It’s time to talk about oil and one of the best stocks to trade oil. In early July, I covered the political impact on the supply side of oil in an article with the very political title “The New Liberal Order Makes Marathon Oil A Strong Buy”. In this article, I’m going to build on that as new developments have happened. Recession fears have hit the market, pressuring energy commodities and everything related to that. However, oil is starting to rally again as we’re seeing clear signs of what could be a commodity super cycle. That’s fantastic news for Marathon Oil (NYSE:MRO), thanks to its low breakeven drilling prices, healthy balance sheet, and its focus on buybacks, which should help long-term total returns.

So, without further ado, let’s get to it!

It’s A New Energy Era

In my last article, I used the words of one of President Biden’s highest advisors, who made the case that the “Liberal world order” demands enduring high gas prices.

New York Post

The New York Post – among many others – reported that National Economic Council director Brian Deese (Biden’s personal advisor) had a somewhat unexpected answer to the following question asked by CNN:

“What do you say to those families who say, ‘Listen, we can’t afford to pay $4.85 a gallon for months, if not years. This is just not sustainable?”

He answered:

“What you heard from the president today was a clear articulation of the stakes,” Deese answered. “This is about the future of the liberal world order and we have to stand firm.”

Now, as I’m not in the business of starting a political discussion, let me elaborate on this by showing you comments from the IEA. Headquartered in Paris, France, the International Energy Agency is what they call an autonomous intergovernmental organization that provides policy recommendations, analyses and data, and coverage of global energy markets.

For example, the IEA is working with the European Union on challenging energy problems in times of the Russia/Ukraine war.

Earlier this year, the organization asked a key question in one of its many reports.

A key question is what today’s energy crisis means for fossil fuel investments if we are still to achieve our collective climate goals. Are today’s sky-high fossil fuel prices a signal to invest in additional supply or a further reason to invest in alternatives?

The answer is exactly why I am bullish on fossil fuels as the answer – according to the IEA – is accelerating investments in renewables.

In the IEA’s landmark Roadmap to Net Zero Emission by 2050 published in May 2021, the analysis indicated that a massive surge in investment in renewables, energy efficiency and other clean energy technologies could drive declines in global demand for fossil fuels on a scale that would as a result require no investment in new oil and gas fields.

The need for this clean energy investment surge is greater than ever today. As the IEA has repeatedly stated, the key solution to today’s energy crisis – and to get on track for net zero emissions – is a dramatic scaling up of energy efficiency and clean energy.

The IEA is not wrong – theoretically speaking. By reducing demand for fossil fuels, prices will be pressured. There are, however, (at least) two problems.

