skynesher

Thesis

The Macquarie Global Infrastructure Total Return Fund (NYSE:MGU) had announced on August 11 that its board of directors approved the reorganization of the fund into Aberdeen Standard Global Infrastructure Income Fund (ASGI). The merger was contingent on shareholder approval and green light for ASGI to issue new shares. As predicted in our prior article, the approvals have now been obtained:

PHILADELPHIA, PA / ACCESSWIRE / December 9, 2022 / abrdn Global Infrastructure Income Fund announced that it held a special meeting of shareholders on December 9, 2022 (the “Meeting”) at which shareholders of the Fund voted to approve (i) the issuance of additional shares of the Fund in connection with the proposed reorganization of Macquarie Global Infrastructure Total Return Fund Inc. and (ii) ratified the selection of KPMG LLP as the Fund’s independent registered public accounting firm for the fiscal year ending September 30, 2023.

The shareholders of MGU approved the reorganization at a special shareholder meeting also held on November 9, 2022. It is currently expected that the reorganization will be completed in the first quarter of 2023 subject to the satisfaction of customary closing conditions.

With all necessary approvals now obtained, it is a matter of time and operational swiftness to complete the merger. Ultimately MGU shares will cease to trade, with only the ASGI ticker outstanding. MGU belongs to the Macquarie/Delaware Management Company CEF family and Macquarie is liquidating that business with all the CEFs being merged into Aberdeen funds.

Mergers are delicate times, and we are keen to see exactly how the ultimate management team shakes out.

What does it mean for shareholders?

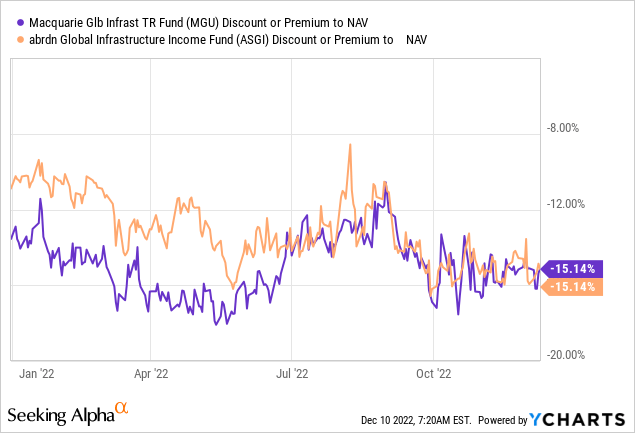

With the approvals now obtained, investors can now look at ASGI and MGU as being proxies for each other. That means that any significant divergence in premiums / discounts to NAV can be traded here, since ultimately the merger approval means that a share of MGU equates a share of ASGI. Let us have a look at how the discounts to NAV have performed:

Since the merger was announced, the two discounts to NAV have converged, with the market signaling the corporate action will move forward. We can see the two funds have identical discounts to NAV now. Any divergence here can be traded.

From a total risk perspective, the holders in the funds are most certainly running the same market and credit risks as before, with the ongoing bear market having a profound impact on the collateral pool. It is going to be interesting to see though how the ultimate collateral pool is going to be adjusted, and what portfolio managers are ultimately going to end up running the combined fund. These are trying times for both management teams, and we are presuming there is significant current internal strife in order to secure appropriate roles for each portfolio manager.

We are of the opinion that there will be another leg down in the wider risk markets, so we like to be in cash or cash like instruments for now. Given the ongoing internal alignments for the management teams we are of the opinion that investors are best served to sit on the sidelines for now with respect with both funds, with the timing of the operational merger occurring, coinciding with what we think will be a bottom in the wider risk markets.

Conclusion

The MGU / ASGI merger has now been fully approved by all shareholders. This leaves just the operational aspect open, where the asset pools are merged, and the MGU shares are retired and replaced with ASGI ones. The two funds will also need to come up with a unified portfolio management team that is going to define the strategy for the fund going forward. The two CEFs have the same discount to NAV now, not leaving any space for a merger arbitrage trade. If any differences arise, a retail investor can trade the differential, since the two tickers are now virtually equivalent. We believe that from a macro perspective we are entering another leg down in a bear market, hence we would rather be long cash than any risk. We also feel that this tumultuous period of asset mergers and internal political alignments to the new structure will take some focus away from the optimal day to day collateral positioning. Therefore we would rather be in cash than in ASGI/MGU, and would only trade a merger arbitrage opportunity if it would arise (i.e. a significant divergence between the discounts to NAV for the two funds).

Be the first to comment