fcafotodigital/E+ via Getty Images

MamaMancini’s Holdings, Inc. (NASDAQ:MMMB) is a food manufacturer and distributor focusing on fresh deli-prepared meal options with an Italian flavor. The items here include prepared pasta and fresh meat dishes typically found at to-go grocery store delis, along with an assortment of ready-to-eat retail packages.

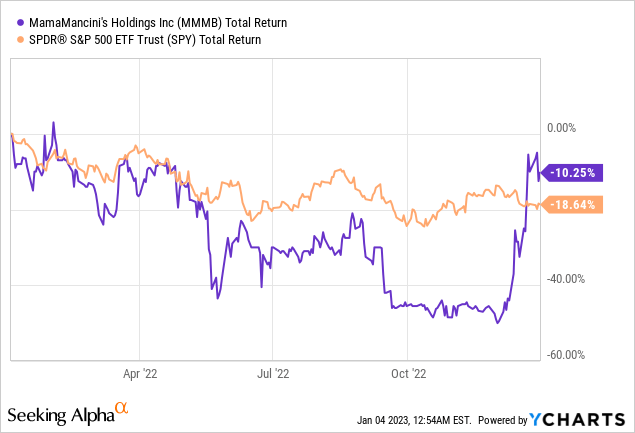

The stock crossed our radar by making a big move in recent weeks following the Q3 earnings report in December which we believe marked a turning point for the company. Indeed, shares have more than doubled since their December low with the latest operating trends and financial momentum signaling a runway for strong growth. We see the potential for more upside going forward.

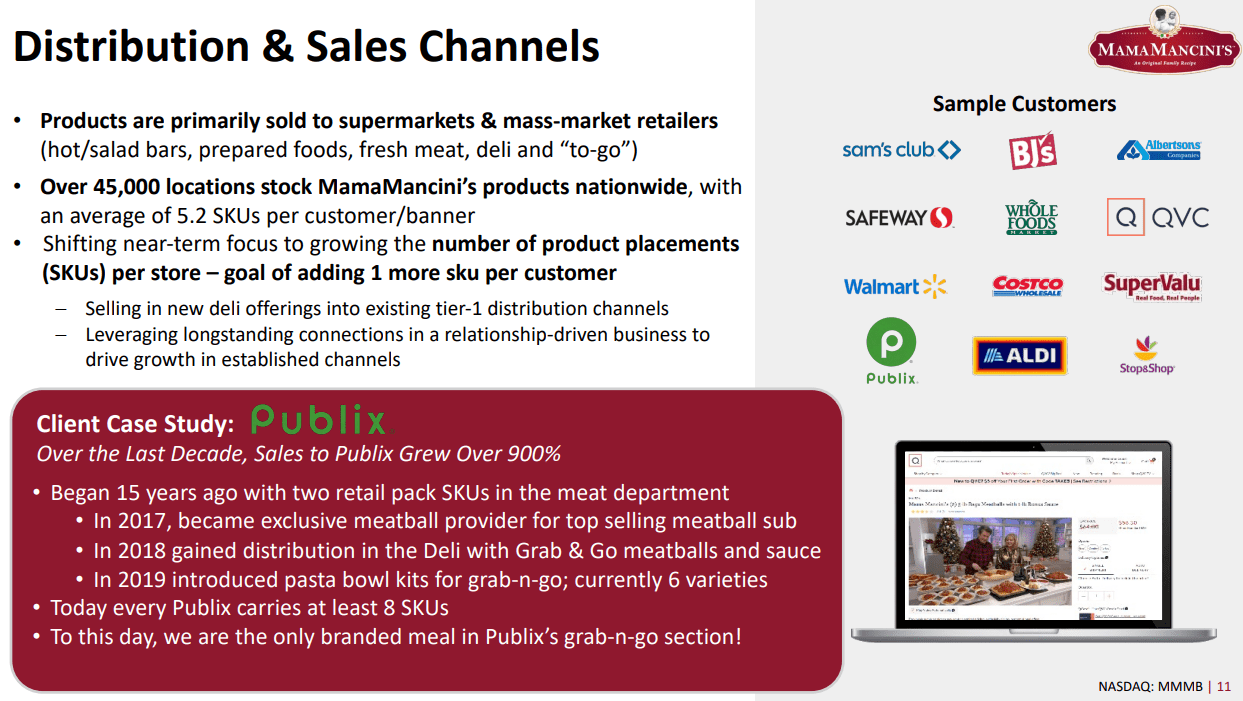

MamaMancini’s is still a micro-cap with a market value of just $65 million, but our message here is that this is more than just a “penny stock”. The attraction is an impressive distribution footprint with products found at more than 45,000 locations in the U.S. through supermarkets and major retailers. Strategy initiatives including expanding manufacturing capacity, while entering new categories highlight a positive long-term outlook.

