Lemon_tm

We maintain our buy rating on Meta Platforms (NASDAQ:META) as we believe the worst has been priced into the stock and see Meta recovering toward 2H23. Since our last publication on Meta in early November, the stock has risen nearly 41%.

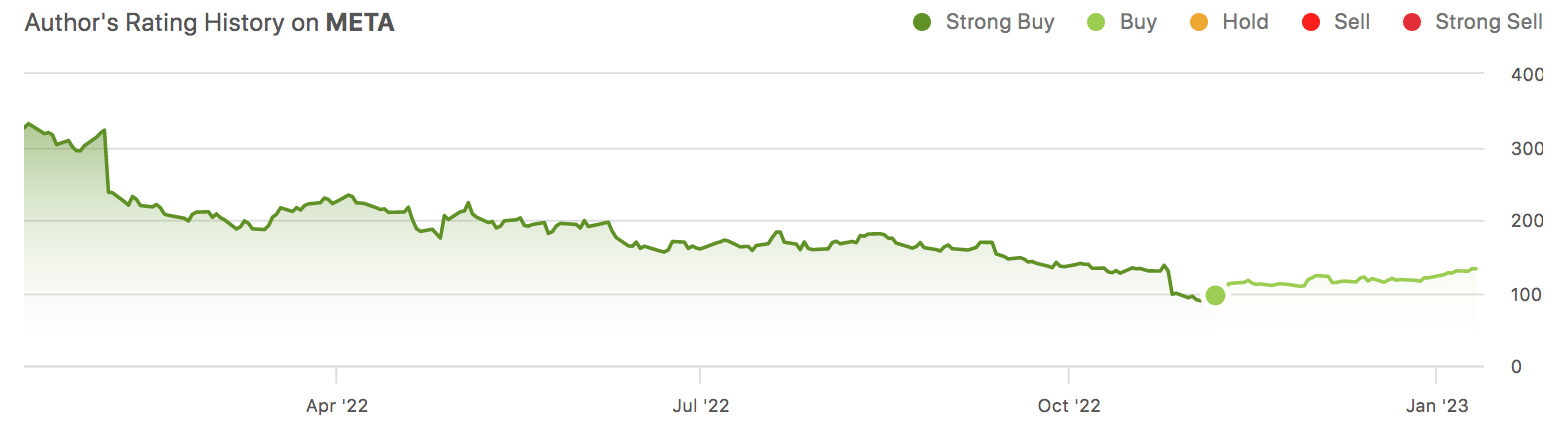

The following graph outlines our rating history on META.

SeekingAlpha

We expect Meta’s stock to continue to be driven higher as the company takes steps to be more disciplined when managing Metaverse spending. We also believe Meta is working to improve engagement in its Family Apps group. We continue to expect the stock price to remain volatile in the near term, but expect the sell-off last year to provide a favorable entry point into Meta as a value stock. We believe investors jumping into the stock at current levels will be well-rewarded in 2023.

Favorite pick among FANG stocks

While 2022 was a rough year for the entire tech space, it hit Meta particularly hard, with the stock reaching a low of $88.09 late last year. Our bullish sentiment on Meta is driven by our belief that Meta is a value stock at current levels with potential growth drivers in 2023. We expect management to bring its A-game to improve audience engagement; we’ve already seen this with Meta’s Instagram adding the reel feature to better compete with Chinese giant TikTok.

While we saw tech stocks drop across the board over the past 15 months, we believe that part of Meta’s pullback was self-inflicted. To better outline why we expect Meta to recover in 2023, we believe it’s essential to discuss why the stock is down so low in the first place, addressing how these negative headwinds will be flipped over for the stock to grow meaningfully.

1. Macroeconomic headwinds spilling into Ad spending

Macroeconomic headwinds is a phrase that doesn’t seem to be getting old, even in 2023. We believe Meta’s pullback in 2022 was largely the result of the weaker spending environment resulting from heightened inflationary pressures and spiked interest rates. We saw advertisement spending weaken significantly in 2022. We believe the weaker spending environment took a bit out of Meta’s ad revenue, which accounted for roughly 49% in 3Q22. Meta’s 3Q22 earning report showed an ad revenue decline of nearly 4% Y/Y. We believe the weaker spending played a big role in the large tech stock pullback not only for Meta but for Alphabet (GOOG) and Snap (SNAP), reporting slower ad revenue growth. We believe the ad spending environment will remain tight for the 1H23. We believe the ad weakness has been priced into the stock, and hence, we remain bullish on Meta’s growth story in 2023.

2. (Over)Spending on Reality Labs

Meta’s name change in 2021 from Facebook to Meta Platforms came with a foreshadowing of massive spending on Mark Zuckerberg’s dreams to spearhead the journey of making the Metaverse a reality. Over the past four years, Meta allocated nearly $36B to developing its Reality Labs project. The overspending signaled major red flags for investors globally as the Metaverse project will likely take years to become profitable but will continue deepening operation losses on Meta’s financials. In 2021, Reality Labs lost $10.2B in operational losses and another $5.8B in the first half of 2022. While Meta’s overspending on its Reality Labs has undoubtedly caused a dent in Meta’s stock, we’re more constructive on the stock now as we expect to see management practice more disciplined spending going forward.

