Daniel Besic

Main Thesis & Background

The purpose of this article is to evaluate Mid-America Apartment Communities Inc. (NYSE:NYSE:MAA) as an investment option. The company is a “real estate investment trust that focuses on the acquisition, selective development, redevelopment, and management of multifamily homes throughout the Southeast, Southwest, and Mid-Atlantic regions of the United States”.

This has been a REIT I cover regularly, and actually recommended about four months ago. In hindsight, that idea worked out very nicely for a while. Two months after publication the gain was in double-digits. At that point, I suggested caution:

Outlook Shift (Seeking Alpha)

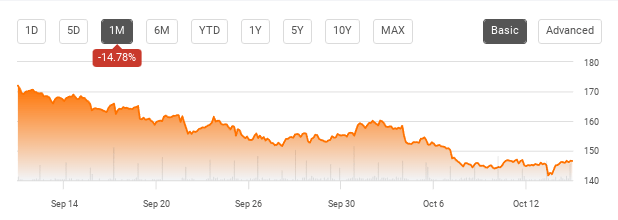

Simply, the performance over the last month vindicates that change of heart. The 1-month chart looks very nasty by comparison:

1-Month Performance (Seeking Alpha)

Given that the stock has hit correction territory in the short-term, I thought it was time to do another review. After some thought, I believe a buy case has opened up again for MAA. I will explain my reasoning below.

Rents Are Up, Be The Landlord

To begin, I want to touch on the primary reason I like MAA, and rental apartment plays in general at the moment. This has to do with rising rents. The cost of housing has gone up across the board, grabbing a larger share of America’s disposable income. It probably comes as no surprise to readers that cost of shelter has been going up, but the pace of this rise has been historic:

Cost of Shelter (Yahoo Finance)

When I see metrics like this my instinct is always – how can I profit from it?

Certainly, owning a home helps with the wealth effect, so I’m covered there. Another way would be to be a landlord – in that way benefiting from rising rents by being able to charge more. But I don’t want to directly do that. It isn’t my wheelhouse nor my passion. So – what is the next best thing? Own a stock in a management team that does have that expertise.

This leads me to MAA, and apartment investment plays in general. Why not buy this exposure and capitalize on a sector that has clearly been able to pass on higher costs (rents) through to their end users.

I view this as particularly relevant right now because inflation is top of mind of households and investors alike. This means everyone is thinking “how can I beat this?” (or at least how can I manage it!). But there are a number of different factors influencing inflation and a number of different ways to play it.

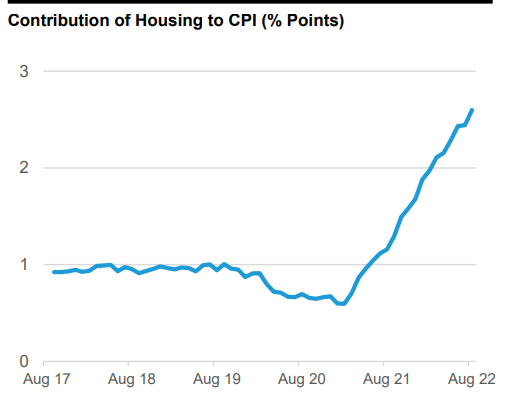

With this in mind, why do I feel apartment plays like MAA are relevant right now? This stems from the fact that housing as a whole is becoming a bigger and bigger issue with respect to inflation. Since last year, the share of shelter costs as a percentage of total inflation has been rising. Currently, it is well above levels we have seen in the past five years:

Housing Costs Becoming More Important (U.S. Bureau of Economic Analysis)

The takeaway for me is that for investors who are looking to beat inflation, they should be looking at what the biggest drivers of inflation are right now. Energy, specifically oil and gas, are certainly drivers, and that is a sector I have been suggesting for a while. Beyond that, rising shelter costs are becoming an increasingly important role in overall CPI figures. This means this is as relevant as an investment idea as it ever has been, and I believe getting in now before more investors pick up on that fact is a smart move.

