fcafotodigital/E+ via Getty Images

McCormick (NYSE:MKC) is a global manufacturer in the marketing and distribution of cooking ingredients to the entire food industry, which includes retailers, other food manufacturers, and foodservice businesses.

Their products include spices, seasoning mixes, condiments, and other flavorful products. Currently, they have the number one market share position in herbs and spices.

The business operates in two distinct segments, Consumer and Flavor Solutions. The Consumer segment, which represents approximately 60% of total net sales, sells spices, herbs, extracts, and other blends and sauces to the consumer food market.

The Flavor segment sells similar-type products, but their end-users are food manufacturers and the food service industry.

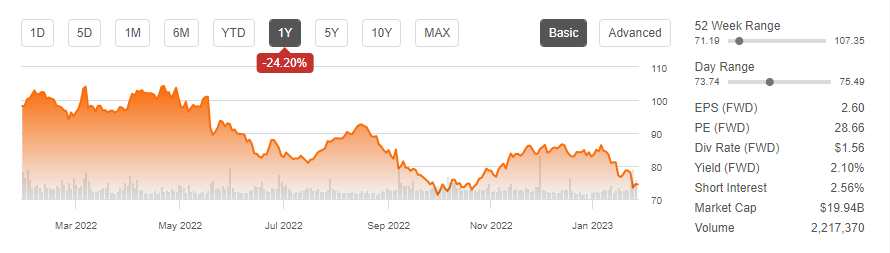

Over the past year, shares are down nearly 25%. In addition, they are down over 10% YTD. This contrasts unfavorably to the S&P 500 (SPY), which is currently in positive territory to start 2023.

Seeking Alpha – Basic Trading Data Of MKC

Following their Q4 earnings release, shares slipped further on weak performance and softer profit guidance. At present, the stock now trades near the bottom-end of their 52-week range at about 28.6x forward earnings. Despite its pullback, shares offer limited appeal to investors seeking new positioning. While their Flavor segment offers promising future growth potential, particularly in emerging markets, the unit is weighing on overall profitability. Recent cost-cutting initiatives may produce a turnaround, but it may prove beneficial to hold until the company produces more competitive results.

Q4FY22 Overall Sales And Operating Income Performance

In Q4FY22, MKC’s total reported revenues were down 2.3% YOY. This also missed estimates by +$80M. In constant currency, sales grew 2%. Though this was within guidance for 2022, it was still below management expectations for the quarter.

Contributing to the weaker than expected sales figures was greater-than-expected COVID-related disruptions in China, which unfavorably affected both consolidated sales and sales within their Consumer segment by about 2%. Excluding the impact of these disruptions, sales would have grown about 4% on a constant currency basis.

Other factors, excluding those relating to China, driving consolidated quarterly constant currency sales results was a 9% favorable impact from pricing-related actions, offset by a 2% volume decline relating to the divestiture of Kitchen Basics and their exits of low margin business in India and their Consumer business in Russia, as well as a 4% decline in all other volume and product mix.

Weaker sales paired with the higher cost operating environment resulted in a decline of 10% in adjusted operating income and a 13% decline in adjusted earnings per share (“EPS”).

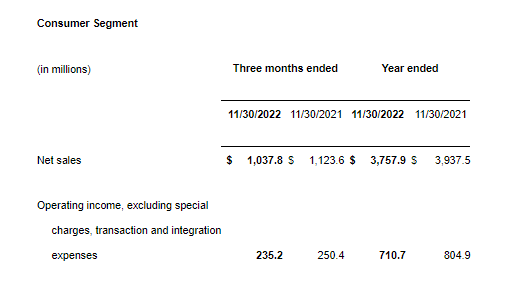

Q4FY22 Consumer Segment Performance

Within the segments, constant currency Consumer sales declined 4% YOY due to lower volume and product mix. This was partially offset by favorable pricing actions in all three of their operating regions.

In the Americas, Consumer sales were down 4%, with negligible impacts from currency. This decline was due in part to a 2% unfavorable impact from their previously mentioned divestiture of Kitchen Basics. In addition, difficult comparisons to elevated household restocking trends in 2021 also unexpectedly impacted results in the current quarter.

Q4FY22 Earnings Release – Summary Of Results Of Operations Of MKC’s Consumer Segment

Overall, consumer consumption grew 6%. Therefore, despite the challenging comps, their underlying volume performance in Q4 was still better than their Q2 and Q3 performance.

