The COVID-19 pandemic continues to disrupt all areas of the economy. However, there are few companies whose business models are relatively resilient to this challenge and hospital supply companies top the list. As the global healthcare system continues to fight this pandemic, there has emerged an acute shortage of critical care products including ventilators, ICU smart beds, patient monitoring and diagnostics, and physical assessment tools and consumables.

In this backdrop, I believe that the healthcare sector in general and the hospital supply sector, in particular, can be more immune to long-term disruptions. While all sectors have suffered in some of the other ways, healthcare stocks are bound to be less affected than other economy dependent sectors such as energy, retail, hospitality, restaurants, and tourism.

Masimo Corporation (MASI) and Hill-Rom Holdings (HRC) are the two companies that may not only withstand but can also see some upside in these COVID-19 times. We are going for companies with a COVID-19 resilient business model, which are profitable, and do not require to raise capital on an urgent basis. Here, let us check the key growth drivers and risks of these healthcare stocks.

{kind=link}

Masimo Corporation

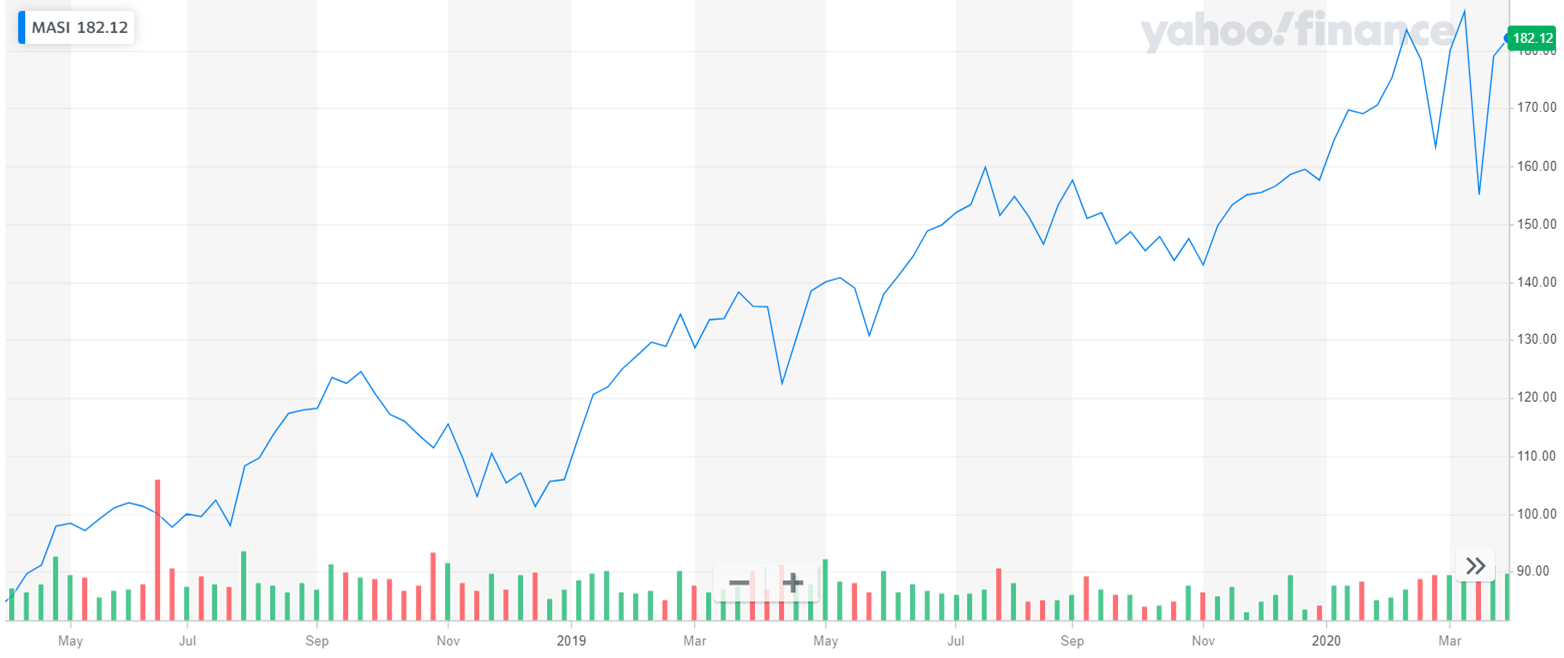

Masimo Corporation is up by 15.22% in 2020 YTD (year-to-date). Compare this with the S&P 500’s 22.97% YTD drop, and Masimo’s performance seems nothing less than remarkable. Even in March 2020, when almost all stocks got battered, Masimo was fast to recover. In fact, the company has gained 1.93% in the last one month. The jump, howsoever small, is a positive one. Masimo Corporation’s market capitalization is $9.89 billion.