Problem 1: Oil drilling risk management

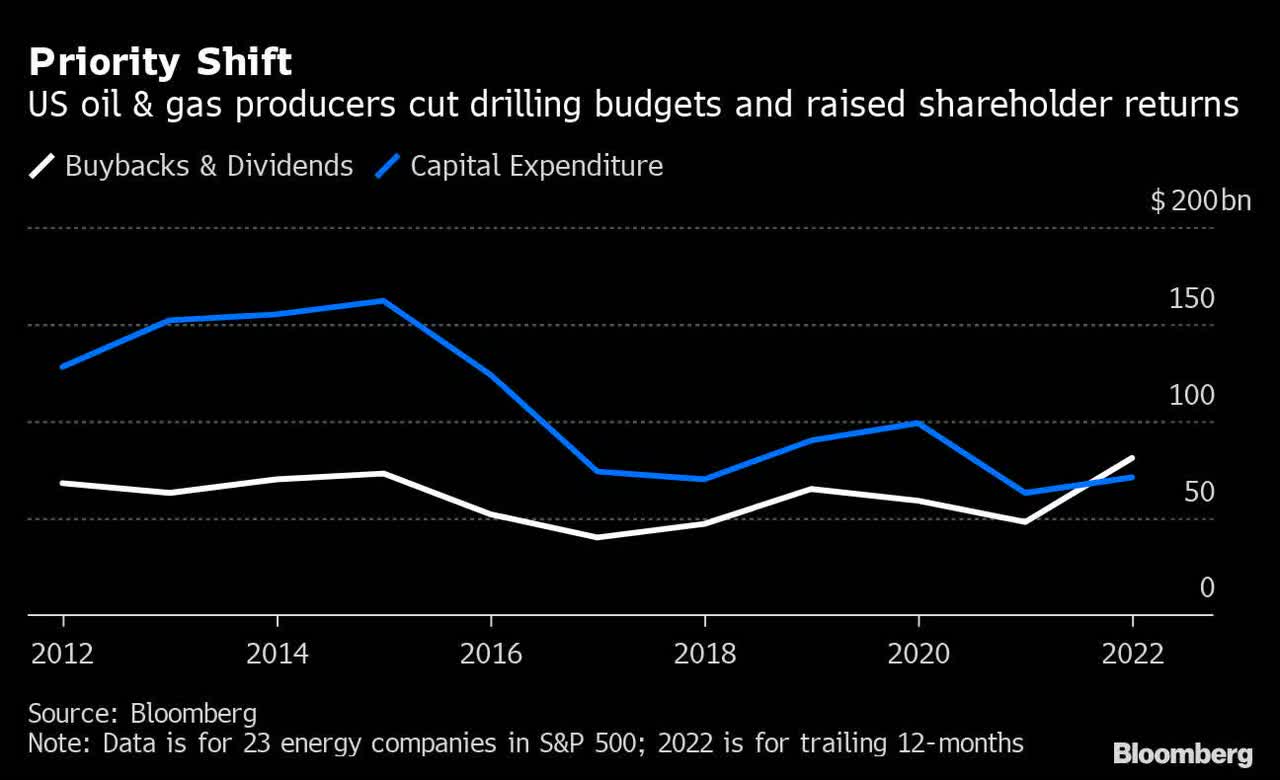

By declaring that oil and gas companies are the enemies of a “renewable” world, these companies are unlikely to boost production as they rather benefit from low capital expenditures, which paves the way for high free cash flow. High FCF can be used to improve balance sheet health and shareholder distributions. After all, nobody guarantees that oil companies will get support when oil prices implode in the future. After all, they are not wanted.

As a result, oil companies are now prioritizing shareholder distributions over capital expenditures. The chart below shows that going into this year, buybacks and dividends exceeded CapEx. Moreover, we see that CapEx is roughly $100 billion below its peak. That’s a huge number as it shows that drilling CapEx is down at a time when demand is back.

Bloomberg

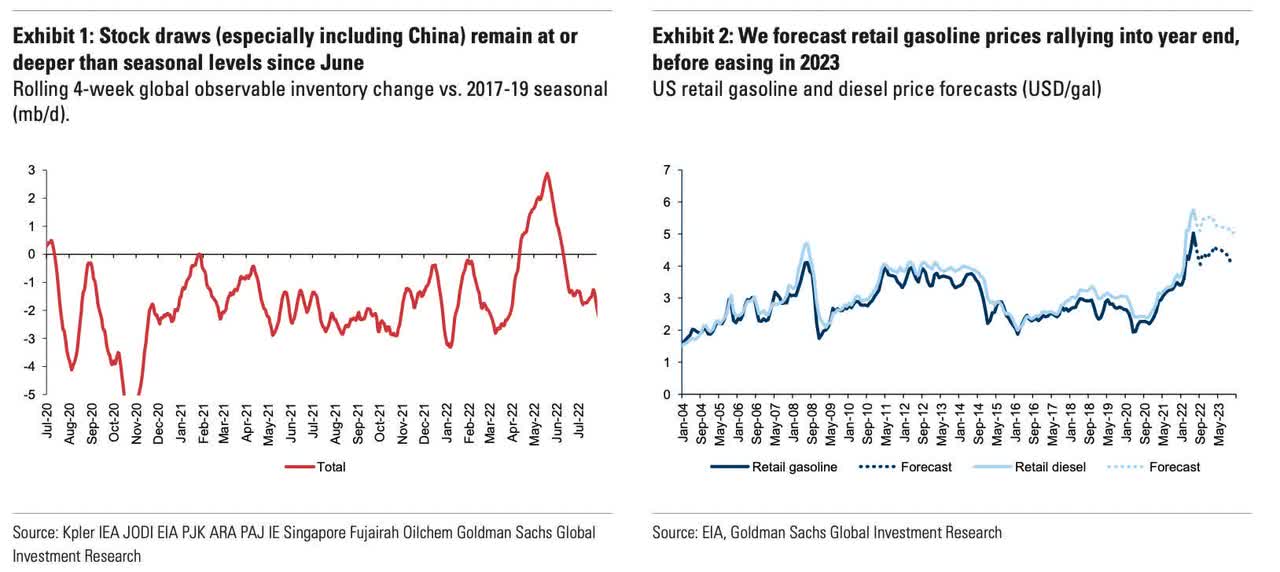

On top of that, oil inventories remain low. Especially in industrial nations like China that have kept a lid on demand with a strict zero-COVID policy and (related) economic struggles in construction. If demand comes back in these nations, supply and demand will be even further apart.

Hence, Goldman Sachs believes that oil could make its way to $130 by the end of this year.

Goldman Sachs

The charts below show global oil inventories and the bank’s forecast that gasoline prices will remain elevated in the United States.