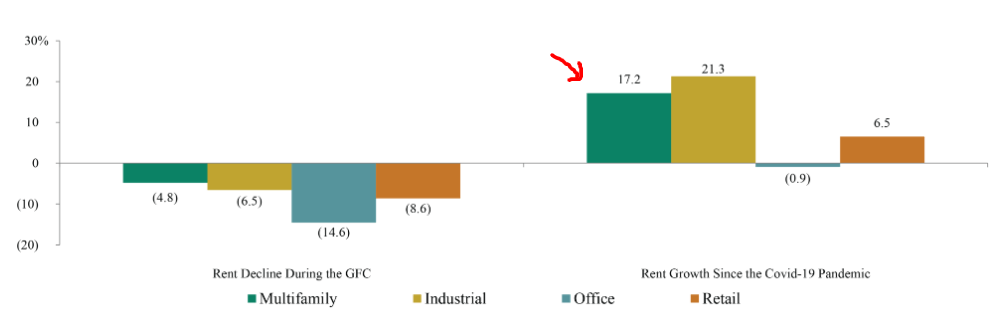

Rents In General Rising More Than Other Property Sectors

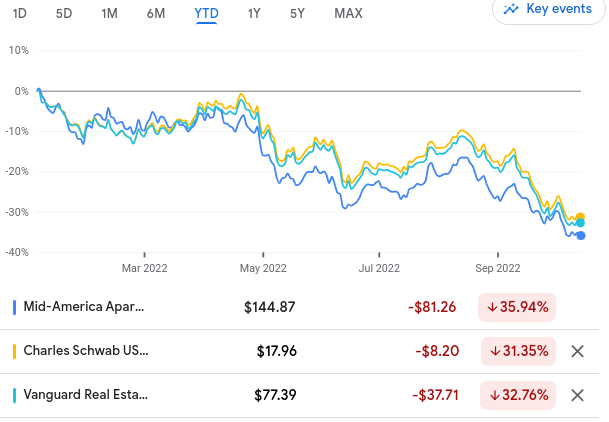

Expanding on the discussion above, I recognize that investors have a number of choices when it comes to “REITs”. Generally speaking this is an area that often performs well during inflationary periods because rising land/property values helps to act as a buffer against overall inflation. Of course, this is counterbalanced to a degree during rate hike cycles. When the Fed raises interest rates, as it is right now, that often acts as a headwind for income-producing investments. The idea is that investors can earn higher yields elsewhere, so the income derived from higher-yielding sectors like Real Estate and Utilities often become less attractive as a result. For support, we should consider that is probably why Real Estate is down this year, including MAA:

YTD Performance (MAA; SCHH;VNQ) (Google Finance)

It is in this light that I urge readers to be very selective with where they put their Real Estate dollars at the moment. This is an area that has a number of different sub-sectors that have been impacted by the pandemic differently. For example, retail and office space have both been hit very hard by a stay-at-home, work-from-home, shop-from-home culture. While that dynamic has been shifting back to normalcy, this has been a slow road and one that will probably not get back to the “normal” we knew before Covid-19 started. By contrast, rents for multi-family living and industrial warehouse spaces have been rising by leaps and bounds. There is a substantial divergence among these sub-sectors within the broader Real Estate arena:

Rent Growth (By Sector) (Oak Tree Capital)

The conclusion I draw here is that Real Estate investors need to be selective. This means focusing on the areas with the best growth prospects, such as rental apartments/homes and industrial buildings. MAA falls directly in to this bucket, helping to support my buy rating on the stock.

I View The Dividend Positively

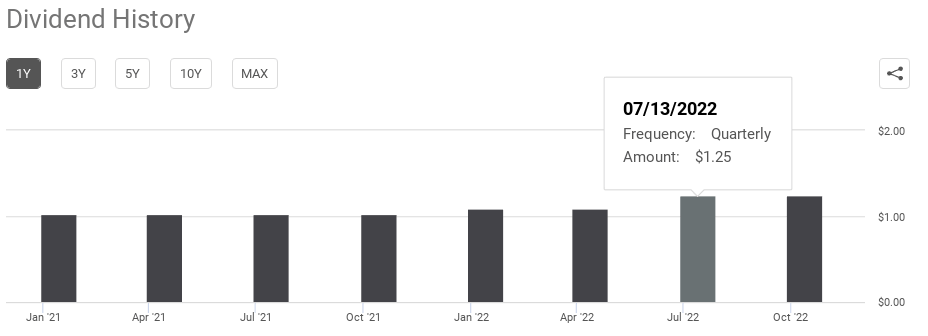

I will now dig in to MAA individually. A top-line reason I continue to like building positions here has to do with the dividend. The upside to the stock’s massive decline in 2022 has been that the yield has shot back up near the 3.5% level. This gets me a lot more interested than last year when it fell below the 3% marker.

Of note, the rise in yield has not just been solely because of a falling share price (which isn’t exactly a good thing!). In July of this year, MAA began paying $1.25/share as a quarterly dividend, up $.16/share from the prior level:

MAA’s Dividend History (Seeking Alpha)

The simple fact is I view this positively. MAA has a relatively high current yield compared to the broader market and the company has shown a willingness to raise it over time – including very recently. I see this as another supporting factor for owning this REIT.

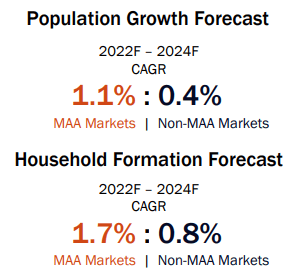

Geographic Exposure Remains A Tailwind

Another key reason for liking MAA has to do with where its properties are located. I won’t go in to a ton of detail here because this is something I have emphasized over the years of covering the company. But the fact is it bears repeating again because it continues to be relevant.

The reality is MAA is located primarily in the Mid-Atlantic, Southeast, and Southwest regions of the country. These are fast growing areas for a number of reasons – climate, favorable taxes, job opportunities, etc. In particular these regions are increasingly popular with white-collar, younger professionals. This is a key demographic for companies offering luxury-style apartments that cater to those who can afford above-average rents. To put this dynamic in perspective, consider that the markets MAA serve are growing markedly faster than the national average:

Population Forecasts (Data from Moody’s)

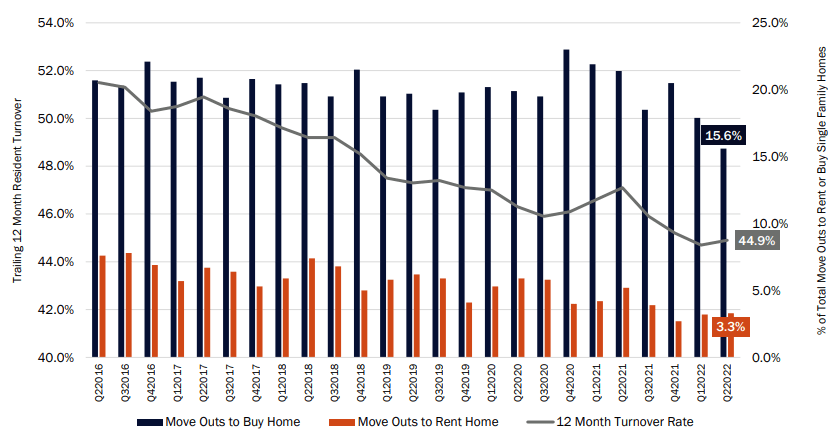

The takeaway for me is that if there is stronger growth, it supports higher occupancy rates and, by extension, the opportunity for higher rents. This has been playing out across the country and fits in to MAA’s hands. In fact, it clearly illustrates why the turnover rate at MAA-owned properties has been falling consistently over time. It has recently touched a multi-year low:

Turnover Rate at MAA Properties (National average) (MAA Investor Relations)

With growing populations and an already low (historically speaking) turnover rate, MAA is in a good position. This tells me higher rents will be offered and paid, boding well for investors in the company.

Rising Borrowing Costs Not An Immediate Concern

As with any investment, readers should take care to evaluate the risks. I already noted one in particular, which is that rising interest rates can take a toll on higher-yielding plays. This has no doubt been weighing on MAA’s performance of late, as suggested by the sharp decline over the past month.

