 2024 as expected by analyst consensus

- Thereafter, 4% CAGR AFFO growth (below historical growth rates and likely conservative)

- Dividend imputed as known, then dividend growth CAGR of 4% (in line with assumed AFFO growth and historical dividend growth)

- 18 P/AFFO exit multiple (below historical valuation and likely conservative)

Total Return Expectations (Copyright © 2022, F.A.S.T. Graphs™ – All Rights Reserved )

Source: Copyright © 2022, F.A.S.T. Graphs™ – All Rights Reserved

Under these quite conservative but reasonable assumptions, MAA is poised to deliver a 5.3% total return p.a., mainly through the dividend. The currently relatively high valuation reduces the return expectations. Instead assuming a more aggressive 6% AFFO/dividend growth rate and 21x exit multiple leads to 9% total returns p.a.

Conclusion

Overall, it can be concluded that MAA’s dividend raises this year show a lot of confidence. Based on the available evidence, I think that MAA will continue to perform very well operationally and raise its dividend. However, the size of the recent increases cannot perpetuate into the future and a mid-single-digit dividend growth rate is much more probable. This and its stable business model makes MAA a solid investment for the future, but further >20% dividend increases and outsized returns are unlikely. Depending on the investor’s risk appetite, this may still make MAA an attractive opportunity in today’s turbulent markets. My rating thus is ‘Neutral’ or ‘Buy’ depending on the individual preferences.

Be the first to comment