Goldman Sachs

Problem 2: The transition cannot be accelerated (related to problem 1)

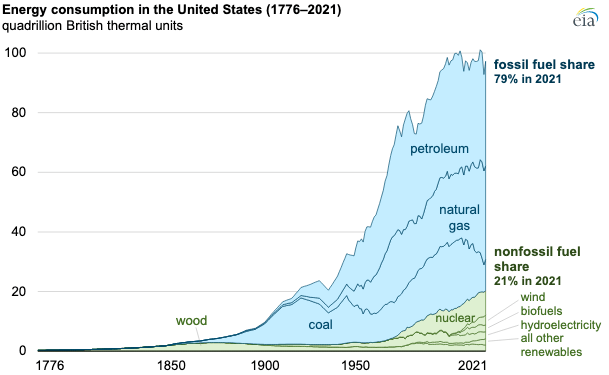

I’ve used the chart below in a number of articles because I believe it’s so important. At the end of 2021, 79% of the energy supply in the United States came from fossil fuels. Almost all of it consisted of petroleum and natural gas products with coal coming in third.

EIA

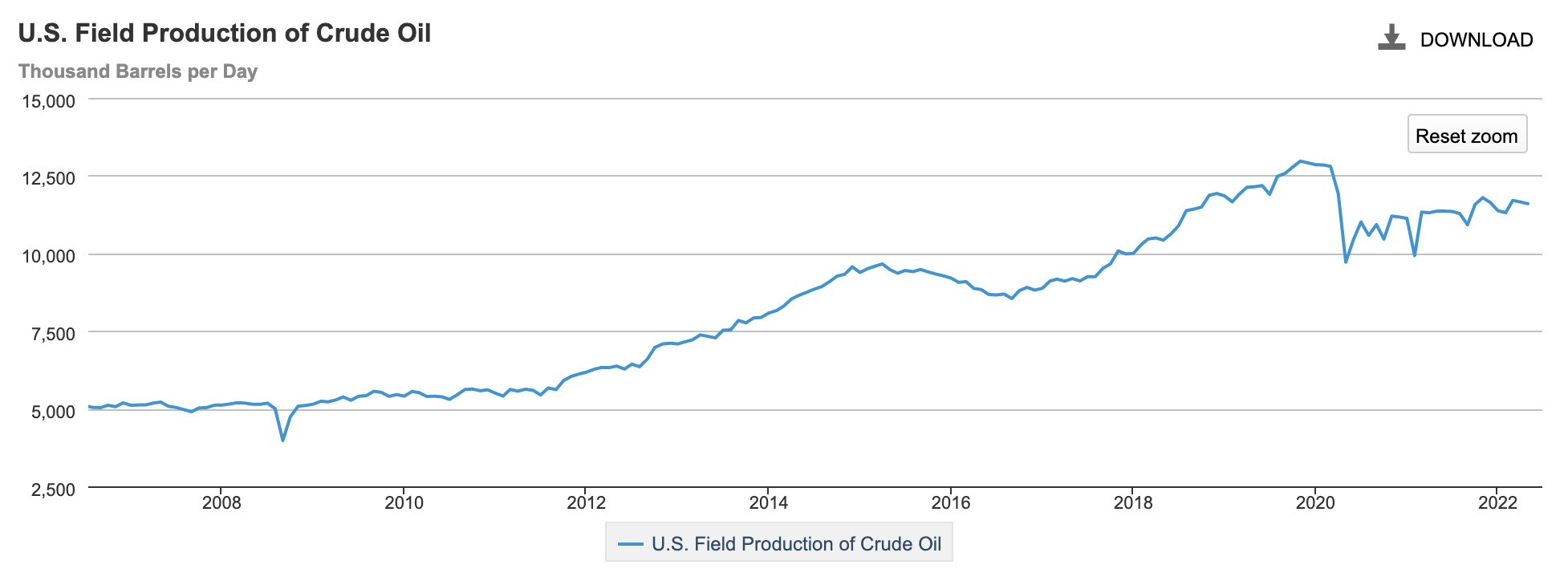

Not only is fossil fuel production being discouraged, but we’re also witnessing supply problems. First of all, US field production of crude oil is going sideways at roughly 11.6 million barrels per day. This is the first time since the oil boom that a recession is not followed by higher production.

EIA

Given high inflation and related problems like labor shortages, energy companies are forced to boost their CapEx just to sustain current production levels.

The extra spending won’t boost oil and gas production. Instead, the increase is necessary to meet their production targets for the year, most of the companies said. The production of shale wells declines rapidly, forcing companies to drill new wells to sustain output. Rising costs to drill are making it harder to stave off the declines.

Moreover:

“Tightness in the oil patch is leading to higher inflation [and] is making it harder to put production online in a timely manner,” said Kevin MacCurdy, a managing director at Pickering Energy Partners.

Some producers, including ConocoPhillips, Pioneer and Diamondback, allowed their oil production in the continental U.S. to drop between about 1% and 2% from the prior quarter. Pioneer cited a divestiture as a reason for the decrease.

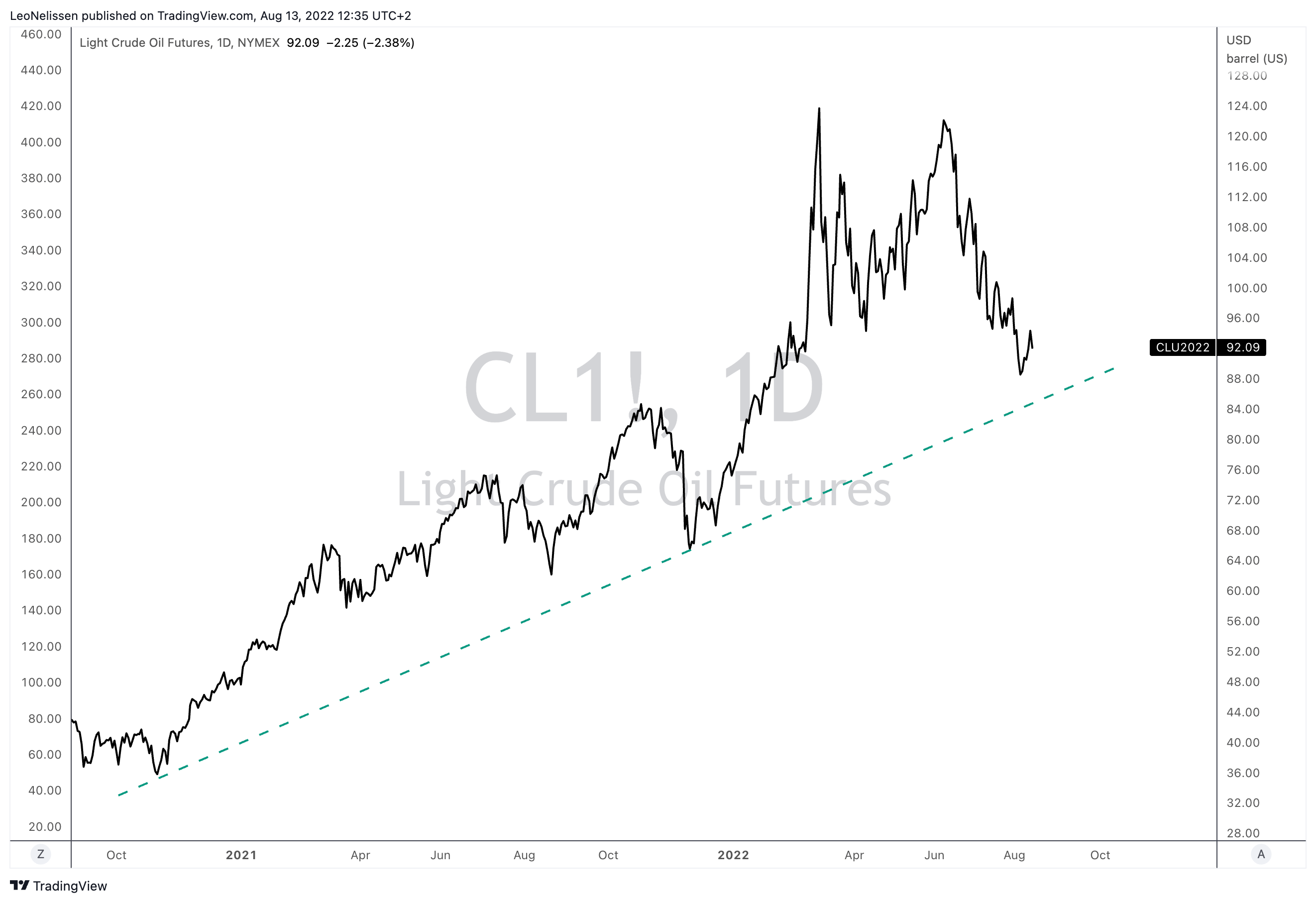

Combining everything so far, I believe we’re looking at a significant risk of a super cycle in oil. As my former colleague and oil expert Tracy Shuchart explained in a recent video, we’re looking at significant risks of a super cycle in commodities (not just oil). As oil supply is constrained, higher demand will cause long-term upwards pressure, which works its way to other commodities as well. Especially metals and agriculture are highly dependent on energy prices.

Tracy mentioned multiple cycles starting in 1967-1969 with new supply shocks in 1973/74 (oil embargo), which triggered central banks to hike into economic weakness.

I agree with that and I have thought about it a lot. I believe that economic weakness can temporarily pressure oil prices. However, let’s say we enter a huge recession and demand implodes. What follows will be even more pressure on supply as economic growth improves. This is indeed a viable multi-wave inflation scenario.

TradingView (WTI Crude Oil)

We can only escape from this situation if climate targets are adjusted to incorporate a much slower transition and/or if oil companies start a massive spending spree. I don’t think any of this is likely.

So, I’m preparing for long-term elevated oil prices, which is why more than 20% of my entire net worth is invested in oil companies. They are all long-term investments and one of them is Marathon Oil.

Marathon Oil Remains Too Cheap

With a market cap of $16.3 billion, Marathon Oil is one of America’s largest onshore drilling companies.

The company has operations in Eagle Ford, Oklahoma, Permian, and Bakken Basins as well as Equatorial Guinea.

Marathon Oil

In 2Q22, the company produced 167 thousand barrels of oil per day. That’s roughly in line with 1Q22 levels. Including natural gas, production was 343 thousand barrels of oil equivalent per day. 83% of these volumes were produced in the United States.

In 3Q22, the company expects to produce 172,000 barrels of oil with total equivalent production remaining equal.

What helps is that Marathon produces in very efficient basins allowing the company to achieve a free cash flow breakeven price of $35 per barrel. This means that an oil price of $35 also covers CapEx, meaning that every dollar above $35 can (partially) flow towards shareholders.

Hence, the company, which is not expected to boost CapEx this year (beyond prior plans), is in a great position to boost shareholder returns. This year, the company expects $4.5 billion in free cash flow based on $100 WTI and $6 Henry Hub natural gas.

$4.5 billion in FCF is roughly 28% of the company’s market cap, which is a sky-high yield. Moreover, every $1 increase in WTI increases operating cash flow by $60 million.

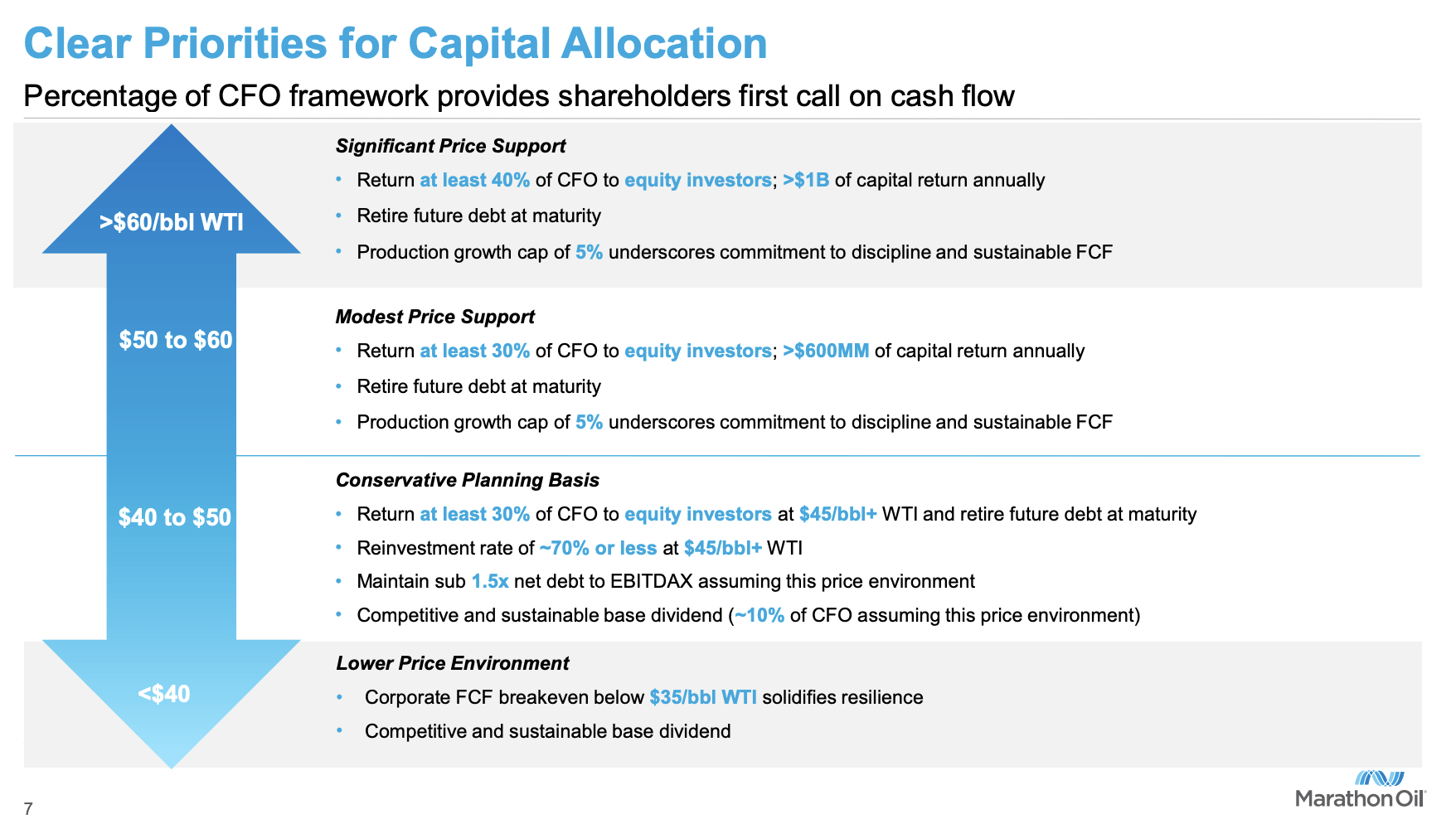

With prices above $60, the company is looking to return at least 40% of operating cash flow to investors – at least $1 billion of capital returns per year. The goal is also to maintain 5% production growth, which is an increasingly expensive commitment, but an important step for MRO to do its part to ease supply issues.

Marathon Oil

Since achieving its leverage target in October of 2021, the company has returned $2.5 billion to shareholders. Over the past three quarters, MRO has returned 55% of operating cash flow, which is roughly 75% of free cash flow. That’s $2.3 billion worth of share repurchases, reducing the number of shares outstanding by 15% in just 10 months.

If oil were to rally to $120 with $8.00 Henry Hub, the company would have an implied FCF yield of 35%.

Marathon Oil

Moreover, with regard to the leverage comments, the company ended 2021 with just $3.4 billion in net debt. That was less than 1x EBITDA. This year, the company is set to lower net debt to $1.9 billion, or a mere 0.3x EBITDA.

What this means is that if we’re indeed in a long-term oil bull market, the company can accelerate the MRO uptrend by aggressively buying back shares.

If oil remains at $100, the company is in a good spot to boost total shareholder returns by at least 10%-15% per year. That’s the base case. Now, if we assume a commodity super-cycle, MRO is truly one of the best places to be.

This is important to keep in mind, MRO emphasizes buybacks. Other companies decide to go with dividends.

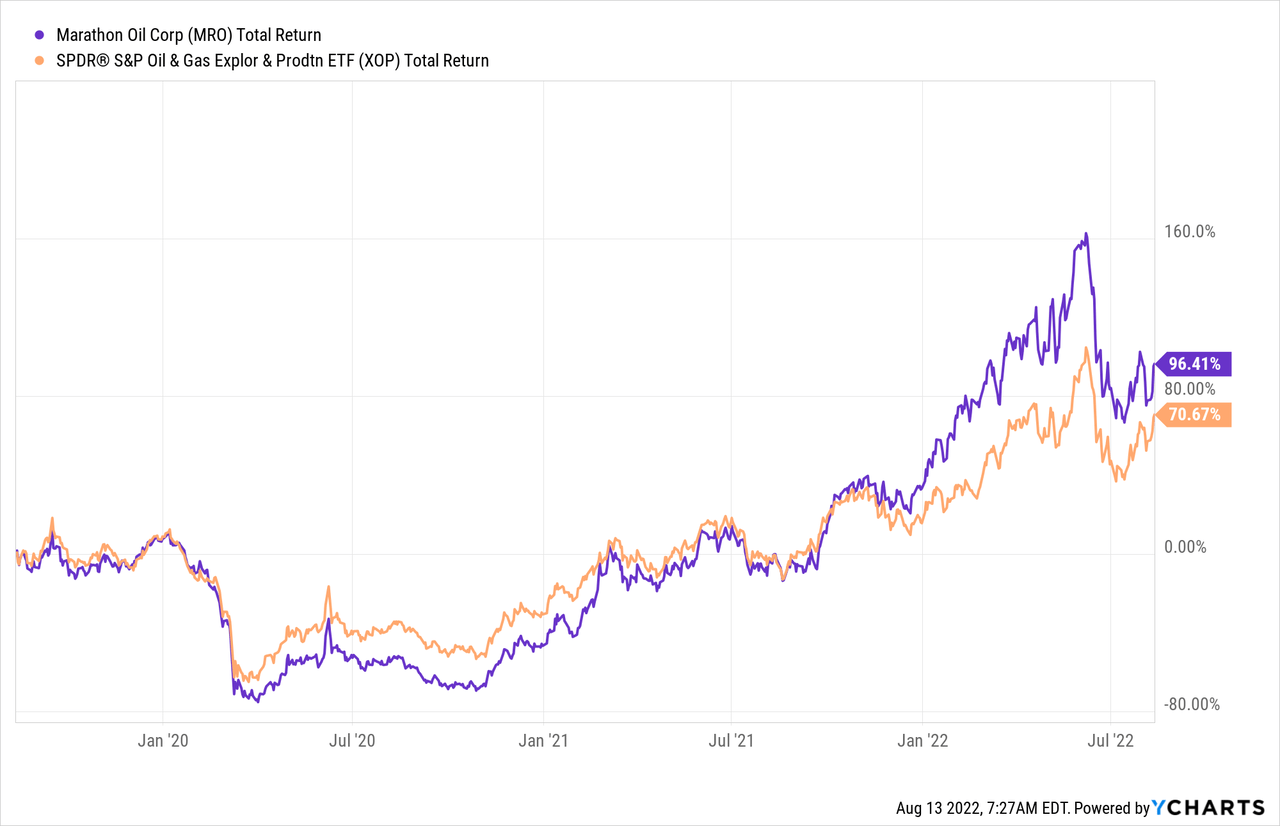

The chart below shows the impact of buybacks quite nicely. MRO shares have traded almost in lockstep with the SPDR S&P Oil & Gas Exploration & Production ETF (XOP). That changed when the company reached its leverage target and started to boost buybacks (at the end of 2021).

MRO Total Return Level data by YCharts

I expect MRO to continue long-term outperformance for all the reasons mentioned in this article.

Valuation

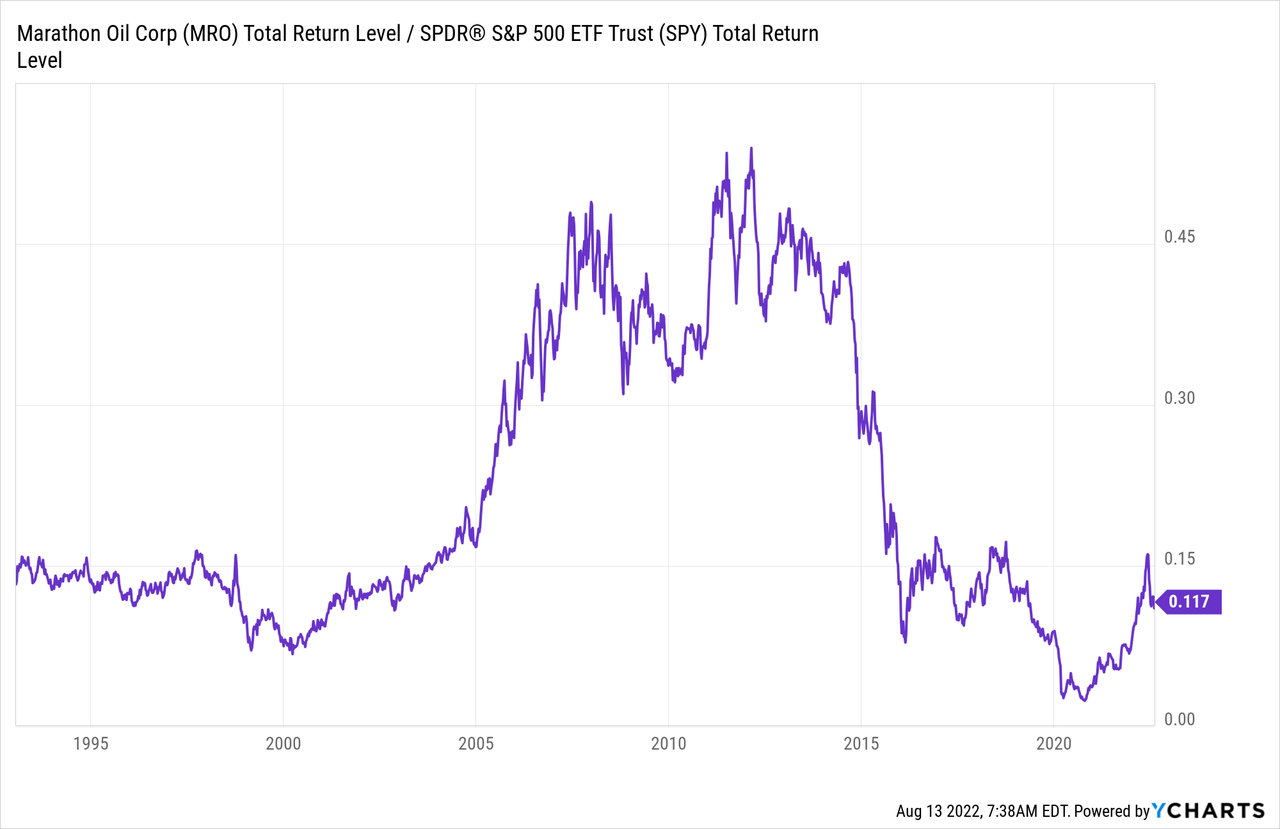

Marathon Oil has outperformed the S&P 500 since early 2020. Yet, the relative performance is below anything investors have seen between the start of the commodity super-cycle in 2000 and the energy peak of 2014. I expect MRO outperformance to continue on a long-term basis as the market will steadily figure out how much money these energy companies can generate.

Fundamental Chart data by YCharts

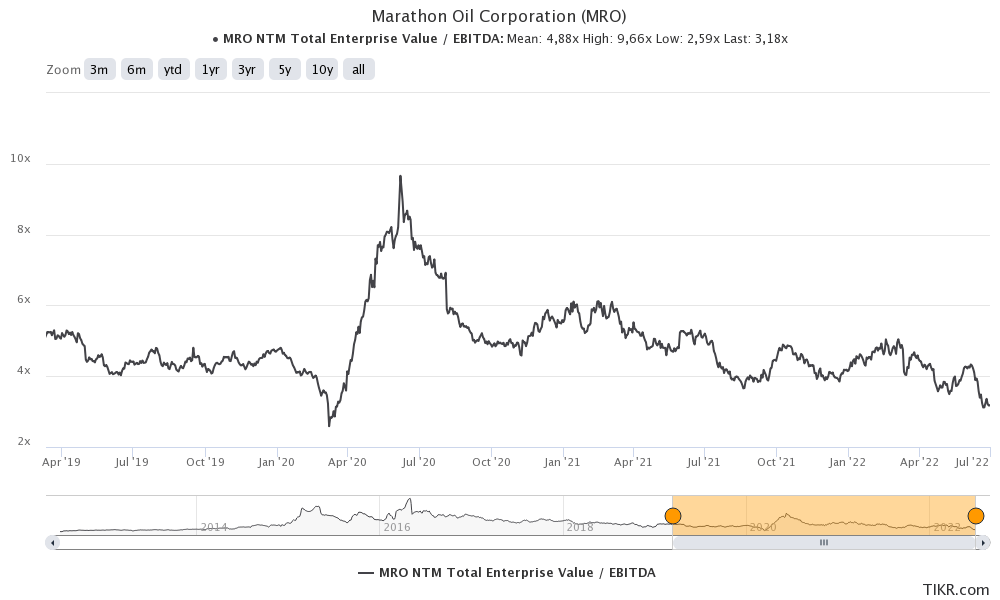

When it comes to the valuation, MRO is still too cheap. The company has an implied enterprise value of $18.3 billion consisting of its $16.3 billion market cap, $1.9 billion in expected 2023 net debt, and $120 million in pension-related liabilities. Using $5.2 billion in expected 2023 EBITDA, the company is trading at a 3.5x multiple.

Using the company’s EV/EBITDA history (next twelve months EBITDA) and the oil industry in general, I would make the case that anything below 4.0x is “really cheap”.

TIKR.com

In other words and conservatively speaking, I think that MRO has at least 25% upside on a 1-6 months basis.

Beyond that, and on a long-term basis, I’m close to saying “the sky is the limit”.

Takeaway

I remain very bullish on oil companies for a wide range of reasons. The core problem is that supply is constrained and I don’t see significant improvements anytime soon. The global push for renewables is accelerating to combat high energy prices. I believe that’s the wrong way to deal with issues as it only takes away incentives for drillers to increase production. Moreover, by cutting back on dominating energy sources, we’re triggering inflation, which is working its way through all industries, especially the ones that are energy intensive like agriculture and metals.

I expect oil companies to prioritize free cash flow and shareholder distributions over CapEx. Especially Marathon Oil benefits from that as it has a very low breakeven price, strong, an implied double-digit free cash flow yield, a healthy balance sheet, and the determination to spend most of it on shareholders.

While this will mainly be done through buybacks, it paves the way for long-term outperformance in an industry that I believe is undervalued in general.

So, long story short, I have little doubt that MRO will remain a terrific source of long-term total returns.

The only thing I need to mention is that regardless of how good the bull case sounds, please be aware that energy stocks are volatile. Do not go overweight and be aware of these volatility-related and cyclical risks. I believe the long-term trend is up, but it will come with downturns every now and then.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment