Jean-Luc Ichard

A prospective investment in Microsoft (NASDAQ:MSFT) invites a legitimate bull/bear debate. Even detractors acknowledge that MSFT has a legal monopoly and a reliable, long-term revenue stream in Microsoft Office and Microsoft 365.

That side of the business is married to Azure, a surefire growth engine for the foreseeable future. Add the potential for robust growth from AI, advertising, and gaming, and one can understand why bulls favor MSFT.

The bear’s argument lies largely in the sheer size of the company. The law of large numbers requires monstrous levels of growth to support a P/E ratio that is 20% above that of the S&P 500.

Furthermore, a lesson learned from this bear market is that even the best companies can be overvalued. Proof positive for that claim lies in the losses suffered by the FAANMG stocks over the last year.

Microsoft’s stock recorded its third-worst performance since the company went public in 1986, and 2022 was the first year that MSFT didn’t outperform the S&P 500 since 2012.

However, potential for growth lies in Microsoft’s cloud offerings, LinkedIn and gaming. But with a market cap of $1.8 trillion, can they generate a revenue stream that supports P/E ratios associated with growth stocks? And with a possible recession on the horizon, are the shares destined to decline?

Q1 Earnings: A Mixed Bag

MSFT Q1 2023 earnings beat on the top and bottom lines. EPS of $2.35 and $50.1 billion in revenue topped analysts’ forecasts of $2.31 a share and $49.78 billion in sales.

Azure and other cloud services posted 20% year-over-year growth and brought in $20.3 billion. Productivity and business processes, which includes Office commercial and consumer products and cloud services, grew revenues by 9% year-over-year to $16.5B.

Those were the highlights on the positive side. Unfortunately, there were also a handful of negatives to consider.

Revenue from personal computing “decreased slightly” to $13.3 billion. While intelligent cloud recorded robust growth, there was a significant deceleration from the comparable quarter’s 31% growth rate.

Additionally, during the year-ago quarter, Microsoft posted EPS of $2.71, $0.36 above this quarter’s results.

FX headwinds decreased the firm’s revenues by 5%.

During the conference call, CFO Hood forecast double-digit year-over-year growth for FY23, and at the same time, she warned of weakness in the PC market.

All told, investors weren’t impressed, and the stock fell over 6% in after-hours trading.

Where We Must See Strong Growth

There is no doubt the cloud will provide robust growth for the foreseeable future. Grandview Research forecasts a CAGR for the global cloud computing market of 15.7% through 2030, and Fortune Business Insights projects the cloud computing market will record a CAGR of 19.9% through 2029.

Even so, that falls well short of the growth rates witnessed over the last few years.

Technology Blog

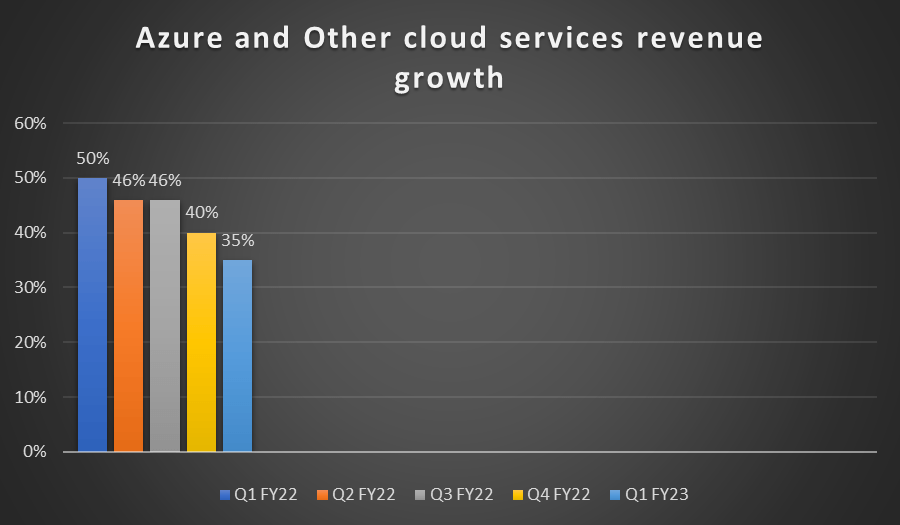

MSFT is adversely affected by the trend. The following chart records the deceleration in the growth of Azure and Other cloud revenues over the last five quarters.

Company reports/author

Microsoft recently revealed plans to expand Azure by building data centers in eleven new regions, and there are additional reasons to believe the company can continue to push outsized growth via its cloud offerings.

Furthermore, Morgan Stanley analyst Keith Weiss believes MSFT has the inside track in the race for IT spending. Weiss cites a survey of chief information officers showing Microsoft is set to tally 40% of expected share gains for IT wallet spending, versus Amazon’s 24%. Nearly half of the CIOs surveyed expect MSFT to garner the lion’s share of IT budgets over the next three years.

Activision’s Part In This Picture

Early last year, Microsoft announced plans to acquire Activision Blizzard (ATVI) in an all cash transaction valued at $68.7 billion. If the deal is consummated, it will mark Microsoft’s largest-ever acquisition.

The addition of Activision would be immediately accretive to adjusted earnings and add leading titles including Call of Duty, World of Warcraft, Overwatch, Diablo, and Candy Crush to Microsoft’s portfolio of games. It would also push Microsoft into third place among the globe’s game developers.

Last month, the U.S. Federal Trade Commission, or FTC, announced it intends to block the acquisition of Activision Blizzard. By no means does that mean the death of the deal; however, MSFT and the FTC will meet in court to do battle before a judge.

Count me as one that is skeptical regarding the FTC’s ability to block this deal. Microsoft holds a 35% global market share versus Sony’s (SONY) near 65% share. Furthermore, Xbox had a 16% market share of consoles in 2021, while Microsoft’s video titles garnered a rather paltry 10% market share.

Activision’s CEO and Microsoft’s President both assured investors they are confident the deal will go through.

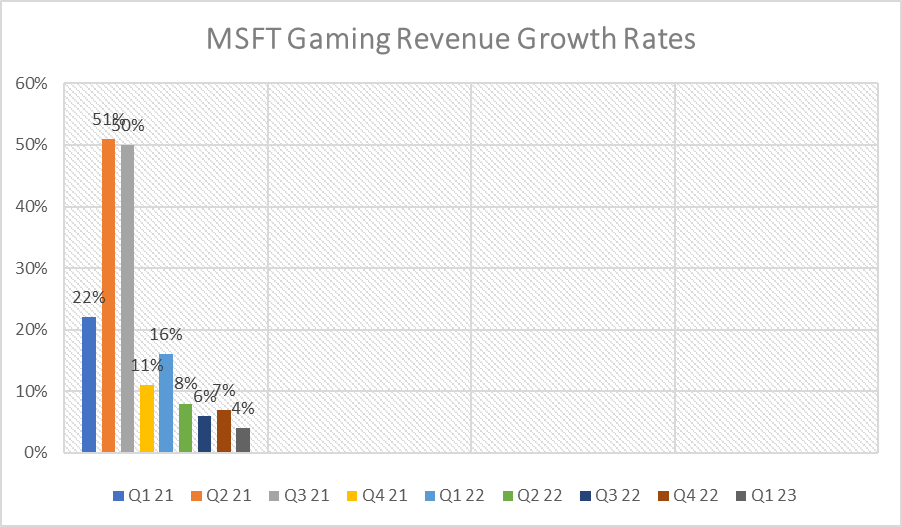

Unfortunately, the Activision deal is not the only problem facing the gaming division. The following chart gives investors a picture of the role gaming played in Microsoft’s growth.

FourweekMBA

Outside of the cloud-related businesses, Gaming has been by far the strongest growth driver. The next chart gives a history of Microsoft’s gaming industry growth over the last nine quarters.

Company reports/ Author

I understand that FY 2022 was in relation to extraordinary growth; however, for a company like MSFT, with a market cap of $1.8 trillion, routine, robust growth is required to maintain an above average stock valuation.

According to a study by Technavio, the gaming market is projected to record a CAGR of 12% from 2021 through 2025. That projection is in the same ballpark as a report by Acumen Research and Consulting that forecasts a 10.2% CAGR for the gaming industry from 2022 through 2030.

LinkedIn And Advertising’s Role

When one thinks of digital advertising, Alphabet and Facebook (META) come to mind. However, MSFT garners $10 billion through advertising through Bing, the Xandr platform, and LinkedIn ads.

With over 875 million professionals and 61 million companies using the service, LinkedIn generated 8% of revenue last quarter and notched a 21% growth rate.

Precedence Research forecasts a CAGR of 9.22% for the global digital ad spending market size from 2022 to 2030.

However, advertisers are quick to cut budgets when a recession is looming. It would not be surprising to see advertising related revenues suffering over the short term.

On the advertising front, there has been a great deal of talk lately regarding ChatGPT, an artificial intelligence chatbot created by OpenAI. It answers users’ verbal questions and can also write and debug computer programs, compose music, to list but a few of its capabilities.

The company’s founder claimed over a million users for the text-based application within a few days of its debut. That prompted immediate chatter among investors regarding how ChatGPT might be used by Bing to challenge Google.

I’ve conducted my due diligence on ChatGPT, but for the sake of brevity, I’ll refer you to the following quote to sum up my perspective.

Microsoft invested $1 billion in OpenAI, in 2019, and there have been reports the company is considering investing another $10 billion into Open AI.

ChatGPT is incredibly limited, but good enough at some things to create a misleading impression of greatness. It’s a mistake to be relying on it for anything important right now. It’s a preview of progress; we have lots of work to do on robustness and truthfulness.

Fun creative inspiration; great! reliance for factual queries; not such a good idea. We will work hard to improve!

Altman, CEO, OpenAI

I’ll add that Google has a similar language model, LaMDA.

ChatGPT may hold potential, but it will by no means contribute to Microsoft’s growth in a meaningful way over the foreseeable future.

Debt, Dividend, And Valuation

In Q3, MSFT held $107 billion in cash and short-term investments and had debt of $48.6 billion.

Microsoft is one of only two publicly traded companies with a AAA credit rating from Standard & Poor’s.

The current yield is 1.14%, the payout ratio is 27.37%, and the 5-year dividend growth rate is 9.82%.

MSFT trades at $239.23 per share. The average one-year price target of the 33 analysts that rate MSFT is $293.09. The price target of the 23 analysts that rated the stock following Q3 earnings is $281.65.

The stock’s forward P/E is 25.10x, well below the 5-year average P/E of 30.77x. The 5-year PEG is 2.10x, a bit below the 5-year average for that metric of 2.17x.

Is Microsoft a Buy, Sell, Or Hold

Microsoft is not immune to macroeconomic factors. The relatively lackluster results in Q3 reflect that. Although Azure recorded robust growth, it was well below that of prior quarters.

Once robust growth in the gaming business has also faltered, PC sales have slowed markedly, and with prospects of a recession looming on the horizon, the digital advertising market is in decline.

That must be weighed against the company’s fiscal year 2022 results. Microsoft generated record revenue of $198.3 billion, up 18%, along with operating income of $83 billion climbing by 19%. Furthermore, Microsoft can boast of net margins above 30%, and Azure has near guaranteed double-digit growth for the foreseeable future.

Unfortunately, growth is not the problem when considering Microsoft as a prospective investment: rather, it is the rate of sustained growth that must be achieved to support a high valuation in a company with a market cap of $1.8 trillion.

Investors should consider that after MSFT shares plummeted in value in early 2000, it took until 2015 for the stock to recover.

I rate MSFT as a BUY, but by the narrowest of margins.

I initiated a very small position in the company while conducting my due diligence for this article (I sold all of my FAANMG stocks early last year.)

An uptick in cloud, gaming, and advertising demand are essential for MSFT to maintain long term, strong growth. The Activision deal moving forward, while not essential, would be a solid plus.

I would say the next two years are probably going to be the most challenging, because after all, we did have, you know, a lot of acceleration during the pandemic, and there is some amount of normalization of that demand. There is a real recession in large parts of the world. And so the combination of ‘pull forward and recession’ means we will have to adjust.

Microsoft CEO Satya Nadella

With MSFT, we are dealing with the law of large numbers; therefore, to build more than a small position in the company, I need to have confidence that the Microsoft can drive growth in each of these businesses.

I’ll add that we are likely to enter a recession this year, and that we could very well experience further downside in the market. Obviously, that could lead to additional downside for the stock.

Be the first to comment