cotuvokne/iStock via Getty Images

Marubeni (OTCPK:MARUY)(OTCPK:MARUF) is yet another Japanese trading conglomerate that does business by owning interests in a host of assets and businesses. Breaking down its segments exposure we see some positives, such as structural supply challenges that support the price in many of its commodity markets. Moreover, it has a decent chunk of less cyclical businesses that aren’t a bet on the continuation of the commodity cycle. Comprehensively, its multiple looks low based on the relative valuation of its largest parts with peers, but the problem is there’s no yield. Efforts are being focused on a pretty rapid deleveraging, but modes of capital return could be a little limited as is often the case with Japanese companies. A yield may develop but payout may be too low.

Q3 Discussion

First let’s discuss Marubeni’s businesses in Q3.

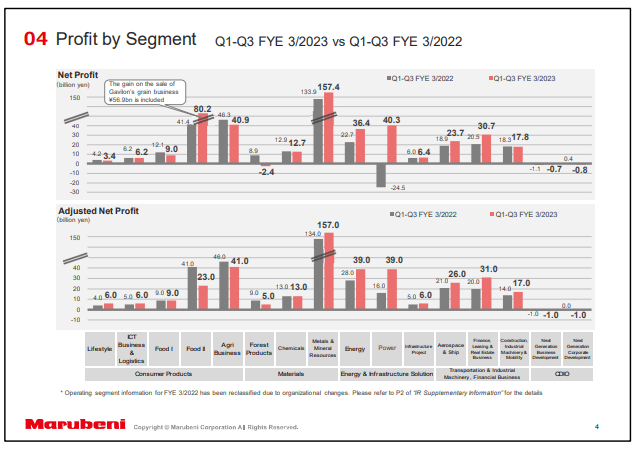

Segments (Q3 2023 Pres)

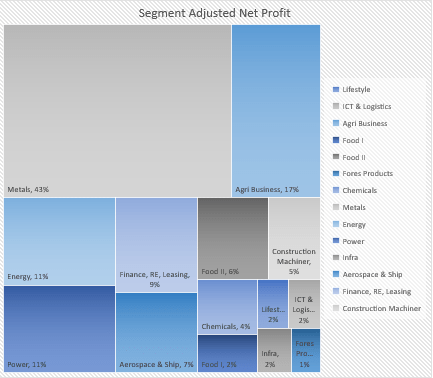

We’ve broken down the segment exposures into a treemap.

Segments (treemap) (VTS)

Metals are the biggest exposure. The assets here are smelters, iron ore mines, and ash coking facilities. So in other words their exposures are the coking of coal for metallurgical purposes, not for burning for energy which remains an essential use of coal that is not being phased out, as well as the vertically integrated production of steel products. We estimate about a 50:50 net income split between the steel and coking businesses based on price changes in steel and coal as well as evolutions in net income, so a 5-6x PE makes sense coming from these businesses based on peers. This business is forecast to flatten in Q4 as steel prices average at similar levels to last year, and metallurgical coal prices come down rapidly from highs.

Next is agricultural businesses, which essentially comes down to fertiliser and pesticide production – so an agrichem business. Comps in fertiliser production can trade around 9-10x PE with similar leverage, and specialty chemical producers could trade even higher within the crop protection products sphere. This is another business advantaged by the fallout from the Ukraine war due to Russian capabilities of producing fertilisers. Prices have been falling here, and they are forecast to continue falling at this rate into Q4, but income is relatively resilient.

The energy business is quite diversified, but it includes LNG plans, E&P interests, but also nascent hydrogen infrastructure and Uranium mines. The net income evolutions demonstrate that LNG is probably more important than their crude production in this business. Probably a 6-7x PE would make sense for these businesses, based on similarly diversified peers with similar leverage.

The power business is very easy to understand as it’s a bunch of power generation assets. Generation focused utilities trade highly, easily above 20x in PE. The growth here was pretty phenomenal thanks to sales in the UK of wholesale electricity. The especially high generation prices are somewhat likely to persist, but declines are being observed as we get closer to closing out the FY results with Q4 included, which net gains in power prices being slashes down by a quarter according to forecasts.

The rest of the exposures are more centre-lane industrial exposures but also food exposures, but less so after a grain business divestment. Industrial exposures make sense to value at long-term market average PEs at around 15x, but 80% of the businesses have been accounted for more specifically.

Bottom Line

Marubeni sits at around a 5-6x PE, which is already lower than their average large exposures. There probably is some value here, and the rapid deleveraging is at least reducing financing costs. However, there is absolutely no yield, and Japanese companies tend to keep payouts very low. While not a net-cash proposition, where capital return is even more dependent on payout policy, reticence of allocators to come in and help close gaps is an issue. Moreover, the coal exposures may exclude it by ESG mandates. Still, the company is cheaper than an average of its parts’ multiples. Our concern is the commodity exposures, we don’t want to make new bets on that cycle anymore.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment