DjelicS

Take a look at the bond market now.

See what investors seem to be expecting.

The yield on the 2-year U.S. Treasury note (US2Y) is around 4.15 percent.

The yield on the 10-year U.S. Treasury note (US10Y) has recently been around 3.45 percent.

The yield on the 10-year U.S. Treasury Inflation Protected securities (10YTIPS) (“TIPS”) has been around 1.35 percent.

Economic Recession

So, the first conclusion that I draw from this is that investors are expecting a recession.

The yield spread on the nominal Treasury issues is a negative 0.700.

When the Treasury yield curve has a negative spread, an economic recession usually follows.

U.S Treasury spreads have been negative since early July of last year. That is, we have had a negative term structure of interest rates for over seven months. During this time, the term structure has become more negative.

So, the investment community appears to expect a recession relatively soon, and the recession will not just be a short, minor one.

Receding Inflation

The second conclusion that can be drawn from these market numbers is that inflation is supposed to drop.

And, the drop is expected to be relatively substantial.

If one subtracts the yield on the 10-year TIPs from the yield on the 10-year nominal U.S. Treasury note, one comes up with an expected inflation rate of 2.10 percent.

Note that the goal of the Federal Reserve is to achieve a 2.00 percent rate of inflation.

The Fed’s Picture

These numbers are actually quite consistent with the most recent projections of the Federal Reserve System.

In terms of economic growth, the real economic growth of the United States is expected to be 0.5 percent in 2023. This follows an expected 0.5 percent rate of growth, year-over-year in 2022, and a 1.6 percent, year-over-year rate of growth in 2023.

Whether these numbers qualify as a recession is not clear, but it is clear that the Federal Reserve does not expect economic growth to improve any in 2023. In fact, the growth rate expected to be achieved after 2023 is below 2.0 percent.

This is not a very active economy in terms of economic growth.

As far as inflation is concerned, the Federal Reserve sees the inflation rate dropping to 2.0 percent, right on target within a four or five-year period.

Thus, one can make the argument that the investor expectations built into the bond market are quite consistent with the economic future the Federal Reserve sees for the United States economy.

How We Got Here

The term structure of interest rates turned negative in early July of this year.

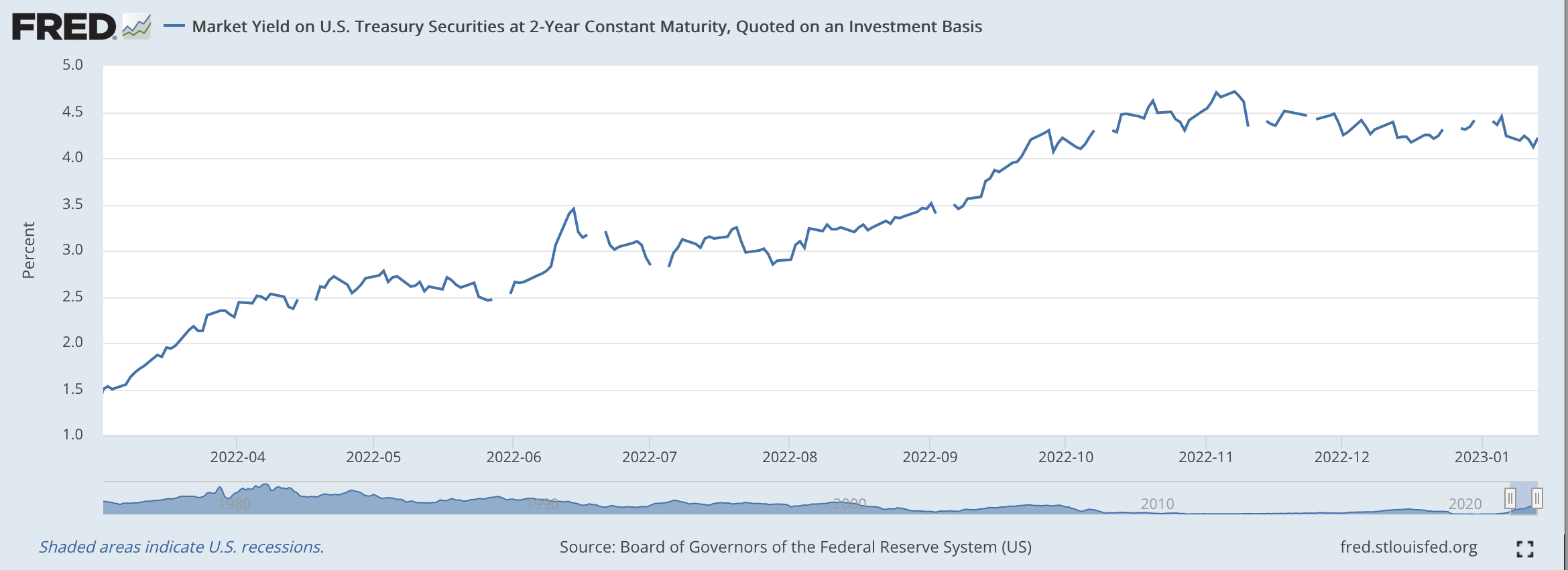

As the Federal Reserve tightened up on monetary policy this year, the yield on the 2-year U.S. Treasury note rose quite rapidly.

Yield on 2-year U.S. Treasury Note (Federal Reserve)

Note that the 2-year yield rose relatively rapidly at the first and then began to taper off beginning in November 2022.

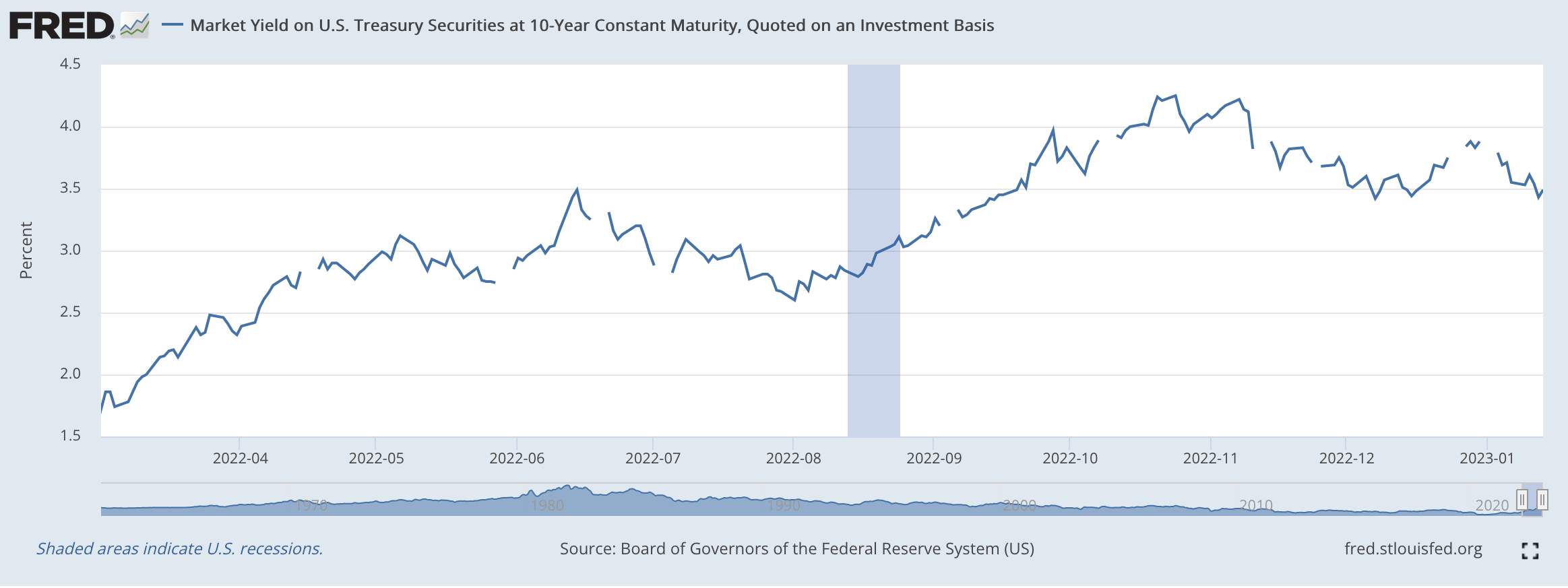

The yield on the 10-year U.S. Treasury note acted a little bit differently.

Yield on 10-year U.S. Treasury note (Federal Reserve)

Note that the yield on the 10-year Treasury note did not continue to rise through the summer, as did the yield on the 2-year Treasury note. Also note that since November 2022, the yield on the 10-year U.S. Treasury note has actually declined.

This is a little bit unusual, to have the longer-term yield drop at this time.

In most of the cases, historically, the yield curve keeps its negative tilt, but the longer-term rate continues to rise with the shorter-term rate but at a slower pace.

Thus, the yield curve becomes more negative, but with both yields rising.

One could argue that in the current case, investors have taken quite seriously the commitment of the Federal Reserve to reduce inflation and have taken the Fed’s “forward guidance” to heart.

But, this raises another question.

Many times over the summer and fall, it has appeared as if the investment community did not believe the Federal Reserve was going to stick by its plans to battle inflation and “pivot” away from the tight monetary policy.

The consequences of this thinking resulted, many times, in stock prices rising on some whim that the Fed would soon cease to keep to its program to reduce inflation to 2.0 percent.

Right now, I don’t have an answer for this concern.

In one case, the case of the expectations built into the bond yields, it appears as if investors are right in line with Federal Reserve signals, whereas in another case it appears as if investors believe that the Fed will back out of the inflation fight before inflation is fully brought under control.

We need to investigate more into this concern.

Inflationary Expectations

In terms of inflationary expectations, we look at the movement in the yield on the TIPs to see how investors saw changes in inflationary expectations taking place over time.

Here is how the yield on 10-year Treasury Inflation Protected securities moved over the same period of time.

Notice that in March, when the Federal Reserve began to tighten up its monetary policy, the yield on 10-year TIPs was in negative territory.

Now, the yield on these 10-year TIPs is over 1.3 percent. During this time period, the yield got up around 1.5 percent.

Note that the yield on the TIPs notes can be used to represent investors’ expectations about what the real rate of growth of the economy might be.

Remember, from above, the Fed’s projections of economic growth over the “longer run” was in the 1.6 percent to 1.8 percent range.

Thus, these investor expectations built into the yield on the Treasury’s inflation protected securities are not that much different from the expected rate of real economic growth built into the Treasury securities.

Again, the investment community seems to be in about the same place as Federal Reserve officials.

Summing Up

It feels a little strange to me to have investor expectations so in line with the forecasts of the Federal Reserve.

In one sense, it says that the Fed’s forward guidance is really being taken seriously by the investment community.

If this is the case, then the behavior of the financial markets in the next year or two should be relatively stable.

This, of course, would be a very good result.

However, there are other market situations, like investors looking for the Fed to “pivot” from its current restrictive position, that don’t match up with this.

This is why investors need to continue asking questions about what is going on. In a time of radical uncertainty, like the one we are now in, we must try to keep on top of all market situations.

Be the first to comment