MMMB Key Metrics

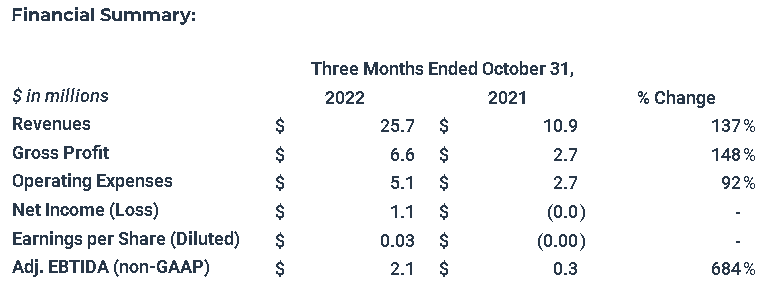

The company last reported its Q3 financial results on December 12th with EPS of $0.03, turning positive compared to a near breakeven EPS of -$0.00 in the period last year. Revenue of $25.7 million was up 137% year-over-year, exceeding management’s previous guidance of reaching an annualized sales rate of $100 million by year, a quarter early. Sales also climbed by 13% from Q2.

source: company IR

The context of the top-line strength considers not only launching with two new major customers but also increasing the number of items sold per store. The company has also been able to push pricing as a response to inflationary cost pressures.

The Q3 gross margin at 25.7% improved by 1,100 basis points from 14.7% in the first half of the year with efforts to improve efficiency across areas like procurement, manufacturing, and logistics management. Freight costs also declined connected with lower energy prices in the period. The success is evident at the adjusted EBITDA level which reached $2.1 million from just $0.3 million in the period last year.

source: company IR

Overall, the tone during the conference call projected optimism with an expectation for the trends to continue. The company ended the quarter with $3.5 million in cash against $14 million in total debt. Keep in mind that the annualized EBITDA rate now above $8 million suggests a net leverage rate under 2x which is stable in our opinion. A path for stronger earnings should further improve liquidity and ease any solvency concerns.

What’s Next for MMMB?

What we like about MamaMancini’s is the sense that its market positioning catering to grocery store deli and salad-bar operations with fresh pre-cooked meals at a national scale is relatively unique. This is in contrast to either small independent local shops or major industry players that specialize more in frozen foods.

Industry data suggests the deli department of grocery stores is seeing double-digit growth adding incentives for stores to invest in this category as a valuable service to customers. The idea is that shoppers are responding to these often healthier food options as an alternative to quick-service restaurants in what remains an underpenetrated opportunity. The company plan going forward is to introduce new categories like soups and pizza options that can add to growth.

source: company IR

As it relates to the stock, the bullish case is simply that MamaMancini’s can continue with more of what we saw for Q3. The annualized pace of earnings implies a year-ahead EPS of $0.12 which means MMMB is trading at approximately 15x as a forward P/E ratio. Annualizing the Q3 adjusted EBITDA to $8.4 million also arrives at a forward EV to EBITDA multiple of around 9x. These levels are compelling considering the latest operating performance and growth potential.

On the other side of the discussion, we can recap some of the risks going back to the company’s still micro-cap profile which keeps shares speculative. Everything looks good to go, but there are a lot of uncertainties related to the financials and earnings potential looking past the next several quarters.

One dynamic we’re considering is that if the company has already secured distribution with most major retailers, the next phase in growth to double sales from here will be more difficult if the “low-hanging fruit” has already been covered. Further efforts to expand manufacturing capacity or attempt new strategic acquisitions could require significant cash commitments and ultimately pressure earnings.

MMMB Stock Price Forecast

We’re bullish on MMMB and see shares trending toward $2.50 as our price target, implying a 35% move higher from the current level, and a 21x multiple on the annualized EPS trend from Q3. This is a level the stock last traded at in Q4 2021 and the argument we have is that the outlook may now be better than ever. We believe MMMB can go significantly higher longer term but will need a few more quarters to confirm the complete financial turnaround is in place.

It’s possible that the significant rally since the Q3 report has already captured much of the positive story meaning some consolidation in the share price around the current level and renewed volatility can be expected in the near term. Within risks, a scenario where economic conditions deteriorate future would likely pressure sales growth and open the door for more downside in the stock. The gross margin and cash flow trends will be important monitoring points through 2023.

To conclude, consider all the warnings and risks of a speculative micro-cap like MMMB, but we believe this one is worth watching with some real meat on the bones.

Seeking Alpha

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment