pcess609

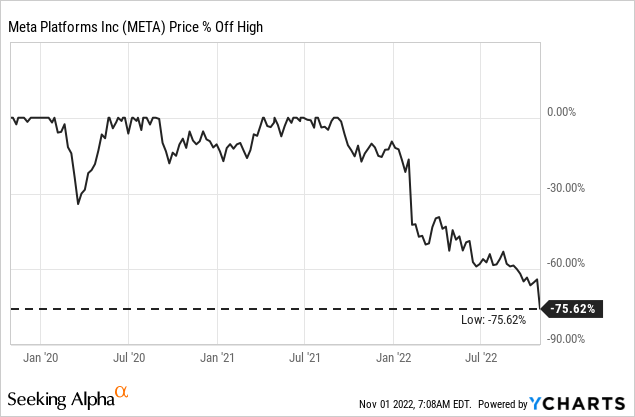

The pessimism surrounding Meta Platforms, Inc. (NASDAQ:META) is astonishing but certainly not unprecedented. The performance of the stock is reminding of several technology companies during the Dotcom crash and recently several technology companies – including the Chinese counterpart Tencent Holdings (OTCPK:TCEHY, OTCPK:TCTZF) – performed similar. So far, Meta Platforms has lost 75% of its value and turned from a company that was briefly worth above $1 trillion (and among the top companies in the world by market cap) to a $250 billion company ranging only on the 33rd spot on the list of the most valuable companies in the world.

When reading comments – including comments on Seeking Alpha – I seldom see analysis and logic but just expressions of hate for Mark Zuckerberg, using the word “woke” countless times and talking about “Karma.” And while this is obviously no analysis, it is an expression for the sentiment surrounding Meta Platforms. In such a sentiment-driven environment, decisions are often lacking the necessary objectivity to make good investment– which might explain why the stock is trading below $100 and close to the point of maximum pessimism.

Declining Profitability

Of course, fundamentals also justify the stock to go lower from its previous all-time highs of $380. And one fundamental problem is the declining profitability for Meta Platforms in the last few quarters. In Q3/22, the company had to report huge declines for the bottom line once again. Diluted earnings per share declined from $3.22 in the same quarter last year to $1.64 this quarter. And when looking at the results for the first nine months, EPS declined from $10.11 in the same timeframe last year to $6.82 this year.

Meta Q3/22 Earnings Release

When looking for the reasons, we can mention several aspects. Although playing only a small role, interest payments of $88 million had a negative effect (due to the company’s $10 billion in long-term debt). Cost of revenue declined about 1% to $5,716 million, but the operating expenses increased dramatically. General and administrative expenses increased 14.9% year-over-year to $3,384 million, and research and development expenses increased 45.2% YoY to $9,170 million. And the result was operating income cut in half from $10,423 million in Q3/21 to $5,664 million this quarter.

Top Line Growth Slowing Down

But not only increased costs had a negative effect. Revenue also declined from $29,010 million in Q3/21 to $27,714 million in Q3/22 – resulting in 4.5% decline YoY. Management was pointing out, that on a constant currency basis revenue increased 2% year-over-year. We can also look at the different regions and different segments and see mixed trends. Dave Wehner gave details during the last earnings call:

The healthcare and travel verticals were the largest positive contributors to growth in Q3. However, this was offset by continued softness in other verticals, including online commerce, gaming, financial services and CPG. On an advertiser size basis, revenue growth from large advertisers remains challenged, while we have seen more resilience among smaller advertisers. Foreign currency was a significant headwind to advertising revenue growth in all international regions. On a user geography basis, year-over-year ad revenue growth was strongest in Asia-Pacific and rest of world at 6% and 3% respectively, with both regions continuing to benefit meaningfully from strong growth in click-to-messaging ads. North America and Europe declined 3% and 16% respectively.

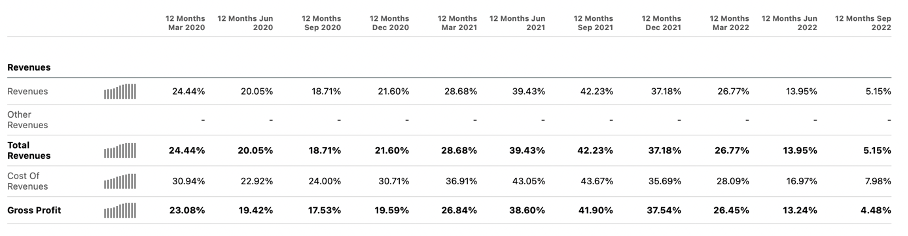

And during the last few quarters, growth clearly slowed down – when looking at the TTM numbers, revenue growth declined for four quarters in a row from 42.33% growth in September 2021 to only 5.15% right now.

Meta Platforms TTM numbers, year-over-year growth (Seeking Alpha)

Problems, Problems, Problems?

We should not ignore the problems Meta Platforms is clearly facing. Revenue growth is slowing down and, due to increasing costs (we will get to that), profitability is declining and earnings per share are crumbling. And the stock certainly deserved to decline in value, but a 75% decline was unjustified – especially as Meta Platforms was not so expensive to begin with (even more true when comparing to several other hyped stocks). When looking at the results in more detail, there are signs to be optimistic.

Small Signs of Growth

First, on a constant currency basis, revenue increased 2% year-over-year. This is still not great, but we should also not ignore the strong U.S. dollar being a headwind – for Meta Platforms as well as most other U.S. companies. And daily active users for the Family of Apps increased from 2.88 billion last quarter to 2.93 billion this quarter, and year-over-year the DAUs increased about 4%. And daily active users for Facebook also increased from 1,930 million in the same quarter last year to 1,984 million this quarter – resulting in 2.8% year-over-year growth.

Meta Platforms Q3/22 Presentation

Of course, these are not impressive growth rates, but the company is still growing which is good news. During the earnings call, Dave Wehner stated:

So on time spent, we are really pleased with what we’re seeing on engagement. And as Mark mentioned, Reels is incremental to time spent. Specifically, in terms of aggregate time spent on Instagram and Facebook, both are up year-over-year and in both the U.S. and globally.

And while revenue stagnated, the total number of ad impressions served across the different apps increased 17%, which is a good sign for underlying growth. Growth was especially driven by Asia-Pacific and rest of world. On the other hand, the average price per ad decreased 18%, but the reasons might be temporary – like the shift to Reels.

Shift to Reels

Another reason for the top-line troubles is the move from Feed and Stories to Reels, as the monetization is still problematic. During the earnings call, Mark Zuckerberg commented:

Moving to monetization, I’ve discussed in the past how the growth of short-form video creates near-term challenges since Reels doesn’t monetize at the rate of Feed or Stories yet. That means that as Reels grows, we are displacing revenue from higher monetizing surfaces. And I think this is clearly the right thing to do, so Reels can grow with the demand that we are seeing, but closing this gap is also a high priority. Even with the progress we have made, we are still choosing to take a more than $500 million quarterly revenue headwind with this shift, but we expect to get to a more neutral place over the next 10 – sort of 12 to 18 months. I mentioned last quarter that Instagram Reels had crossed a $1 billion annual revenue run-rate. We continue scaling monetization across both Instagram and Facebook and the combined run-rate across these apps is now $3 billion.

And Reels is growing quickly and at a high pace. According to Zuckerberg, there are more than 140 billion Reels plays across Facebook and Instagram each day, which is a 50% increase from 6 months ago. And although this is not backed up by numbers, Zuckerberg believes that Meta is gaining time spent share on competitors like TikTok.

And the path for Reels monetization seems similar than the path towards monetization of Feeds or the switch to mobile. The company first had to focus on increasing engagement and growing demand for the products. Monetization efficiency followed in the next step. But Zuckerberg also admits it is hard to predict the monetization efficiency for Reels in advance.

New Ways of Monetization

Aside from trying to monetize Reels more efficiently, Meta Platforms is also seeing another major monetization opportunity in messaging. During the last earnings call, Mark Zuckerberg explained:

Beyond Reels, messaging is another major monetization opportunity. Billions of people and millions of businesses use WhatsApp and Messenger everyday and we are confident that we can connect them in ways that create valuable experiences. We started with click-to-messaging ads which lets businesses run ads on Facebook and Instagram that start a thread on Messenger, WhatsApp or Instagram Direct, so they can communicate with customers directly. And this is one of our fastest growing ads products with a $9 billion annual run-rate.

In the previous earnings call, the company already pointed out the big potential it sees in messaging. Meta Platforms reported strong double-digit year-over-year growth rates, and these messages are particular popular with small and medium-sized businesses in emerging markets like Brazil and Mexico.

Scary Metaverse

In my opinion, investors are mostly scared by Mark Zuckerberg’s plans for the Metaverse and the huge expenses necessary. By focusing on the Metaverse (and seeing it as a huge cash-burning fantasy of a billionaire), they are overlooking that Meta Platforms is still a solid, highly profitable cash cow (yes it is, even when it will struggle for a few quarters). And the vision of the Metaverse is generating uncertainty, and investors don’t like uncertainty.

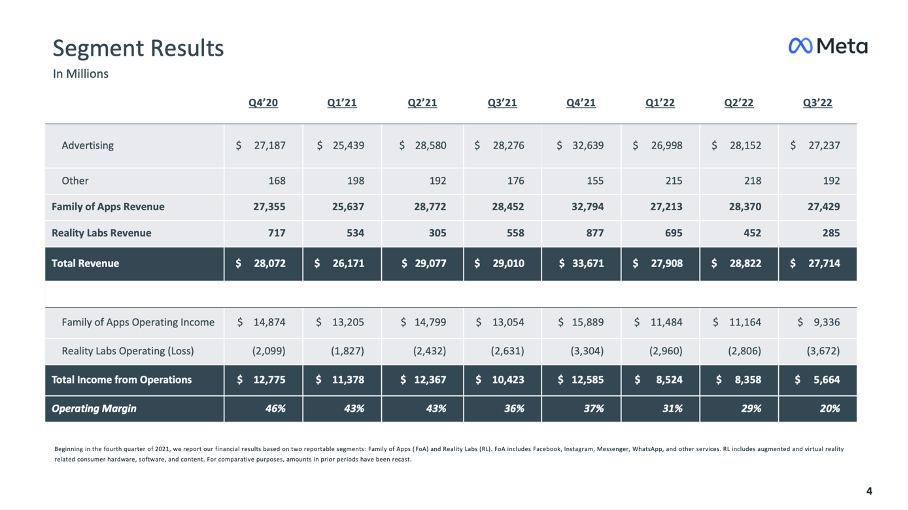

And there are reasons to be cautious (or even pessimistic). In the last few weeks, disappointing data about the Metaverse has been reported – about users not returning and fewer than 200k users signing up for the Horizon World. And when looking at the results for the third quarter of fiscal 2022, revenue for the Reality Labs business segment was only $285 million and 49% lower than in the same quarter last year. And not very surprisingly, the segment had to report an operating loss once again – $3,672 million. And when looking at the last eight quarters, this is the biggest operating loss for the segment so far.

Meta Platforms Q3/22 Presentation

What shocked investors in particular was the fact that Meta Platforms won’t cut down on spendings and will continue to rely heavily on its vision of the Metaverse. While total expenses for fiscal 2022 are expected to be in the range of $85 billion to $87 billion, management is anticipating full year 2023 total expenses to be in the range of $96 billion to $101 billion. And management is also anticipating that Reality Labs operating losses will grow significantly year-over-year.

And the voices are getting louder that Mark Zuckerberg should let go of his vision of the Metaverse and cut spendings to an absolute minimum. But Zuckerberg seems to hold on to his vision, and although he is acknowledging it will take time (several years) and several tries before the right platforms and apps exist, he is optimistic that Meta Platforms is on the right path:

Work in the metaverse is a big theme for Quest Pro. There are 200 million people who get new PCs every year, mostly for work. And our goal for the Quest Pro line over the next several years is to enable more and more of these people to get their work done in virtual and mixed reality eventually even better than they could on PCs. And to deliver a great work and productivity experience, I am excited about the partnerships that we announced with Microsoft, bringing their suite of productivity and enterprise management services to Quest; Adobe and Autodesk bringing their creative tools; Zoom bringing their communication platform; Accenture building solutions for enterprises and more.

Takeaway

In my opinion, we can break this story down in two key messages:

- Business Cycle: Meta Platforms is a company undergoing a cyclical low – like several other technology companies – and is therefore reporting low growth rates and is struggling on several fronts. Considering the fact that we are on the eve of a major recession it is not surprising for a business depending on advertisement revenue to report slowing revenue growth. And not only Meta Platforms is struggling – peers like Alphabet (GOOG, GOOGL), Amazon (AMZN), and Tencent are struggling as well.

- Investing in the future: Meta Platforms is investing in its huge vision of the metaverse, which is expensive and has a negative impact on the bottom line and the company’s ability to generate free cash flow.

These two aspects combined create a scenario that looks like Armageddon for Meta Platforms – but it is not. The first problem (the cyclical low) will pass, and revenue growth and profitability will increase again. The second problem (high expenditures) could actually be a huge opportunity for billions and billions in profits in the years to come. And this is even if the scenario that Meta Platforms is failing with its vision of the Metaverse and Facebook and Instagram just returning to normal ways of profitability after the recession is not priced in (the current stock price, at least).

Intrinsic Value Calculation

And as I have mentioned several times in the past, the Metaverse does not have to work out in any way for Meta Platforms to be a bargain. It is not like we are paying any form of premium for Meta Platforms on the hope of billions in profits from the Metaverse. Just returning to previous profitability levels and generating about $40 billion in free cash flow would make the stock worth about $150 (without any growth assumptions).

And although it sounds absurd right now, Meta Platforms should be able to grow in the mid-to-high single digits in the years to come. Not only have we to assume Meta Platforms being able to grow its top line again. Additionally, Meta Platforms could use share buybacks to grow its bottom line (if all the other growth initiatives won’t work). Last quarter, Meta Platforms spent $7,365 million on share buybacks, which is resulting in $29,460 million on annual share buybacks. At the current depressed stock price, this is enough to repurchase more than 10% of outstanding shares and add 10% growth to the bottom line. Combined with revenue growth, this would lead to double-digit growth for Meta Platforms.

Meta Platforms Q3/22 Presentation

Free cash flow in the last four quarters was $25,713 million and we are using this amount as basis in our calculation. For fiscal 2023, we assume 0% growth as the company is not so optimistic for the next years and the recession will have a negative impact. For the years from fiscal 2024 going forward (and till perpetuity), we assume only 5% growth. This is resulting in an intrinsic value of $182.69 (assuming 2,687 million outstanding shares and 10% discount rate). When assuming 6% instead, the intrinsic value would be $221.44, and these are still cautious assumptions.

Conclusion

In past articles I mentioned several times that I don’t like the term “buying opportunity of a lifetime” – especially as it was often used after small corrections implying that a 10% or 20% correction is already generating a deeply undervalued stock. But Meta Platforms is a huge buying opportunity, in my opinion, and the stock could easily double or triple over the next few years as Meta Platforms is trading nowhere close to its intrinsic value. In different calculations (which I did not include in this article), we also get an intrinsic value around $400 for Meta Platforms right now.

And in the coming quarters, bad news will continue as the recession, which will hit the United States with a high probability in 2023, will lead to more trouble for Meta Platforms. But at this point, most of the bad news should be priced in, and further bad news should not be a major shock. Over the next few years, you probably won’t regret an investment in Meta Platforms (and for the next few quarters just go to sleep, as we don’t know what will happen).

Be the first to comment