SAUL LOEB/AFP via Getty Images

Microsoft (NASDAQ:MSFT) announced its Q2 earnings on Tuesday and initially the stock popped 5% as the company’s cloud business was particularly strong. However, Microsoft gave guidance during the conference call and shortly after announcing Q3 revenue guidance shares of Microsoft did a U-turn.

Microsoft Q3 Revenue Guidance

- Productivity and Business Processes: $16.9B – $17.2B

- Intelligent Cloud: $21.7B – $22B

- Personal Computing: $11.9 – $12.3B

- Revenue Guidance Totals: $50.5B – $51.5B

Source: Microsoft Q3 Outlook Slides

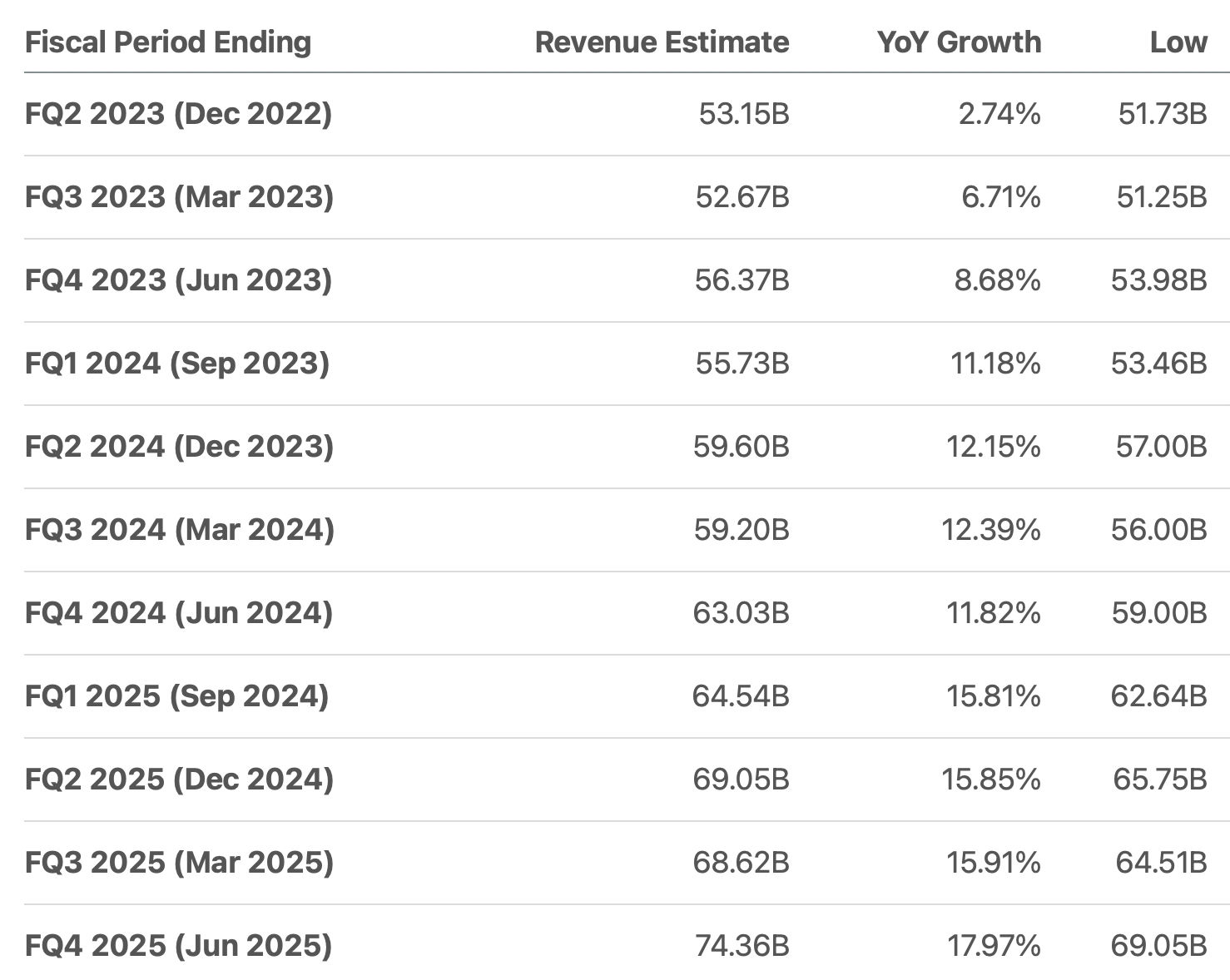

Q3 Wall Street estimates for Microsoft ranged from $51.25B on the low end to $57.33B on the high end – with a consensus of $52.67B (6.7% growth) for the upcoming quarter.

Keep in mind, the $52.67B Q3 consensus has steadily been revised down by analysts over the past six months, meaning Microsoft’s revenue bar was already lowered – and the company is guiding underneath it.

As a long term focused investor, I’m not overly concerned about the next few quarters where it appears Microsoft will miss the mark from a revenue perspective.

However, start stretching Microsoft’s revenue estimates out into fiscal Q1 (September 2023) and beyond, Wall Street is expecting revenue growth to reaccelerate back into the low double digits.

Microsoft Revenue Estimates (Seeking Alpha)

It’s likely analysts are expecting the Activision Blizzard (ATVI) deal to close by Q4/Q1 which would add anywhere between $1.7B – $2.2B+ to Microsoft’s quarterly revenues based on Activision’s recent performance.

Yes, if the Activision deal closes – Microsoft can bolt on enough revenue to reaccelerate to low double digit revenue growth.

That obviously comes at a price.

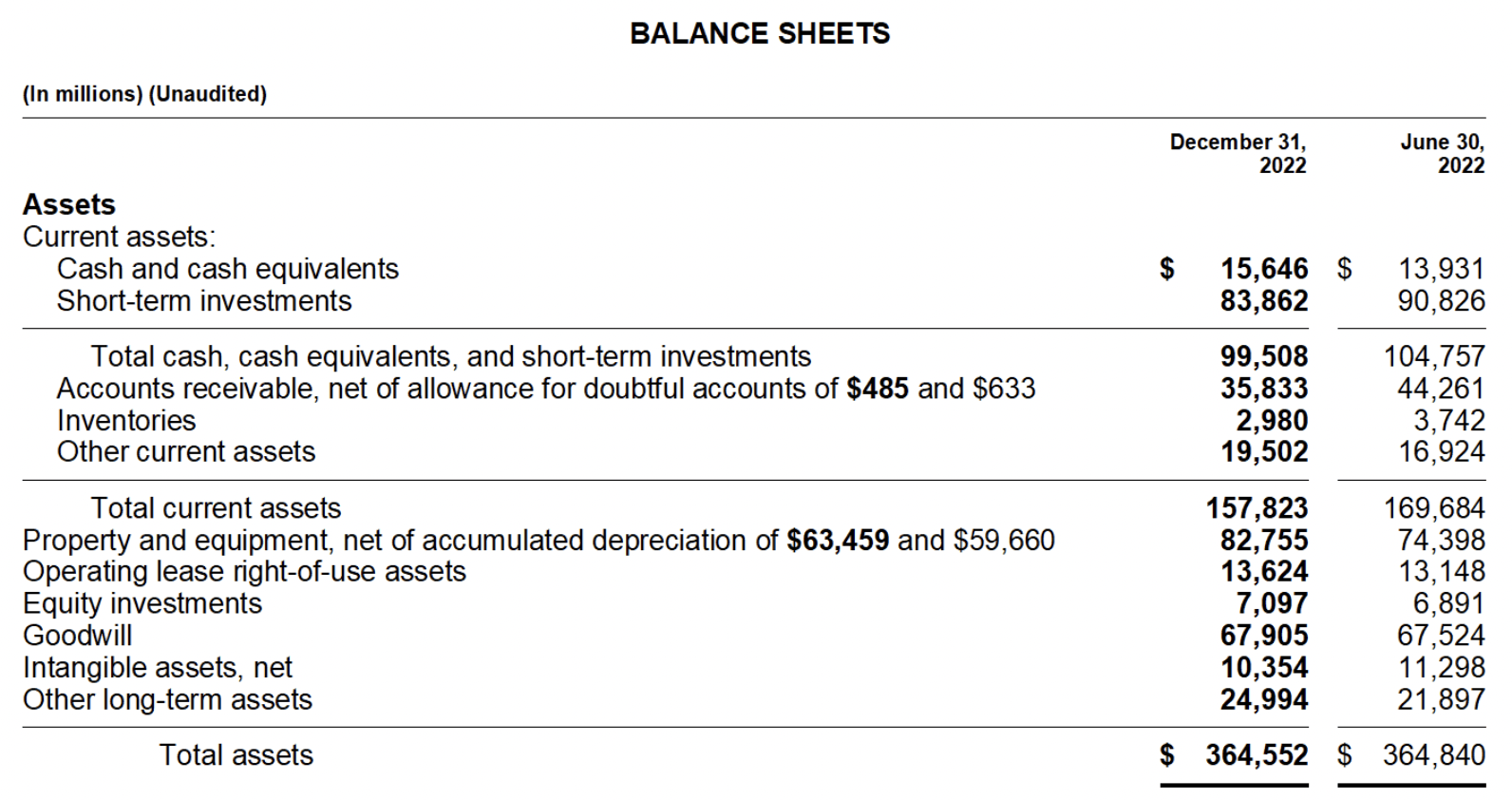

Microsoft Q2 Balance Sheet (Microsoft Q2 10-Q)

The company agreed to an all-cash $69B purchase price and Microsoft has $99B in cash and another $35B+ in receivables. Obviously Microsoft doesn’t need to necessarily come up with $69B all from its cash pile, but I’m assuming it will.

The risk for investors is if Microsoft peels off $69B from the cash pile and things get materially worse for Microsoft’s core business – then the road to outperformance might be longer than anticipated.

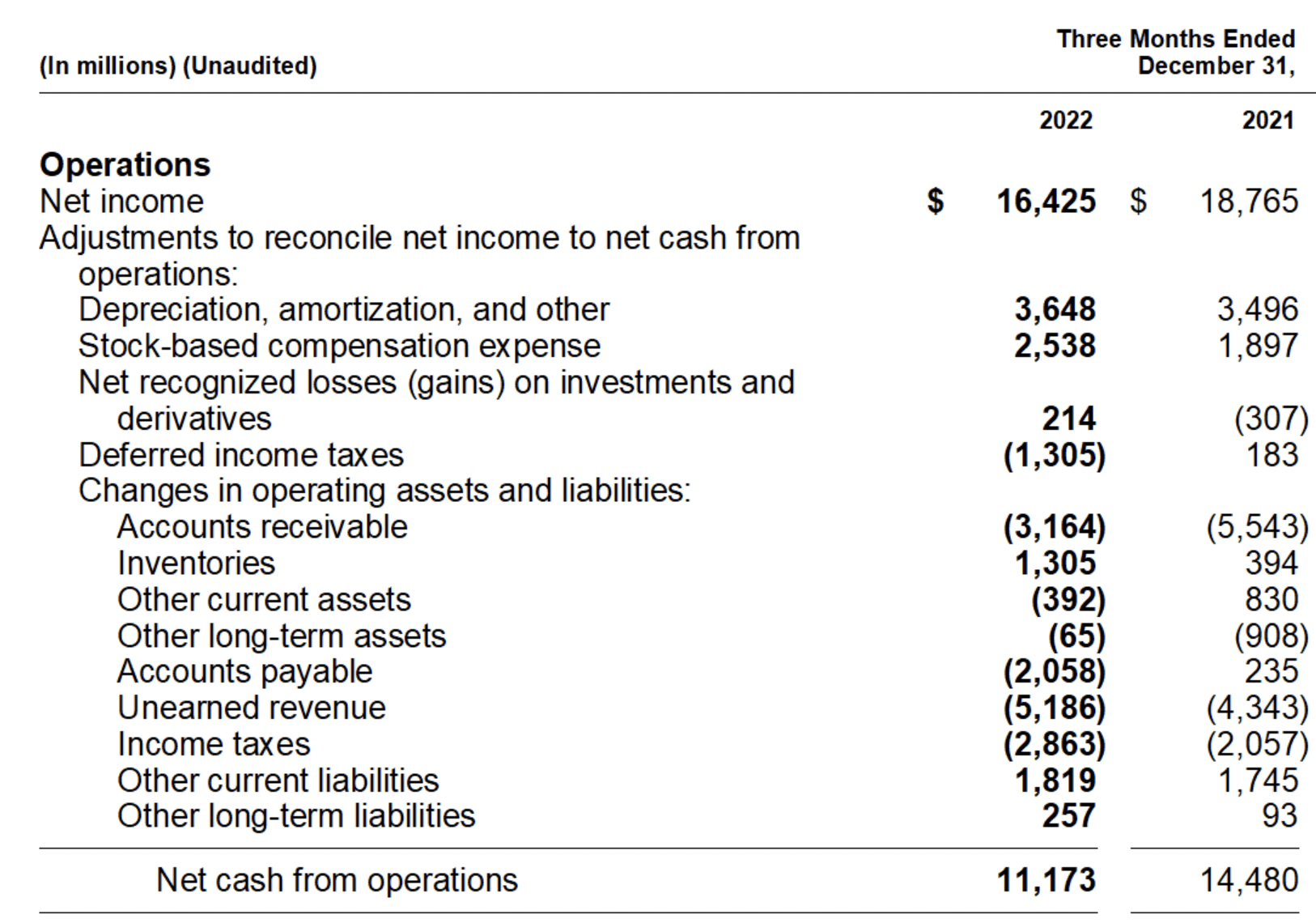

Microsoft Q2 Cash Flow (Microsoft Q2 10-Q)

With revenues stalling out, Microsoft is printing less money to the net income side. Yes, the company has reacted by laying off 10,000 employees – that should improve operating/net profits in upcoming quarters to a certain degree. However, with just $11.2B in operating cash flow in Q2, this essentially only covers the share buy-backs, dividends and debt payments.

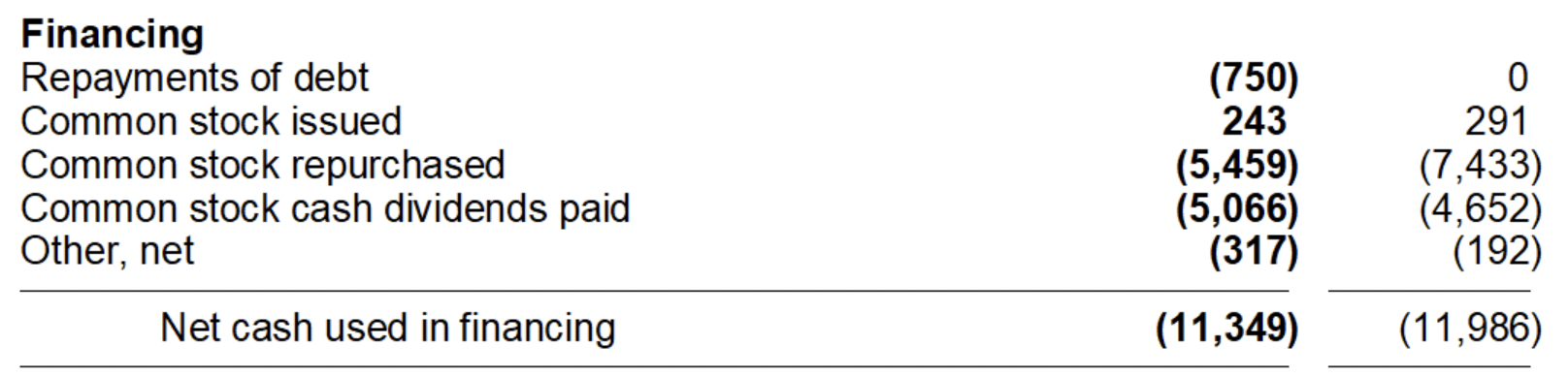

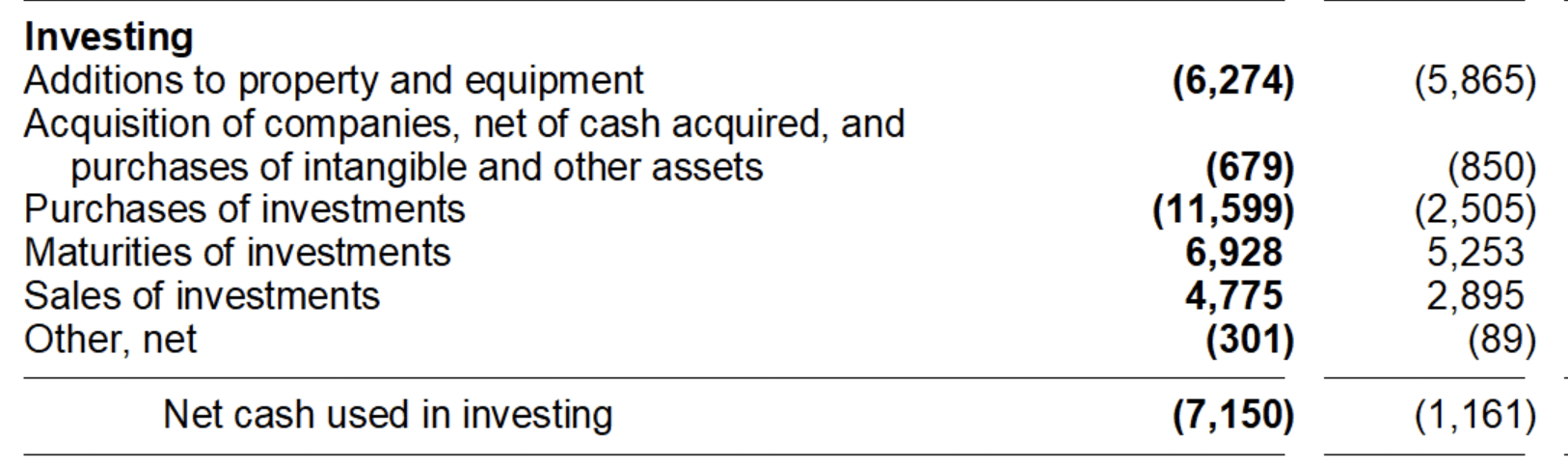

Microsoft Q2 Financing Activities (Microsoft Q2 10-Q) Microsoft Q2 Investing (Microsoft Q2 10-Q)

Bolt on another $6.27B in property, plant & equipment and $11.6B in investment purchases – Microsoft burned through nearly $7.3B in cash in the quarter.

No one is going to sound any alarm bells as the company’s cash pile, even after subtracting $69B for Activision, is unusually large. However, if the company struggles to either reaccelerate revenues, and/or doesn’t cut expenses enough, it could create some concerns among investors used to a larger cash pile at Microsoft.

The Opportunity

Herein lies the opportunity with Microsoft. Over the next 12 months things are likely not going to be smooth sailing. Even if the Activision deal closes, revenue estimates are still likely generous as the company heads into calendar 2024. Management didn’t particularly sound rosy about the macro economy on the Q2 conference call, and even guided to slowing Cloud/Azure growth in Q3.

The good news is everyone is facing the same challenges. In a roaring bull-market OpenAI (the parent company of ChatGPT) possibly goes public or has a line out the door of investors looking to throw money at it.

The rumor is for an additional $10B investment into OpenAI Microsoft gets 75% of OpenAI’s profits until the $10B is recouped, then it gets 49% of the company. Sounds like a deal Kevin O’Leary makes to a fledgling entrepreneur on Shark Tank, not for one of the hottest startup companies on the planet.

The longer the macro economy remains weak, the more of these deals materialize for Microsoft.

At 25x FWD earnings, and 8-9x forward sales, valuation wise, Microsoft isn’t wildly cheap. Historically, the company has traded comfortably higher than this. However with growth likely stalling, many investors will try to argue the stock is too expensive in the short term.

Longer term focused investors that believe we’re on the edge of a new computing revolution with AI would be wise to accumulate Microsoft. Azure wasn’t even a product at Microsoft until it was announced in 2008. It’s likely AI’s impact on Microsoft’s financials materialize even faster.

Conclusions

Microsoft’s Q2 earnings show the company isn’t bullet proof. Operating profits, net income and operating cash flows all declined. Short term investors are going to panic and point to valuation metrics taught in finance 101 classes.

Long term investors are going to realize Microsoft is perfectly positioned to capitalize on the next computing breakthrough. Reading about the advancements in AI reminds me of reading about cloud computing in the early 2000’s and personal computers in the 1990’s.

Given the macro environment and the significant server costs/infrastructure required to run AI powered solutions, Microsoft is well positioned to partner and potentially acquire many startups over the next few years. This should ultimately reaccelerate revenues for Microsoft and creates a unique opportunity for investors to accumulate before they materialize.

Be the first to comment