Currently, Meta is one of the top Virtual-Reality Hardware platforms through its Oculus devices. Hence, we believe if any company is well-positioned to profit from the long-term investment in the metaverse, it’s Meta Platforms. We believe the company’s Family Apps segment with Facebook and Instagram apps provides a cash flow to fund the company’s investment in the metaverse.

We believe the stock price will remain volatile in the near term; we believe the worst is behind for Meta. Our expectation of a volatile stock price is due to the macroeconomic environment and rising costs on all fronts. Meta’s revenue declined by 4% in 3Q22. We also believe, consistent with management’s announcement in the 3Q22 earnings call, foreign exchange headwinds will cause a 7% headwind on total revenue in 4Q22. Despite this, we believe the company is better positioned to grow now and believe it provides a favorable risk-reward profile after the stock sell-off.

Valuation

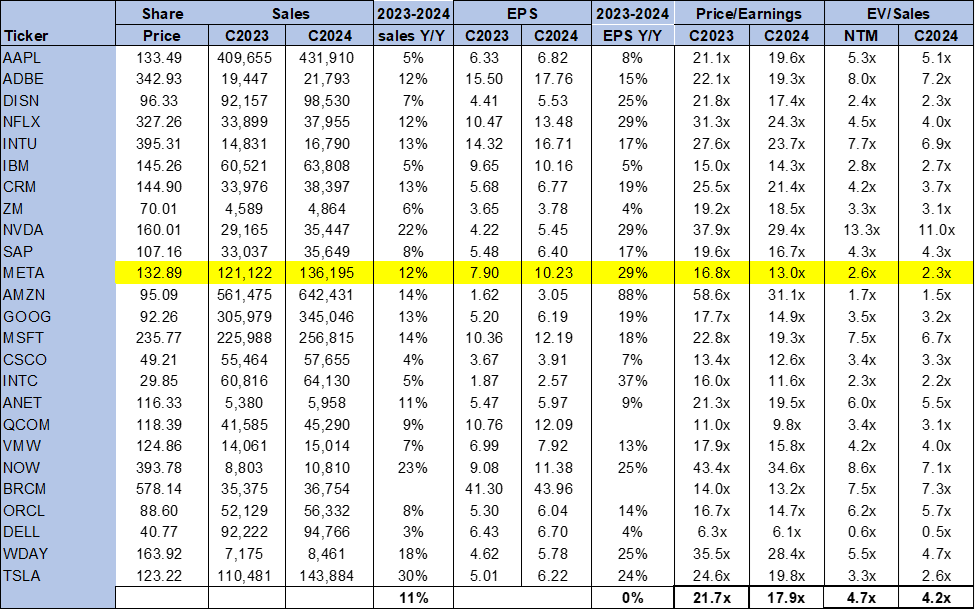

We believe Meta Platforms is a value stock trading significantly lower than the peer group average. On a P/E basis, the stock is trading at 13.0x C2024 compared to the peer group average at 17.9x. The stock is trading at 2.3x EV/C2024 versus the peer group average of 4.2x. Meta Platforms is our favorite pick among the FANG stocks at the moment, as we believe the stock’s sell-off last year provides an attractive entry point into Meta’s long-term growth.

The following table outlines META’s valuation in the peer group.

TechStockPros

Word on Wall Street

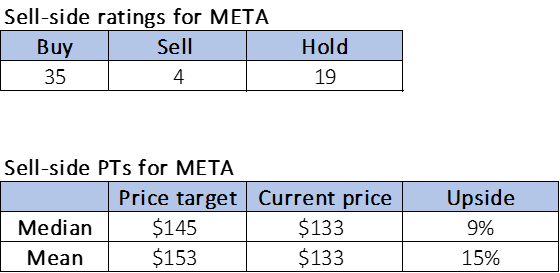

The majority of Wall Street is bullish on Meta Platforms. Of the 58 analysts covering the stock, 35 are buy-rated, 19 are hold-rated, and the remaining are sell-rated. The stock is currently priced at $133. The median sell-side price target is $145, while the mean is $153, with a potential upside of 9-15%.

The following tables outline META’s sell-side ratings and price targets.

TechStockPros

What to do with the stock

We’re bullish on Meta. We believe Meta is a value stock trading well below the peer group. With the disappointing and expected 3Q22 earning results and the stock pullback last year, we believe Meta is at the bottom and on its way back up. We’re more constructive on Meta in 2023 as we see management exercise more discipline in Metaverse spending. We also expect the weakness of ad spending amid macro headwinds to have been priced into the stock at current levels. Meta is our favorite stock in the FANG group; hence, we recommend investors buy the stock at current levels.

Be the first to comment