JOSEP LAGO/AFP via Getty Images![]()

What’s Happening?

Microsoft (NASDAQ:MSFT) reported its fiscal second-quarter results after the close of regular trading today, Tuesday, January 24th.

Analysts were expecting earnings of $2.30 per share, adjusted, and revenue of $52.96 billion. Q2 Non-GAAP EPS of $2.32 beat by $0.02, so that worked out.

Growth was expected to come in at just 2.3% year over year, which would have been the weakest expansion for Microsoft in any period since 2016. Unfortunately for active investors, it was a bit lower, with revenue coming in at 1.9%. This was due, in part, to flagging PC sales as reflected in More Personal Computing. It’s what I call a known drag.

With that out of the way, in this article we’ll dig into job cuts, Azure a bit, but also what some analysts are thinking going forward. I have other things to say above and beyond, including the impact of OpenAI.

Recent Past

MSFT is facing concerns across the board. CEO Satya Nadella announced 10,000 job cuts last week, noting that clients in every industry around the world have taken a more cautious approach due to recession concerns.

Google (GOOGL) (GOOG) has laid off 12,000 employees, Salesforce (CRM) has laid off 8,000, MSFT has laid off 10,000, and Amazon (AMZN) has laid off 18,000. These cuts come on top of earlier layoffs at Snap (SNAP), which laid off 1,300 in August, and Meta (META), which laid off 11,000 in November.

In other words, the technology sector got ahead of itself. Like the rest, MSFT has been caught out over their skis. Dan Ives says:

The cuts come on the heels of unsustainably rapid hiring over the last five years, Ives said. “Now, the clock’s struck midnight for hyper-growth, [and] you’re seeing tech CEOs rip the Band-Aid off.”

To me, this says less about a coming recession or macro conditions, and more that these companies did a poor job forecasting growth. They expected too much of a good thing, and for the extra high growth recent past to continue into the future. The pandemic screwed them all up, including MSFT.

For quick reference, here are the layoffs in terms of headcount impact:

- META 13%

- CRM 10%

- GOOGL 6.4%

- MSFT 4.5%

- AMZN 1.5%

In terms of a financial impact:

In addition, the company will take a $1.2 billion charge in its second fiscal quarter when it releases its full financial results next week. Nadella told employees that the charge is “related to severance costs, changes to our hardware portfolio, and the cost of lease consolidation as we create higher density across our workspaces.”

So, there is a hit.

How About Azure And All The Rest?

Microsoft’s Azure public cloud, a key component of the company’s Intelligent Cloud unit, is facing challenges with growth. CEO Satya Nadella recently stated that “we’re now seeing them optimize their digital spend to do more with less,” highlighting the cautious approach clients are taking in light of the economic uncertainty.

Additionally, the company’s Windows business, which is housed within the More Personal Computing unit, is also facing a decline in the PC market. As Kitagawa points out:

“PC demand among enterprises began declining in the third quarter of 2022, but the market has now shifted from softness to deterioration. Enterprise buyers are extending PC lifecycles and delaying purchases, meaning the business market will likely not return to growth until 2024.”

In addition, the Productivity and Business Processes unit, which contains the Microsoft 365 productivity suite, may see slower growth in seats purchased by business customers.

Given the results, analysts have lowered their guidance, like Brent Hill:

“We are lowering our FY23 growth from 7.1% to 4.8% year over year (10%+ year over year constant currency guidance rescinded) as macroeconomy continues to weigh on results with tough comparables and lowest commercial bookings growth in five years…”

Of course, there’s more here. In other words, it’s not the current results that concern everyone. Instead, it’s the forward guidance, especially the deceleration with Azure. Sure, growth is still high, but it’s slowing.

None of this is catastrophic. As I write this, MSFT is down less than $2, and therefore, down less than 1%. The stock has brushed off the bad news.

The OpenAI Wild Card

MSFT announced that it will be investing $10 billion in OpenAI, a company known for its cutting-edge artificial intelligence tools. One such tool, ChatGPT, has caused quite a stir on the internet since its introduction in November. The program amassed over a million users within days and has sparked a renewed conversation about the role of AI in the workplace.

This is not the first time MSFT has invested in OpenAI as the company invested $1 billion in 2019 and again in 2021. This new investment will give Microsoft an edge in the race to dominate the rapidly growing AI industry, as they compete against other tech giants such as GOOGL, AMZN, and META. Clearly, this move is a sign of the importance Microsoft is placing on AI technology and its potential to shape the future.

Here’s some thinking about the integration plans:

Microsoft has said it plans to use ChatGBT in all of its products. However, it’s hard for investors not to consider the particular implications for Microsoft’s search engine, Bing.

Bing is the number two search engine behind Google. But with a single-digit market share, Bing is a distant second to Google, which has about 70% market share.

[…]

Therefore, if such integration were to happen, it would make Bing an even more formidable competitor to Alphabet’s dominance in search. If the rumors are true, Alphabet Inc., the parent company of Google, is keenly aware of the threat this poses.

This is what’s driving GOOGL’s “Code Red” and demonstration update. Indeed, this is happening very quickly:

Google plans to unveil more than 20 new products and demo a version of Google Search with AI chatbot features this year, The Times reported, citing a presentation it had seen and two people familiar with the plans.

Ultimately, this is a growth driver. What remains to be seen is how much of an ROI will MSFT get from the OpenAI investment. If nothing else, it puts GOOGL on watch, which gives MSFT some breathing room.

If nothing else, Satya Nadella is very optimistic, especially the integration of OpenAI and Azure:

So, that’s sort of, I think core Azure itself is being transformed for the core infrastructure business, it’s being transformed. And so you can see us with data beyond Azure OpenAI services even, think about what Synapse plus OpenAI APIs can do.

Some Quick Charts

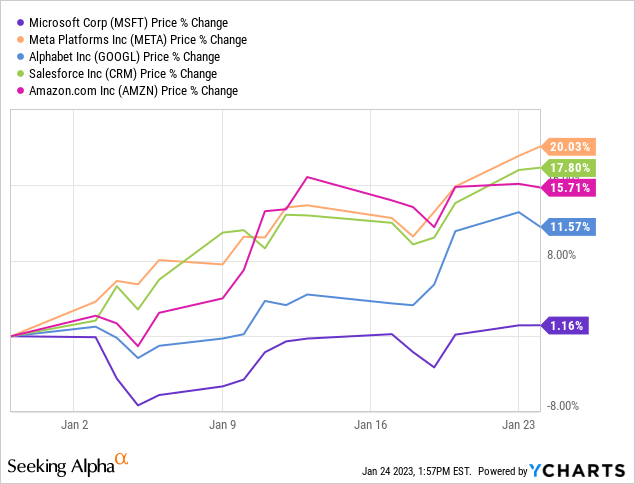

Here’s how MSFT compares to some other tech companies. You may, or may not consider these peers. It kind of depends on what aspect of MSFT you’re considering. In any event:

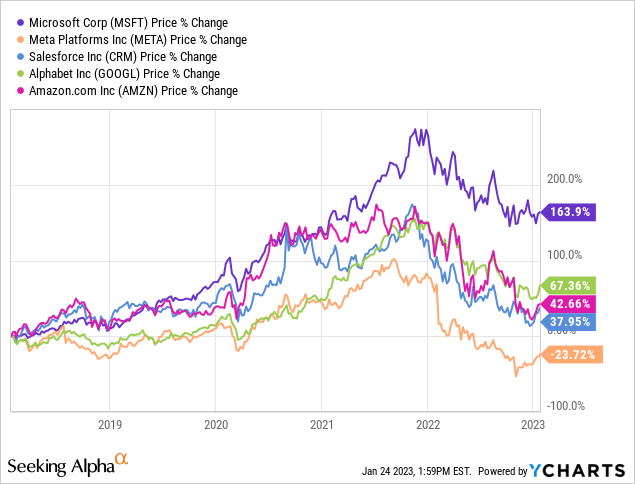

That’s interesting to me because while all of these companies are up, MSFT is lagging behind this year. But, if we zoom out:

The story here is pretty simple. MSFT has done better over the last 3-year period and 5-year period. Further, MSFT just got ahead of these peers sooner, and now they are catching up a bit. We can attribute this to macro factors, or risk appetite, or whatever else. But, it comes down to timing and perspective in the market. Let’s simply call this sentiment. All-in-all, MSFT has done well in the medium term.

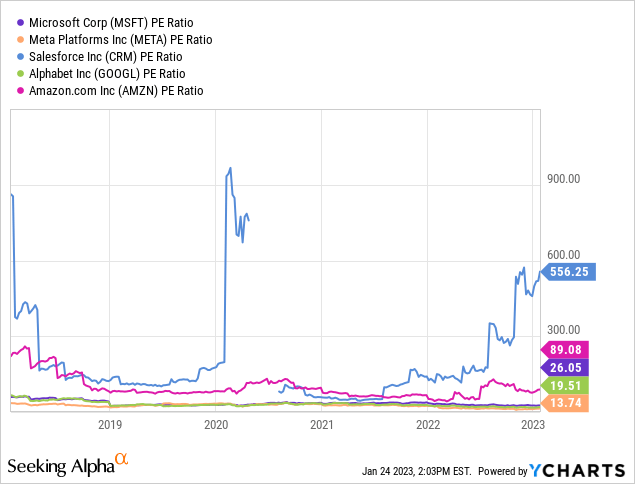

Now, while this is terribly misused metric, and it’s not entirely appropriate, I still think the P/E ratio changes over time are instructive. I’ll merely zoom right out to the 5-year view to save us all sometime:

As most investors already know, the CRM P/E is kind of broken. They are a dominant company, still growing strongly. Roughly speaking, they neglect profit for the sake of that growth. And, AMZN is very similar. All the “profits” are poured back into growth. So, we can mostly ignore CRM and AMZN here, for this exercise.

Per the chart above, I see MSFT at 26 which makes sense given their strength right now. This also explains why the price hasn’t moved much this year. At the same time, GOOGL and META are catching up, as I said before.

Looking at all this from outer space, this quick view tells me that MSFT is probably priced about right, whereas GOOGL and META are potentially undervalued a bit. Note that this is only in relation to peers. Therefore, further fundamental analysis would definitely be required to issue a strong call to Hold or Buy here for these stocks.

Wrap Up

Adding it up, I see MSFT as a Hold. I’m not invested in MSFT but I’d be interested if the P/E fell down below 20. I don’t see that happening in the near term, but hey, you never know.

MSFT is on my watchlist. While I’m not keen on MSFT’s starting dividend, which is about 1.1%, I’m loving MSFT’s 15-year dividend growth rate which is over 13%. With the payout ratio around 25-30%, there’s room for a lot more growth there too. So, as a dividend growth investment, it could be a win.

Wrapping it up, Hold if own, watch if you don’t and Buy if you want a safe dividend and high dividend growth. But, generally speaking, it’s a Hold.

Be the first to comment