Jean-Luc Ichard

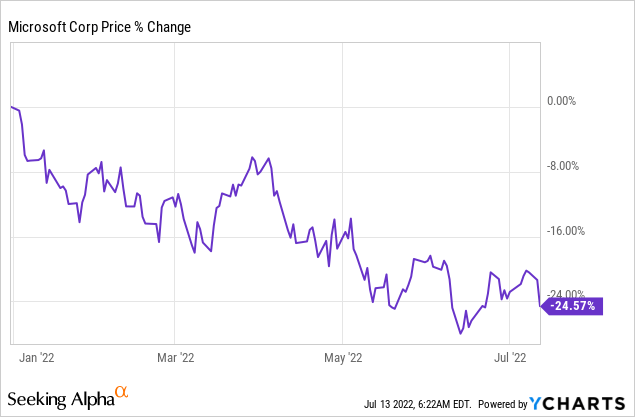

Shares of Microsoft (NASDAQ:MSFT) skidded 4% on Tuesday, bringing the company’s year to date losses to about 25%. Inflation and an appreciating USD are top challenges for U.S. companies right now, including Microsoft. However, Microsoft’s cloud business is resilient and is set to benefit from growing customer adoption despite economic headwinds. I believe Microsoft represents deep recession value at the current valuation and shares are a buy before earnings!

Why Microsoft could submit a strong earnings card for FQ4’22

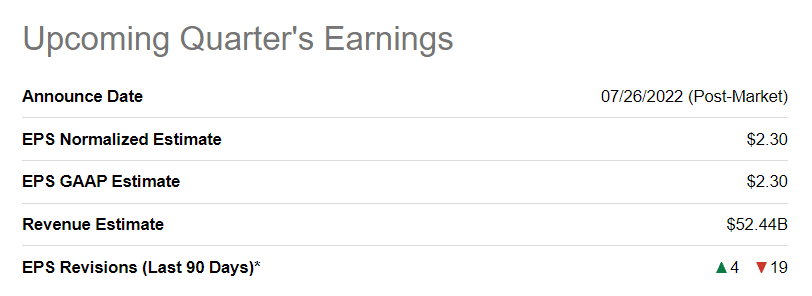

Microsoft will deliver earnings results for FQ4’22 in roughly two weeks, on July 26, 2022. Microsoft is expected to report a fourth-quarter EPS of $2.30, which would show roughly 6% year over year growth. On the top line, Microsoft is expected to see $52.4B, implying a year over year growth rate of 14%.

Seeking Alpha

I believe Microsoft will deliver a strong earnings card, despite short term business headwinds coming from an appreciating USD. The market has also had more than enough time to price in currency headwinds – which were the chief reason behind Microsoft updating its guidance for FQ4’22 in June – but I believe strong commercial performance, especially in the cloud business, could potentially provide an offset to a stronger USD.

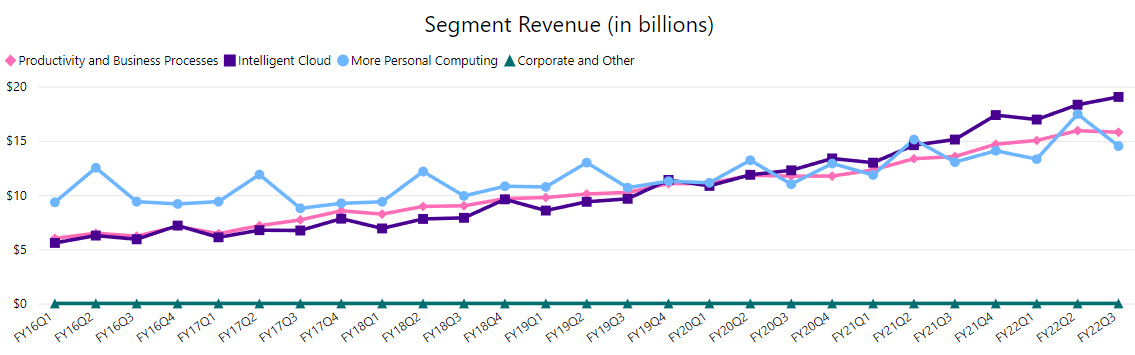

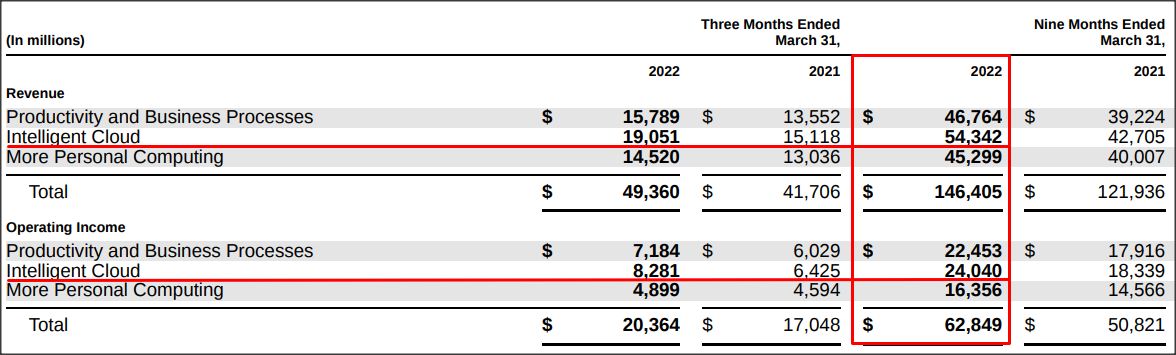

After years of aggressive investments into the cloud business, Microsoft’s Intelligent Cloud business finally overtook the previously dominating Personal Computing business in FQ3’21. The Personal Computing business, which is still quite relevant with revenues of $14.5B in FQ3’22, generates revenues from Windows OEM as well as hardware sales. However, Personal Computing is no longer as important for Microsoft as is the cloud business.

Intelligent Cloud is now Microsoft’s largest business, generating $19.1B in revenues in FQ3’22, and it is the fastest-growing business as well with year over year growth of 29% in FQ3’22 (based on constant currencies). Microsoft’s cloud revenues, due to accelerating market demand for cloud solutions and increasing customer adoption, have increased by a factor of 3.4 X since FQ1’16 and the long-term trend in cloud segment revenue growth is unbroken.

Microsoft

The transition to cloud products and services has been a great success for Microsoft and resulted in the firm achieving a 37% cloud revenue share and a 38% operating income share (based off of YTD FY 2022 figures). The revenue share of Intelligent Cloud increased to 39% and the operating income share to 41% in FQ3’22, showing continual momentum in this business segment. Based on current growth rates, Intelligent Cloud could generate about half of Microsoft’s revenues within three years and also be responsible for about 50% of segment profits.

For FQ4’22, I expect cloud segment revenues to come very close to $20B (and perhaps even exceed $20B for the first time) and an even higher cloud revenue share between 40% and 41%.

Microsoft

But Intelligent Cloud offers Microsoft investors something else besides enterprise-leading growth rates and billions of dollars in quarterly revenues: a recession buffer. Microsoft’s Intelligent Cloud business is set to grow even during a recession due to rising customer adoption and growing demand on IT infrastructure. Companies look to lower their costs and achieve efficiencies during recessions and cloud platforms allow companies to scale.

Since the cloud segment is already the biggest growth machine within Microsoft regarding revenue and operating income contribution, a strongly performing cloud business could also offset other headwinds in the business, such as short-term currency headwinds.

Lower EPS and currency headwinds are priced into Microsoft’s valuation

Microsoft trimmed its outlook for the fourth-quarter due to persistent USD strength. The tech firm lowered both its top line and EPS guidance in June: Fourth-quarter revenues are set to reach $51.94-52.74B, down from $52.40-53.20B, while EPS is now expected to be within a range of $2.24-2.32, down from $2.28-2.35. The guidance was specifically lowered due to currency headwinds.

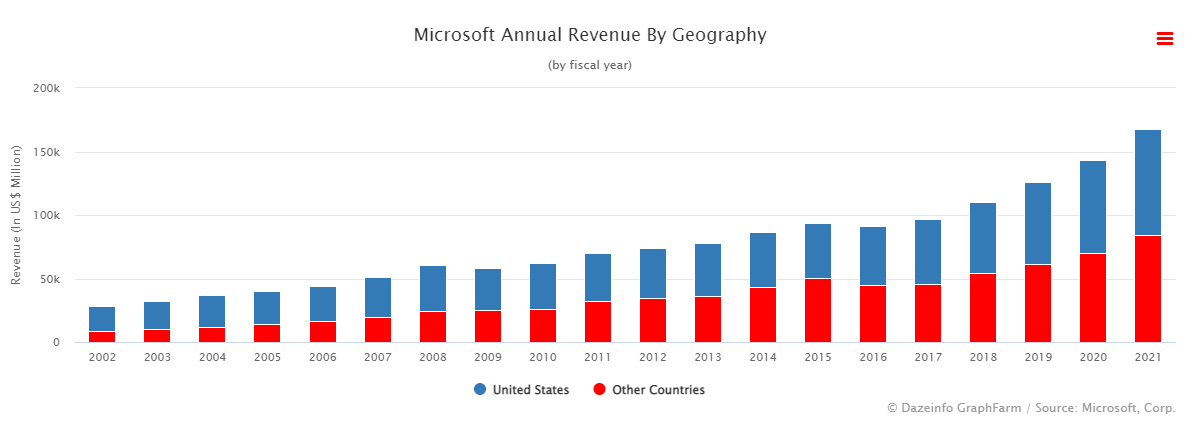

As a global enterprise, Microsoft has exposure to currencies other than the US Dollar. Microsoft bills customers, and incurs expenses, in other currencies such as the Euro, Japanese Yen, British Pound, Canadian Dollar and Australian Dollar. Microsoft achieves approximately 50% of its revenues outside of the U.S., a percentage that has held steady over time. In FQ3’22, Microsoft produced $24.8B in revenues in the U.S. and $24.6B in revenues outside of the U.S., giving the U.S. a slightly more than 50% revenue share.

Dazeinfo Graphs

With 50% of Microsoft’s revenue base being tied to foreign currencies, continual short-term USD strength could impact Microsoft’s earnings outlook beyond FQ4’22, but those headwinds are relatively insignificant considering the strong and durable business trends that Microsoft sees especially in its cloud business.

Microsoft has given an estimate as to how much a strong USD is affecting its earnings picture: A 10% decrease in foreign exchange rates – which is the equivalent of a 10% appreciation in the USD – is expected to translate to earnings headwinds totaling $6.7B.

Microsoft

Microsoft’s business is cheap

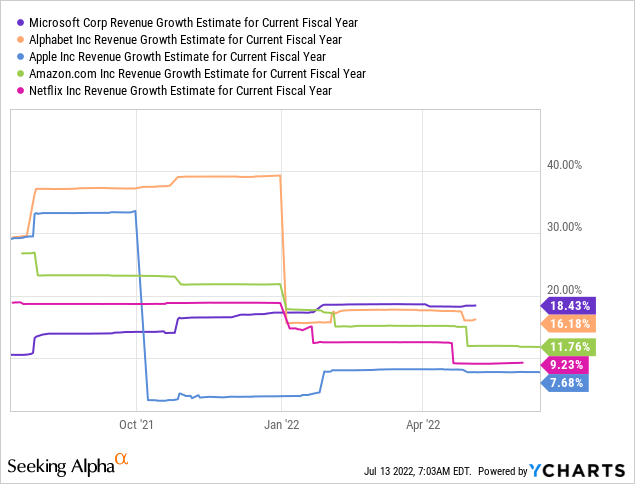

It is unfortunate that currency headwinds take investors’ focus away from the sound nature of Microsoft’s business. Microsoft is expected to grow revenues at an annual average rate of 14% between 2022 and 2026. By 2026, Microsoft is expected to generate $335.4B in revenues and $17.16 in EPS. By this time, Microsoft’s cloud business could generate more than 50% of Microsoft’s consolidated revenues. Microsoft is the fastest-growing big tech company, based on 2022 growth expectations, with an estimated top line growth rate of 18.4%.

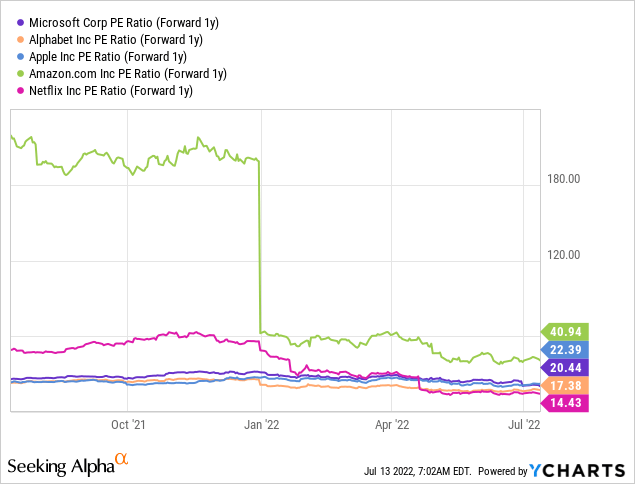

Shares of Microsoft currently have a P-E ratio of only 20.4 X despite significant free cash flow value. Google (GOOG) (GOOGL), as the dominant company in search, cloud and digital marketing, represents deep recession value… just like Microsoft.

Risks with Microsoft

The significant increase in consumer prices is still a major concern for U.S. companies and while inflation numbers for last month have not been reported yet, it is likely that inflation actually accelerated in June. A hot inflation report could result in significant short term valuation headwinds for U.S. stocks, including Microsoft.

What I see as a bigger risk for Microsoft, from a commercial perspective, is a slowdown in the firm’s most priced asset: the cloud business. A deterioration of key metrics such as top line growth, customer adoption or margins would create additional headwinds for the stock and get me to reevaluate my recommendation for Microsoft.

Final thoughts

Shares of Microsoft are a buy before the company submits its earnings card for the fourth-quarter because the cloud business is likely to have seen continual momentum in FQ4’22 and it could provide an offset to an appreciating USD. Microsoft’s long term growth trends in the cloud business are unlikely to be materially impacted by inflation or short term USD strength. Because cloud is now determining the direction of Microsoft’s business, I believe the tech company has great recession value as well!

Be the first to comment