Masimo Corporation is in the business of noninvasive monitoring technologies and hospital automation solutions. The company’s major product offerings are Masimo SET (Signal Extraction Technology) pulse oximetry, Masimo rainbow SET platform to noninvasively and continuously monitor twelve major blood parameters, and SedLine brain function to measure the brain’s electrical activity. Recently, the company has come out with Patient SafetyNet, surveillance, remote monitoring, and clinician notification solution targeted at controlling opioid use in post-surgical settings.

Almost all of Masimo’s product offerings are mostly used in non-elective procedures. Besides, the company is also bound to see increased demand for its ventilators and patient monitoring solutions for managing COVID-19 admissions. Masimo Corporation has also launched a dedicated range of products to address the COVID-19 pandemic. These include surge capacity management support solution, home monitoring and telemedicine solutions, and infection control and prevention solutions.

To further leverage the opportunity, the company has also announced the acquisition of an innovative ventilation company, TNI medical AG. The latter’s novel softFlow technology is designed to provide high flow, warmed and humidified respiratory gases to spontaneously breathing patients suffering from serious pulmonary conditions. With infection rates spiking in Europe and the U.S., these COVID-19 targeted products will be increasingly required to manage the disease while ensuring quality and controlling costs.

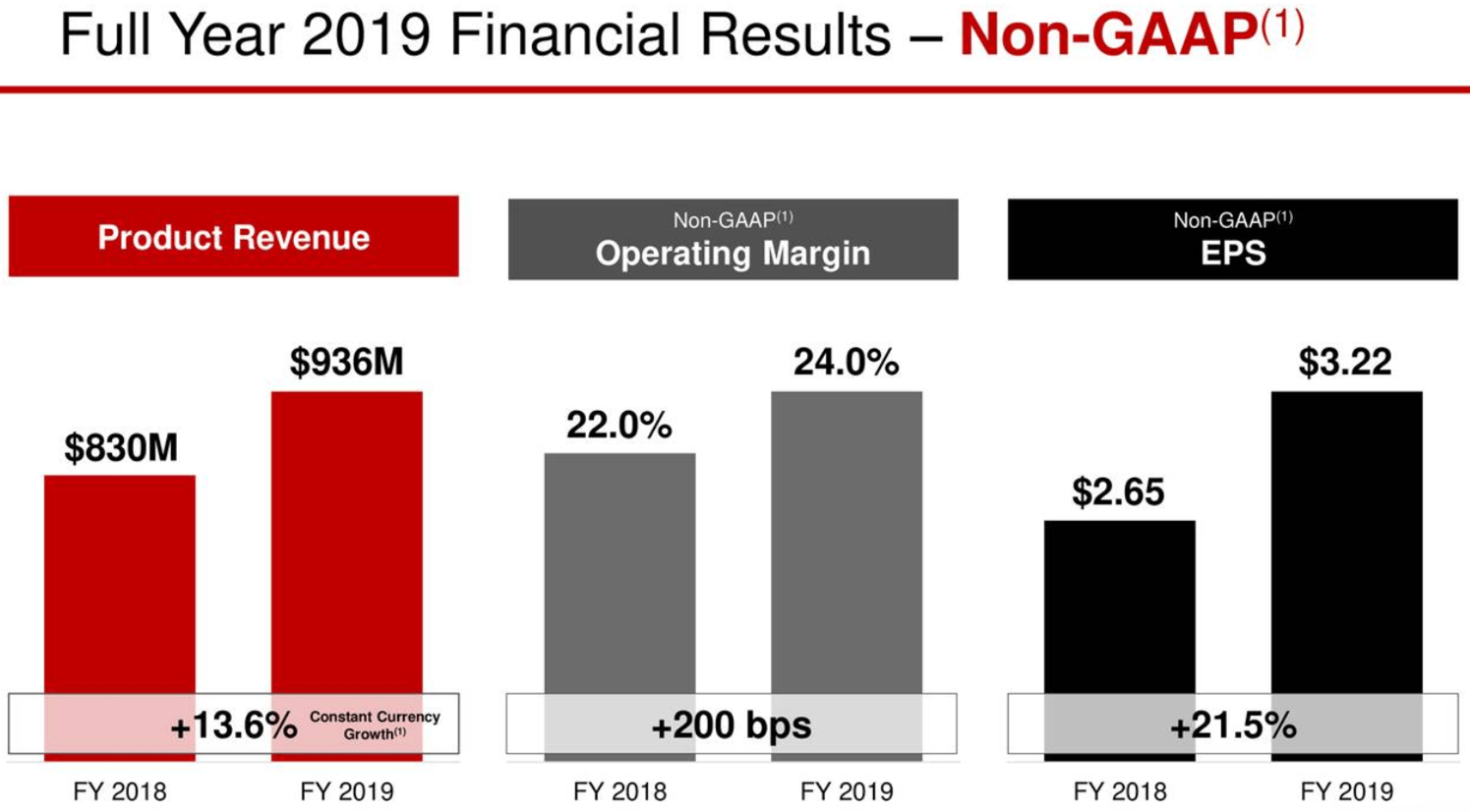

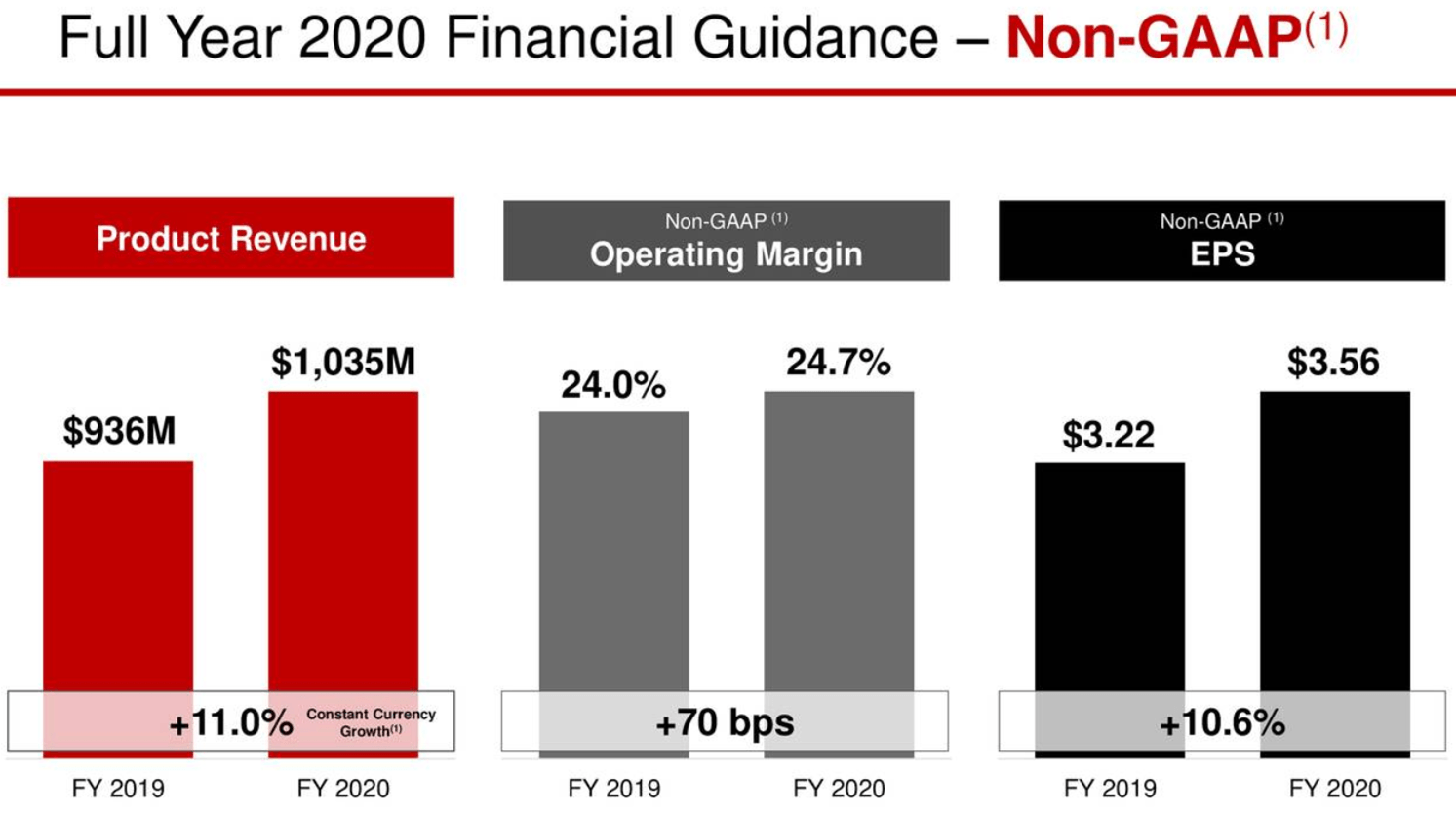

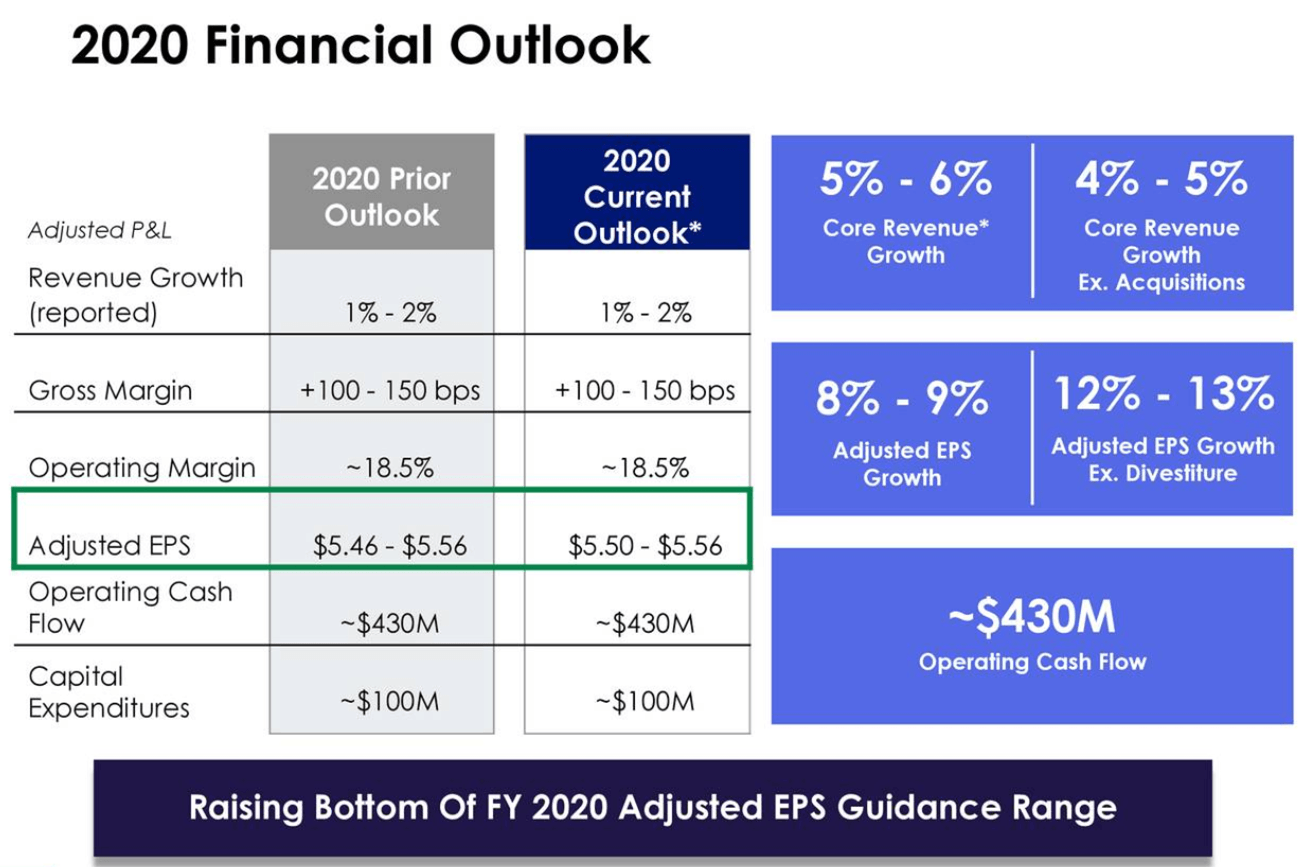

The company is profitable and reported solid double-digit revenue and earnings growth in 2019.

The majority of MedTech stocks are down due to expectations of lowered capital spending from healthcare providers affecting their topline and bottomline in 2020. Masimo, however, may not face much of a downward impact considering that hospitals would require to purchase these critical care products to improve outcomes and control costs even for COVID-19 patients. It is essential to accurately monitor oxygen saturation levels of COVID-19 patients who are suffering from respiratory distress.

The current median analyst price target on MASI is $196.20 a share, only 7.73% above the current trading level of the stock. I feel that this is a conservative estimate in current times. Instead, Piper Sandler’s target price of $201 seems to better reflect the growth potential in this relatively COVID-19 resilient stock. Investors seeking out higher returns can choose for a lower entry point, close to $170.

Lofty valuations with P/E (price-to-earnings) of 52.99x and a forward P/E of 44.93x is a major risk for the company. Such valuations expose the stock to significant downward volatility in the face of any unfavorable news or earnings miss. The second key risk for the company is the lower percentage of recurring revenues.

Hill-Rom Holdings

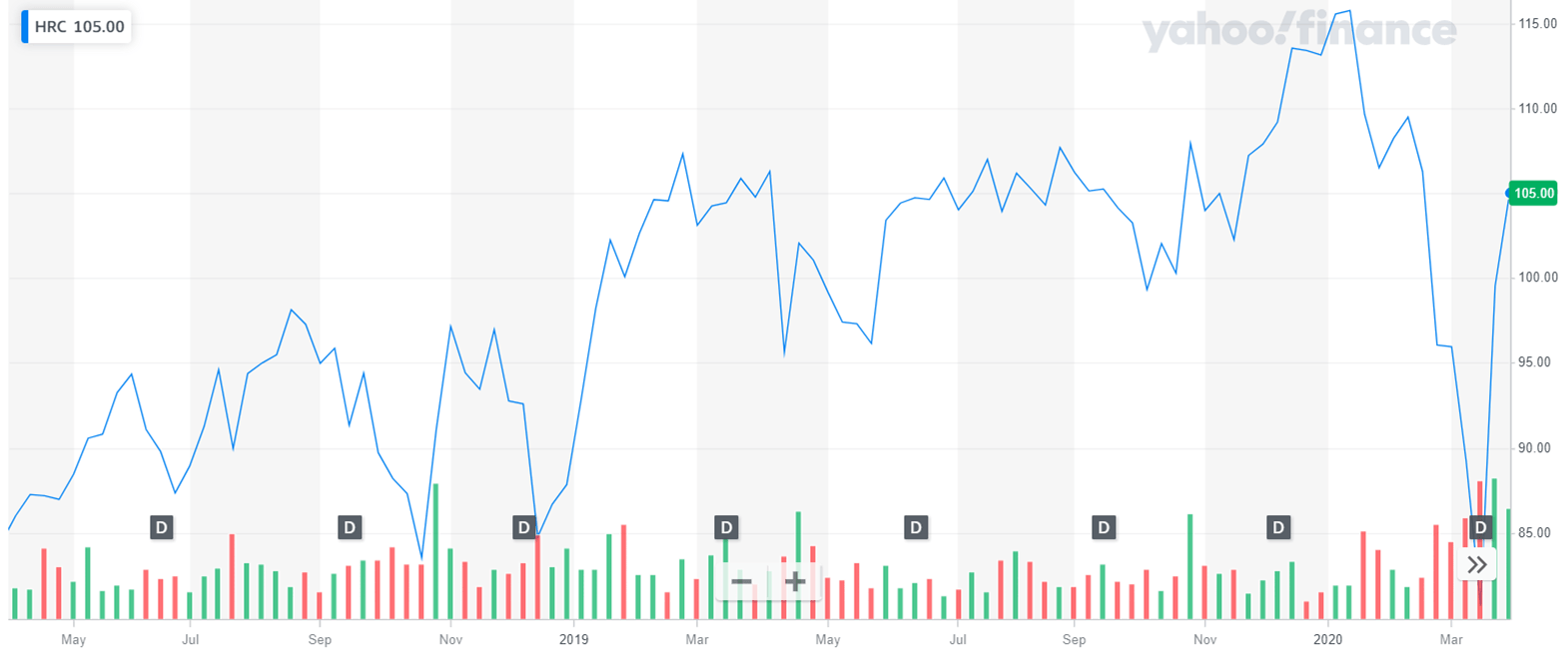

Hill-Rom Holdings is down 7.51% YTD, much lower than the S&P 500’s downtrend in the same time frame. The stock had dipped to $74.88 on March 23 but started recovering almost immediately. The stock is already up by 4.36% in the last one month, a feat in current times. The company’s market capitalization is $7.22 billion.

Hill-Rom Holdings is in the business of Patient Support Systems, Front Line Care, and Surgical Solutions. The company’s product offerings include medical-surgical beds, intensive care unit beds, bariatric patient beds, lifts and other devices, non-invasive therapeutic products and surfaces, and information technologies and software solutions. The company also offers patient monitoring and diagnostics products, such as patient exam and diagnostics, patient monitoring, diagnostic cardiology, vision screening, and diagnostics products, and respiratory health products comprising Vest System, VitalCough System, MetaNeb System, Monarch, and Life2000 systems. The company offers surgical solutions that include surgical tables, lights, and pendants; positioning devices for use in the shoulder, hip, spinal, and lithotomy surgeries, as well as platform-neutral positioning accessories for operating room tables. Hill-Rom Holdings either sells these products or offers them on rent to healthcare providers.

Hill-Rom Holdings’ products remain in high demand for battling the pandemic. Besides, the delay in elective procedures will have a limited impact on Hill-Rom, since Surgical Solutions is a much smaller revenue contributor for the company.

On March 24, Hill-Rom announced that it is ramping up production to more than the double capacity for its respiratory products, ICU and med-Surg unit smart beds, and Patient monitoring and diagnostics products. In respiratory health, the company is working to increase its production capacity of a non-invasive ventilator currently approved in the U.S., Life2000, five-fold on an annualized basis. This portable and lightweight ventilator can be used for treating COVID-19 patients with mild to moderate respiratory distress across various acute care settings. The company anticipates increased demand for Life2000, which will, in turn, help free up capacity for invasive ventilators for the most serious COVID-19 patients. Besides, the company is also working to ramp up capacity of Progressa ICU bed, Centrella Smart+ bed, Hillrom 900, Hillrom 900 Accella, Connex and Spot Vital Signs monitors, and physical assessment tools and consumables, including thermometry, probe covers and blood pressure devices and cuffs. The company has not reported any material interruption to its business operations.

On April 2, President Trump issued an order under the Defense Production Act to ensure that domestic manufacturers can produce ventilators. The order mentions Hill-Rom as one of the key domestic manufacturers of ventilators. The order will ensure that Hill-Rom has stable access to all the supplies required to manufacture ventilators.

Hill-Rom Holdings has been a profitable company and is expected to report decent revenue and earnings growth in 2020. I do not expect to see much downward revision in Hill-Rom’s 2020 guidance, which is not what can be said for the majority of the companies in the market.

The current median analyst price target on HRC is $122.75 a share, only 16.90% above the current trading level of the stock. Barclays has set a target price of $116, while Morgan Stanley’s target price is $138. I believe that $122.75 is a pretty achievable target price for the company which offers a favorable risk-reward position to retail investors.

Although less expensive than Masimo, Hill-Rom Holdings is definitely not a cheap stock. The company is trading at P/E of 47.32x and a forward P/E of 17.20x. These numbers seem high, considering the low topline and bottomline growth rate of the company. Such high valuations result in high share price volatility. Hill-Rom Holdings also carries a total debt of $2.09 billion with long-term debt of $1.77 billion, while cash holdings are only $204.40 million. Although I do not see this affecting the company’s operations, investors should remember that Hill-Rom definitely does not boast of a pristine balance sheet.

Considering the change in business dynamics, I believe that these two stocks can be safe bets during the COVID-19 pandemic. Retail MedTech investors with above-average risk appetite and an investment horizon of at least a year can consider going for these companies in April 2020.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment