Vertigo3d

Manole Capital Management

4th Quarter Newsletter

December 2022

Manole Capital’s 4th Quarter Newsletter:

We’re using our 4th quarter newsletter as a way of summing up a challenging 2022 and (more importantly) looking forward to 2023. We will provide some tidbits on the macro environment (i.e., interest rates, inflation, Fed commentary, etc.), and we’ll attempt to weave in some insights into our unique investment process and philosophy.

Introduction:

As we always say, if you’re looking for political thoughts, you are absolutely in the wrong place. We never comment on politics and leave that to others. Our comments are entirely focused on the markets, especially our version of FINTECH. We define FINTECH rather uniquely, as “anything utilizing technology to improve an established process.” If you have any free time or if you’re having a hard time sleeping, you can better understand our version of FINTECH by reading our proprietary research. Just search on Seeking Alpha for our prior newsletters, stock specific pitches, thematic notes, or Gen-Z surveys.

We know that volatility is the short-term price that equity investors must pay for long-term attractive returns. All investors eventually feel the anxiety and pain of a volatile market. However, we choose to plan for and model in this type of volatility, so we aren’t surprised when it eventually arrives. We have stayed true to our bottoms up, research-intensive process and continue to spend all of our time doing FINTECH and company-specific analysis.

2022:

This year and last year seem like polar opposites. In 2021, the S&P 500 rose +29% and everybody was having success picking stocks. This year, the S&P 500 is down roughly (20%) and finding winners is much more challenging.

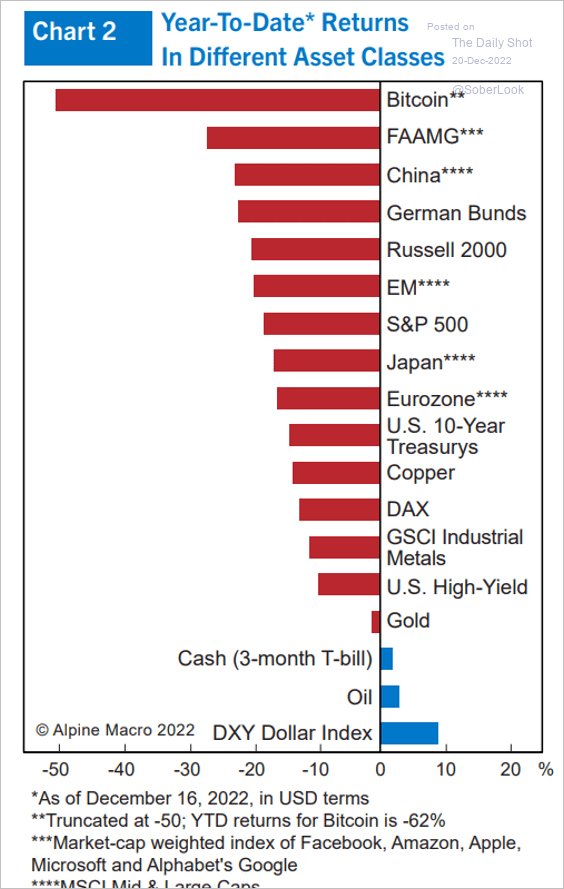

In a year like 2022, when everything from crypto to equities to fixed income is down, it was hard to find a “place to hide.” As you can see on this chart, other than good ol’ cash and energy, pretty much every asset class and geography went down this year.

The Daily Shot (The Daily Shot)

Warren Buffett once said “Rule #1 is never lose money. Rule #2 is never forget rule #1.” While we strive to always make money, the unfortunate truth is we sometimes get a stock wrong – shocker! We might share a first name with Mr. Buffett, but we absolutely aren’t perfect. For us, we define success as “generating excellent long-term returns and limiting a material loss of capital.”

In the 1960’s, growth stocks had a massive rally, with the Top 50 companies becoming the “Nifty 50”. Those “sure things” led investors to pay unheard of valuations (50x forward earnings). By the end of that decade, Mr. Buffett had become so frustrated at the exuberance of the market that he dissolved his investing fund and simply moved to the sidelines. We weren’t that frustrated with equity markets last year, but we appreciate his principle.

By 1973, with an oil embargo and runaway inflation, Mr. Buffet re-emerged and began to put his cash to work. He was quoted in Forbes saying he felt “like an oversexed guy in a harem.” While we aren’t about to say the 2023 is that enticing, we continue to selectively put additional capital to work.

Santa Claus Rally:

Since 1950, the 4th quarter has generated the best average quarterly returns for the S&P 500 of +4.1%. In a normal year, stocks normally head higher in mid-to-late December, in what is commonly referred to as a Santa Claus Rally. Over the last 70 plus years, from December 23rd through the last five trading days of the year, the S&P 500 averages gain of +1.4%. Not this year!

After some initial excitement over the smaller interest rate pace (just 50 basis points, instead of 75 basis points), it didn’t take very long for the markets to realize that the Fed expects to continue to hike and go longer than most expect. As Chairman Powell stated, “While smaller rate hikes are a promising development and a welcome sign that tightening policies are helping, it does not mean that we have restored price stability or that inflation has been tamed. He then emphasized that “It will take substantially more evidence to give comfort that inflation is actually declining” and “by any standard, inflation remains much too high.” Then, the Fed downwardly revised its GDP growth estimate for next year to only 0.5% (from +1.2%) and upped its estimate for unemployment to 4.6% next year (currently at 3.7%).

Fed policymakers now have a median federal funds target projection 5.1% next year, a level not seen since 2007. To hit that target next year, the Fed will likely raise rates by 25 basis points in February, March, and May. That’s what the CME FedTool is currently indicating. With public comments like these, one might think Chairman Powell is trying to be the Grinch that stole Santa’s rally.

Our 2022 Performance:

We aren’t able to construct a disaster proof portfolio, but we can manage our net exposure and lean into positions that present the best upside. I guess you can say we are patiently waiting for our opportunities to appear. As Bruce Lee once said, “Patience is not passive, on the contrary, it is concentrated strength.”

We try to segment our performance into 3 various camps. The first is our long-only portfolios (publicly-traded FINTECH securities), the second is our long and short portfolios (also publicly traded FINTECH companies) and the last is our hedge fund – the Manole Fintech Fund (i.e., The Fund). The Fund is the only vehicle that can own both publicly traded, as well as privately held FINTECH companies.

In our long-only portfolios, which can be viewed here, we continue to own a concentrated mix of FINTECH securities. When the market declines and financial risk is heightened, we cannot hedge this portfolio with our short book. We choose to increase our cash, as a form of downside protection. In an inflationary environment, this can be an expensive proposition, but it is not our long-term intention to run the portfolio with cash levels this elevated. It is simply a temporary solution to a challenging environment. After 13 consecutive years of positive performance, the Nasdaq 100 just had its worse year since 2014. With so many technology names in our concentrated portfolio, we were not immune.

Our“Low Net” long / short FINTECH portfolio attempts to keep our net exposure low (in the + or – 500 basis point level). When the market is steadily moving higher (like 2021), the long names perform, but the shorts detract from overall performance. When the market stumbles (like 2022), we like to see our long names “hold their own”, while the shorts materially add to performance. This is exactly what happened this year and the portfolio should end the year up in the +7% range.

Since its inception, The Fund has generated solid performance from its private investments, but that changed in 2022. In the summer, Klarna raised money and it equated to a down round of over (85%). We are far from perfect, and this is just one example of the dangers of investing in private companies (less transparency and limited liquidity). In The Fund, we anticipate 2022 performance being slightly positive. This year, the short book materially assisted overall performance, which essentially is the opposite story from 2021. While this is the worst absolute annual result in its 4 years of existence, one could argue it is the best relative return too (compared to a market down roughly 20%).

Sexy and innovative stocks were in vogue in 2021, as the market climbed higher and higher. Some of our “boring” and free cash flow companies were better performers this year. As we look to 2023, we are excited that most of our secularly growing FINTECH companies will generated meaningful annual EPS growth. The overall market EPS outlook will be lucky to be flat next year, but our free cash flowing FINTECH companies should be able to produce high-single-digits earnings growth.

2023:

Last year, the S&P 500 topped out at a forward P/E of over 21x. Today, looking at 2023 (which is still too high) earnings, the market’s P/E is roughly 17x to 18x. If we go back to the late 1970’s, the P/E was in the single-digit range. We aren’t saying valuations are “dirt cheap”, but we are finding interesting “bargains” in some of our favorite names.

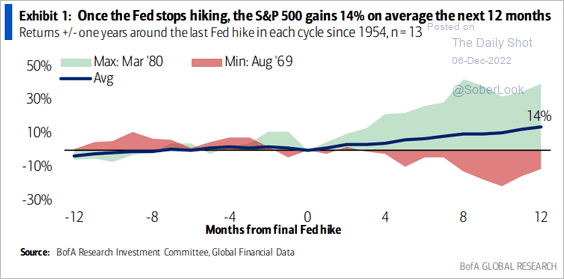

If we were to summarize the consensus outlook for 2023, we would say that most market pundits are predicting 6 months of continued tough conditions, followed by 6 months of a positive rebound in sentiment. This forecast corresponds with continued interest rate increases at the next 3 Fed meetings, followed by a pivot and loosening of conditions. We understand why the market is hoping for this pivot, as the S&P 500 typically performs nicely once the Fed stops raising rates. As this Bank of America Research chart shows, the S&P 500 delivers an average of +14%, over the following 12-months once the Fed is done tightening.

Bank of America Research (Bank of America Research)

While the speed at which the Fed has raised rates is significant, we are more interested in how long the Fed decides to hold rates at these levels. The slower the Fed acts, the chances that it overdoes this tightening and causes a major slowdown theoretically gets lowered. Maybe it comes down to how a pivot is perceived. In our opinion, a reduction in the pace of rate hikes is not a pivot. We continue to think that the Fed’s quantitative tightening program will continue, especially since little has been accomplished with its enormous $8.6 trillion balance sheet. As the Fed continues to tighten (into a deeply inverted treasury yield curve), we believe it is best to remain conservative and expect elevated volatility.

Today’s market seems entirely focused on macro commentary emanating from the Fed. We understand this but aren’t going to change our process because the market is fixated on Chairman Powell’s comments. Quite simply, we don’t believe that things will miraculously get better once the Fed stops raising interest rates and pauses. We are modeling in a continued sluggish environment, where companies with cash flow and dominant franchises will perform, while less capitalized (i.e., weaker) competitors fail. If the Fed were to reverse course and suddenly get accommodative, it would likely mean the economy has performed remarkably well. If that’s the case, our market leading companies should post excellent returns and results.

Inflation, Interest Rates, and the Fed:

The Fed continues to target 2% inflation, which it struggled to achieve for a couple of decades. Finally, inflation rises to 7% to 8% and the global economy goes haywire. Why should we expect that the Fed will quickly reverse course and cut interest rates? As Chairman Powell stated, “it is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy.”

We are pleased that inflation has fallen from +8.6% in September down to +7.1% in November, but we remain very far from that Fed 2% target. We wouldn’t call 10 to 20 bps of a decline (versus Street expectations) equal to a deflationary environment. In our opinion, inflation running in the high-single-digits isn’t worthy of a celebration.

Don’t get us wrong. Lower inflation readings are a net positive, but the absolute level is unfortunately still troublesome. We hate to make a complicated subject so simple, but inflation running over 7% is still a Fed problem.

Fed Governor Christopher Waller recent comments resonated with us, when he said “we’re not softening…quit paying attention to the pace and start paying attention to where the endpoint is going to be. Until we get inflation down, that endpoint is still a ways out there.” Governor Waller believes the Fed is “on the right path” because all of the rate increases this year have done little to break inflation. He said, “For all the talk of crashing the economy and breaking the financial markets…it hasn’t done that.”

Does this sound like somebody that will quickly pivot and change course in 2023 (and cut rates)? Lower interest rates would clearly help hyper growth companies that aren’t terribly sustainable in this higher rate environment, but we just don’t believe that forecast is probable. We will continue to assume inflationary pressures in our proprietary models, and if that ultimately disappears, we’ll be pleasantly surprised to the upside.

Investing Styles:

Understanding a manager’s process, strategy and philosophy can often be a challenge for investors to comprehend. Our investing style was developed under the umbrella of Herb Ehlers and Goldman Sachs Asset Management’s Growth Equity team. Many of the critical investing themes we discuss, were learned from years of experience on that successful team.

There are macro or top-down managers, that make decisions based on economic fundamentals. There are quantitative managers, using algorithms, machine learning and sometimes artificial intelligence to make trading decisions. There are arbitrage shops that look for opportunities with M&A disparities and technical managers making intra-day trading calls. Frankly, there are dozens and dozens of different types of asset managers.

As our loyal readers know, we don’t make grand proclamations or forecasts on macro topics, as that isn’t our area of expertise. We are not going to guess the how many basis points the Fed will increase at their next meeting in February. We aren’t going to provide an inflation target, a market guestimate for foreign currencies or make any bold commodity predictions. Instead of guessing where prices will go, we prefer to own the exchanges where all of these products trade. We would rather own a transaction processor benefitting from higher volatility, as opposed to speculating on the next leg up or leg down in various commodities.

Instead of macro forecasting, we will continue to focus entirely on doing bottoms up, fundamental research. We love to do scenario analysis to understand how our companies will perform in various environments and economic conditions. Maybe we need a hobby?

Different Strokes for Different Folks:

Let’s start our discussion on investment styles with a Hotel.com’s Captain Obvious type of statement. While Tampa has done a fantastic job building up its downtown, it isn’t mid-town Manhattan. In New York City, one might see a dozen hedge funds all located in one office building. That isn’t Tampa, as our city is much more of a doctor / lawyer type of town.

Over a year ago, Cathie Wood relocated her Ark Investment Management firm from New York City to St. Petersburg, FL. We were thrilled to have more financial professionals and money managers in our “neck of the woods”. With over $14 billion in assets under management, Ark’s ETFs remain quite popular.

Ms. Wood has become something of an “investment rock star” with her ability to articulate and explain financial concepts to retail investors. Ms. Wood is a tremendous speaker and eloquently goes from macro commentary to deeper, stock specific issues. Back in August 2021, the New York Times profiled Ms. Wood and her “unusual approach to investing.” We have seen her on CNBC and Bloomberg TV, and she always seems to wonderfully discuss the markets and Ark’s investment style.

A month ago, we went to one of Ms. Wood’s discussions, to hear how she invests. We weren’t trying to get any new stock specific ideas, but we wanted to understand her process and investing philosophy. There was standing room only in Ms. Wood’s presentation and the attendees were gripped to her comments. We looked at the audience and wondered…if we were to give a market update to prospective clients, we’d be lucky to get our parents to show up (and probably only if there were passed appetizers and an open bar).

Getting back to Ms. Wood and the presentation we heard a month ago. Once again, we are a fan of hers and are impressed with her ability to articulate her investment philosophy and style. Where we differ is on Ark’s strategy of deploying capital and maybe on portfolio construction too. Also, we tend to disagree with some of her recent market comments; here are a few of the quotes we jotted down that made us “scratch our head.”

“Disruptive Innovation”:

Ms. Wood often mentions “disruptive innovation” when she discusses her portfolios. She defines it as ” the introduction of a technologically enabled new product or service that potentially changes the way the world works.”

Ms. Wood invests with a mindset that“sacrifices short-term profits to capitalize on the exponential growth and highly profitable opportunities that a number of innovation platforms are creating.” On this, we absolutely agree and we also look for companies with open-ended and attractive secular growth opportunities.

We can appreciate this longer-term perspective, but not all market conditions allow a manager the latitude to sacrifice today’s pain for tomorrow’s gains. We aren’t looking for our companies to alter their capital allocation plans for the near-term, but we think excellent management teams can use free cash flow for re-investing back in their business, plus provide steady dividends and possibly even stock buybacks. Just because a company generates more cash flow that it needs to grow does not mean it isn’t innovative.

At her Ark presentation, Ms. Wood spent a bit of time discussing how she viewed the future, specifically discussing air and robo-taxis. She claims that this industry has a forward addressable market opportunity of $10 trillion. While that might actually happen, we tend to be much more grounded in today and tomorrow type of issues. We aren’t short-term focused, but we tend to prefer to model how our businesses will do in 2023 and 2024, rather than 2035.

One of our favorite cartoon shows (growing up) was The Jetson’s and we loved how forward-thinking it seemed. The show came out in 1962 and the futuristic family cartoon predicted what life would be like in 2062. The writers for The Jetsons were way ahead of their time, correctly predicting flat screen TV’s, smart watches, drones, video calls, digital newspapers, holograms, and even robotic vacuums.

While we model what happens to our payment companies as you use more cards (and less cash), Ms. Wood seems to model which companies will succeed with the advent of flying taxi’s. I guess we aren’t visionaries or maybe we aren’t that good at making long, long, long-term forecasts.

Deflation or Inflation:

Ms. Wood expressed a “greater risk of deflation, than inflation” and then explained how former Treasury Secretary Larry Summers is “very wrong” with his inflationary worries. Ms. Wood believes that inflation is temporary and that “it is a 15-month problem, not a 15-year problem”, while Summers argues that the Fed will continue to raise interest rates (possibly to 5.5% to 6.0%), as long as inflation is running at a near 40-year high. Instead of discussing this deflationary threat in detail, we have attached Ms. Wood’s open letter to the Fed here. If we were to pick sides in this inflationary debate, we’d probably lean towards Mr. Summers, rather than deflation becoming a problem next year.

What did the independent Fed have to say about this exact topic? Well, Chairman Powell said, “We need to be honest with ourselves that there’s inflation. 12-month core inflation is 6% CPI. That’s three times our 2% target. Now it’s good to see progress, but let’s just understand we have a long ways to go to get back to price stability.” Instead of hoping the Fed pivots and begins to cut interest rates, which many are expecting in mid-2023, we envision inflation remaining stubbornly high. How long? We don’t know, but we aren’t in the camp that the Fed will begin to lower interest rates in the middle of next year.

Diving deeper into this topic, we can appreciate why Ms. Wood wants a lower interest rate environment. If your portfolio is filled with hyper growth companies, with negative operating leverage and cash flow problems, you need the Fed to stop raising interest rates. You hope and pray for another bull market and an environment that rewards innovation and growth, at the expense of profits.

Ms. Wood said she is investing like we are “going to see an environment like the ‘Roaring 20’s’.” Those type of conditions are possible, but it isn’t what we are anticipating. Another difference in our money management style comes down to what happens to a company’s fundamentals – if the “weather gets rough” and economic conditions worsen (like 2022). All of our companies generate free cash flow and can “weather the storm”, while certain Ark Investment positions appear to be built for “calmer seas.”

Portfolio Construction:

Ms. Wood closed her presentation with her thoughts about the upside of her portfolio. She said, “our companies are going to go up 100x, and Microsoft won’t”. We agree that Microsoft, with its $1.8 trillion market capitalization, has absolutely no chance to go up 10x, let alone 100x. We don’t own Microsoft, so we aren’t taking offense to that comment. For us, it led to a question about portfolio construction.

Our investment process strives to balance risk and reward. We are happy with some of our positions generating 10% to 20% gains. Using a baseball analogy: Not every name needs to be a “home run”. We are pleased with some of our companies delivering “singles or doubles” or simply “bunting to reach 1st base.” Our portfolios attempt to marry some names that have higher risk / higher reward, with those that are steadier and have more predictable returns. We don’t have a ton of holdings that are going to end up being worth 100x their current valuation, but we also don’t have positions that might end up worthless (knock on wood).

None of the prior few pages are intended to be disparaging towards Ms. Wood or Ark’s investment philosophy. She should be applauded for building Ark into a large, well-known, and profitable asset manager (significantly larger than Manole Capital). All we are trying to do is differentiate between investment styles, and to provide more insight into our unique strategy and philosophy.

We find it interesting that Ark’s FINTECH ETF owns 30 different companies and yet there are only 4 names that overlap with our flagship FINTECH portfolio. Clearly, we have a very different definition and version of FINTECH.

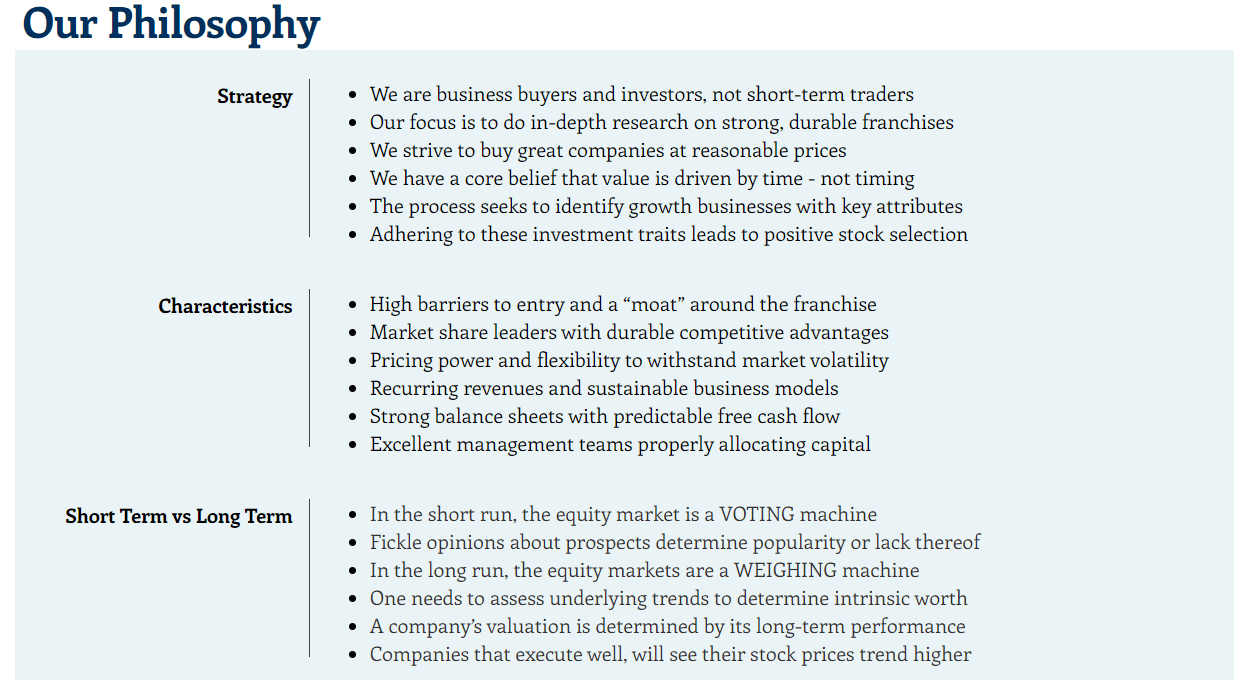

In our opinion, it comes back to our process, strategy, and investment philosophy, which can be summarized on this 1-page from our website. We are confident that the companies we own possess these important characteristics and follow our long-term investment strategy.

Manole Capital Philosophy (Manole website)

Conclusion:

The early days of a new bull market are extremely difficult to decipher and there will be plenty of pundits calling it a bear market rally. From 1942 to today, the average bear market lasted roughly 11.1 months with an average decline of (32%). Counter those bearish stats with that of the average bull market, which lasted for 4.4 years, produced an average return of +156%. When pessimists try to ruin your holidays, simply tell them that “bull markets are longer and stronger than bear markets.”

We are more focused on looking forward, than looking backwards. We strive to be anticipatory, not reactive. There were few investors that properly called the bottom in March of 2009 and even fewer that perfectly timed it in March of 2020. We are never going to be market timers, but we are going to follow our disciplined investment philosophy and be prepared for when a market rebound emerges.

Many have been warning of a coming US and global recession. On JP Morgan’s 3rd quarter conference call, CEO Jamie Dimon said storm clouds will arrive in the next 6 to 9 months and “very serious” headwinds were looming. The IMF just stated that “the worst is yet to come,” and the US economy will “stall” in 2023. Instead of grand proclamations, we prefer to understand how our companies will perform in different scenarios. Will they be able to pass along higher prices? Will they adjust their expense base for a new environment? Are management teams properly allocating capital?

Managing money is hard to do. Maybe it wasn’t too challenging in 2021, when everything seemed to simply head higher. 2022 has been our version of “normal”, where winners and losers are getting differentiated. This John F. Kennedy quote seems apropos for today’s market environment. He said that “The Chinese use two brush strokes to write the word ‘crisis.’ One brush stroke stands for danger: the other for opportunity. In a crisis, be aware of the danger – but recognize the opportunity.” We feel like today’s market conditions are ripe with juicy opportunities.

In conclusion, we understand that the short-term is impacted by negative sentiment and market timers. However, we will not stray from our disciplined investing philosophy and strategy. We remain true to our investing process and are taking advantage of this volatility and uncertainty. Manole Capital remains a long-term investor, in a short-term trading environment.

We look forward to speaking with you soon.

Warren Fisher, CFA

Founder and CEO

Manole Capital Management

|

DISCLAIMER: Firm: Manole Capital Management LLC is a registered investment adviser. The firm is defined to include all accounts managed by Manole Capital Management LLC. In general: This disclaimer applies to this document and the verbal or written comments of any person representing it. The information presented is available for client or potential client use only. This summary, which has been furnished on a confidential basis to the recipient, does not constitute an offer of any securities or investment advisory services, which may be made only by means of a private placement memorandum or similar materials which contain a description of material terms and risks. This summary is intended exclusively for the use of the person it has been delivered to by Warren Fisher and it is not to be reproduced or redistributed to any other person without the prior consent of Warren Fisher. Past Performance: Past performance generally is not, and should not be construed as, an indication of future results. The information provided should not be relied upon as the basis for making any investment decisions or for selecting The Firm. Past portfolio characteristics are not necessarily indicative of future portfolio characteristics and can be changed. Past strategy allocations are not necessarily indicative of future allocations. Strategy allocations are based on the capital used for the strategy mentioned. This document may contain forward-looking statements and projections that are based on current beliefs and assumptions and on information currently available. Risk of Loss: An investment involves a high degree of risk, including the possibility of a total loss thereof. Any investment or strategy managed by The Firm is speculative in nature and there can be no assurance that the investment objective(s) will be achieved. Investors must be prepared to bear the risk of a total loss of their investment. Distribution: Manole Capital expressly prohibits any reproduction, in hard copy, electronic or any other form, or any re-distribution of this presentation to any third party without the prior written consent of Manole. This presentation is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary to local law or regulation. Additional information: Prospective investors are urged to carefully read the applicable memorandums in its entirety. All information is believed to be reasonable, but involve risks, uncertainties and assumptions and prospective investors may not put undue reliance on any of these statements. Information provided herein is presented as of the date in the header (unless otherwise noted) and is derived from sources Warren Fisher considers reliable, but it cannot guarantee its complete accuracy. Any information may be changed or updated without notice to the recipient. Tax, legal or accounting advice: This presentation is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any statements of the US federal tax consequences contained in this presentation were not intended to be used and cannot be used to avoid penalties under the US Internal Revenue Code or to promote, market or recommend to another party any tax related matters addressed herein. |

Be the first to comment