NoDerog

Q2 recap and thesis

Microsoft Corporation (NASDAQ:MSFT) just announced its FY 2023 Q2 earnings report (“ER”) on Tuesday. By this time, I am sure most investors have already fully digested the results in detail. Thus, in this article, I will not go into a full review of the ER. Instead, I will only highlight a few items briefly that I think are important for the long term, and then I will move on to discuss my outlook beyond the immediate Q2 results.

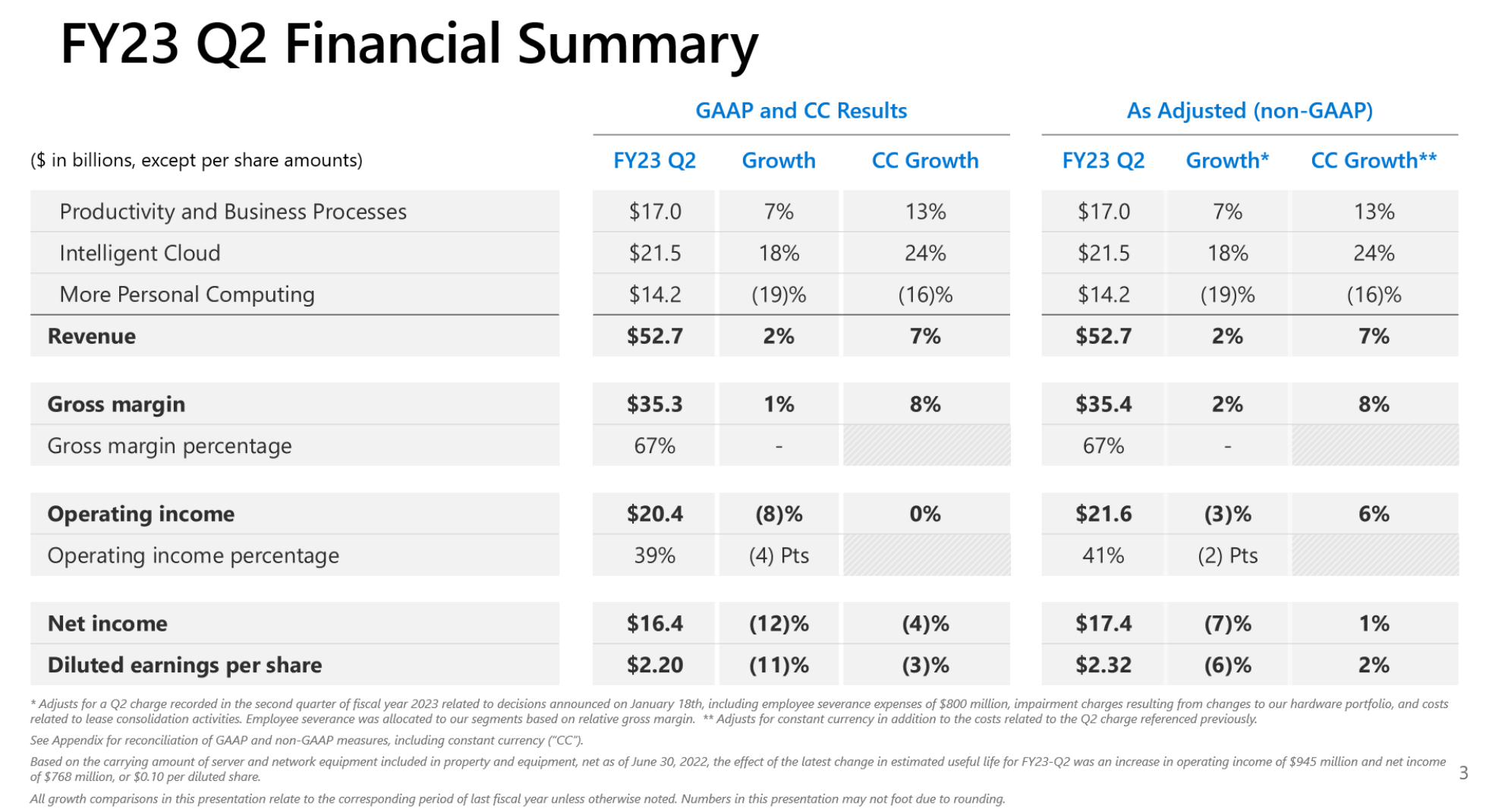

Overall, I see the Microsoft ER as another solid quarter. The results came in slightly missing analysts’ expectations on revenue ($52.7 billion vs. $52.9 billion consensus estimates), but ahead on EPS (adjusted EPS: $2.32 vs. $2.30 consensus estimates). The following segment results are more telling in my view:

- Its cash cow business, the Productivity and Business Processes segment, kept enjoying healthy growth. In particular, the Microsoft 365 subscription base grew for another quarter to exceed 63 million members. It’s a highly lucrative and repeatable revenue source.

- On the negative side, the More Personal Computing segment suffered a setback. Windows OEM revenue decreased by 39% during the past quarter, and its devices revenue decreased by 39%. In my mind, the key drivers for such a setback involved the global PC demand softening and renormalization. The COVID breakout in 2020 unexpectedly triggered a wave of new device purchases and upgrades. Now, with the wave subsiding, the demand is going through a renormalization and I view this setback only as temporary.

- Finally, the intelligent cloud kept its growth momentum. Admittedly, its cloud business growth slowed in Q2. The Intelligent Cloud segment grew 18% and Azure services grew 31%, compared to a YOY growth rate of 26% and 46%, respectively, in the previous quarter. However, I view its current growth rate as already sufficient. The cloud segment represents a new wave of computing as CEO Satya Nadella mentioned in the ER below (the quote is abridged, and the emphasis was added by me).

MSFT CEO Satya Nadella: The next major wave of computing is being born, as the Microsoft Cloud turns the world’s most advanced AI models into a new computing platform. We are committed to helping our customers use our platforms and tools to do more with less today and innovate for the future in the new era of AI.

Source: MSFT Q2 ER

Overall, I view the business as an excellent combination of a mature and reliable cash cow segment and a few high-growth segments. I won’t suggest investors worry about its quarterly fluctuations in terms of QoQ or YoY growth rates. I view it as a textbook Buffett-type perpetual compounder and encourage you to take the same long-term view also.

The only reservation I have about Microsoft Corporation stock has been its high valuation. I have been writing a series of articles reminding readers of the danger of buying a high-quarter business at a high price. To wit, I have been cautioning readers about its valuation risk in my first article at price levels around ~$290 (back in Aug 2021) up till very recently.

And now, I see the valuation to be much more reasonable after the price corrections since then. Under current conditions, I begin to see its price approaching its fair valuation. And next, I will show this using a very simple discounted cashflow method using the treasury rates as discount rates, as promoted by Warren Buffett.

MSFT deserves treasury rates as discount rates

A key wisdom from Buffett is that we should not be afraid to apply risk-free interest rates as the discount rate for proven compounders like MSFT. For example, in his 996 BRK annual letter, he mentioned (slighted abridged with emphases added by me):

… But we believe in using a government bond-type interest rate. We believe in trying to stick with businesses where we think we can see the future reasonably well – you never see it perfectly, obviously – but where we think we have a reasonable handle on it.

If you say I’m going to stick an extra 6 percent in on the interest rate to allow for the fact – I tend to think that’s kind of nonsense. I mean, it may look mathematical. But it’s mathematical gibberish in my view.

You better just stick with businesses that you can understand, use the government bond rate. And when you can buy them – something you understand well – at a significant discount, then, you should start getting excited.

The wisdom here is so simple and timeless on so many levels. First, as just mentioned, for proven compounders like MSFT, we should not be afraid to apply treasury rates as discount rates. There is no reason to stick to the “commonly used” discount rates of 8% to 10% from the CAPM model (the capital asset pricing model, and more on this later) for example. And second, as a corollary to my first point, for stocks that do not have reliable compounding power (or that you do not understand well), sticking a few extra points on the discount rates is purely mathematical gibberish. By messaging the discount rates, you can justify any valuation – no matter how poorly or superb the business actually is.

And next, I will argue why MSFT deserves the treatment of treasury rates as its discount rates. And you will see that this treatment shows its current price is close to its fair valuation.

CAPM and profitability

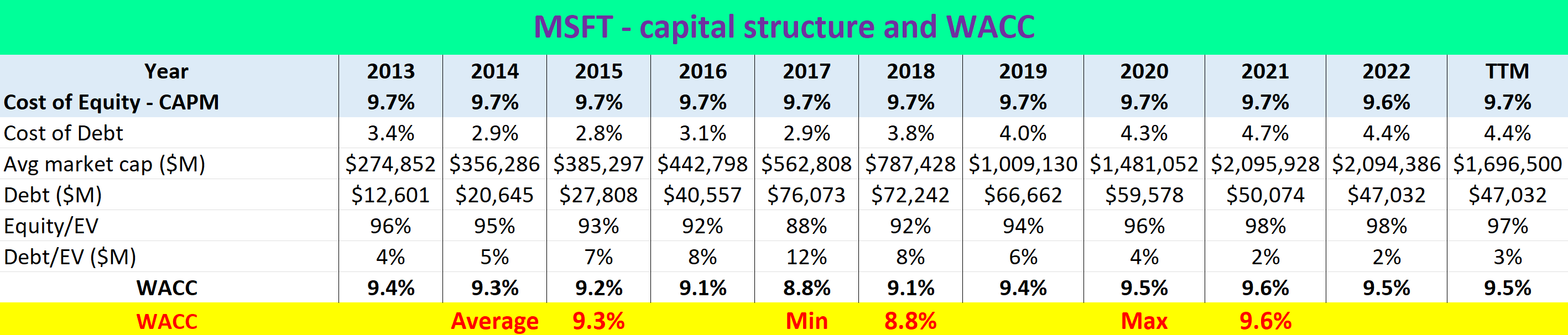

As just mentioned, there is no reason to stick to the “commonly used” discount rates obtained from the CAPM model for reliable compounders like MSFT. To show the inadequacy of the model in this case, the next table shows my CAPM analysis on MSFT. The model has been detailed in my other articles and I will directly go into the results. As seen, the cost of equity and also the Weighted Average Cost of Capital (“WACC”) from the CAPM model for MSFT have been both stable at around 9%, consistent with the commonly accepted range.

Source: author based on Seeking Alpha data

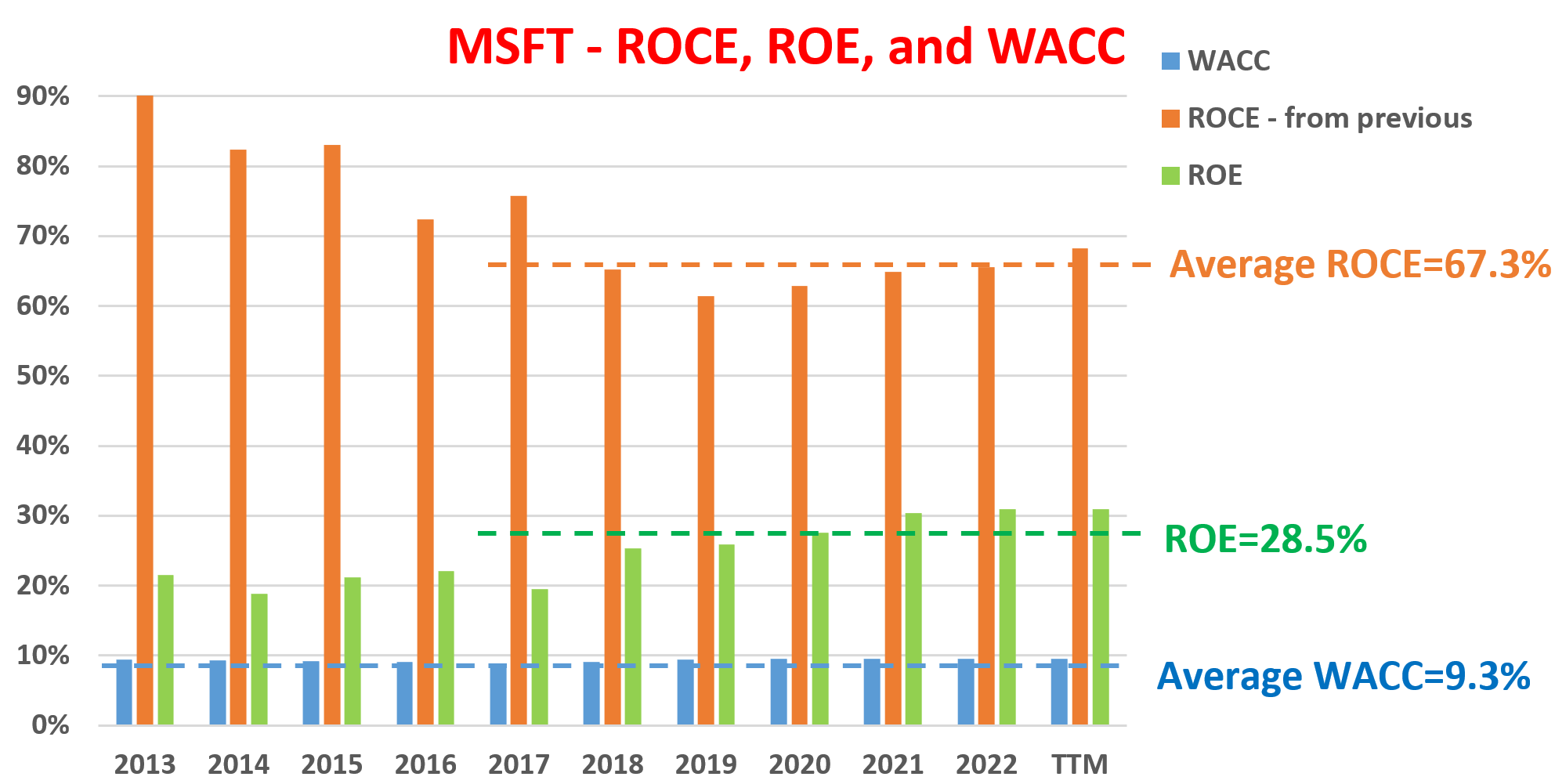

Then the next plot shows a comparison of MSFT’s WACC versus its return on capital employed (“ROCE”) and returns on equity (“ROE”). In my mind, this comparison clearly displays the inadequacy of the above WACC results in the case of MSFT and why it deserves the treatment of the treasury rates as the discount rates. In particular, both its ROCE and ROE have both consistently and substantially above its WACC. To wit, its ROE averages 28.5%, almost 3x above its WACC. And its ROCE averages 67.3%, more than 7x higher than its WACC. Hence, its profitability (either measured in ROCE or ROE) renders any variance in the WACC totally irrelevant (for example, due to the choice of beta, borrowing costs, et al.).

Source: author based on Seeking Alpha data

Fair valuation vs. market price

If you agree with the above argument and accept the risk-free rates as a discount rate for MSFT, then the rest of the discussion is quite straightforward. Next, I will use the discounted dividend model (“DDM”) to arrive at its fair valuation (considering its superb stable dividends). In this DDM model, I used 4.5% as the discount rate, which is my estimate of the steady-state level for 10-year treasury rates (which is also close to the Fed’s current dot-plot). And I used its FW dividend payout of $2.72 per share in the DDM analysis. Finally, for its terminal growth rate, I used the product of its ROCE analyzed above (67.3%) and its reinvestment rates (RR, ~5% based on its long-term historical average). These assumptions led to a terminal growth rate of 3.38% (67.3% ROCE x 5% RR).

With the above parameters, a fair valuation of $242 was obtained from the DDM model ($2.72/(4.5% – 3.38%)). As of this writing, the stock is trading at a price of $232, within 5% of its fair valuation.

Risks and final thoughts

To recap, I see many of the headwinds facing MSFT as only temporary. The declines in Windows OEM and personal devices in particular are caused by the PC market renormalization past COVID in my view. It is both inevitable and temporary in the way I see things. Its cloud business growth slowed in Q2 compared to previous quarters. However, I view the current growth rate as already sufficient. And moreover, I do not suggest investors pay too much attention to the QoQ fluctuations anyway. The main risk I see is the relatively narrow margin of safety here. As just mentioned, the current stock price is within 5% of its fair valuation, leaving little margin of safety.

All told, I view Microsoft Corporation as a textbook Buffett-type perpetual compounder. It features an excellent combination of a mature and reliable cash cow segment and a few high-growth segments. If you take a long view and ignore the quarterly noises, you should not be afraid to apply the treasury rates as its discount rates. And in this case, I see much of Microsoft Corporation’s valuation risks have evaporated already thanks to the 2022 corrections. I see Microsoft Corporation’s current price approaching its fair valuation.

Be the first to comment