mccawleyphoto

Introduction

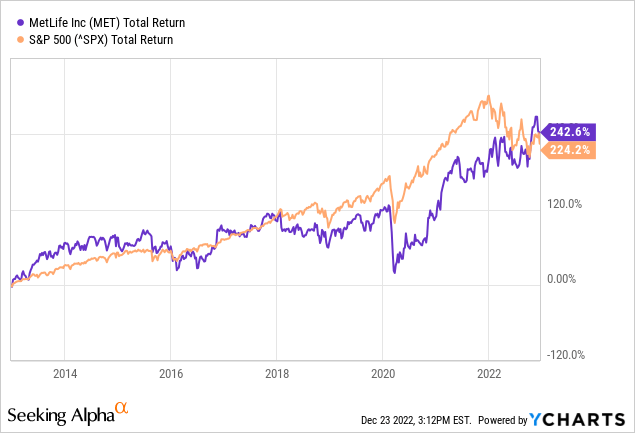

MetLife (NYSE:MET) is a major insurer that has expanded rapidly in recent years. Over the last decade, total stock returns have averaged 13% per year, nearly matching the total return of the S&P 500.

Even though the GAAP P/E ratio is at an all-time high, the shares are fairly valued. MetLife is benefiting from rising interest rates, and investment income is soaring. The company is steadily growing, the stock’s valuation is in line with its historical average, and the stock is therefore worth buying.

Company Overview

MetLife is a leading global provider of insurance, annuities, and employee benefit programs, serving 90 million customers in more than 60 countries. The company was founded in 1868 and is headquartered in New York City.

MetLife operates through three primary business segments:

- Insurance Products

- Retirement Products

- Asset Management

The Insurance Products segment offers a range of life, accident and health, and property and casualty insurance products. The Retirement Products segment provides retirement savings and income solutions. The Asset Management segment manages a diverse set of investment assets, including public and private equity, fixed income, and real estate. MetLife is committed to helping its customers and communities navigate the complexities of the financial world and is known for its strong financial stability and customer service.

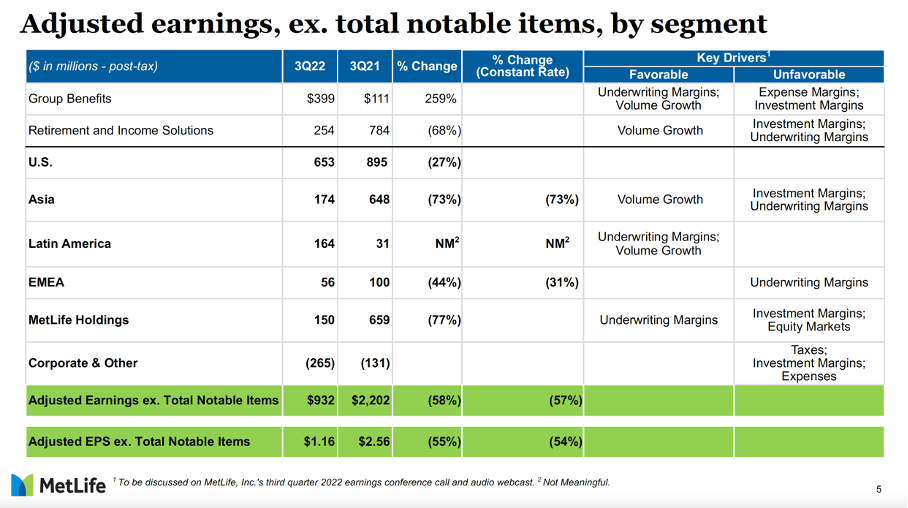

Third Quarter Results Came In Mixed

Adjusted Earnings (MetLife’s 3Q22 investor presentation)

MetLife’s third quarterly earnings came in mixed as the company showed net investment losses for the quarter of $433M excluding hedge adjustment losses. Net income came in at $331M while adjusted net earnings came in at $966M for the quarter.

Many of the macroeconomic trends from the first half of the year continued into the third quarter. Equity markets fell, interest rates rose and a recession is imminent.

Private equity results reflect the difficult equity market in the second quarter, which fell 16.4% as measured by the S&P 500. Negative private equity returns had a strong impact on quarterly earnings as private equity losses were $53M for the quarter.

MetLife navigated an interest rate environment in which the new money rate was lower than our roll-off rate. That changed in the second quarter, when the new money rate exceeded our roll-off rate. This was repeated to greater effect in the third quarter. MetLife anticipates that the impact of this change will be felt over time, given that the average duration of our investment portfolio is approximately 8 years. Rising interest rates are generally beneficial to MetLife.

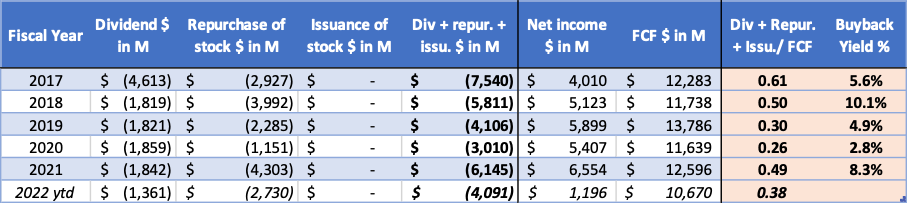

Dividends And Share Repurchases

MetLife is a publicly traded company and has a history of paying steadily growing dividends to its shareholders. The dividend per share has grown from $1.58 in 2016 to $1.90 per share in 2021, representing an annual growth rate of 3.8%. The dividend currently stands at $2.00, making the dividend yield 2.8%.

MetLife’s dividends per share, in cents (DividendMax)

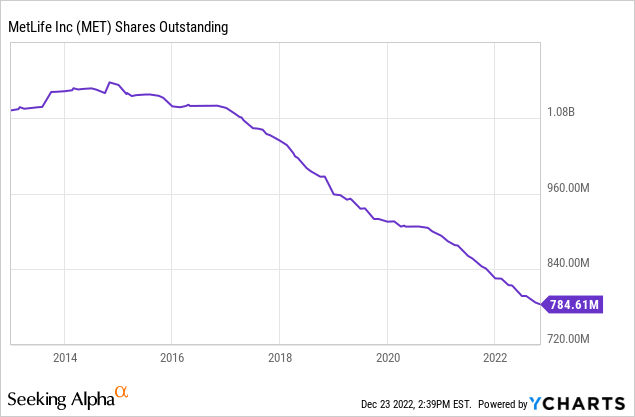

In addition to dividends, MetLife also repurchases shares. Share repurchases can be used to reduce the number of outstanding shares and increase the value of the remaining shares, which can benefit shareholders by increasing the value of their investment. Share repurchases increase dividends per share. Like dividends, share repurchases are typically authorized by the company’s board of directors and can be adjusted over time.

The company repurchased $4.3B of shares in fiscal 2021, making the repurchase yield high: 8.3%. Currently MetLife has repurchased $2.7B of shares year-to-date, the repurchase yield is already above 5%.

The company can sustain dividend payments and share buybacks well, as this accounted for only about 49% of free cash flow in 2021.

MetLife’s cash flow highlights (SEC and author’s own calculations)

Share buybacks have reduced the number of shares outstanding from 1.1 billion in 2014 to 785 million today, a decline of nearly 4% per year. Share buybacks can increase the share price if the shares are bought in the open market while supply declines. The share price has risen 47% since 2014.

Valuation In Line With Its Average

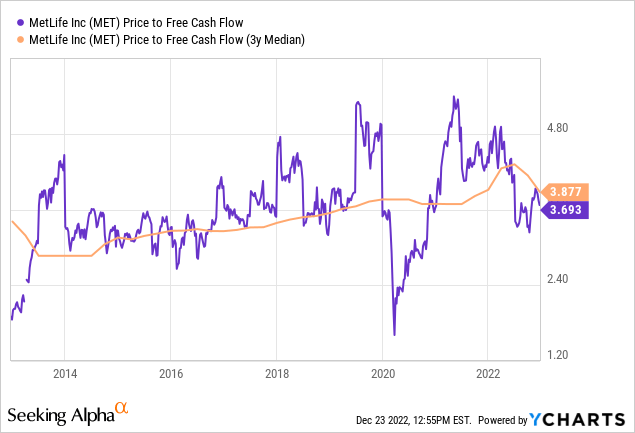

Net income has fallen significantly since the beginning of the year, pushing the GAAP P/E ratio to unprecedented levels. In situations where the P/E ratio is high and net income is falling, it may be useful to consider other financial benchmarks, such as the price-to-free cash flow ratio. The price-to-free cash flow ratio is a measure of a company’s valuation that takes into account the company’s ability to generate cash flow. It is calculated by dividing the market price per share by the company’s free cash flow per share.

The price to free cash flow ratio currently stands at 3.7, indicating that the stock is below historical benchmarks of 3.9. During the 2020 stock market crash, the stock was trading at an all-time low price to free cash flow of 1.3. This sigma event should not occur from time to time. The current price to free cash flow ratio compares favorably with historical benchmarks.

Conclusion

MetLife has been serving customers since 1868 as a global provider of insurance, annuities, and employee benefit programs. The total stock return matches the S&P 500, and valuation suggests that the company is undervalued in comparison to the S&P 500 and its historical benchmarks. Even though GAAP P/E is at an all-time high due to private equity losses, the company trades favorably on the market when measured by its price to free cash flow ratio. MetLife is benefiting from rising interest rates, and investment income is soaring. The company is a strong dividend compounder, with annual dividend growth of 3.8% on average. The company is steadily growing, the stock is valued in line with its historical average, and the stock is worth buying.

Be the first to comment