In the Europe, Middle East, and Africa (“EMEA”) regions, MKC turned in their strongest Consumer sales growth for the year in Q4.

This in-turn resulted in market share gains relative to both 2019 and 2021 in herbs, spices, and seasoning in their U.K. and Eastern European markets. These gains were partially offset by softer performance in France.

The overall strong sales performance in the region was primarily attributable to improved price realization and improvements in volume.

In the Asia/Pacific region, Consumer sales were hit by weakness relating to COVID-related disruption in China as well as their exit of lower margin business in India.

On an overall constant currency basis, Consumer sales in the region were down 22%. And over the last three years, quarterly sales have now declined at an 8% compound rate, driven by volume declines in both China and India.

In addition to weaker sales, the Consumer segment also turned in a 5% decline in constant currency operating income, due largely to the inflationary cost environment.

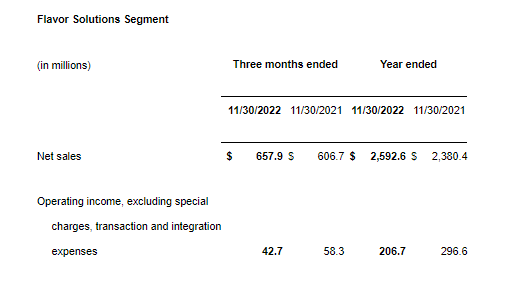

Q4FY22 Flavor Solutions Segment Performance

In their Flavor Solutions segment, sales remained robust, led higher by both pricing actions and higher base volume growth in new products. Overall, constant currency sales were up 14%.

Q4FY22 Earnings Release – Summary Of Results Of Operations Of MKC’s Flavor Solutions Segment

Leading the way higher in sales was their EMEA region, which reported 16% constant currency sales growth. This was attributable to strong growth to quick service restaurants (“QSR”) and packaged food and beverage customers.

Supplementing the strength in their EMEA region was 13% and 11% sales growth in their Americas and Asia/Pacific region, respectively.

Despite outstanding sales growth in the segment, MKC is still not realizing profit growth. In the quarter, operating income was down 26% in constant currency terms, driven by inflationary cost pressures, elevated costs to meet rising demand, unfavorable product mix, and increased spending related to supply chain investments.

Post-Earnings Insights

MKC is not heading into 2023 with their best foot forward. Overall sales in the final quarter of the year came within range of guidance, but below management’s own expectations.

Weakness in the Asia/Pacific region primarily resulting from the disruptions in China was the main culprit. But an expectedly difficult comparative environment to last year relating to restocking trends was another driver of volume weakness.

While favorable pricing blunted some headwinds, operating income still logged declines for the period.

One positive growth engine is their Flavor Solutions segment, which continues to drive double-digit sales increases in all regions. Shifting consumption trends to healthier home-cooked meals is likely to serve as a tailwind for this segment in future periods as consumers increasingly seek out more innovative ways to enrich their meals.

Despite its positive impact on sales, however, the Flavor segment is not profitable. In the current quarter, for example, operating income was down 26% in constant currency terms. Adjusted operating income in the Consumer segment, by contrast, was down just 5%.

Looking ahead, recently announced cost-savings measures could result in a boost to earnings in future periods. These measures include the elimination of +$100M in supply chain costs over the next two years paired with organizational streamlining actions, which are expected to generate an incremental +$25M in cost savings. Together, the company is expected to realize about +$75M in 2023.

As a result of these measures, Bernstein recently upped their price target to $90/share. This would represent upside of about 20% from current trading levels. This, however, may be a bit ambitious. While MKC’s EPS targets are expected to be lower in 2023, they do expect to increase sales by 5-7%, which is notably above consensus estimates of about a 3.4% increase.

The higher sales expectations could produce further share price declines on any miss. And given the current environment, where an increasing number of consumers are trading away from more expensive brands to private label, the sales outlook could be even more challenging in 2023.

At nearly 29x forward earnings, shares trade near historical five-year averages but are well above the average multiple commanded by the broader S&P, which is approximately 17x. For investors seeking a bargain addition to their long-term portfolios, MKC didn’t provide enough conviction on their most recent earnings release to justify new positioning.

Be the first to comment