JHVEPhoto

One of the companies hit hard by the COVID-19 crisis was Marriott International, Inc. (NASDAQ:MAR). And in my last article about the company that was published in December 2021, I still considered COVID-19 as one of the major risks for the business. Now that worldwide traveling is returning almost to “normal” levels again, we see another risk rising for Marriott International – a potential global recession. And considering these risks surrounding the business, I still don’t see it as a solid investment, as I will explain in the following article. But, let’s start with some positive aspects.

Improving Results

One positive aspect about Marriott international we can mention are the improving quarterly results. In the first quarter of fiscal 2022, Marriott generated a total revenue of $4,199 million and compared to $2,316 million in Q1/21 this is an increase of 81.3% YoY. Operating income could multiply from $84 million in the same quarter last year to $558 million in Q1/22, and diluted earnings per share improved from a loss of $0.03 in Q1/21 to $1.14 this quarter. Of course, we always must keep in mind that we are comparing the current quarter with one of the worst quarters in a long time, and therefore high growth rates are not surprising.

Marriott International FactBook

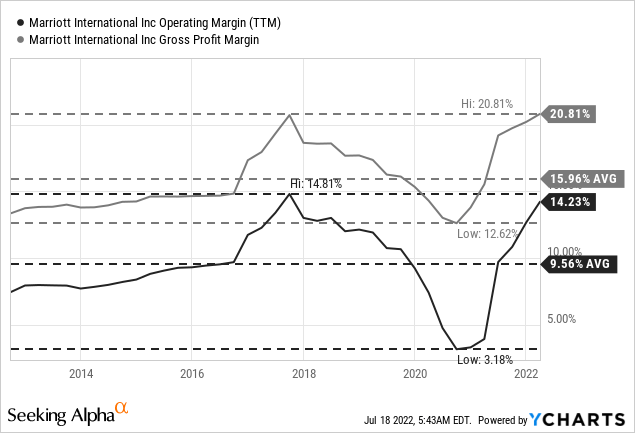

And we also see improvements over the last few quarters. While revenue hasn’t reached pre-crisis levels yet, Marriott is more profitable than before the pandemic. While operating margin has almost reached the same levels as in 2017 again, gross margin is at the highest level it has been in a long time. And as a result, operating income as well as earnings per share are higher than they were in the quarters before the COVID-19 crisis.

And aside from revenue and earnings per share, different metrics (like the revenue per available room) also improved, as Marriott stated in its May press release:

In the 2022 first quarter, worldwide RevPAR increased 96.5 percent (a 95.5 percent increase using actual dollars) compared to the 2021 first quarter. RevPAR in the U.S. & Canada increased 99.1 percent (a 99.1 percent increase using actual dollars), and RevPAR in international markets increased 88.5 percent (an 84.8 percent increase using actual dollars).

Balance Sheet Improved and Dividend Resumed

Aside from improved results, Marriott International could also improve its balance sheet. On March 31, 2022, the company had $8,738 million in long-term debt as well as $731 million in short-term debt on its balance sheet (resulting in $9,468 million in total debt). And compared to $10,057 million in debt one year earlier this is a reduction by 6%. During the same timeframe, total equity also improved from only $234 million one year ago to $1,772 million on March 31, 2022. And cash and cash equivalents also increased from $628 million on March 31, 2021, to $1,042 million on March 31, 2022.

While the balance sheet clearly improved, Marriott International still has a debt-equity ratio of 5.34 and it would still take almost 4.5 times the operating income of the last four quarters to repay the outstanding debt. And while we should not be concerned about those numbers, the balance sheet is still not great.

Aside from improving the balance sheet, Marriott International also resumes paying a cash dividend and the company will pay a quarterly dividend of $0.30. And although this is still lower than the dividend before the COVID-19 crisis (which was $0.48) it is a positive sign.

However, we can identify at least three reasons why Marriott International is probably not a great investment right now – starting with COVID-19, which is still an issue.

Reason I: COVID-19

In my last article about Marriott International, I mostly focused on the risk presented by COVID-19. Now, about eight months later COVID-19 still seems like an issue that is not completely resolved. We certainly don’t know what the next fall and winter will bring and as mentioned in my last article, we don’t know what long-term effects the pandemic will have on business travelling. It might be a possibility that conferences and meetings will be less in-person and business traveling will decline a bit. And when talking about this issue we should also keep in mind that society can’t really afford to travel and fly the same way it has before when taking climate change seriously.

Reason II: Recession

And while these might rather be mid-to-long-term trends, there is another risk for the next few quarters: the recession that seems already visible on the horizon. And while we can argue that Marriott is rather focused on high-income individuals that might not be affected so much by the recession (as it is especially the low- and mid-income population that is affected) the past recessions are painting a different picture.

When looking at the last three recessions, we can see steep declines for earnings per share, and especially after the Great Financial Crisis it took several years before Marriott could reach pre-crisis levels again. And for the next recession, we must assume a similar negative effect on Marriott’s business, and we must assume declining revenue as well as declining earnings per share. Especially for earnings per share, it seems likely that the business will report a loss for one or several quarters once again.

Reason III: Valuation

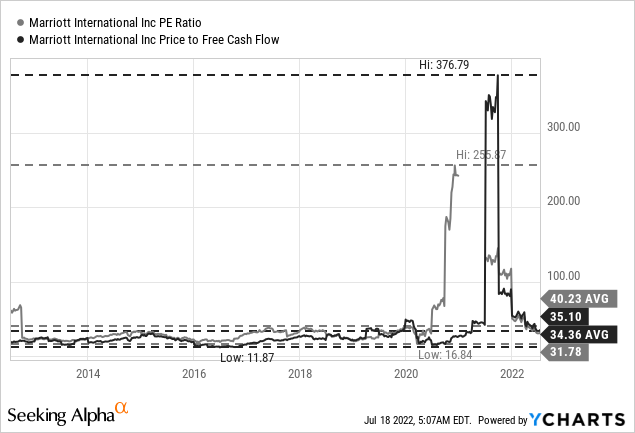

And a third risk (or reason not to buy Marriott International) is the valuation of the stock. When looking at the simple valuation metrics we see the stock trading for 32 times earnings per share as well as 35 times free cash flow. And although valuation multiples constantly declined over the last few months and the valuation multiples are in-line with the 10-year average numbers, I still don’t consider Marriott being cheap. Valuation multiples above 30 might be justified for companies growing with a high pace but considering the upcoming recession I don’t think these P/E ratios or P/FCF ratios as justified for Marriott.

When trying to calculate an intrinsic value for Marriott International, we can also use a discount cash flow calculation. As basis we can use the free cash flow of the last four quarters, which was $1,346 million. When taking 330 million outstanding shares and a 10% discount rate, Marriott must grow its free cash flow almost 11% annually for the next decade followed by 6% growth till perpetuity to be fairly valued.

But especially for the next two or three years, we should not assume high growth rates. Considering a potential recession, we rather must assume declining earnings per share and declining free cash flow. And we should also be a little cautious about the capital expenditures. The numbers in the last few quarters were extremely low. In the last four quarters, capital expenditures were only $202 million compared to about $600 million in capital expenditures in previous years. And while it is possible for Marriott to reduce capital expenditures for some time, it is not possible for a longer time without negative impacts on the business. And therefore, we must assume higher capital expenditures in the years to come which will lead to lower free cash flow.

Conclusion

Marriott International is still not a great investment and we should be rather cautious. Not only is COVID-19 still an issue and we don’t know what the next fall and winter will bring, but the looming recession is also a huge threat for Marriott International as earnings per share could decline similar to previous recessions. And when considering that Marriott is trading for a higher share price as before the pandemic, we can’t consider Marriott as cheap, and it is not an investment I would make at this point.

Be the first to comment