Galena Georgieva/iStock via Getty Images

Investment Thesis

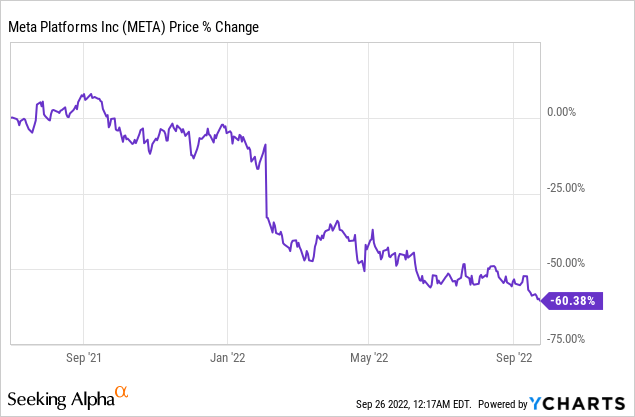

Meta (NASDAQ:META) today is a very compelling investment opportunity. But it’s not immediately obvious why. In fact, I declare that there are three reasons why the stock is going to fare badly in the near term.

Increased competition, too aggressive investment into unproven endeavors, and the one topic that few investors are discussing, the impact of the strong USD on its Q4 guidance.

However, despite all that, I’m still bullish on Meta. Indeed, I believe that paying 14x next year’s depressed run-rate EPS coming out of Q4 2023, is a compelling valuation.

There are a lot of nuances, so let’s get to them.

I Get How We Got Here, But What’s Next?

Back in 2020-2021, a confluence of factors came together and drove a massive move towards online advertising. It was the exclamation point on a decade-plus bull run.

Companies and investors were all drinking from the same punch bowl, and everyone, myself included, was extrapolating into the future.

But that’s done now. Nearly all stocks have already come down 30%, 40%, and sometimes as much as 95% from their highs. Indeed, aside from Apple (AAPL) and Tesla (TSLA), the last two generals left holding up this market, the rest of the market has already taken a lot of medicine.

And this is where things get really interesting. A lot of the high-flying consumer-facing businesses have already been selling off since February 2021! Throughout 2021, small and medium cap businesses had already seen a lot of their air taken out of their ballons.

Indeed, those high-flying names, are already 18 months into this bear market. Think about that. Today, while a lot of the headlines are now incredibly bearish, it’s actually interesting to note that the junkier names have actually stopped getting hit as hard in the past several months.

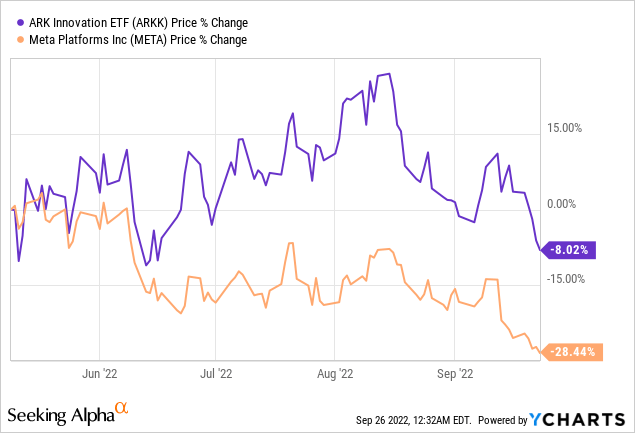

So the market is starting to bifurcate and think through, where is the value left.

And I know that it feels like nothing short of blasphemy to even proclaim that any ARK-like (ARKK) business holds ”value”, but do believe that in the same way that the market got carried away with one idea on the way up, it has now taken the idea too far in the other direction, believing that there’s no value in tomorrow’s disruptive technologies.

And this is where things get really interesting. Meta saw an opportunity in the metaverse. They were perhaps too bold with their investments into an unproven technology, but there’s nothing that can be done about that now.

This doesn’t mean that Meta hasn’t learned some lessons in the past year, and is now much more astutely measuring their progress for a clear return on investment hurdle.

Because ultimately, Meta had to do something to find its next growth engine. As we all know, the social media space continues to get increasingly competitive from the likes of TikTok (BDNCE).

Essentially, Meta was making the right moves, it just got caught flatfooted with the environment going from everything is going smoothly and predictable, to everything has become uncertain, unknowable, and unpredictable.

And when that happens, given that business is essentially fully driven by advertising revenues, that left Meta very poorly positioned in a weakening economy on three fronts.

Top 3 Reasons to Avoid Meta

In the first instance, as noted already, Meta’s core advertising business was struggling for growth. Both because of increased competition but also because of a weakening economy.

The second reason that was plaguing the company was that it was aggressively investing in an unproven area. As discussed already, perhaps Meta would have been more prudent and less aggressive with its metaverse investments if investors for their part weren’t clamoring for growth at any cost strategies.

In actuality, I argue that investors were to blame too, as the investment community was welcoming all kinds of half-baked businesses and rewarding them. As you know.

Needless to say that in that environment it made all the sense in the world for Meta to embark on its journey.

And the third, and less discussed reason to avoid Meta is because of an aspect that I believe too few investors are putting enough consideration towards. The dollar is now a massive headwind.

Recall, more than two-thirds of Meta’s business (including Canada) comes from overseas. And with the USD making a parabolic move in the last few weeks, this is going to make Meta’s Q4 revenue growth rates look materially worse than what the market is pricing in.

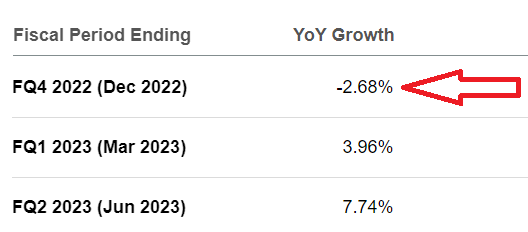

Meta’s revenue consensus estimates

Presently, analysts are still expecting that Meta’s Q4 revenues are only going to be down approximately 3% y/y.

And here I believe that expectations are irrationally high. Right now, analysts and the investor community as a whole are slowly taking hold of this line of thought, but nobody is really putting pen to paper and making the necessary adjustments.

Nobody wants to be the first to downgrade the stock and be on the receiving end of all those negative indirect ”losses in perks”. It’s a sin for a respected analyst house to downwardly revise a stock. You have to wait for someone else to do it first. And then, the sting is out and everyone can do it.

With all this in mind, let’s now turn our focus to Meta’s valuation.

META Stock Valuation – 14x EPS?

If you’ve read this far, you’ve had to digest a lot of bad news. Nobody likes receiving bad news on a stock they own, right? And I fundamentally believe that things will get substantially worse for Meta. And that analysts have yet to downwardly revise their Q4 and early 2023 revenue estimates.

That being said, even while I believe that things are going to get a lot worse in the near term, I also believe that looking beyond the next 6 to 9 months, Meta will come out significantly stronger from this calamity.

This is a company with a long history of failure. Failures to get its platform to move beyond the desktop, scandals with Cambridge Analytica, failure in getting any traction with its Diem currency, failures with breaking into hardware, and countless other failures too. It’s a company that takes the mantra of innovate or die to heart.

And yet, lest we forget, even up to the last reported quarter, the business still had 29% GAAP margins! This is an impressive free cash flow generating business, that actually makes GAAP margins. In fact, very high GAAP margins.

Yet, as I’ve asserted already, I very much believe that the very near-term will see Meta’s earnings getting downwardly revised. And that makes it difficult to get a good grip on its forward EPS figure.

Could Meta be on a $10 EPS run-rate as it exits Q4 2023? I believe that’s a very reasonable assessment of its potential.

Hence, that means that the stock today is priced at approximately 14x next year’s depressed earnings. This strikes me as a very attractive valuation.

The Bottom Line

Men, it has been well said, think in herds. It will be seen that they go mad in herds, while they only recover their senses slowly, and one by one. (Charles Mackay)

While the stock offers positive risk-reward, nuances are important.

On the one hand, I do believe that as Meta comes out of this downturn on the other side, it will have learned a lot of difficult lessons. And so I believe that the business will put in place measures to be less cyclical with its advertising revenues.

On the other hand, nobody rings a bell letting you know when the bottom is in on a stock. What’s more, the game isn’t about getting in at the bottom. The game is only about buying low and selling high. And even if things do become worse here in the near term, it’s difficult to imagine that the outlook is going to get a lot more negative than it is right now. I’m confident you’ll agree.

Be the first to comment