Beyond just pressuring share prices, rising interest rates pose other challenges. For companies with a lot of debt, or who plan on raising debt in the near term, higher rates means higher borrowing costs. This pressures earnings and any forward outlook, as well as the multiple investors are willing to pay for that exposure.

This is relevant to MAA because the company does have over $4.5 billion of current debt according to the company’s recent financial report. This could be a headwind for a couple reasons. One, if the debt was issued at a floating interest rate, the rate would reset at the prevailing higher rates. This means borrowing costs would increase. Two, if the debt is going to mature soon and the company will have to raise new debt to pay off those obligations, they would again be forced to raise cash in a higher rate environment. Either of these scenarios will weigh on overall company performance. This is true for MAA and every single company in the S&P 500. So investors need to carefully consider this risk.

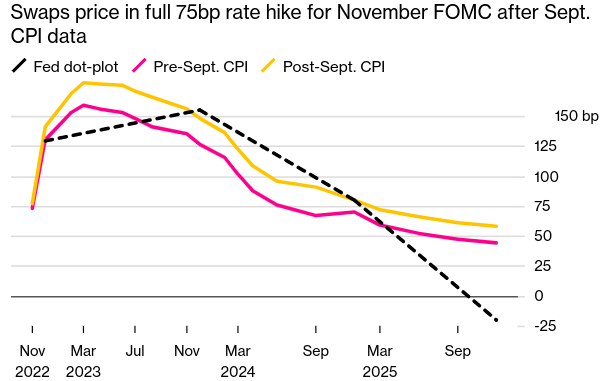

The good news is this risk is muted with MAA. Unlike other companies that are less financially secure, MAA has issued its debt with fixed interest rates. This means that rate is locked in through maturity, and management does not have to worry about the rate resetting. This is critical because rates have been going up consistently in 2022, and the Fed’s forward path suggests this theme will remain in place in 2023 as well:

Fed Dot-Plot (CME Group)

However, even if debt is fixed, if it is going to mature soon it doesn’t offer a lot of protection. Unless the company no longer needs to raise cash they will be at the mercy of current conditions.

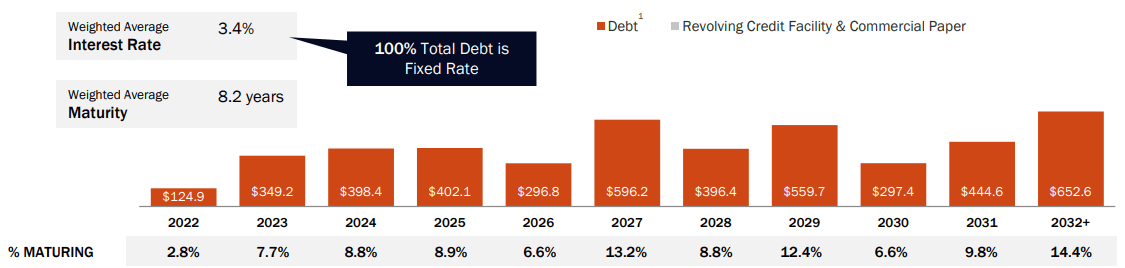

Fortunately, the story again here is positive for MAA. In addition to have fixed-rate obligations the company also has a well-laddered debt profile. Maturities range from this year through past 2032, with the majority of this debt maturing well in to the future:

MAA’s Debt Maturity Profile (MAA Investor Relations)

As you can see, MAA is not at risk of having to contend with floating-rate loans that reset at much higher rates, nor is it going to have to replace a large chunk of maturing debt in the short-term. This is another supporting factor on why I favor MAA – it is run by a disciplined management team. This helps set the company up in a differentiating way from other companies that rely more on floating-rate loans and/or who have a shorter maturity profile.

Bottom-line

MAA had been overpriced for a long time but I believe that climate is over. The company is well positioned to benefit from geographical trends in the U.S., rising rents, and can manage higher interest rates given its debt structure. I would use the recent sell-off as a buying opportunity and I am once again placing a “buy” rating on this stock. In my view, readers should give the idea some consideration at this time.

Be the first to comment